Global Autonomous Farm Equipment Agricultural Robots Market

Market Size in USD Billion

USD

20.20 Billion

USD

50.01 Billion

2025

2033

USD

20.20 Billion

USD

50.01 Billion

2025

2033

| 2026 - 2033 | |

| USD 20.20 Billion | |

| USD 50.01 Billion | |

| % | |

|

What is the Autonomous Farm Equipment (Agricultural Robots) Market Size and Growth Rate?

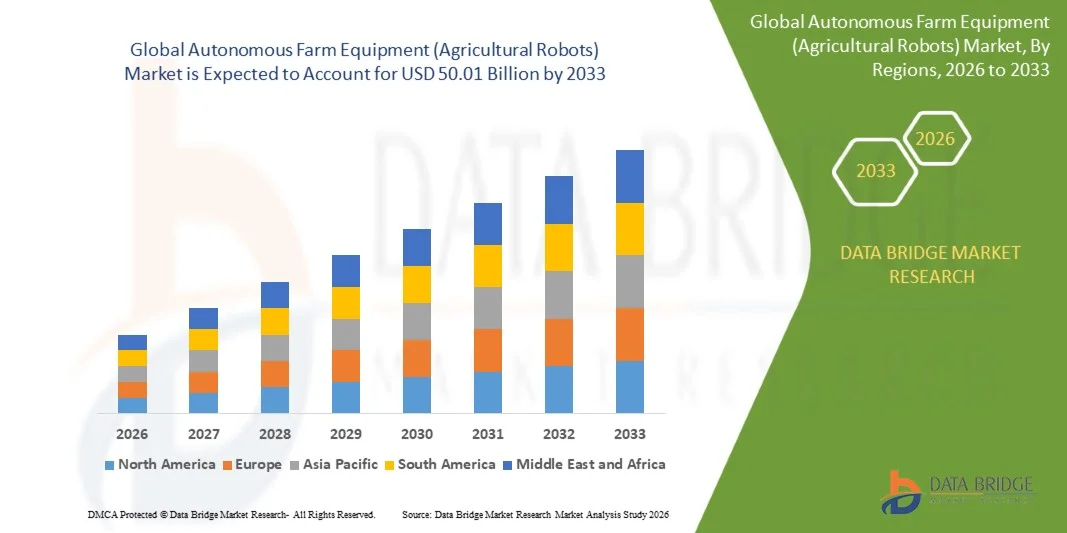

- The Autonomous Farm Equipment (Agricultural Robots) Market size was valued at USD 20.20 billion in 2025 and is expected to reach USD 50.01 billion by 2033, at a CAGR of 12.00% during the forecast period

- Rising adoption of automation in agriculture, increasing labor shortages, demand for precision farming, growing use of driverless tractors, UAVs, and dairy robots, and technological advancements in hardware, software, and services are key factors driving market growth

- Expansion of smart farming practices, integration of IoT and AI for monitoring, surveillance, and yield optimization, and increasing government initiatives supporting sustainable agriculture further fuel market development

What are the Major Takeaways of Autonomous Farm Equipment (Agricultural Robots) Market?

- Increasing deployment of advanced agricultural robots for planting, spraying, harvesting, and livestock monitoring across developed and emerging economies is creating massive growth opportunities for the market

- High initial investment, maintenance complexities, and lack of skilled personnel for operating advanced farm robots may act as restraints, potentially slowing adoption in smaller farms or developing regions

- North America dominated the autonomous farm equipment market with an estimated 43.3% revenue share in 2025, driven by early adoption of precision agriculture, large-scale commercial farming, and strong investments in agri-technology across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of around 7.32% from 2026 to 2033, driven by rising food demand, labor shortages in rural areas, and rapid modernization of agriculture across China, Japan, India, South Korea, and Southeast Asia

- The Planting & Seeding Management segment dominated the market with a 32.5% share in 2025, driven by the widespread adoption of precision agriculture practices, automated sowing technologies, and GPS-guided seed placement systems

Report Scope and Autonomous Farm Equipment (Agricultural Robots) Market Segmentation

|

Attributes |

Autonomous Farm Equipment (Agricultural Robots) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Autonomous Farm Equipment (Agricultural Robots) Market?

“Rising Adoption of AI-Driven, Sensor-Integrated, and Autonomous Machinery for Precision Agriculture”

- The autonomous farm equipment market is witnessing rapid uptake of AI-enabled, GPS-guided, and sensor-integrated machinery designed for precision planting, automated harvesting, livestock monitoring, and real-time farm decision-making

- Leading manufacturers are introducing self-driving tractors, robotic harvesters, UAV crop sprayers, and automated milking systems equipped with LiDAR, computer vision, AI algorithms, and cloud connectivity for fleet management

- Increasing demand for labor-efficient, fuel-optimized, and data-driven farming operations is driving deployments across commercial farms, large-scale agricultural estates, and smart farming initiatives

- For instance, companies such as Deere & Company (U.S.), CNH Industrial (U.K.), AGCO (U.S.), Kubota (Japan), and Autonomous Tractor Corporation (U.S.) are advancing autonomous platforms with predictive maintenance, remote monitoring, and safety features

- The need for round-the-clock operations, precise input application, and optimized crop yield is accelerating the shift toward semi- and fully autonomous farm solutions

- As agriculture becomes more data-intensive and sustainability-focused, autonomous farm equipment will remain central to modern, high-efficiency farming ecosystems

What are the Key Drivers of Autonomous Farm Equipment (Agricultural Robots) Market?

- Rising labor shortages, increasing wages, and the need to reduce workforce dependency in agriculture are major drivers of autonomous equipment adoption

- For instance, in 2024–2025, leading OEMs such as John Deere, CNH Industrial, and AGCO expanded their autonomous product portfolios with AI-based navigation, precision planting, and fleet management solution

- Growing adoption of precision farming, IoT-enabled sensors, and smart agriculture platforms across North America, Europe, and Asia-Pacific is boosting market demand

- Advancements in GPS accuracy, edge computing, computer vision, AI-based crop analytics, and cloud-based monitoring have enhanced operational reliability and efficiency

- Increasing focus on sustainable farming, optimized resource usage, and higher crop yields encourages greater investment in autonomous farm machinery

- Supported by government subsidies, digital agriculture initiatives, and agritech innovation programs, the autonomous farm equipment market is expected to witness robust long-term growth

Which Factor is Challenging the Growth of the Autonomous Farm Equipment (Agricultural Robots) Market?

- High costs of AI sensors, autonomous control systems, robotic hardware, and safety technologies limit adoption among smallholder and medium-sized farms

- For instance, in 2024–2025, rising semiconductor prices and global supply chain disruptions increased production costs for autonomous machinery

- Complexity in system integration, maintenance, and real-time decision-making algorithms increases dependency on skilled operators and technician training

- Limited digital infrastructure and low awareness of autonomous farming benefits in emerging economies slow market penetration

- Regulatory uncertainties regarding autonomous vehicle operation, safety compliance, and liability create adoption challenges

- To address these barriers, manufacturers are focusing on cost-effective autonomous platforms, scalable solutions, farmer training programs, and integrated software-hardware systems to expand global adoption of autonomous farm equipment

How is the Autonomous Farm Equipment (Agricultural Robots) Market Segmented?

The market is segmented on the basis of application, type, and offering.

• By Application

On the basis of application, the autonomous farm equipment (agricultural robots) market is segmented into Planting & Seeding Management, Spraying Management, Milking, Monitoring & Surveillance, Harvest Management, Livestock Monitoring, and Others. The Planting & Seeding Management segment dominated the market with a 32.5% share in 2025, driven by the widespread adoption of precision agriculture practices, automated sowing technologies, and GPS-guided seed placement systems. These solutions enhance crop yield, reduce labor requirements, and optimize field efficiency, making them highly preferred among commercial farms and large-scale agricultural operations.

The Harvest Management segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing demand for automated harvesting machines, robotic crop pickers, and yield monitoring systems that reduce post-harvest losses and improve operational productivity across global farms.

• By Type

On the basis of type, the market is segmented into Driverless Tractors, UAVs, Dairy Robots, and Material Management. The Driverless Tractors segment dominated the market with a 38.7% share in 2025, supported by their versatility in performing tillage, plowing, planting, and field maintenance with minimal human intervention. Their integration with GPS, IoT, and AI technologies enables precise field operations, improving fuel efficiency and reducing labor costs, which drives adoption in developed and emerging regions.

The UAVs segment is expected to register the fastest CAGR from 2026 to 2033, driven by rising utilization in crop monitoring, spraying, and aerial surveillance. UAVs provide high-resolution imaging, real-time data collection, and actionable insights for precision farming, making them essential tools for smart agriculture and resource optimization.

• By Offering

On the basis of offering, the market is segmented into Hardware, Software, and Services. The Hardware segment dominated the market with a 41.2% share in 2025, attributed to the growing deployment of autonomous tractors, robotic harvesters, milking machines, and sensor-enabled farm machinery. Advanced hardware ensures durability, reliability, and real-time operation under diverse agricultural conditions, which makes it the core component of autonomous farming solutions.

The Software segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by the increasing demand for farm management platforms, AI-based crop analytics, data-driven decision support, and precision agriculture solutions. Software offerings enable seamless integration of machinery, monitoring systems, and analytics platforms, optimizing farm productivity and reducing operational costs across smallholder and commercial farms.

Which Region Holds the Largest Share of the Autonomous Farm Equipment (Agricultural Robots) Market?

- North America dominated the autonomous farm equipment market with an estimated 43.3% revenue share in 2025, driven by early adoption of precision agriculture, large-scale commercial farming, and strong investments in agri-technology across the U.S. and Canada. High labor costs, farm consolidation, and increasing focus on productivity optimization have accelerated adoption of autonomous tractors, harvesters, and robotic field equipment

- Leading manufacturers and agri-tech companies in North America are actively deploying AI-enabled guidance systems, GPS-based navigation, machine vision, and telematics platforms, strengthening the region’s technological leadership

- Strong availability of skilled workforce, supportive regulatory pilots, and continuous investments in smart farming infrastructure further reinforce North America’s dominance

U.S. Autonomous Farm Equipment (Agricultural Robots) Market Insight

The U.S. is the largest contributor within North America, supported by large farm sizes, acute labor shortages, and rapid adoption of precision farming technologies. Increasing use of autonomous tractors, robotic harvesters, and UAVs for planting, spraying, and yield monitoring is driving market growth. Strong presence of global OEMs, agri-startups, and advanced R&D ecosystems further accelerates adoption.

Canada Autonomous Farm Equipment (Agricultural Robots) Market Insight

Canada contributes significantly, driven by mechanized farming practices, growing adoption of smart agriculture, and government support for agri-innovation. Autonomous equipment is increasingly used to improve efficiency in large grain and oilseed farms, supporting steady market expansion.

Asia-Pacific Autonomous Farm Equipment (Agricultural Robots) Market

Asia-Pacific is projected to register the fastest CAGR of around 7.32% from 2026 to 2033, driven by rising food demand, labor shortages in rural areas, and rapid modernization of agriculture across China, Japan, India, South Korea, and Southeast Asia. Increasing adoption of smart farming, government subsidies for mechanization, and growing use of AI- and IoT-enabled agricultural equipment are accelerating regional growth.

China Autonomous Farm Equipment (Agricultural Robots) Market Insight

China leads the region due to strong government support for agricultural modernization, rapid deployment of smart tractors and drones, and large-scale investments in agri-robotics. China’s growth is supported by advanced robotics capabilities, smart farming programs, and strong integration of AI and automation technologies.

Which are the Top Companies in Autonomous Farm Equipment (Agricultural Robots) Market?

The autonomous farm equipment (agricultural robots) industry is primarily led by well-established companies, including:

- Deere & Company (U.S.)

- CNH Industrial N.V. (Netherlands)

- KUBOTA Corporation (Japan)

- AGCO Corporation (U.S.)

- JCB (U.K.)

- Trringo (India)

- Escorts Limited (India)

- Tractors and Farm Equipment Limited (India)

- The Papé Group, Inc. (U.S.)

- Premier Equipment Limited (Canada)

- Flaman (Canada)

- Pacific Ag Rentals (Canada)

- Pacific Tractor & Implement (U.S.)

- Farmease (India)

- KWIPPED, Inc. (U.S.)

- Cedar Street (U.S.)

- EM3 Agri Services (India)

- Princeville (U.S.)

- Friesen Sales & Rentals (Canada)

- Messick's (U.S.)

- Autonomous Tractor Corporation (U.S.)

What are the Recent Developments in Autonomous Farm Equipment (Agricultural Robots) Market?

- In November 2025, Claas showcased its advanced TORION Autonomy Connect system at Agritechnica, featuring an autonomous wheel loader powered by LiDAR sensors and AI-based pile analysis for GPS-independent silage handling, alongside the launch of the Weed Detector system for real-time weed mapping and the Dynamic Field Scout combining RTK positioning with AI imaging for accurate field boundary detection, highlighting Claas’s focus on precision, efficiency, and next-generation autonomous farming solutions

- In May 2025, Case IH revealed a concept autonomous tractor incorporating advanced AI algorithms, radar-based obstacle detection, and remote operation functionality, designed to perform essential tasks such as tillage and planting with high efficiency, underscoring the company’s vision for the future of precision-driven and intelligent agriculture

- In January 2025, at CES, John Deere introduced its next-generation autonomous machinery portfolio led by the autonomous 9RX tractor, engineered for large-scale tillage and equipped with 360-degree perception using 12 stereo cameras, LiDAR sensors, and AI-powered obstacle detection, reinforcing John Deere’s leadership in large-farm automation and smart equipment innovation

- In January 2025, Kubota made a strong presence at CES by unveiling multiple autonomous innovations, including the Agri Concept 2.0 electric tractor with GPS guidance and remote mission planning, a smart autonomous sprayer with AI-based spot treatment, a multifunctional robotic cart, and robotic orchard pruners, demonstrating Kubota’s comprehensive approach to advancing sustainable, automated, and technology-driven agriculture

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.