Global Autonomous Surgical Robotics Market

Market Size in USD Billion

USD

1.59 Billion

USD

4.48 Billion

2024

2032

USD

1.59 Billion

USD

4.48 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.59 Billion | |

| USD 4.48 Billion | |

| % | |

|

Autonomous Surgical Robotics Market Size

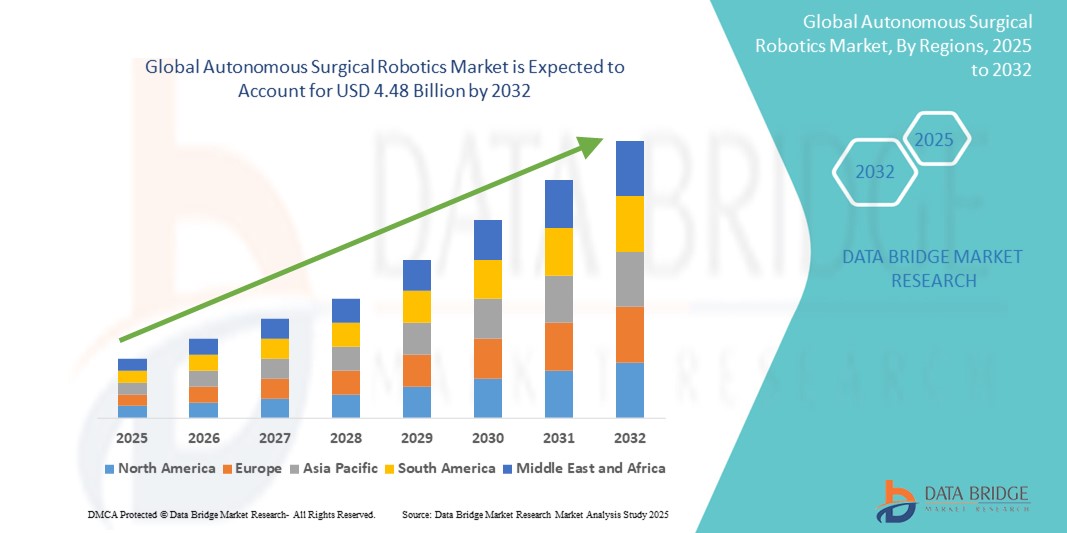

- The global autonomous surgical robotics market size was valued at USD 1.59 billion in 2024 and is expected to reach USD 4.48 billion by 2032, at a CAGR of 13.80% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within surgical automation and robotic-assisted procedures, leading to increased digitalization in both operating rooms and outpatient surgical settings

- Furthermore, rising demand for precise, minimally invasive, and AI-integrated surgical solutions is establishing autonomous surgical robotics as the next-generation advancement in surgical technology. These converging factors are accelerating the uptake of Autonomous Surgical Robotics solutions, thereby significantly boosting the industry's growth

Autonomous Surgical Robotics Market Analysis

- Autonomous surgical robotics, which utilize advanced imaging, AI-driven navigation, and robotic precision to perform minimally invasive procedures with minimal human intervention, are becoming increasingly vital in modern operating rooms. These systems enhance surgical accuracy, reduce complications, shorten recovery times, and enable complex procedures in hard-to-access anatomical areas

- The growing demand for autonomous surgical robotic systems is primarily fueled by the rising prevalence of chronic diseases requiring surgery, increasing adoption of minimally invasive techniques, technological advancements in AI and machine learning, and a global shortage of skilled surgeons

- North America dominated the autonomous surgical robotics market with the largest revenue share of 42.5% in 2024, driven by early adoption of robotic surgery platforms, well-established healthcare infrastructure, favorable reimbursement policies, and strong presence of major players such as Intuitive Surgical, Medtronic, and Johnson & Johnson. The U.S. leads the regional market, with widespread installations across tertiary hospitals and surgical centers and rapid integration of AI-guided decision support tools

- Asia-Pacific is expected to be the fastest growing region in the autonomous surgical robotics market during the forecast period, projected to grow at a CAGR of 19.3% from 2025 to 2032, due to increasing healthcare investments, rising medical tourism, improving surgical infrastructure, and growing demand for precision surgical interventions in populous nations such as China and India

- The surgical systems segment dominated the autonomous surgical robotics market with largest market revenue share of 58.3% in 2024, driven by rising demand for fully integrated robotic platforms that perform surgical tasks with minimal human intervention. These systems offer precise control, reduced trauma, and quicker recovery times, which contribute to improved patient outcomes and hospital cost efficiency

Report Scope and Autonomous Surgical Robotics Market Segmentation

|

Attributes |

Autonomous Surgical Robotics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Autonomous Surgical Robotics Market Trends

“Advancements in Intelligent System Capabilities and Surgical Precision”

- A significant and accelerating trend in the global autonomous surgical robotics market is the integration of advanced artificial intelligence (AI), machine learning, and real-time data analytics into robotic-assisted surgical platforms. These technologies are enhancing surgical planning, intraoperative decision-making, and procedural execution, enabling greater precision, safety, and personalization in minimally invasive surgeries

- For instance, leading platforms such as Medtronic’s Hugo RAS system and CMR Surgical’s Versius system are equipped with AI-powered modules that assist surgeons with real-time anatomical mapping, instrument trajectory adjustments, and automatic safety protocols. These features significantly reduce the margin for human error and improve patient outcomes

- AI integration in robotic systems enables the continuous learning of surgical patterns, predictive analytics for complication prevention, and post-surgical data analysis to optimize future interventions. Some systems can autonomously identify anatomical landmarks, assess tissue response, and guide tools accordingly, thereby minimizing reliance on manual control during critical phases of surgery

- These intelligent surgical platforms are also increasingly incorporating natural language processing (NLP) capabilities, allowing surgeons to interact with robotic systems through hands-free, voice-based commands during procedures. This reduces workflow interruptions and enhances focus during complex operations

- Moreover, the integration of autonomous robotics with hospital-wide electronic health records (EHR) and imaging systems enables preoperative data import and postoperative outcome tracking, creating a more streamlined and connected surgical ecosystem

- The growing demand for highly automated, AI-enhanced robotic surgical platforms is rapidly transforming operating rooms across both developed and emerging healthcare systems. Hospitals and surgical centers are prioritizing technologies that reduce procedure time, improve accuracy, and lower complication rates—fueling sustained market growth for autonomous surgical robotics

Autonomous Surgical Robotics Market Dynamics

Driver

“Growing Need Due to Rising Surgical Demand and Technological Advancements”

- The increasing prevalence of chronic diseases and the global rise in the aging population are significantly driving the demand for advanced surgical procedures. In response, the adoption of autonomous surgical robotics is accelerating as healthcare systems seek precision, consistency, and improved outcomes in surgery

- For instance, in April 2024, Intuitive Surgical unveiled updates to its da Vinci system incorporating AI-based enhancements aimed at improving autonomous maneuvering during complex procedures. Such strategic innovations by key companies are expected to drive the Autonomous Surgical Robotics industry growth in the forecast period

- As hospitals and surgical centers focus on reducing operative times, enhancing surgical accuracy, and improving patient safety, autonomous surgical robots offer superior capabilities such as real-time analytics, enhanced visualization, and automated tool control, providing a compelling upgrade over traditional manual surgeries

- Furthermore, the growing popularity of minimally invasive surgery and the demand for shorter hospital stays are making autonomous robots a central component in modern operating rooms, with seamless integration into hospital IT systems, AI-based decision-making, and remote-control options

- The convenience of robotic precision, lower risk of complications, reduced surgeon fatigue, and the ability to support training via simulation platforms are key factors propelling the adoption of autonomous surgical robotics across general, orthopedic, cardiovascular, and neurosurgical procedures. The trend toward outpatient robotic surgeries and the increasing availability of modular, user-friendly robotic systems further contributes to market growth

Restraint/Challenge

“Concerns Regarding High Initial Costs and Data Security”

- The high upfront cost of robotic surgical systems, along with the expense of maintenance, training, and required infrastructure upgrades, continues to be a major barrier to widespread adoption—especially in developing and budget-constrained healthcare markets

- For instance, the average cost of installing an advanced surgical robotic suite can exceed USD 2 million, making ROI a critical consideration for smaller hospitals and ambulatory surgical centers

- Furthermore, cybersecurity concerns surrounding connected robotic devices—such as potential hacking, data breaches, or AI manipulation—pose growing risks. As surgical robots increasingly rely on network connectivity and cloud-based analytics, protecting patient data and surgical protocols becomes paramount

- Addressing these challenges through robust data encryption, secure software architectures, frequent system updates, and compliance with international health IT security standards (e.g., HIPAA, GDPR) is essential to build stakeholder confidence.

- Companies such as Stryker, Medtronic, and Johnson & Johnson are investing heavily in improving both the affordability and security of their autonomous systems, offering scalable models and cybersecurity-embedded platforms

- Overcoming these hurdles through innovations in cost-effective robot-as-a-service (RaaS) models, expanding surgeon training programs, and increasing awareness of clinical benefits will be vital for sustained growth in the autonomous surgical robotics market

Autonomous Surgical Robotics Market Scope

The market is segmented on the basis of type, application, and end user.

- By Type

On the basis of type, the autonomous surgical robotics market is segmented into surgical systems, instruments and accessories, and services. The surgical systems segment dominated the largest market revenue share of 58.3% in 2024, driven by rising demand for fully integrated robotic platforms that perform surgical tasks with minimal human intervention. These systems offer precise control, reduced trauma, and quicker recovery times, which contribute to improved patient outcomes and hospital cost efficiency.

The services segment is expected to witness the fastest CAGR of 18.9% from 2025 to 2032, due to the growing need for maintenance, software updates, training, and technical support. As hospitals expand their robotic infrastructure, demand for support services to ensure uptime and optimal performance is increasing rapidly.

- By Application

On the basis of application, the autonomous surgical robotics market is segmented into general surgery, urology surgery, gynecology surgery, orthopedic surgery, cardiology surgery, head and neck (including neurology) surgery, and other surgeries. The orthopedic surgery segment accounted for the largest market revenue share of 31.6% in 2024, driven by the increasing prevalence of joint disorders and the high success rates associated with robotic-assisted joint replacements. Robotic systems allow for better alignment and implant positioning, leading to improved surgical precision and reduced recovery times.

The gynecology surgery segment is expected to register the fastest CAGR of 17.4% during the forecast period, supported by the growing demand for minimally invasive hysterectomy and myomectomy procedures, especially in developed markets.

- By End User

On the basis of end user, the autonomous surgical robotics market is segmented into hospitals, ambulatory surgery centers (ASCs), and others. The hospitals segment held the largest market revenue share of 65.2% in 2024, due to their significant investment capacity, presence of multidisciplinary surgical departments, and growing adoption of technologically advanced solutions to enhance surgical precision and patient care.

The ambulatory surgery centers (ASCs) segment is projected to grow at the fastest CAGR of 16.1% from 2025 to 2032, driven by the increasing shift toward outpatient surgeries, demand for same-day procedures, and the adoption of compact and cost-efficient robotic systems in smaller clinical setups.

Autonomous Surgical Robotics Market Regional Analysis

- North America dominated the autonomous surgical robotics market with the largest revenue share of 42.5% in 2024, driven by the rapid adoption of robotic-assisted surgeries

- favorable reimbursement policies, and the presence of major market players such as Intuitive Surgical, Stryker, and Johnson & Johnson

- The region’s advanced healthcare infrastructure, coupled with strong demand for minimally invasive procedures and investments in AI-powered surgical platforms, continues to fuel growth in both inpatient and outpatient settings

U.S. Autonomous Surgical Robotics Market Insight

The U.S. autonomous surgical robotics market captured the largest revenue share of 81% within North America in 2024, attributed to its leadership in robotic surgery installations, innovation in AI integration, and growing procedural volumes across cardiology, orthopedics, and urology. The country’s expanding elderly population, surgeon preference for robotic assistance, and increasing FDA approvals for novel autonomous platforms are accelerating industry growth.

Europe Autonomous Surgical Robotics Market Insight

The Europe autonomous surgical robotics market accounted for 30.6% of the global revenue in 2024 and is projected to grow at a CAGR of 17.8% from 2025 to 2032, driven by rising adoption of robotic technologies in public and private hospitals, as well as supportive regulatory initiatives from the European Commission for digital healthcare transformation. Leading nations such as Germany, France, and the U.K. are focusing on expanding access to precision surgery through national funding and clinical research partnerships.

U.K. Autonomous Surgical Robotics Market Insight

The U.K. autonomous surgical robotics market is expected to grow at a CAGR of 16.9% during the forecast period, supported by growing investments in surgical innovation and NHS-led initiatives for integrating robotic systems in operating theatres. The emphasis on patient safety, quicker recovery, and digital surgical training programs is fostering adoption in both academic medical centers and community hospitals.

Germany Autonomous Surgical Robotics Market Insight

The Germany autonomous surgical robotics market is projected to expand at a CAGR of 18.1%, owing to its technologically progressive healthcare system, early uptake of autonomous navigation in surgery, and rising demand for robotic-assisted oncology and orthopedic procedures. Government-backed AI health initiatives and partnerships with medtech innovators are making Germany a focal point for robotic surgical deployments in Europe.

Asia-Pacific Autonomous Surgical Robotics Market Insight

The Asia-Pacific autonomous surgical robotics market accounted for 19.3% of the global revenue in 2024 and is poised to grow at the fastest CAGR of 24.0% from 2025 to 2032, driven by rising healthcare investments, medical tourism, and increasing adoption of smart hospitals in countries such as China, Japan, and India. Growing awareness of advanced surgical techniques and cost-effective manufacturing of robotics components are contributing to regional expansion.

Japan Autonomous Surgical Robotics Market Insight

The Japan autonomous surgical robotics market contributed 26.3% to the Asia-Pacific revenue in 2024, fueled by a high-tech healthcare ecosystem, rising elderly patient population, and early integration of robotics into neurology and cardiology departments. Japan's leadership in precision engineering and AI-based diagnostics enhances its capability to develop and adopt sophisticated autonomous surgical platforms.

China Autonomous Surgical Robotics Market Insight

The China autonomous surgical robotics market held the largest share within Asia-Pacific at 41.8% in 2024, supported by strong government initiatives under “Healthy China 2030,” increasing access to tertiary care, and significant investment in robotic R&D and clinical AI. Local companies, including those backed by public-private partnerships, are advancing affordable robotic systems and expanding their presence in both public and private hospitals.

Autonomous Surgical Robotics Market Share

The autonomous surgical robotics industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Medtronic (Ireland)

- Smith+Nephew (U.S.)

- Intuitive Surgical Operations, Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Olympus Corporation (Japan)

- Renishaw plc (U.K.)

- ACCURAY Incorporated (U.S.)

- Corindus Vascular Robotics Inc. (U.S.)

- Aethon (U.S.)

- Omnicell, Inc. (U.S.)

- Asensus Surgical, Inc. (U.S.)

- Globus Medical (U.S.)

Latest Developments in Global Autonomous Surgical Robotics Market

- In June 2024, Medtronic plc announced the first U.S. patient enrollment in its pivotal trial evaluating the Hugo robotic-assisted surgery (RAS) system for general surgery procedures. The trial aims to support FDA clearance in the U.S., following the successful use of Hugo in international markets. This milestone marks a major step in Medtronic’s strategy to disrupt the surgical robotics space dominated by Intuitive Surgical

- In May 2024, CMR Surgical raised USD 165 million in a funding round to accelerate the global expansion of its Versius surgical robotic system. The capital will support entry into new markets and the development of next-generation digital surgical capabilities. Versius has gained popularity for its modular design and ease of integration in smaller hospitals and ambulatory surgery centers

- In March 2024, Intuitive Surgical received CE Mark approval for the da Vinci 5, its next-generation surgical robotic platform. The system includes enhanced AI-driven features, improved haptic feedback, and greater precision for a wide range of procedures. With over 12 million surgeries performed globally using da Vinci systems, this latest iteration reinforces Intuitive’s leadership in the field

- In January 2024, Johnson & Johnson’s MedTech division unveiled updates on its OTTAVA surgical robot, announcing plans to begin clinical trials in late 2024. Unlike traditional robotic systems, OTTAVA features a compact, table-mounted design integrated with imaging and analytics. Its development represents J&J’s continued effort to compete in the growing autonomous surgical robotics landscape

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.