Global Battery Packaging Material Market

Market Size in USD Billion

USD

41.24 Billion

USD

102.12 Billion

2025

2033

USD

41.24 Billion

USD

102.12 Billion

2025

2033

| 2026 - 2033 | |

| USD 41.24 Billion | |

| USD 102.12 Billion | |

| % | |

|

Battery Packaging Material Market Size

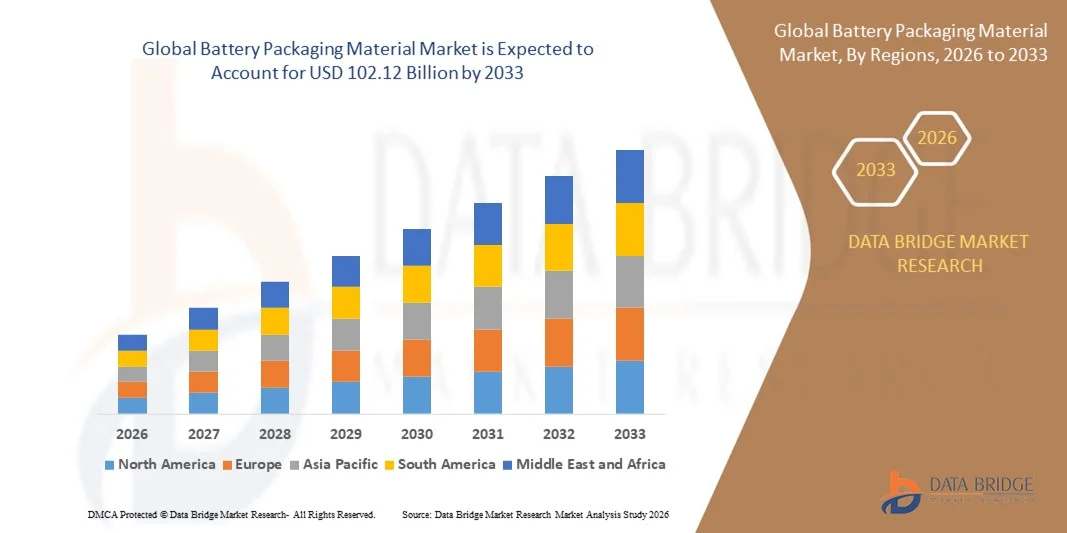

- The global battery packaging material market size was valued at USD 41.24 billion in 2025 and is expected to reach USD 102.12 billion by 2033, at a CAGR of 12.00% during the forecast period

- The market growth is largely fuelled by the increasing adoption of electric vehicles (EVs), energy storage systems, and portable electronic devices, which demand high-performance and safe battery packaging materials

- The growing emphasis on sustainable and recyclable packaging materials is further encouraging innovation and the use of eco-friendly materials, such as aluminum, polymer composites, and fiber-based solutions, to meet environmental regulations

Battery Packaging Material Market Analysis

- The market is witnessing significant technological advancements, with manufacturers focusing on improving thermal management, structural integrity, and chemical resistance of packaging materials to ensure enhanced battery safety and longevity

- Moreover, rising investments in battery gigafactories and large-scale renewable energy storage projects are creating strong demand for advanced packaging solutions that support efficient transportation, storage, and recycling of high-capacity batteries

- North America dominated the battery packaging material market with the largest revenue share of 38.42% in 2025, driven by the rapid growth of electric vehicle (EV) production and strong demand for energy storage solutions across the region

- Asia-Pacific region is expected to witness the highest growth rate in the global battery packaging material market, driven by large-scale battery manufacturing hubs in China, Japan, and South Korea, alongside strong demand from automotive and consumer electronics industries

- The Lithium Ion segment held the largest market revenue share in 2025, driven by its extensive adoption in electric vehicles, consumer electronics, and renewable energy storage systems. Lithium-ion batteries require highly durable and thermally stable packaging to ensure safety, which has led to growing demand for advanced polymer films, metal foils, and composite enclosures

Report Scope and Battery Packaging Material Market Segmentation

|

Attributes |

Battery Packaging Material Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Battery Packaging Material Market Trends

Shift Toward Sustainable and Recyclable Battery Packaging Solutions

- The growing emphasis on environmental sustainability is driving a significant shift toward recyclable and eco-friendly battery packaging materials. Manufacturers are increasingly adopting paper-based, bio-based polymers, and recyclable metal foils to minimize environmental impact and meet global sustainability mandates. This transition is especially prominent among electric vehicle (EV) and consumer electronics manufacturers seeking to align with circular economy goals. The initiative is also helping companies enhance brand image, comply with global ESG standards, and attract eco-conscious investors across developed and emerging markets

- The demand for green packaging solutions is further accelerated by stringent regulations across major economies such as the U.S., China, and European countries, which are enforcing limits on hazardous waste and encouraging sustainable production practices. This regulatory support is compelling battery producers to incorporate recyclable packaging materials into their supply chains, promoting industry-wide innovation. As a result, the number of sustainable packaging patents and pilot programs has surged globally, encouraging collaboration between chemical firms and battery manufacturers

- Companies are also investing in life cycle assessments and material recovery technologies to enhance the recyclability and reusability of battery components. This not only helps in reducing waste but also optimizes resource efficiency and supports long-term cost savings across the battery ecosystem. Furthermore, innovations in chemical recycling and closed-loop manufacturing systems are being developed to reduce reliance on virgin materials, thereby promoting sustainable industrial ecosystems

- For instance, in 2024, several leading EV battery manufacturers in Europe collaborated with packaging firms to develop aluminum-based recyclable casings, improving both safety and sustainability standards. These solutions helped reduce material wastage while meeting strict EU environmental compliance norms. Such partnerships have set a benchmark for sustainable innovation, encouraging smaller firms to adopt similar approaches for scalable and cost-effective green packaging

- While sustainable battery packaging offers long-term benefits, the shift requires consistent R&D investment and standardization across global markets. Manufacturers must balance cost-effectiveness with performance, durability, and safety to ensure widespread adoption of eco-friendly packaging solutions. The integration of advanced testing, smart materials, and data-driven monitoring systems will be crucial to achieving mass adoption and reducing environmental impact throughout the battery lifecycle

Battery Packaging Material Market Dynamics

Driver

Rising Adoption of Electric Vehicles (EVs) and Energy Storage Systems (ESS)

- The accelerating global transition toward electric mobility and renewable energy integration is a major driver of the battery packaging material market. As the demand for lithium-ion and solid-state batteries surges, the need for durable, thermally stable, and protective packaging materials has increased significantly. EV manufacturers are prioritizing packaging that ensures safety, reliability, and longer battery lifespan. This demand has spurred innovations in lightweight composites and next-generation polymers designed for high-efficiency energy systems

- Energy storage systems used in renewable applications such as solar and wind power further contribute to demand growth. The deployment of large-scale ESS solutions requires robust packaging to prevent leakage, thermal runaway, and mechanical damage during storage and transportation. This has led to the development of new packaging designs that can withstand extreme temperatures and environmental stress, ensuring reliability and performance in grid-scale energy applications

- In addition, advancements in material technology, such as the use of high-performance polymers and metal composites, are enhancing the protective capabilities of battery packaging materials. These materials ensure high thermal resistance, lightweight properties, and improved mechanical strength, enabling safer and more efficient energy systems. Manufacturers are also integrating smart sensors within packaging to monitor temperature, pressure, and charge levels, ensuring greater operational safety and predictive maintenance

- For instance, in 2025, several major EV manufacturers in Asia-Pacific increased their procurement of advanced multilayer polymer films for lithium-ion batteries, citing their superior heat resistance and recyclability. This trend has driven innovation across the supply chain and expanded production capacity for high-performance packaging materials. The collaborations between polymer producers and EV companies are also helping establish new benchmarks for energy density, cost reduction, and performance optimization

- While EV and ESS adoption are accelerating market growth, maintaining consistency in global safety standards and reducing material costs are essential to ensure long-term market scalability and competitiveness. Continuous innovation in production technologies, such as automation and 3D printing, can help streamline manufacturing processes and reduce waste, further supporting market expansion

Restraint/Challenge

“High Cost of Advanced Packaging Materials and Complex Manufacturing Processes”

- The high production cost associated with advanced battery packaging materials, such as composite films and heat-resistant polymers, poses a major challenge for manufacturers. These materials often require precision engineering, specialized coatings, and high-temperature processing, significantly increasing overall production expenses. Small and medium-sized producers, in particular, struggle to achieve cost competitiveness, limiting large-scale adoption

- In addition, the complexity of designing packaging that meets both safety and environmental standards adds to manufacturing challenges. Producers must ensure compliance with transportation safety regulations while maintaining lightweight and compact designs suitable for EVs and portable electronics. The development of next-generation designs also demands significant testing and certification costs, extending product development timelines

- Limited availability of raw materials and supply chain disruptions further hinder cost efficiency, particularly in regions dependent on imports for specialized metals and polymers. This can lead to fluctuations in production timelines and overall pricing instability in the global market. Moreover, geopolitical tensions and logistics constraints have exacerbated material shortages, impacting long-term procurement strategies for key manufacturers

- For instance, in 2024, multiple Asian battery packaging suppliers reported cost surges due to rising raw material prices for aluminum and polymer films, affecting delivery schedules and margins for EV battery manufacturers. This trend highlighted the need for regional supply chain diversification and local material sourcing to mitigate risks associated with import dependency

- While advanced materials enhance performance and safety, addressing cost and production challenges through innovation in material science, recycling processes, and automation will be key to achieving large-scale affordability and sustainable market growth. Collaborative research programs and public-private partnerships can also accelerate innovation, reduce manufacturing costs, and ensure consistent quality across the global supply chain

Battery Packaging Material Market Scope

The market is segmented on the basis of battery type, material type, and packaging type.

- By Battery Type

On the basis of battery type, the battery packaging material market is segmented into Lithium Ion, Lead Acid, Nickel Cadmium, and Nickel Metal Hydride. The Lithium Ion segment held the largest market revenue share in 2025, driven by its extensive adoption in electric vehicles, consumer electronics, and renewable energy storage systems. Lithium-ion batteries require highly durable and thermally stable packaging to ensure safety, which has led to growing demand for advanced polymer films, metal foils, and composite enclosures.

The Nickel Metal Hydride segment is expected to witness the fastest growth rate from 2026 to 2033, fuelled by its increasing use in hybrid vehicles and portable electronic devices. Its stable performance, high energy density, and eco-friendly characteristics make it a preferred alternative to conventional battery types. Manufacturers are increasingly focusing on developing lightweight and recyclable packaging materials to support the expanding NiMH battery applications in automotive and industrial sectors.

- By Material Type

On the basis of material type, the market is segmented into Cardboard, Wood, Foam, and Plastics. The Plastics segment accounted for the largest market share in 2025 due to its versatility, lightweight nature, and superior resistance to moisture and corrosion. Plastic packaging materials such as polyethylene and polypropylene are widely used for both consumer and industrial batteries, offering durability and cost efficiency in large-scale transportation and storage.

The Foam segment is projected to grow at the fastest rate during the forecast period owing to its exceptional cushioning, thermal insulation, and shock absorption properties. Foam packaging is increasingly adopted for high-value batteries used in EVs and aerospace applications, where protection from vibration and impact is critical. Continuous advancements in eco-friendly foam formulations are also boosting its adoption in sustainable battery packaging solutions.

- By Packaging Type

On the basis of packaging type, the battery packaging material market is segmented into Corrugated, Wooden Boxes, and Plastic Cases. The Corrugated segment dominated the market in 2025, attributed to its low cost, recyclability, and flexibility in design. Corrugated boxes are extensively used for shipping and storing lead-acid and lithium-ion batteries, providing robust protection against external damage while ensuring compliance with international transport regulations.

The Plastic Cases segment is expected to witness the highest growth from 2026 to 2033, driven by their superior strength, durability, and adaptability for various battery chemistries. Plastic cases offer enhanced safety and longer lifespan compared to traditional materials, making them ideal for automotive and industrial applications. Furthermore, the growing focus on reusable and modular packaging systems is encouraging manufacturers to adopt innovative plastic case designs with improved sealing and fire-retardant properties.

Battery Packaging Material Market Regional Analysis

- North America dominated the battery packaging material market with the largest revenue share of 38.42% in 2025, driven by the rapid growth of electric vehicle (EV) production and strong demand for energy storage solutions across the region

- The region’s well-established automotive industry, along with extensive R&D investments in advanced battery technologies, has significantly increased the demand for safe, durable, and sustainable packaging materials

- The widespread presence of major battery manufacturers and the implementation of stringent environmental regulations are further propelling the market, ensuring high-quality packaging standards and promoting innovation in eco-friendly materials

U.S. Battery Packaging Material Market Insight

The U.S. battery packaging material market captured the largest revenue share in 2025 within North America, driven by strong growth in EV manufacturing and large-scale renewable energy storage projects. The country’s commitment to reducing carbon emissions and promoting sustainable mobility has boosted the demand for high-performance battery packaging. Furthermore, leading companies are investing in lightweight, thermally stable materials to ensure enhanced battery safety and compliance with transportation standards. The expansion of the domestic supply chain for lithium-ion batteries is also contributing to market stability and growth.

Europe Battery Packaging Material Market Insight

The Europe battery packaging material market is expected to witness substantial growth from 2026 to 2033, supported by the EU’s strict environmental policies and rising demand for EVs and grid storage systems. The European Union’s focus on circular economy principles and reduction of hazardous waste is encouraging the adoption of recyclable and biodegradable packaging materials. Moreover, ongoing investments in gigafactories across Germany, France, and Sweden are boosting local production and creating opportunities for sustainable packaging manufacturers.

U.K. Battery Packaging Material Market Insight

The U.K. battery packaging material market is expected to witness the fastest growth rate from 2026 to 2033, fuelled by the country’s increasing focus on EV adoption and renewable energy storage systems. The government’s commitment to phase out internal combustion engines and support domestic battery manufacturing is enhancing demand for innovative packaging solutions. British manufacturers are also investing in recyclable and lightweight materials to meet sustainability goals and reduce import dependency.

Germany Battery Packaging Material Market Insight

The Germany battery packaging material market is expected to witness substantial growth from 2026 to 2033, driven by the country’s strong automotive sector and commitment to green technology. The presence of leading EV manufacturers and battery producers is fostering innovation in advanced packaging materials with high thermal and mechanical resistance. Furthermore, initiatives to establish local supply chains for lithium-ion and solid-state batteries are enhancing demand for sustainable, high-performance packaging materials.

Asia-Pacific Battery Packaging Material Market Insight

The Asia-Pacific battery packaging material market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, urbanization, and surging demand for electric mobility in countries such as China, Japan, and India. The region’s expanding manufacturing capacity for EV batteries and energy storage systems is creating strong demand for durable and cost-effective packaging materials. In addition, favorable government policies supporting local production and recycling initiatives are strengthening market growth.

Japan Battery Packaging Material Market Insight

The Japan battery packaging material market is projected to expand significantly from 2026 to 2033, driven by the country’s advanced technology ecosystem and focus on sustainable innovation. Japan’s growing EV production and the development of next-generation solid-state batteries are increasing the need for high-strength and thermally efficient packaging materials. The government’s push toward carbon neutrality is further promoting the adoption of recyclable and eco-friendly packaging solutions across battery applications.

China Battery Packaging Material Market Insight

The China battery packaging material market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to its dominance in global battery manufacturing and raw material processing. The country’s strong presence in the EV and consumer electronics sectors continues to fuel demand for high-quality packaging materials. Government initiatives promoting local production, recycling, and the use of sustainable materials are accelerating market expansion. In addition, domestic innovation in composite and metal-based packaging materials is enhancing the competitiveness of Chinese manufacturers in global markets.

Battery Packaging Material Market Share

The Battery Packaging Material industry is primarily led by well-established companies, including:

• Targray (Canada)

• Amcor plc (U.K.)

• Owens-Illinois Inc. (U.S.)

• NEFAB GROUP (Sweden)

• International Paper (U.S.)

• CL Smith (U.S.)

• Mondi (U.K.)

• Stora Enso (Finland)

• Wellplast AB (Sweden)

• Heitkamp & Thumann Group (Germany)

• DS Smith (U.K.)

• DHL International GmbH (Germany)

• Epec, LLC (U.S.)

• Smurfit Kappa (Ireland)

• WestRock Company (U.S.)

• Rogers Corporation (U.S.)

• Coveris (Austria)

• United Parcel Service of America, Inc. (U.S.)

• Umicore (Belgium)

• ZARGES GmbH (Germany)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Battery Packaging Material Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Battery Packaging Material Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Battery Packaging Material Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.