Global Autonomous Vehicle Ai Platform Market

Market Size in USD Billion

USD

42.00 Billion

USD

242.44 Billion

2025

2033

USD

42.00 Billion

USD

242.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 42.00 Billion | |

| USD 242.44 Billion | |

| % | |

|

Autonomous Vehicle AI Platform Market Overview

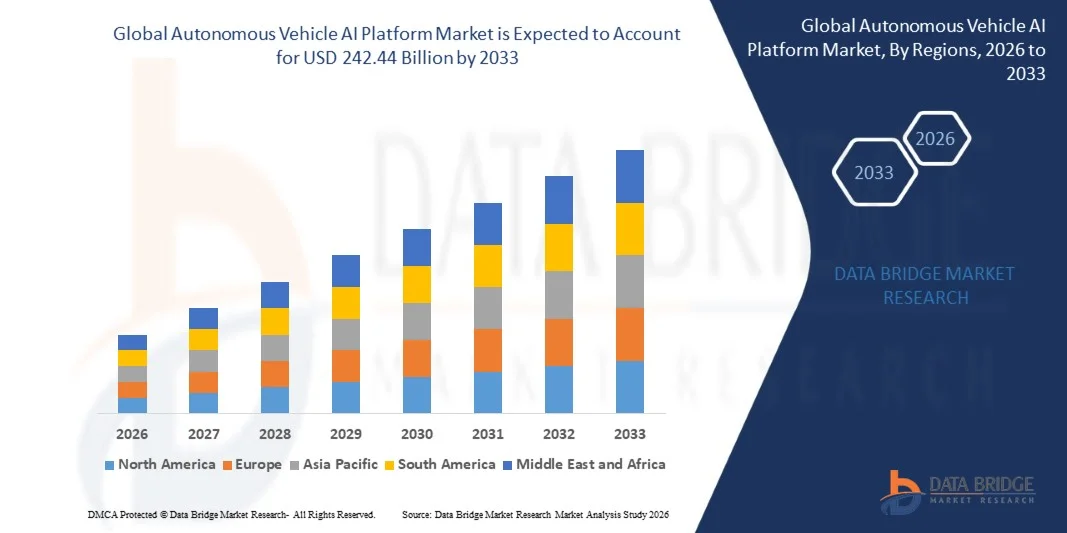

The Autonomous Vehicle AI Platform Market was valued at USD 42 billion in 2025 and is projected to reach USD 242.44 billion by 2033, growing at a CAGR of 24.5% from 2026 to 2033. The market is experiencing rapid expansion driven by advancements in artificial intelligence, sensor fusion technologies, edge computing, and the increasing commercialization of autonomous driving systems across passenger and commercial mobility ecosystems.

The rising demand for safer, more efficient, and software-defined vehicles is accelerating the adoption of AI-driven autonomous driving platforms that integrate perception, planning, mapping, and control systems into unified architectures. Additionally, the convergence of cloud-based AI training, high-definition mapping, and real-time vehicle-to-cloud communication is enabling continuous learning and large-scale deployment of autonomous mobility solutions across global transportation networks.

Key Market Trends & Insights

- North America is the dominating region in the Autonomous Vehicle AI Platform Market, accounting for the largest market share of 39.2% in 2025, driven by strong investments in autonomous driving technologies, presence of leading AI and automotive technology firms, and early regulatory support for autonomous mobility testing and deployment.

- Asia-Pacific is the fastest-growing region in the market, projected to expand at a CAGR of 14.8%, fueled by large-scale deployment of smart mobility infrastructure, rapid electrification of vehicles, and strong government support in countries such as China, Japan, and India for autonomous and connected vehicle ecosystems.

- Perception Systems represent the dominating component segment in the Autonomous Vehicle AI Platform Market, accounting for the largest market share of 31.5% in 2025, driven by critical demand for object detection, sensor fusion, and real-time environmental understanding in autonomous driving systems.

- Simulation & Validation Platforms are the fastest-growing component segment, projected to expand at a CAGR of 15.6% from 2026 to 2033, supported by increasing reliance on virtual testing environments, scenario generation, and AI-based safety validation for autonomous vehicle deployment.

- By Platform Type, Full-Stack Autonomous Platforms dominate the market with a 36.7% share in 2025, driven by strong adoption by OEMs and mobility companies seeking end-to-end integrated solutions covering perception to control.

- Cloud AI Training Platforms are the fastest-growing platform type segment, projected to grow at a CAGR of 16.2%, driven by rising demand for scalable AI model training, fleet learning, and continuous improvement of autonomous driving algorithms.

- By Autonomy Level, Level 2 (Driver Assistance) remains the dominating segment with a 44.1% market share in 2025, due to widespread adoption in modern passenger vehicles with advanced driver assistance systems (ADAS).

- Level 4 (High Automation) is the fastest-growing autonomy level segment, projected to expand at a CAGR of 17.3%, driven by pilot deployments in robotaxi services, autonomous shuttles, and logistics operations in controlled environments.

- By Application, Personal Mobility is the dominating segment, accounting for 29.6% market share in 2025, driven by integration of AI-driven driver assistance and semi-autonomous features in consumer vehicles.

- Ride-Hailing / Robotaxi Services is the fastest-growing application segment, projected to grow at a CAGR of 18.1%, supported by increasing investments in autonomous mobility fleets and pilot commercialization in urban transport ecosystems.

Market Size & Forecast

- Global Market Value (2025): USD 42 Billion

- Expected Market Value (2033): USD 242.44 Billion

- Forecast CAGR (2026–2033): 24.5%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Autonomous Vehicle AI Platform Market Segmentation

|

Attributes |

Autonomous Vehicle AI Platform Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Waymo LLC (U.S.) · Tesla, Inc. (U.S.) · NVIDIA Corporation (U.S.) · Mobileye (an Intel Company) (Israel) · Aurora Innovation, Inc. (U.S.) · Aptiv PLC (Ireland) · Baidu, Inc. (China) · Uber Technologies, Inc. (U.S.) · Zoox (Amazon) (U.S.) · Toyota Motor Corporation (Japan) · General Motors (Cruise LLC) (U.S.) · Huawei Technologies Co., Ltd. (China) · Qualcomm Technologies, Inc. (U.S.) · Bosch Mobility Solutions (Germany) · Continental AG (Germany) · Pony.ai (U.S./China) · WeRide Inc. (China) |

|

Market Opportunities |

· Expansion of end-to-end autonomous driving stacks integrating perception, planning, and control in unified AI platforms · Rapid growth of robotaxi and autonomous fleet-based mobility services in urban environments · Increasing adoption of cloud-based AI training and simulation platforms for large-scale autonomous driving model development |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Autonomous Vehicle AI Platform Market Trends

Trend: Integration of Generative AI and End-to-End Autonomous Driving Models

Autonomous vehicle AI platforms are increasingly adopting generative AI and end-to-end deep learning models to enhance perception accuracy, decision-making efficiency, and scenario prediction capabilities. Companies are moving away from modular rule-based systems toward unified neural network architectures that process raw sensor inputs directly into driving actions. This shift is enabling faster iteration cycles, improved adaptability to edge cases, and more human-like driving behavior in complex environments.

Autonomous Vehicle AI Platform Market Dynamics

Key Market Driver: Rapid Advancements in AI, Sensor Fusion, and Edge Computing

The increasing sophistication of AI models combined with advances in LiDAR, radar, and camera-based sensor fusion is significantly boosting the performance of autonomous driving systems. Automotive OEMs and technology providers are heavily investing in AI-first vehicle architectures that enable real-time decision-making with low latency. For example, companies developing robotaxi and autonomous logistics fleets are leveraging high-performance GPUs and edge AI chips to process massive sensor datasets in real time, enabling safer and more reliable autonomous navigation.

Key Restraint/Challenge: Regulatory Uncertainty and Safety Validation Complexity

A major challenge in the autonomous vehicle AI platform market is the lack of standardized global regulations and the complexity of validating safety across billions of real-world driving scenarios. Autonomous systems must be tested across diverse weather, traffic, and geographic conditions, which makes large-scale validation extremely resource-intensive. Additionally, liability concerns in accident scenarios and inconsistent regulatory frameworks across regions slow down large-scale commercialization of Level 4 and Level 5 autonomous systems.

Key Market Opportunity: Expansion of Autonomous Mobility Ecosystems and AI Cloud Infrastructure

The growing deployment of autonomous mobility ecosystems such as robotaxis, autonomous shuttles, and freight delivery fleets is creating strong opportunities for AI platform providers. Cloud-based AI training infrastructure allows continuous learning from fleet data, enabling rapid improvements in autonomy performance. Companies are also investing in digital twin environments and large-scale simulation platforms to replicate real-world driving conditions, significantly reducing testing costs and accelerating deployment timelines for autonomous vehicles worldwide.

Autonomous Vehicle AI Platform Market Scope

The autonomous vehicle AI platform market is segmented on the basis of component, platform type, autonomy level, vehicle type, application, and end user.

- By Component

On the basis of component, the Autonomous Vehicle AI Platform Market is segmented into perception systems, planning & decision systems, control systems, HD mapping & localization, simulation & validation platforms, and fleet & OTA software infrastructure. The Perception Systems segment dominated the market with a 31.5% share in 2025, driven by its critical role in enabling real-time environment understanding, object detection, sensor fusion, and scene interpretation in autonomous driving systems. Perception stacks form the foundational intelligence layer for safe navigation across complex driving conditions.

The Simulation & Validation Platforms segment is expected to witness the fastest growth at a CAGR of 15.6% from 2026 to 2033, driven by the increasing need for large-scale virtual testing, scenario generation, and AI-based safety validation. Rising adoption of digital twins, closed-loop simulation environments, and cloud-based autonomous driving test infrastructure is further accelerating demand for this segment.

- By Platform Type

On the basis of platform type, the Autonomous Vehicle AI Platform Market is segmented into full-stack autonomous platforms, modular AV platforms, cloud AI training platforms, and edge AI vehicle platforms. The Full-Stack Autonomous Platforms segment dominated the market with a 36.7% share in 2025, due to strong adoption by OEMs and mobility companies seeking integrated end-to-end solutions covering perception, planning, mapping, and control within a unified architecture.

The Cloud AI Training Platforms segment is expected to register the fastest growth at a CAGR of 16.2% from 2026 to 2033, driven by increasing demand for scalable AI model training, fleet data learning, and continuous software improvement cycles. Expansion of GPU-accelerated cloud infrastructure and distributed learning frameworks is further supporting segment growth.

- By Autonomy Leve

On the basis of autonomy level, the Autonomous Vehicle AI Platform Market is segmented into Level 2 (Driver Assistance), Level 3 (Conditional Automation), Level 4 (High Automation), and Level 5 (Full Automation). The Level 2 segment dominated the market with a 44.1% share in 2025, supported by widespread integration of advanced driver assistance systems (ADAS) in passenger vehicles across global automotive OEMs.

The Level 4 segment is expected to witness the fastest growth at a CAGR of 17.3% from 2026 to 2033, driven by increasing deployment of robotaxis, autonomous shuttles, and logistics pilot programs operating in geo-fenced and controlled environments. Continuous improvements in AI decision-making, sensor fusion, and regulatory approvals are further accelerating adoption.

- By Vehicle Type

On the basis of vehicle type, the Autonomous Vehicle AI Platform Market is segmented into passenger vehicles, commercial vehicles, robotaxis & mobility fleets, and autonomous shuttles. The Passenger Vehicles segment dominated the market with a 41.8% share in 2025, driven by rapid integration of ADAS and semi-autonomous features in mass-market vehicles, luxury cars, and EV platforms.

The Robotaxis & Mobility Fleets segment is expected to witness the fastest growth at a CAGR of 18.1% from 2026 to 2033, fueled by expanding autonomous ride-hailing pilots, fleet-based mobility models, and increasing investment from technology companies and mobility service providers in urban transport automation.

- By Application

On the basis of application, the Autonomous Vehicle AI Platform Market is segmented into personal mobility, ride-hailing / robotaxi services, freight & logistics, and last-mile delivery. The Personal Mobility segment dominated the market with a 29.6% share in 2025, driven by widespread use of AI-powered driver assistance and semi-autonomous features in consumer vehicles.

The Ride-Hailing / Robotaxi Services segment is expected to witness the fastest growth at a CAGR of 18.1% from 2026 to 2033, driven by rapid commercialization of autonomous mobility services, increasing urban deployment of robotaxi fleets, and growing partnerships between OEMs and mobility platform providers.

- By End User

On the basis of end user, the Autonomous Vehicle AI Platform Market is segmented into OEMs, Tier-1 suppliers, mobility service providers, logistics companies, and technology providers. The OEMs segment dominated the market with a 38.4% share in 2025, driven by strong investments in autonomous driving integration, software-defined vehicle architectures, and in-house AI platform development.

The Mobility Service Providers segment is expected to witness the fastest growth at a CAGR of 17.6% from 2026 to 2033, driven by expansion of robotaxi networks, autonomous shuttle services, and fleet-based mobility ecosystems supported by AI-driven dispatching and route optimization systems.

Autonomous Vehicle AI Platform Market Regional Analysis

North America dominated the autonomous vehicle AI platform market and accounted for the largest revenue share of 39.2% in 2025, driven by strong presence of leading AI technology companies, advanced autonomous driving R&D ecosystems, early regulatory testing frameworks, and high investment in robotaxi and autonomous logistics development. The region also benefits from strong integration of cloud AI infrastructure and high-performance computing capabilities across automotive innovation centers.

U.S. Autonomous Vehicle AI Platform Market Insight

The U.S. autonomous vehicle AI platform market is witnessing strong expansion due to rapid advancements in AI-driven mobility systems, increasing deployment of robotaxi pilots, and significant investments in autonomous driving technologies by both automotive OEMs and technology firms. Companies such as Waymo LLC, Tesla, Inc., and NVIDIA Corporation are actively developing end-to-end autonomous driving stacks combining perception, planning, and control systems. Additionally, strong venture capital funding and supportive regulatory testing environments are accelerating commercialization efforts.

Europe Autonomous Vehicle AI Platform Market Insight

The Europe autonomous vehicle AI platform market is driven by strong automotive engineering capabilities, increasing adoption of software-defined vehicle architectures, and growing investment in mobility innovation ecosystems. The region benefits from leading OEMs integrating advanced driver assistance systems and autonomous features into production vehicles. Companies such as Volkswagen Group, Mercedes-Benz Group AG, and BMW Group are actively investing in AI-driven mobility platforms, while regulatory emphasis on safety and sustainability is accelerating simulation-based validation adoption.

U.K. Autonomous Vehicle AI Platform Market Insight

The U.K. autonomous vehicle AI platform market is experiencing steady growth supported by strong research initiatives in autonomous systems, AI, and robotics. Increasing deployment of autonomous mobility trials in urban environments, along with government-backed smart transport initiatives, is strengthening market expansion. Universities and technology firms are actively contributing to advancements in perception systems, sensor fusion, and decision-making algorithms for autonomous vehicles.

Germany Autonomous Vehicle AI Platform Market Insight

The Germany autonomous vehicle AI platform market is expanding due to the country’s leadership in automotive manufacturing and engineering excellence. German OEMs and Tier-1 suppliers are integrating AI-driven simulation, HD mapping, and advanced driver assistance technologies into next-generation vehicles. Companies such as Mercedes-Benz Group AG and BMW Group are investing heavily in autonomous driving platforms, particularly for Level 3 and Level 4 automation systems. The strong presence of industrial automation and Industry 4.0 infrastructure further supports market development.

Asia-Pacific Autonomous Vehicle AI Platform Market Insight

The Asia-Pacific autonomous vehicle AI platform market is expected to witness the fastest growth, driven by large-scale deployment of smart mobility infrastructure, strong government support for autonomous driving technologies, and rapid expansion of electric vehicle ecosystems. Countries such as China, Japan, and India are investing heavily in AI-powered mobility systems, autonomous logistics networks, and smart city initiatives. Increasing adoption of cloud-based AI training platforms and cost-efficient edge computing solutions is further accelerating regional growth.

Japan Autonomous Vehicle AI Platform Market Insight

The Japan autonomous vehicle AI platform market is growing steadily due to strong focus on robotics, precision engineering, and automotive innovation. Companies such as Toyota Motor Corporation and Honda Motor Co., Ltd. are actively developing autonomous driving systems integrated with AI-based perception and control modules. The country is also advancing research in digital twins, HD mapping, and simulation-based validation for autonomous mobility systems.

China Autonomous Vehicle AI Platform Market Insight

The China autonomous vehicle AI platform market is expanding rapidly due to strong government support for intelligent transportation systems, large-scale EV adoption, and rapid advancements in AI and semiconductor technologies. Companies such as Baidu, Inc. and Huawei Technologies Co., Ltd. are leading the development of autonomous driving platforms and cloud-based AI ecosystems. The country is also witnessing strong growth in robotaxi deployments and autonomous logistics applications, making it one of the fastest-growing markets globally.

Autonomous Vehicle AI Platform Market Share

The autonomous vehicle AI platform industry is primarily led by well-established companies, including:

- Waymo LLC (U.S.)

- Tesla, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Mobileye (an Intel Company) (Israel)

- Aurora Innovation, Inc. (U.S.)

- Aptiv PLC (Ireland)

- Baidu, Inc. (China)

- Uber Technologies, Inc. (U.S.)

- Zoox (Amazon) (U.S.)

- Toyota Motor Corporation (Japan)

- General Motors (Cruise LLC) (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Qualcomm Technologies, Inc. (U.S.)

- Bosch Mobility Solutions (Germany)

- Continental AG (Germany)

- ai (U.S./China)

- WeRide Inc. (China)

Latest Developments in Autonomous Vehicle AI Platform Market

- In October 2025, NVIDIA Corporation strengthened its DRIVE AV ecosystem by expanding the NVIDIA DRIVE AGX Hyperion 10 platform, enabling Level 4-ready autonomous vehicle development through a scalable reference architecture combining AI compute, sensor fusion, and DriveOS software. The upgrade supports automakers such as Mercedes-Benz, Stellantis, and Lucid in building end-to-end autonomous driving systems while integrating Uber’s global robotaxi deployment plans, reinforcing NVIDIA’s leadership in AI-defined mobility and autonomous vehicle infrastructure.

- In June 2025, NVIDIA Corporation advanced its DRIVE full-stack autonomous vehicle software into full production, offering a unified AI platform that integrates perception, planning, simulation, and accelerated compute for automakers, robotaxi operators, and mobility startups. The platform enhances real-time decision-making and supports large-scale deployment of software-defined autonomous vehicles across global transportation networks.

- In January 2025, NVIDIA DRIVE Hyperion platform achieved key automotive safety and cybersecurity validation milestones from TÜV SÜD and TÜV Rheinland, strengthening its position as a certified end-to-end autonomous driving stack. The platform integrates NVIDIA DriveOS, high-performance DRIVE SoCs, and scalable sensor architectures, enabling automakers such as Toyota and Volvo to accelerate deployment of Level 2+ to Level 4 autonomous driving systems.

- In October 2025, Uber Technologies, Inc. expanded its collaboration with NVIDIA DRIVE ecosystem by integrating AI training and simulation tools based on NVIDIA Cosmos and DGX Cloud infrastructure. This development supports large-scale robotaxi fleet deployment, enabling Uber to prepare for autonomous ride-hailing operations powered by DRIVE-compatible vehicles across global markets starting in 2027.

- In May 2025, Aurora Innovation, Inc. advanced its autonomous trucking program built on NVIDIA DRIVE-based compute infrastructure, expanding driverless freight operations and extending routes across multiple U.S. logistics corridors. The company is also enhancing nighttime and adverse weather driving capabilities, strengthening its position in Level 4 autonomous freight transportation within the DRIVE ecosystem.

- In January 2025, Toyota Motor Corporation expanded its collaboration within the NVIDIA DRIVE ecosystem by adopting DRIVE AGX Orin-based platforms for next-generation vehicles, enabling advanced driver assistance and early autonomous driving capabilities. This integration supports Toyota’s strategy to accelerate AI-driven mobility development across passenger and commercial vehicle segments.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.