Global Battery Binders Market

Market Size in USD Billion

USD

2.50 Billion

USD

8.60 Billion

2025

2033

USD

2.50 Billion

USD

8.60 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.50 Billion | |

| USD 8.60 Billion | |

| % | |

|

Battery Binders Market Overview

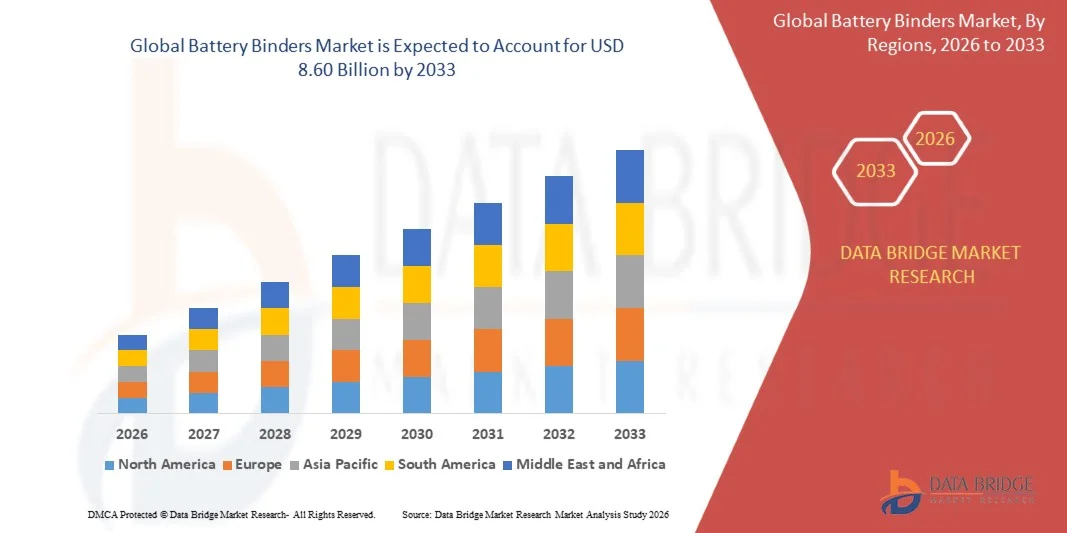

As per Data Bridge Market Research analysis the Battery Binders Market was valued at USD 2.50 billion in 2025 and is projected to reach USD 8.60 billion by 2033, growing at a CAGR of 16.70% from 2026 to 2033. The market is witnessing robust growth driven by the rapid expansion of electric vehicle production, increasing deployment of lithium-ion batteries across energy storage systems, and continuous advancements in battery materials designed to improve energy density, cycle life, and operational safety.

The accelerating global transition toward clean energy and electrified transportation, combined with rising investments in battery manufacturing facilities and government support for localized battery supply chains, is significantly increasing demand for advanced battery binders. Water-based binders such as styrene-butadiene rubber (SBR) and carboxymethyl cellulose (CMC), along with high-performance polyvinylidene fluoride (PVDF) binders, are increasingly replacing conventional materials by providing superior electrode adhesion, mechanical stability, and electrochemical performance. Furthermore, continuous innovation in silicon-anode and solid-state battery technologies is creating new opportunities for next-generation binder formulations capable of enhancing battery durability, charging efficiency, and long-term performance.

Market Size & Forecast

- Global Market Value (2025): USD 2.50 Billion

- Expected Market Value (2033): USD 8.60 Billion

- Forecast CAGR (2026–2033): 16.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the battery binders market with the largest revenue share of 40.5% in 2025, supported by rapid investments in electric vehicle manufacturing, battery gigafactories, and advanced energy storage technologies. The region benefits from strong government support for domestic battery supply chains, growing adoption of renewable energy storage systems, and increasing research into next-generation battery chemistries.

- Asia-Pacific battery binders market is expected to witness the fastest growth rate from 2026 to 2033 with approximately 25% of the global market share, supported by large-scale battery manufacturing, expanding electric vehicle production, and growing renewable energy storage deployments across China, Japan, South Korea, and India.

- The lithium-ion batteries segment held the largest market share in 2025, driven by the increasing production of electric vehicles, battery energy storage systems, and portable consumer electronics. Battery binders play a critical role in maintaining electrode integrity, improving adhesion between active materials and current collectors, and enhancing battery cycle life. The growing adoption of high-energy-density batteries across automotive and renewable energy applications continues to strengthen demand for advanced binder materials. Rising investments in lithium-ion battery gigafactories across Asia-Pacific, Europe, and North America are further supporting segment growth.

- The lead-acid batteries segment is projected to register the fastest growth from 2026 to 2033, driven by rising demand for cost-effective energy storage, automotive starter batteries, industrial backup power systems, and telecommunication infrastructure. Increasing deployment of uninterrupted power supply (UPS) systems and data center backup solutions is creating additional demand for lead-acid batteries. Their established recycling infrastructure, lower production costs, and widespread use in industrial applications continue to support market expansion.

- The anode binder segment held the largest market share in 2025, driven by its extensive use in graphite anodes for lithium-ion batteries. These binders provide excellent mechanical strength, maintain electrode stability during repeated charging cycles, and improve overall battery performance. Growing production of electric vehicle batteries and energy storage systems is significantly increasing demand for advanced anode binder technologies. Continuous research into silicon-anode batteries is also encouraging innovations in anode binder formulations.

- The cathode binder segment is projected to witness the fastest growth from 2026 to 2033, driven by increasing demand for high-capacity cathode materials such as NMC, LFP, and high-nickel chemistries. Cathode binders are essential for maintaining electrode cohesion, chemical stability, and long-term cycling performance under high-voltage operating conditions. Rising investments in next-generation battery technologies and premium electric vehicles are expected to further accelerate segment growth.

Report Scope and Battery Binders Market Segmentation

|

Attributes |

Battery Binders Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Battery Binders Market Trends

Trend: Rising Adoption Of High-Performance And Water-Based Battery Binder Technologies

Growing demand for high-energy-density lithium-ion batteries across electric vehicles, energy storage systems, and consumer electronics is accelerating the adoption of advanced battery binder technologies. Conventional solvent-based binders are associated with higher processing costs, VOC emissions, and stricter environmental regulations, encouraging battery manufacturers to transition toward water-based and next-generation polymer binders that improve sustainability while maintaining electrode performance.

In modern lithium-ion battery manufacturing, companies are increasingly adopting advanced battery binder technologies. For instance, in March 2026, Arkema showcased its latest Kynar PVDF and Incellion battery binder portfolio at InterBattery 2026, introducing new binder solutions for LFP cathodes, silicon anodes, and solid-state batteries to improve electrode adhesion, cycling stability, and energy density while reducing binder loading and manufacturing costs. In addition, polyvinylidene fluoride (PVDF) continues to dominate cathode applications because of its superior electrochemical stability and long cycle life.

The rapid commercialization of silicon-anode batteries and solid-state batteries is further increasing demand for advanced binders capable of accommodating higher electrode expansion and maintaining structural integrity during repeated charge-discharge cycles. In addition, manufacturers are investing in bio-based and fluorine-free binder technologies to comply with tightening environmental regulations while improving battery recyclability. Industry developments during 2024 and 2025, including new PVDF capacity expansions by leading chemical manufacturers, are strengthening global battery material supply chains and supporting next-generation battery production.

Battery Binders Market Dynamics

Key Market Driver: Rapid Expansion Of Electric Vehicle And Lithium-Ion Battery Manufacturing

Global electric vehicle production and renewable energy deployment continue to increase demand for lithium-ion batteries with higher energy density, longer cycle life, and improved safety. Battery binders play a critical role in maintaining electrode cohesion, improving conductivity, and ensuring long-term electrochemical stability, making them essential materials for modern battery manufacturing.

Battery manufacturers across Asia-Pacific, Europe, and North America are significantly expanding production capacity, creating strong demand for advanced binder materials. For instance, according to the International Energy Agency's Global EV Outlook 2025, global battery demand surpassed 1 TWh for the first time in 2024, while EV battery demand exceeded 950 GWh and global battery manufacturing capacity expanded beyond 3 TWh, substantially increasing demand for PVDF, SBR, and CMC battery binders used in lithium-ion cell production.

Similarly, continued gigafactory investments across the U.S., Europe, and Asia are accelerating consumption of high-performance binder materials required for next-generation batteries.

Key Restraint/Challenge: High Raw Material Costs And Supply Chain Dependence

Battery binder manufacturers continue to face challenges associated with volatile raw material prices, dependence on specialty fluoropolymers, and increasing supply chain risks. High-performance binders such as PVDF require fluorinated raw materials and complex manufacturing processes, resulting in higher production costs compared with conventional polymer materials.

In addition, fluctuations in fluorochemical supply, rising energy prices, and increasing environmental regulations governing fluorinated materials continue to create uncertainty for manufacturers. For instance, the European Chemicals Agency (ECHA) continues evaluating the proposed EU-wide PFAS restriction covering thousands of fluorinated substances, encouraging battery material suppliers to accelerate development of fluorine-free binder chemistries while balancing battery performance and regulatory compliance.

Commercial battery manufacturers are also evaluating fluorine-free binder systems to reduce regulatory exposure while maintaining battery performance. However, achieving comparable electrochemical stability, adhesion strength, and long-term cycling performance remains a significant commercialization challenge for next-generation binder technologies.

Key Market Opportunity: Development Of Silicon-Anode And Solid-State Batteries

The emergence of silicon-anode batteries, lithium metal batteries, and solid-state battery technologies is creating substantial opportunities for advanced battery binder manufacturers. These next-generation batteries require highly elastic and chemically stable binders capable of maintaining electrode integrity under significantly higher mechanical stress than conventional graphite-based batteries.

Battery material companies are increasingly developing specialized binder formulations. For instance, in March 2026, Arkema introduced new Incellion EL binder technologies for silicon-rich anodes and all-solid-state batteries at InterBattery 2026, designed to improve adhesion, conductivity, durability, and accommodate silicon volume expansion, supporting commercialization of higher-energy-density battery platforms.

In addition, growing investments in solid-state battery commercialization by automotive manufacturers and battery producers are creating new opportunities for high-performance binder materials compatible with solid electrolytes and advanced electrode architectures. As global battery technology continues to evolve toward higher energy density and faster charging capability, demand for innovative battery binder solutions is expected to accelerate significantly throughout the forecast period.

Battery Binders Market Scope

The market is segmented on the basis of application, type, material type, end use industry, and formulation type.

- By Application

On the basis of application, the battery binders market is segmented into lithium-ion batteries, lead-acid batteries, nickel-metal hydride batteries, and sodium-ion batteries. The lithium-ion batteries segment held the largest market share in 2025, driven by the increasing production of electric vehicles, battery energy storage systems, and portable consumer electronics. Battery binders play a critical role in maintaining electrode integrity, improving adhesion between active materials and current collectors, and enhancing battery cycle life. The growing adoption of high-energy-density batteries across automotive and renewable energy applications continues to strengthen demand for advanced binder materials. Rising investments in lithium-ion battery gigafactories across Asia-Pacific, Europe, and North America are further supporting segment growth.

The lead-acid batteries segment is projected to register the fastest growth from 2026 to 2033, driven by rising demand for cost-effective energy storage, automotive starter batteries, industrial backup power systems, and telecommunication infrastructure. Increasing deployment of uninterrupted power supply (UPS) systems and data center backup solutions is creating additional demand for lead-acid batteries. Their established recycling infrastructure, lower production costs, and widespread use in industrial applications continue to support market expansion.

- By Type

On the basis of type, the battery binders market is segmented into anode binder and cathode binder. The anode binder segment held the largest market share in 2025, driven by its extensive use in graphite anodes for lithium-ion batteries. These binders provide excellent mechanical strength, maintain electrode stability during repeated charging cycles, and improve overall battery performance. Growing production of electric vehicle batteries and energy storage systems is significantly increasing demand for advanced anode binder technologies. Continuous research into silicon-anode batteries is also encouraging innovations in anode binder formulations.

The cathode binder segment is projected to witness the fastest growth from 2026 to 2033, driven by increasing demand for high-capacity cathode materials such as NMC, LFP, and high-nickel chemistries. Cathode binders are essential for maintaining electrode cohesion, chemical stability, and long-term cycling performance under high-voltage operating conditions. Rising investments in next-generation battery technologies and premium electric vehicles are expected to further accelerate segment growth.

- By Material Type

On the basis of material type, the battery binders market is segmented into polyvinylidene fluoride, styrene-butadiene rubber, cellulose, and polyacrylic acid. The polyvinylidene fluoride (PVDF) segment held the largest market share in 2025, driven by its superior thermal stability, outstanding chemical resistance, and excellent electrochemical performance. PVDF remains the preferred binder material for lithium-ion battery cathodes because it enhances battery durability, improves energy density, and supports long service life. Its widespread adoption across automotive, consumer electronics, and energy storage applications continues to reinforce market dominance.

The styrene-butadiene rubber (SBR) segment is projected to register the fastest growth from 2026 to 2033, driven by increasing adoption of water-based electrode manufacturing processes and growing environmental regulations aimed at reducing solvent emissions. SBR offers excellent flexibility, strong adhesion, and improved mechanical stability for graphite anodes. Increasing investments in sustainable battery manufacturing and environmentally friendly production technologies are expected to further support segment expansion.

- By End Use Industry

On the basis of end use industry, the battery binders market is segmented into automotive, consumer electronics, renewable energy, and industrial. The automotive segment held the largest market share in 2025, driven by accelerating electric vehicle production, battery gigafactory expansion, and increasing investments in advanced battery technologies worldwide. Government incentives supporting EV adoption and rising demand for long-range electric vehicles continue to increase battery manufacturing volumes. Battery binders play a crucial role in improving battery reliability, charging efficiency, and operational safety for automotive applications.

The consumer electronics segment is projected to witness the fastest growth from 2026 to 2033, driven by rising demand for smartphones, laptops, tablets, wearable devices, wireless audio products, and other portable electronic devices. Manufacturers are increasingly focusing on compact, lightweight, and high-capacity batteries, creating greater demand for advanced binder materials. Continuous product innovation and shorter consumer electronics replacement cycles are further contributing to market growth.

- By Formulation Type

On the basis of formulation type, the battery binders market is segmented into water-based binders, solvent-based binders, and thermoplastic binders. The water-based binders segment held the largest market share in 2025, driven by stringent environmental regulations, lower volatile organic compound emissions, reduced manufacturing costs, and increasing adoption in lithium-ion battery production. Water-based formulations improve workplace safety while reducing overall production complexity. Their compatibility with graphite anode manufacturing has made them the preferred choice for many battery manufacturers globally.

The solvent-based binders segment is projected to register the fastest growth from 2026 to 2033, driven by continued demand for high-performance PVDF-based cathode binders used in premium electric vehicle batteries and high-energy-density battery applications. These binders offer superior chemical resistance, thermal stability, and electrochemical performance under demanding operating conditions. Growing commercialization of advanced lithium-ion battery chemistries and high-performance energy storage systems is expected to further support segment growth.

Battery Binders Market Regional Analysis

North America Battery Binders Market Insight

North America dominated the battery binders market with the largest revenue share of 40.5% in 2025, supported by rapid investments in electric vehicle manufacturing, battery gigafactories, and advanced energy storage technologies. The region benefits from strong government support for domestic battery supply chains, growing adoption of renewable energy storage systems, and increasing research into next-generation battery chemistries. The presence of leading battery manufacturers, material suppliers, and technology developers continues to strengthen demand for high-performance binder materials across automotive and industrial applications.

U.S. Battery Binders Market Insight

The U.S. battery binders market captured the largest revenue share in 2025 within North America, fueled by expanding lithium-ion battery manufacturing capacity and increasing investments in electric vehicle production. Government initiatives supporting domestic battery material production and supply chain localization are accelerating demand for advanced binder materials. In addition, growing investments in battery recycling, grid-scale energy storage, and next-generation battery technologies are further contributing to market expansion. The continued development of battery gigafactories is expected to strengthen long-term market growth.

Europe Battery Binders Market Insight

The Europe battery binders market with the second largest revenue share of 30.5% in 2025, primarily driven by stringent carbon reduction policies, rapid electric vehicle adoption, and expanding battery manufacturing capacity across the region. Increasing investments under the European Battery Alliance and growing localization of battery material production are supporting demand for advanced binder technologies. Rising emphasis on sustainable manufacturing and environmentally friendly battery materials is further encouraging the adoption of water-based and high-performance binder formulations.

U.K. Battery Binders Market Insight

The U.K. battery binders market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in electric vehicle manufacturing, battery research, and domestic battery supply chain development. Government initiatives supporting net-zero emissions and battery innovation are encouraging manufacturers to adopt advanced battery materials. Growing collaboration between automotive manufacturers, research institutions, and battery developers is expected to accelerate demand for high-performance battery binders across automotive and energy storage applications.

Germany Battery Binders Market Insight

The Germany battery binders market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country's strong automotive manufacturing base and increasing investments in lithium-ion battery production. Germany continues to strengthen its battery value chain through gigafactory developments and advanced battery material research. Rising demand for premium electric vehicles and next-generation battery technologies is accelerating the adoption of high-performance binder materials. Increasing focus on sustainable battery manufacturing further supports market growth.

Asia-Pacific Battery Binders Market Insight

The Asia-Pacific battery binders market is expected to witness the fastest growth rate from 2026 to 2033 with approximately 25% of the global market share, supported by large-scale battery manufacturing, expanding electric vehicle production, and growing renewable energy storage deployments across China, Japan, South Korea, and India. The region serves as the global manufacturing hub for lithium-ion batteries and battery materials, benefiting from strong industrial infrastructure and competitive production costs. Increasing investments in next-generation battery technologies continue to drive demand for advanced battery binders throughout the region.

Japan Battery Binders Market Insight

The Japan battery binders market is expected to witness the fastest growth rate from 2026 to 2033 due to the country's leadership in advanced battery technology, material innovation, and electric vehicle development. Japanese manufacturers continue to invest in solid-state batteries, silicon-anode technologies, and high-performance lithium-ion batteries, increasing demand for specialized binder materials. Strong collaboration between battery manufacturers, automotive companies, and research institutions is further supporting technological advancements and market expansion.

China Battery Binders Market Insight

The China battery binders market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's dominant position in global lithium-ion battery manufacturing and electric vehicle production. China continues to expand battery gigafactory capacity while strengthening domestic production of battery materials and components. Government policies supporting new energy vehicles, renewable energy storage, and battery supply chain localization are significantly driving demand for battery binders. The presence of major battery manufacturers and raw material suppliers continues to reinforce China's leadership in the Battery Binders Market.

Battery Binders Market Share

The Battery Binders industry is primarily led by well-established companies, including:

- BASF SE (Germany)

- Solvay SA (Belgium)

- Kraton Corporation (U.S.)

- Mitsubishi Chemical Corporation (Japan)

- LG Chem Ltd. (South Korea)

- SABIC (Saudi Arabia)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Wacker Chemie AG (Germany)

- Dow Inc. (U.S.)

- Arkema S.A. (France)

- Zeon Corporation (Japan)

- JSR Corporation (Japan)

- Kureha Corporation (Japan)

- Daikin Industries, Ltd. (Japan)

- Asahi Kasei Corporation (Japan)

Latest Developments in Battery Binders Market

- In January 2026, Trinseo expanded its VOLTABOND battery binder portfolio with advanced water-based latex binder technologies designed to improve lithium-ion battery performance, faster charging capability, and manufacturing efficiency. The company also strengthened its battery materials ecosystem through a dedicated battery binder laboratory in Germany to accelerate product development and customer collaboration. This development supports the industry's transition toward sustainable battery manufacturing while enhancing the commercialization of next-generation EV batteries.

- In January 2024, BASF entered a strategic partnership with Stena Recycling to establish a European battery recycling value chain for electric vehicle batteries. The collaboration enables the recovery and reuse of valuable battery materials for new battery production, strengthening regional raw material security and supporting circular economy objectives. The initiative is expected to improve sustainability across the lithium-ion battery supply chain while supporting long-term battery materials demand.

- In May 2023, BASF announced investments to upgrade two production facilities in China for manufacturing Licity and Basonal Power water-based anode binders for lithium-ion batteries. The expansion increased production capacity to more than 100,000 metric tons annually, ensuring a stable supply of advanced binders for the rapidly growing electric vehicle market. The investment strengthens global battery material supply chains while supporting higher battery performance and sustainability.

- In July 2022, BASF commercialized its Licity anode binder portfolio manufactured in Europe to strengthen local supply for lithium-ion battery manufacturers. The new binder range improves battery capacity, charging performance, and sustainability while supporting regional battery production and reducing supply chain dependence. The commercialization further reinforced Europe's expanding electric vehicle battery ecosystem.

- In July 2022, BASF published benchmark performance results for its Licity battery binders following independent testing by CUSTOMCELLS. The evaluation demonstrated improved electrochemical performance and competitive advantages over conventional binder technologies, validating the suitability of Licity for high-performance lithium-ion batteries. The results supported broader commercial adoption of advanced binder materials across the battery manufacturing industry.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Battery Binders Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Battery Binders Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Battery Binders Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.