Global Automotive Vgt Turbocharger Market

Market Size in USD Billion

USD

19.91 Billion

USD

37.26 Billion

2025

2033

USD

19.91 Billion

USD

37.26 Billion

2025

2033

| 2026 - 2033 | |

| USD 19.91 Billion | |

| USD 37.26 Billion | |

| % | |

|

Automotive Variable Geometry Turbocharger (VGT) Market Overview

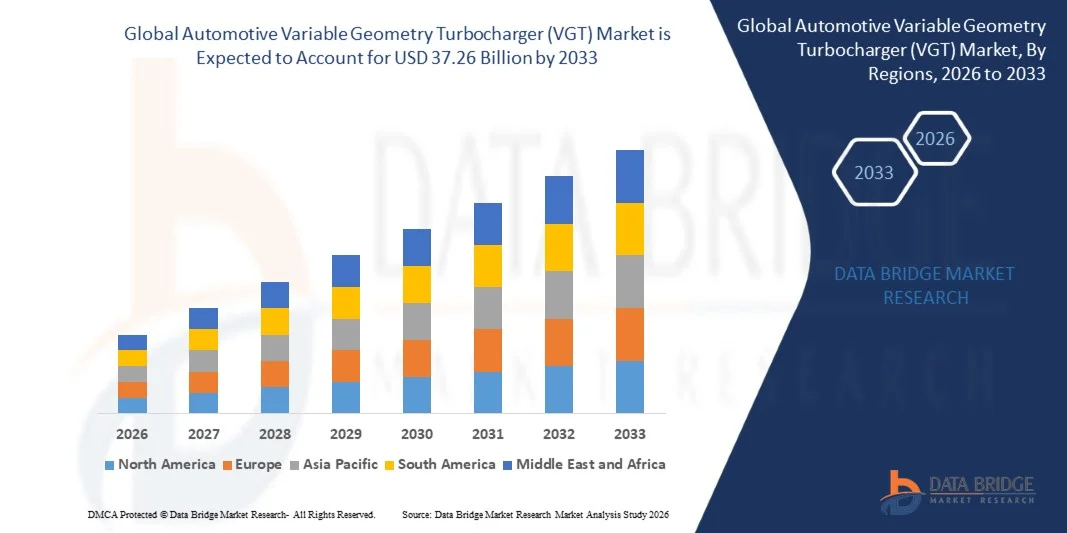

The Automotive Variable Geometry Turbocharger (VGT) Market was valued at USD 19.91 billion in 2025 and is projected to reach USD 37.26 billion by 2033, growing at a CAGR of 8.15% from 2026 to 2033. The market is witnessing strong growth driven by increasing demand for fuel-efficient and high-performance engines, tightening global emission regulations, and rising adoption of turbocharged diesel and gasoline powertrains across passenger and commercial vehicles.

The growing focus of automakers on reducing CO2 emissions while maintaining engine efficiency is significantly boosting the adoption of VGT systems, as they provide improved torque at low engine speeds and enhanced overall engine responsiveness. In addition, advancements in turbocharging technologies, along with increasing penetration of downsized engines in hybrid and internal combustion engine (ICE) vehicles, are further accelerating market expansion across both developed and emerging automotive markets.

Key Market Trends & Insights

- North America dominated the automotive variable geometry turbocharger (VGT) market with the largest revenue share of approximately 34.6% in 2025, supported by strong demand for pickup trucks and heavy-duty commercial vehicles, high adoption of advanced diesel engine technologies, and stringent emission compliance requirements across the transportation and logistics sectors.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 9.1% from 2026 to 2033. Growth is driven by rapid expansion of automotive production, increasing demand for fuel-efficient vehicles, rising industrialization, and strong adoption of turbocharged engines across China, India, and Japan supported by growing logistics and infrastructure development activities.

- The Passenger Cars segment held the largest market revenue share of approximately 46% in 2025 driven by rising adoption of turbocharged downsized engines in SUVs and premium vehicles. VGT systems are widely used in passenger cars to improve fuel efficiency, enhance low-end torque, and reduce turbo lag under urban driving conditions. Increasing consumer preference for high-performance yet fuel-efficient vehicles is further strengthening segment dominance across developed and emerging markets.

- The Heavy Commercial Vehicles (HCV) segment is projected to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing demand for fuel-efficient long-haul transportation and stringent emission regulations across logistics and freight operations. Rising global trade activity and expansion of e-commerce logistics networks are accelerating adoption of advanced turbocharging systems in heavy-duty trucks. In addition, fleet operators are increasingly prioritizing technologies that reduce operational fuel costs and improve engine durability under continuous load conditions.

- The Diesel segment held the largest market revenue share of approximately 58% in 2025 driven by high deployment of VGT systems in commercial vehicles, trucks, and off-highway applications. Diesel engines benefit significantly from VGT technology due to improved combustion efficiency and enhanced torque performance at low engine speeds. Strong penetration of diesel-powered logistics and construction vehicles continues to support demand across global markets.

- The Gasoline segment is projected to register the fastest growth at a CAGR of 10.1% from 2026 to 2033, driven by rising adoption of turbocharged gasoline direct injection (TGDI) engines in passenger cars and hybrid platforms. Increasing regulatory pressure to reduce diesel dependency in certain regions is further accelerating gasoline turbocharging adoption. Automakers are also focusing on engine downsizing strategies that combine VGT systems with hybrid powertrains to achieve better fuel efficiency and lower emissions.

- The Construction Equipment segment held the largest market revenue share of approximately 62% in 2025 driven by extensive use of high-torque diesel engines in excavators, loaders, and bulldozers. VGT systems improve fuel efficiency and operational stability under heavy-load conditions in construction applications. Rapid infrastructure development projects across emerging economies are further boosting equipment demand.

- The Agricultural Tractors segment is projected to grow at the fastest CAGR of 8.8% from 2026 to 2033, supported by increasing mechanization of farming activities and rising demand for fuel-efficient agricultural machinery. Government subsidies for modern farming equipment and growing adoption of precision agriculture practices are also supporting segment expansion. In addition, VGT integration helps improve tractor performance under variable field load conditions, enhancing productivity and fuel savings.

- The Cast Iron segment held the largest market revenue share of approximately 52% in 2025 driven by its high thermal resistance, durability, and ability to withstand extreme exhaust temperatures in heavy-duty engines. Cast iron is widely used in turbine housings and exhaust components due to its cost-effectiveness and long service life. Strong demand from commercial vehicles and industrial applications continues to support this segment.

- The Aluminum segment is projected to register the fastest growth at a CAGR of 9.5% from 2026 to 2033, driven by demand for lightweight materials to improve fuel efficiency and reduce overall vehicle weight in modern automotive platforms. Increasing focus on vehicle lightweighting and emission reduction targets is encouraging OEMs to shift toward aluminum-based turbocharger components. Advancements in high-strength aluminum alloys are also enhancing thermal resistance and performance reliability.

- The Turbine segment held the largest market revenue share of approximately 41% in 2025 driven by its critical role in energy conversion from exhaust gases and direct impact on turbocharger efficiency. Advanced turbine designs in VGT systems enhance responsiveness and performance optimization. Continuous innovation in vane geometry control is further improving engine efficiency across applications.

- The Compressor segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by increasing demand for high-pressure air intake systems in downsized and hybrid engines. Rising focus on improving engine air management efficiency is boosting compressor innovation. Integration of advanced aerodynamic designs is also enhancing boost pressure control and overall engine responsiveness.

- The OEM segment held the largest market revenue share of approximately 73% in 2025 driven by strong integration of VGT systems in new vehicle production across passenger and commercial vehicle platforms. OEMs increasingly prefer factory-fitted turbocharging solutions to meet emission and efficiency standards. Strong partnerships between automakers and turbocharger manufacturers are further strengthening this segment.

- The Aftermarket segment is projected to register the fastest growth at a CAGR of 8.6% from 2026 to 2033, driven by replacement demand, fleet modernization, and rising adoption of performance enhancement upgrades in existing vehicles. Increasing vehicle parc of turbocharged engines is generating steady replacement cycles. In addition, growing interest in engine tuning and efficiency upgrades is further supporting aftermarket expansion.

Market Size & Forecast

- Global Market Value (2025): USD 19.91 Billion

- Expected Market Value (2033): USD 37.26 Billion

- Forecast CAGR (2026–2033): 8.15%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Automotive Variable Geometry Turbocharger (VGT) Market Segmentation

|

Attributes |

Automotive Variable Geometry Turbocharger (VGT) Key Market Insights |

|

Segments Covered |

· By Vehicle Type: Passenger Cars, Light Commercial Vehicles (LCV), and Heavy Commercial Vehicle (HCV) · By Fuel Type: Diesel, Gasoline, and Alternate Fuel/CNG · By End Use: Agricultural tractors and Construction Equipment · By Material: Cast Iron, Aluminum, and Other Materials · By Component: Turbine, Compressor, and Housing · By Sales Channel: OEMs and Aftermarket |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Honeywell International Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Variable Geometry Turbocharger (VGT) Market Trends

Trend: Increasing Adoption Of Variable Geometry Turbocharging In Downsized And Hybrid Engines

Rising demand for fuel-efficient, high-performance, and low-emission powertrains across automotive segments is accelerating the adoption of variable geometry turbocharger (VGT) systems. Unlike fixed geometry turbochargers, VGTs adjust turbine vane angles dynamically, improving boost response, reducing turbo lag, and enhancing overall engine efficiency under varying load conditions. Increasingly stringent emission regulations such as Euro 6 and upcoming Euro 7 standards are pushing OEMs toward advanced turbocharging solutions that optimize combustion efficiency while lowering CO2 and NOx emissions.

In modern passenger vehicles, manufacturers are integrating VGT systems in diesel and gasoline engines, For instance in SUVs and light commercial vehicles, to improve low-end torque delivery and drivability without increasing engine displacement. In heavy-duty commercial vehicles, VGTs are widely used to enhance engine braking performance and maintain efficiency under long-haul operating conditions, improving fuel economy by nearly 5–10% in optimized engine configurations. In addition, hybrid powertrains are increasingly combining VGT-equipped ICE units with electric motors to achieve better thermal efficiency and power balancing. Real-world deployments across European OEM platforms in 2024 demonstrated measurable reductions in turbo lag by nearly 30–40% under city driving cycles, improving acceleration response and drivability consistency.

Automotive Variable Geometry Turbocharger (VGT) Market Dynamics

Key Market Driver: Rising Demand For Fuel Efficiency And Emission-CompliantEngines

Automotive manufacturers globally are under increasing regulatory and economic pressure to improve fuel efficiency and reduce greenhouse gas emissions, driving strong adoption of advanced turbocharging technologies such as VGT systems. These systems enhance air intake control and optimize combustion efficiency, enabling smaller engines to deliver higher power output while consuming less fuel.

Automotive OEMs are increasingly deploying VGT technology in diesel passenger cars, commercial trucks, and off-highway vehicles, For instance in long-haul freight transport, to improve fuel economy and reduce operational costs per kilometer. The growing trend of engine downsizing, combined with stricter emission norms such as BS6 Phase 2 in India and China 6 standards, is further accelerating demand. In heavy-duty diesel engines used in logistics fleets, VGT integration has demonstrated fuel efficiency improvements of approximately 6–12% depending on driving cycles and load conditions in real-world testing environments conducted across North America and Europe in 2025.

Key Restraint/Challenge: High System Complexity And Maintenance Sensitivity

Variable geometry turbochargers involve complex vane mechanisms and precision actuation systems, making them more expensive to manufacture compared to conventional fixed turbochargers. The requirement for high-temperature-resistant materials and precise electronic control systems increases production costs and limits adoption in low-cost vehicle segments.

In addition, VGT systems are more sensitive to soot accumulation and exhaust gas contamination, which can lead to reduced efficiency or mechanical sticking of vanes over time, particularly in diesel applications with frequent short-trip usage patterns. Maintenance and repair costs are also higher due to specialized components and calibration requirements. Industry assessments indicate that VGT units can increase overall turbocharging system cost by approximately 20–35% compared to fixed geometry turbochargers, creating affordability challenges in price-sensitive emerging markets.

Key Market Opportunity: Expansion In Hybrid Vehicles And Advanced Engine Platforms

The growing shift toward hybridization and advanced internal combustion engine optimization is creating significant opportunities for VGT integration across next-generation powertrains. Hybrid electric vehicles increasingly rely on compact, high-efficiency ICE units that require optimized turbocharging to maintain performance while reducing emissions and fuel consumption.

Automotive manufacturers are increasingly deploying VGT systems in hybrid SUVs and performance-oriented vehicles, For instance in plug-in hybrid electric vehicle (PHEV) platforms, to enhance engine responsiveness during charge-sustaining modes. In addition, advancements in electronic actuation and smart turbo control systems are improving precision and durability, enabling wider adoption across global automotive platforms. Pilot fleet data from 2025 in Japan and Germany indicates that hybrid vehicles equipped with VGT-assisted engines achieved up to 8–14% improvement in combined-cycle fuel efficiency and smoother torque delivery under variable load conditions.

Automotive Variable Geometry Turbocharger (VGT) Market Scope

The market is segmented on the basis of vehicle type, fuel type, end use, material, component, and sales channel.

- By Vehicle Type

On the basis of vehicle type, the Automotive Variable Geometry Turbocharger (VGT) Market is segmented into Passenger Cars, Light Commercial Vehicles (LCV), and Heavy Commercial Vehicles (HCV). The Passenger Cars segment held the largest market revenue share of approximately 46% in 2025 driven by rising adoption of turbocharged downsized engines in SUVs and premium vehicles. VGT systems are widely used in passenger cars to improve fuel efficiency, enhance low-end torque, and reduce turbo lag under urban driving conditions. Increasing consumer preference for high-performance yet fuel-efficient vehicles is further strengthening segment dominance across developed and emerging markets.

The Heavy Commercial Vehicles (HCV) segment is projected to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing demand for fuel-efficient long-haul transportation and stringent emission regulations across logistics and freight operations. Rising global trade activity and expansion of e-commerce logistics networks are accelerating adoption of advanced turbocharging systems in heavy-duty trucks. In addition, fleet operators are increasingly prioritizing technologies that reduce operational fuel costs and improve engine durability under continuous load conditions.

- By Fuel Type

On the basis of fuel type, the market is segmented into Diesel, Gasoline, and Alternate Fuel/CNG. The Diesel segment held the largest market revenue share of approximately 58% in 2025 driven by high deployment of VGT systems in commercial vehicles, trucks, and off-highway applications. Diesel engines benefit significantly from VGT technology due to improved combustion efficiency and enhanced torque performance at low engine speeds. Strong penetration of diesel-powered logistics and construction vehicles continues to support demand across global markets.

The Gasoline segment is projected to register the fastest growth at a CAGR of 10.1% from 2026 to 2033, driven by rising adoption of turbocharged gasoline direct injection (TGDI) engines in passenger cars and hybrid platforms. Increasing regulatory pressure to reduce diesel dependency in certain regions is further accelerating gasoline turbocharging adoption. Automakers are also focusing on engine downsizing strategies that combine VGT systems with hybrid powertrains to achieve better fuel efficiency and lower emissions.

- By End Use

On the basis of end use, the market is segmented into Agricultural Tractors and Construction Equipment. The Construction Equipment segment held the largest market revenue share of approximately 62% in 2025 driven by extensive use of high-torque diesel engines in excavators, loaders, and bulldozers. VGT systems improve fuel efficiency and operational stability under heavy-load conditions in construction applications. Rapid infrastructure development projects across emerging economies are further boosting equipment demand.

The Agricultural Tractors segment is projected to grow at the fastest CAGR of 8.8% from 2026 to 2033, supported by increasing mechanization of farming activities and rising demand for fuel-efficient agricultural machinery. Government subsidies for modern farming equipment and growing adoption of precision agriculture practices are also supporting segment expansion. In addition, VGT integration helps improve tractor performance under variable field load conditions, enhancing productivity and fuel savings.

- By Material

On the basis of material, the market is segmented into Cast Iron, Aluminum, and Other Materials. The Cast Iron segment held the largest market revenue share of approximately 52% in 2025 driven by its high thermal resistance, durability, and ability to withstand extreme exhaust temperatures in heavy-duty engines. Cast iron is widely used in turbine housings and exhaust components due to its cost-effectiveness and long service life. Strong demand from commercial vehicles and industrial applications continues to support this segment.

The Aluminum segment is projected to register the fastest growth at a CAGR of 9.5% from 2026 to 2033, driven by demand for lightweight materials to improve fuel efficiency and reduce overall vehicle weight in modern automotive platforms. Increasing focus on vehicle lightweighting and emission reduction targets is encouraging OEMs to shift toward aluminum-based turbocharger components. Advancements in high-strength aluminum alloys are also enhancing thermal resistance and performance reliability.

- By Component

On the basis of component, the market is segmented into Turbine, Compressor, and Housing. The Turbine segment held the largest market revenue share of approximately 41% in 2025 driven by its critical role in energy conversion from exhaust gases and direct impact on turbocharger efficiency. Advanced turbine designs in VGT systems enhance responsiveness and performance optimization. Continuous innovation in vane geometry control is further improving engine efficiency across applications.

The Compressor segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by increasing demand for high-pressure air intake systems in downsized and hybrid engines. Rising focus on improving engine air management efficiency is boosting compressor innovation. Integration of advanced aerodynamic designs is also enhancing boost pressure control and overall engine responsiveness.

- By Sales Channel

On the basis of sales channel, the market is segmented into OEMs and Aftermarket. The OEM segment held the largest market revenue share of approximately 73% in 2025 driven by strong integration of VGT systems in new vehicle production across passenger and commercial vehicle platforms. OEMs increasingly prefer factory-fitted turbocharging solutions to meet emission and efficiency standards. Strong partnerships between automakers and turbocharger manufacturers are further strengthening this segment.

The Aftermarket segment is projected to register the fastest growth at a CAGR of 8.6% from 2026 to 2033, driven by replacement demand, fleet modernization, and rising adoption of performance enhancement upgrades in existing vehicles. Increasing vehicle parc of turbocharged engines is generating steady replacement cycles. In addition, growing interest in engine tuning and efficiency upgrades is further supporting aftermarket expansion.

Automotive Variable Geometry Turbocharger (VGT) Market Regional Analysis

North America Automotive Variable Geometry Turbocharger (VGT) Market Insight

North America dominated the automotive variable geometry turbocharger (VGT) market with the largest revenue share of approximately 34.6% in 2025, supported by strong demand for fuel-efficient commercial vehicles, advanced pickup trucks, and stringent emission regulations. The region benefits from high adoption of turbocharged diesel engines in heavy-duty applications and increasing integration of advanced engine technologies across automotive OEM platforms. Strong presence of leading automotive manufacturers and continuous investment in engine downsizing and emission reduction technologies are further strengthening regional market dominance.

U.S. Automotive Variable Geometry Turbocharger (VGT) Market Insight

The U.S. automotive VGT market captured the largest revenue share in 2025 within North America, driven by strong demand for high-performance pickup trucks, SUVs, and commercial freight vehicles. The growing focus on fuel efficiency improvements and compliance with emission standards such as EPA regulations is accelerating adoption of VGT systems. In addition, increasing deployment of turbocharged engines in hybrid powertrains and fleet modernization initiatives across logistics operators is further boosting market expansion in the country.

Europe Automotive Variable Geometry Turbocharger (VGT) Market Insight

The Europe automotive VGT market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent emission norms such as Euro 7 standards and strong emphasis on vehicle electrification and hybridization. The region is witnessing rising adoption of advanced turbocharging technologies in passenger cars and commercial vehicles to achieve lower CO2 emissions. Increasing investment in sustainable mobility solutions and engine optimization technologies is further supporting rapid market expansion across major automotive manufacturing countries.

U.K. Automotive Variable Geometry Turbocharger (VGT) Market Insight

The U.K. automotive VGT market is expected to witness steady growth from 2026 to 2033, driven by rising demand for fuel-efficient vehicles and increasing adoption of hybrid powertrains. Concerns regarding carbon emissions and government initiatives promoting cleaner transportation are encouraging OEMs to integrate advanced turbocharging systems. In addition, the strong presence of automotive R&D facilities and increasing focus on performance-oriented engine technologies are supporting market growth across passenger and commercial vehicle segments.

Germany Automotive Variable Geometry Turbocharger (VGT) Market Insight

The Germany automotive VGT market is expected to witness strong growth from 2026 to 2033, fueled by the country’s leading automotive manufacturing base and strong emphasis on engineering innovation. Increasing integration of turbocharged downsized engines in premium vehicles is driving demand for VGT systems. Germany’s focus on hybrid vehicle development and compliance with strict emission regulations is further accelerating adoption of advanced turbocharging technologies across passenger cars and industrial vehicle platforms.

Asia-Pacific Automotive Variable Geometry Turbocharger (VGT) Market Insight

The Asia-Pacific automotive VGT market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding automotive production, and increasing demand for fuel-efficient vehicles. Countries such as China, India, and Japan are witnessing strong adoption of turbocharged engines across passenger and commercial vehicle segments. Growing investments in infrastructure development, rising vehicle ownership, and expansion of logistics networks are further boosting demand for VGT systems in the region.

Japan Automotive Variable Geometry Turbocharger (VGT) Market Insight

The Japan automotive VGT market is expected to witness steady growth from 2026 to 2033, driven by strong demand for advanced automotive technologies, hybrid vehicles, and fuel-efficient engine systems. Japan’s focus on precision engineering and environmental sustainability is encouraging adoption of VGT systems in both passenger and commercial vehicles. Increasing integration of turbocharging systems in hybrid powertrains and compact vehicle platforms is further supporting market growth across the automotive sector.

China Automotive Variable Geometry Turbocharger (VGT) Market Insight

The China automotive VGT market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid automotive production growth, strong demand for commercial vehicles, and increasing focus on emission reduction technologies. China’s expanding middle class and large-scale logistics sector are driving adoption of turbocharged diesel and gasoline engines. In addition, government initiatives supporting cleaner mobility and strong domestic automotive manufacturing capabilities are further accelerating market expansion across passenger and commercial vehicle applications.

Automotive Variable Geometry Turbocharger (VGT) Market Share

The Automotive Variable Geometry Turbocharger (VGT) industry is primarily led by well-established companies, including:

• Honeywell International Inc. (U.S.)

• Continental AG (Germany)

• BorgWarner Turbo Systems (U.S.)

• MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan)

• IHI America (U.S.)

• BMTS TECHNOLOGY (Germany)

• Cummins Inc. (U.S.)

• ABB (Switzerland)

• Delphi Auto Parts (U.K.)

• Rotomaster International (Canada)

• Precision Turbo & Engine (U.S.)

• Turbonetics, Inc. (U.S.)

• Kompressorenbau Bannewitz GmbH (Germany)

• Turbo Dynamics (U.K.)

• Weifang FuYuan Turbochargers Co., Ltd (China)

Latest Developments in Automotive Variable Geometry Turbocharger (VGT) Market

- In September 2024, BorgWarner (U.S.) expanded its manufacturing footprint by establishing a new production facility in Mexico focused on variable geometry turbochargers, aimed at increasing output capacity for North American demand. This development strengthens supply chain efficiency, reduces lead times, and lowers production costs, thereby enhancing BorgWarner’s competitiveness in the regional VGT market and supporting growing demand from commercial and passenger vehicle OEMs

- In August 2024, Honeywell (U.S.) entered a strategic partnership with a leading electric vehicle manufacturer to develop next-generation turbochargers optimized for hybrid vehicle applications. The initiative is designed to improve engine efficiency, support hybrid powertrain performance, and align with global electrification trends. This collaboration is expected to strengthen Honeywell’s positioning in the hybrid mobility segment while expanding its advanced automotive turbocharging portfolio

- In July 2024, Garrett Motion (U.S.) launched a new range of turbochargers utilizing advanced ceramic materials engineered for high-temperature resistance and improved thermal efficiency. This innovation enhances durability, reduces energy losses, and improves overall engine performance in high-load applications. The development supports the industry’s shift toward lightweight and high-efficiency materials, strengthening Garrett Motion’s competitiveness in performance and next-generation turbocharging solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.