Global Bean Syndrome Treatment Market

Market Size in USD Billion

USD

1.29 Billion

USD

2.15 Billion

2025

2033

USD

1.29 Billion

USD

2.15 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.29 Billion | |

| USD 2.15 Billion | |

| % | |

|

Bean Syndrome Treatment Market Size

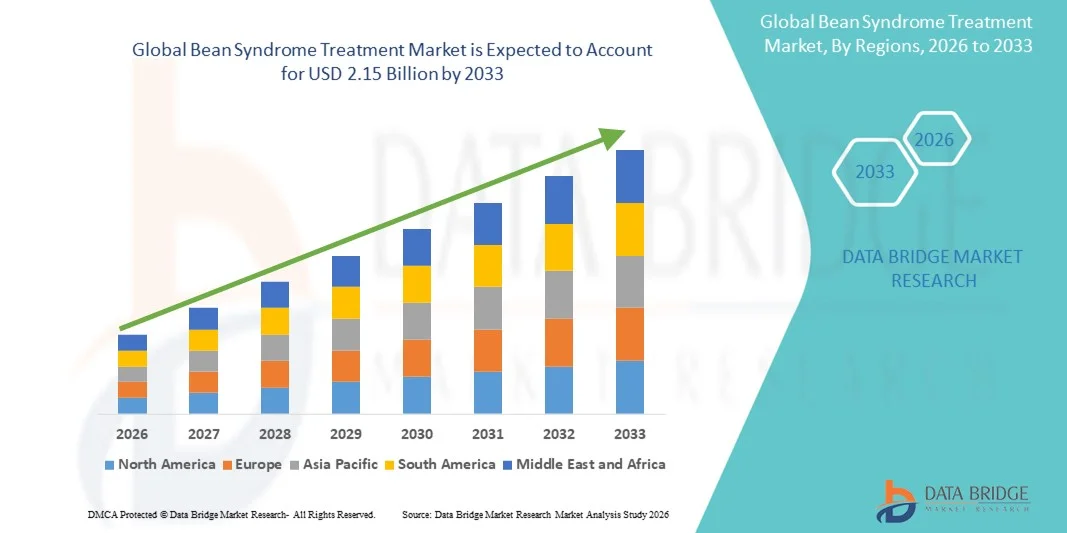

- The global bean syndrome treatment market size was valued at USD 1.29 billion in 2025 and is expected to reach USD 2.15 billion by 2033, at a CAGR of 6.60% during the forecast period

- The market growth is largely fueled by the increasing recognition of Bean Syndrome as a serious genetic and developmental condition, driving higher diagnostic rates and the need for early-stage medical intervention. Advancements in genetic testing, biomarker research, and specialized pediatric care are also contributing to improved identification and management of the disorder, thereby supporting market expansion

- Furthermore, rising investments in rare-disease research, supportive regulatory pathways, and growing awareness among clinicians and families are creating strong demand for safer, more effective, and targeted therapeutic approaches. These converging factors are accelerating the uptake of Bean Syndrome Treatment solutions, thereby significantly boosting the industry's growth

Bean Syndrome Treatment Market Analysis

- Bean Syndrome Treatment solutions, which include genetic testing, symptomatic therapies, and supportive pediatric interventions, are becoming increasingly vital in managing this rare developmental disorder. Their importance is rising due to improved early-diagnosis capabilities, expanding clinical research, and increasing awareness among healthcare providers and families

- The escalating demand for bean syndrome treatment is primarily fueled by advancements in genomics, a growing emphasis on early rare-disease detection, and increasing availability of specialized pediatric healthcare services that prioritize accurate diagnosis and long-term management

- North America dominated the bean syndrome treatment market with the largest revenue share of 38.5% in 2025, characterized by strong rare-disease research infrastructure, early adoption of advanced diagnostic tools, higher healthcare spending, and a robust presence of biotechnology companies developing targeted therapies. The U.S. contributes the largest share due to expanding genetic testing programs and supportive reimbursement policies

- Asia-Pacific is expected to be the fastest-growing region in the bean syndrome treatment market during the forecast period, registering a CAGR of 11.8%, driven by increasing awareness of genetic disorders, improving pediatric healthcare facilities, and rising investment in diagnostic technologies across emerging economies

- The oral segment dominated the largest market revenue share of 46.2% in 2025, primarily due to its widespread use for administering corticosteroids, immunomodulators, and long-term symptom management therapies

Report Scope and Bean Syndrome Treatment Market Segmentation

|

Attributes |

Bean Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Bean Syndrome Treatment Market Trends

Increasing Focus on Early Diagnosis, Symptom Management, and Advanced Therapeutics

- A significant and accelerating trend in the global bean syndrome treatment market is the growing emphasis on early detection, timely intervention, and the development of more specialized therapeutic approaches as awareness increases across both clinical and patient communities. This shift reflects the rising number of identified cases and the growing medical need for more structured management protocols across hospitals, clinics, and specialty centers

- For instance, several healthcare networks in 2024 expanded their diagnostic programs to incorporate routine screening panels and symptom-tracking pathways specifically aimed at identifying Bean Syndrome at earlier stages, improving treatment outcomes and patient monitoring efficiency

- Advancements in symptomatic care are also shaping the market, with treatments increasingly tailored to address complex manifestations such as neuromuscular instability, inflammation, and metabolic disruptions. Some clinical centers are adopting enhanced protocols that rely on structured dosing patterns, patient-specific formulations, and stepwise progression models to improve therapeutic response consistency

- Supportive care advancements, including improved hospital-based monitoring systems, more refined emergency management tools, and better integration between primary and specialty care, are enabling healthcare providers to deliver more efficient and coordinated treatment plans

- The market is further influenced by a shift towards combination therapies, where multiple medications are administered simultaneously or sequentially to manage overlapping symptoms commonly associated with Bean Syndrome. This multidisciplinary approach is expanding across major medical institutions

- As a result, companies operating in the pharmaceutical and medical services sectors are investing in research aimed at refining treatment regimens, expanding clinical evidence, and improving patient-centered outcomes. This trend is pushing the market toward more comprehensive, structured, and evidence-based Bean Syndrome management systems across both developed and emerging regions

- Growing awareness campaigns, improved caregiver training, and expanded access to specialized medical facilities are also driving the trend toward earlier intervention and broader recognition of patient needs

- Consequently, the market is undergoing a notable shift toward more integrated and patient-adaptive treatment models that combine preventive, symptomatic, and supportive care, marking a significant evolution in how Bean Syndrome is clinically approached

Bean Syndrome Treatment Market Dynamics

Driver

Growing Need Due to Rising Symptom Burden and Expanding Clinical Awareness

- The rising prevalence of bean syndrome symptoms across multiple age groups, combined with improved disease recognition among clinicians, is a key driver in increasing the demand for more structured and accessible treatment options. As hospitals and clinics become more aware of the complexity of the condition, they are adopting broader treatment frameworks to address diverse patient needs

- For instance, in March 2025, several regional healthcare systems announced the expansion of their neurology-linked care units to support more efficient Bean Syndrome diagnostic workflows, enabling faster treatment initiation and improved patient monitoring strategies throughout the care timeline

- With increasing attention on severe and recurrent symptoms, patients and caregivers are seeking medical support earlier, fueling demand for both prescription and supportive therapies. Expanded access to laboratory diagnostics and increased physician training also contribute to more consistent case identification

- Growing healthcare investments and the introduction of improved pharmacological options enhance treatment effectiveness while encouraging adoption across both public and private healthcare environments

- The rise of structured outpatient management programs, caregiver education modules, and rehabilitation support services further strengthens the market by improving long-term patient outcomes

- Telemedicine, digital patient tracking, and remote consultation services are also improving accessibility for patients seeking regular symptom management, thus contributing to the broader market uplift

- Altogether, the combination of increased symptom burden, expanding awareness, enhanced medical infrastructure, and improved treatment accessibility is supporting the continuous growth of the Bean Syndrome Treatment market across global regions

Restraint/Challenge

Clinical Limitations, Treatment Variability, and High Management Costs

- Several challenges continue to restrict broader adoption and optimized management of Bean Syndrome, including inconsistencies in disease presentation, limited standardized treatment guidelines, and varying levels of physician experience in handling the condition. These factors contribute to delays in appropriate therapeutic choices and inconsistent outcomes across patient groups

- For instance, the absence of uniform diagnostic protocols in many healthcare systems has resulted in delayed or missed early-stage identification, creating complications in disease management and leading to increased dependence on advanced-stage interventions

- In addition, high treatment costs—especially for specialized medications, repeat diagnostic procedures, and long-term supportive therapies—pose barriers for many patients, particularly in low-resource regions where healthcare funding and insurance coverage remain limited

- The lack of widespread clinical expertise also limits the availability of specialized care, as many general practitioners may not be fully familiar with the full symptom spectrum of Bean Syndrome, leading to underdiagnosis or incomplete management strategies

- Furthermore, the availability of advanced diagnostic tools and specialized therapeutic formulations varies significantly across regions, creating disparities in patient outcomes

- Ongoing challenges surrounding treatment adherence—especially for long-duration regimens—also affect therapeutic success rates

- Overcoming these barriers will require improved clinical training, development of standardized care pathways, broader insurance inclusion, and increased investment in accessible, cost-effective treatment alternatives to support consistent market expansion

Bean Syndrome Treatment Market Scope

The market is segmented on the basis of drug type, treatment, diagnosis, dosage, route of administration, end-users, and distribution channel.

- By Drug Type

On the basis of drug type, the Bean Syndrome Treatment market is segmented into corticosteroids, interferon-alpha, intravenous gamma globulin, vincristine, and sirolimus. The corticosteroids segment dominated the largest market revenue share of 39.4% in 2025, supported by their long-established role in reducing inflammation, alleviating pain, and controlling acute swelling episodes associated with Bean Syndrome. Their widespread clinical acceptance, low cost, and immediate therapeutic effect make corticosteroids the first treatment option recommended in both hospital and outpatient settings. Increasing availability of oral and injectable formulations further strengthens their adoption across diverse patient groups. Physicians continue to rely on corticosteroids for rapid symptom stabilization, especially in cases involving progressive vascular lesions. The strong presence of corticosteroids in global treatment guidelines and their ease of integration into combination therapies reinforce their dominant use. Additionally, their broad accessibility through hospital and retail pharmacies supports continued utilization. Growing diagnosis rates and rising patient visits to specialty clinics also contribute to sustained demand, helping corticosteroids remain the primary and most widely used therapeutic class in the market.

The sirolimus segment is anticipated to witness the fastest growth rate of 18.6% CAGR from 2026 to 2033, driven by its increasing recognition as an effective targeted therapy for complex vascular and lymphatic malformations associated with Bean Syndrome. Rising clinical evidence supporting the role of mTOR inhibition in reducing lesion size and improving functional outcomes is compelling physicians to adopt sirolimus earlier in treatment pathways. The drug’s ability to offer long-term control for patients unresponsive to corticosteroids or conventional immunotherapies is boosting its demand across specialized care centers. Growing availability of real-world clinical data from tertiary hospitals is also accelerating physician confidence. Oral formulations that support daily dosing convenience improve patient adherence, particularly in pediatric cases where non-invasive management is preferred. The inclusion of sirolimus in emerging international treatment protocols further encourages adoption. Growing patient awareness of advanced targeted options and increasing referrals to specialty vascular anomaly centers expand its clinical reach. As rare disease research accelerates globally, greater investment in mTOR-based therapies continues to support market expansion, establishing sirolimus as the fastest-growing drug type during the forecast period.

- By Treatment

On the basis of treatment, the Bean Syndrome Treatment market is segmented into iron therapy, blood transfusions, laser therapy, surgery, sclerotherapy, and medication. The medication segment dominated the largest market revenue share of 42.7% in 2025, supported by its essential role in managing chronic symptoms, reducing vascular complications, and stabilizing patients across all severity levels of the condition. Medications such as corticosteroids, sirolimus, and immunomodulators remain widely prescribed due to their effectiveness in lowering inflammation, controlling lesion progression, and improving overall quality of life. Their ease of administration and compatibility with long-term management strategies make them the most frequently utilized option across hospitals, clinics, and outpatient departments. The availability of both oral and injectable formulations further strengthens their demand across pediatric and adult patient groups. Medications are also the first-line approach before considering invasive procedures, making them central to clinical treatment pathways. Increased patient awareness, rising diagnosis rates, and expanding pharmaceutical access across emerging markets continue to reinforce the dominance of medication-based management. The growing adoption of combination therapy approaches also contributes to sustained market leadership for medications.

Blood transfusions are expected to witness the fastest growth rate of 17.9% CAGR from 2026 to 2033, driven by rising recognition of their importance in managing severe anemia, acute bleeding complications, and advanced-stage Bean Syndrome presentations. Increasing hospitalization rates for critical episodes requiring urgent correction of hemoglobin levels and restoration of blood volume support the rising use of transfusion therapy. Improvements in blood bank infrastructure, growing availability of screened donor blood, and advancements in transfusion safety protocols enhance adoption across developed and developing regions. Physicians increasingly recommend transfusions when patients exhibit rapid clinical deterioration or fail to respond adequately to medication-based interventions. Growing awareness about comprehensive management for rare syndromes further boosts adoption as multidisciplinary treatment centers emphasize timely transfusion support. Increasing integration of transfusion procedures within hospital emergency units enhances access and accelerates clinical decisions. As patient monitoring and hemovigilance systems improve globally, the reliability and safety of transfusions strengthen physician and patient confidence, driving sustained growth. Rising investments in healthcare systems and improved access to specialized care facilities further support strong market expansion for transfusion-based treatments during the forecast period.

- By Diagnosis

On the basis of diagnosis, the Bean Syndrome Treatment market is segmented into blood counts, endoscopy, ultrasound, CT scan, MRI, and histopathology. The blood counts segment dominated the largest market revenue share of 36.8% in 2025, owing to its essential role as the first-line diagnostic approach for identifying anemia, infection, systemic inflammation, and other hematological abnormalities associated with Bean Syndrome. Complete blood count testing is widely accessible, cost-effective, and routinely performed across clinics, hospitals, and diagnostic laboratories, making it a primary investigation during initial patient evaluation. Physicians rely heavily on blood count parameters to determine disease severity, guide treatment decisions, and monitor responses to therapy over time. The ability of blood tests to deliver rapid results supports early diagnosis and immediate intervention, particularly in acute or deteriorating cases. Expanding diagnostic infrastructure in emerging healthcare markets and increasing patient screening rates further strengthen the dominance of blood counts. Their critical role in ongoing patient monitoring, management of treatment complications, and long-term follow-up ensures consistent demand. As awareness and early detection programs improve, blood count testing continues to be the most widely utilized diagnostic method across all stages of care.

MRI is anticipated to witness the fastest growth rate of 19.1% CAGR from 2026 to 2033, driven by its superior ability to visualize deep tissue abnormalities, vascular malformations, and complex lesions often associated with Bean Syndrome. MRI provides high-resolution imaging without radiation exposure, making it suitable for pediatric and recurrent cases requiring repeated evaluation. Increasing physician preference for advanced imaging techniques that offer detailed structural assessment is boosting demand, especially in specialized care centers. MRI helps clinicians differentiate between lesion types, assess the extent of vascular involvement, and plan surgical or interventional procedures with greater accuracy. Technological advancements, including faster imaging sequences and enhanced contrast agents, further elevate diagnostic precision. The rising establishment of dedicated radiology units in hospitals and multispecialty centers improves access to MRI services. As rare disease management shifts toward more comprehensive evaluation, MRI’s role in confirming complex diagnoses continues to expand. Enhanced diagnostic capabilities and increasing referrals from hematologists and vascular specialists significantly contribute to its strong growth trajectory during the forecast period.

- By Dosage

On the basis of dosage, the Bean Syndrome Treatment market is segmented into tablet, injection, capsule, and others. The tablet segment dominated the largest market revenue share of 44.9% in 2025, driven by its widespread use in administering corticosteroids, sirolimus, and other long-term medications essential for managing Bean Syndrome. Tablets are favored for their convenience, accurate dosing, extended shelf life, and suitability for chronic therapy, ensuring strong adherence among adult as well as adolescent patient populations. Their ease of distribution through pharmacies and availability across multiple dosage strengths further support widespread adoption. Tablets are the preferred route in outpatient and routine care settings, where patients require sustained symptom control without invasive interventions. The affordability and simple storage requirements of tablet formulations enhance accessibility across low- and middle-income regions. Physicians continue to prescribe tablets for maintenance therapy, relapse prevention, and gradual tapering schedules. High patient acceptability and compatibility with combination regimens reinforce the dominance of tablets in treatment pathways. Continued pharmaceutical advancements and the introduction of improved oral formulations support steady demand, ensuring tablets remain the leading dosage form in the global market.

The injection segment is expected to witness the fastest growth rate of 18.4% CAGR from 2026 to 2033, supported by the increasing use of intravenous and intramuscular formulations for managing severe complications of Bean Syndrome. Injections are critical in emergency cases requiring rapid stabilization, including acute swelling, severe inflammation, or progression of vascular lesions. Physicians prefer injectable corticosteroids, immunoglobulins, and targeted therapies for their fast onset of action and high bioavailability, making them essential in hospital-based care. Growing adoption of biologics and immunomodulators delivered via injections further strengthens demand. Rising hospitalization rates and the expansion of specialized centers increase access to injection-based treatments globally. The ability to precisely control dosing and achieve strong therapeutic response boosts physician confidence in injectable therapies. Additionally, injections are increasingly used in pre-surgical preparation and post-procedure stabilization, enhancing their role in multidisciplinary care. As healthcare systems expand critical care and infusion units, the utilization of injectable treatments is expected to rise significantly, contributing to its robust growth throughout the forecast period.

- By Route of Administration

On the basis of route of administration, the Bean Syndrome Treatment market is segmented into intramuscular, intravenous, oral, and others. The oral segment dominated the largest market revenue share of 46.2% in 2025, primarily due to its widespread use for administering corticosteroids, immunomodulators, and long-term symptom management therapies. Oral administration is preferred by both patients and healthcare providers for its convenience, non-invasive nature, and ability to support prolonged treatment regimens required for chronic conditions such as Bean Syndrome. The availability of multiple oral dosage forms, including tablets and capsules, enhances treatment flexibility and patient adherence. Oral therapies are also more accessible across pharmacies, making them widely used in both developed and emerging regions. The ease of self-administration reduces dependency on clinical visits, supporting greater patient autonomy. Physicians consistently prescribe oral therapies for initial stabilization, maintenance, and follow-up care. Growing awareness, increased screening rates, and improved access to pharmaceutical supplies further strengthen the segment. The critical role of oral drugs in disease management and relapse prevention ensures the segment’s continued dominance across global markets.

The intravenous segment is anticipated to witness the fastest growth rate of 19.5% CAGR from 2026 to 2033, driven by rising demand for hospital-based administration of immunoglobulins, corticosteroids, and investigational agents used in severe or rapidly progressing cases of Bean Syndrome. Intravenous delivery provides immediate therapeutic impact with controlled dosing, making it a preferred option for acute care and complex treatment protocols. Growing adoption of IV-based targeted therapies and infusion regimens enhances its relevance in specialized centers. Increasing hospitalization for advanced-stage complications supports higher utilization of intravenous administration. Infrastructure improvements, including expanded infusion suites and better-trained nursing staff, are further facilitating adoption across hospitals and tertiary care centers. IV routes are also essential for delivering supportive care such as fluids and emergency treatments. As research pipelines advance, more intravenous formulations are entering clinical use, contributing to the segment’s strong projected growth. The ability to manage critical cases efficiently and reliably positions the intravenous segment as the fastest-growing route of administration.

- By End-Users

On the basis of end-users, the Bean Syndrome Treatment market is segmented into clinic, hospital, and others. The hospital segment dominated the largest market revenue share of 53.1% in 2025, driven by the high concentration of diagnostic imaging, laboratory facilities, and multidisciplinary expertise required for managing Bean Syndrome. Hospitals remain the primary care setting for patients presenting with severe symptoms, complex vascular lesions, or life-threatening complications requiring immediate intervention. Advanced treatment options, including intravenous therapy, blood transfusions, and surgical procedures, are largely administered in hospital environments. The presence of specialized units such as hematology, radiology, and pediatric departments further strengthens hospital-based care. Growing patient admissions, increased awareness programs, and referral patterns from primary care centers contribute to higher patient flow. Hospitals also lead in adopting advanced medical technologies and implementing standardized treatment guidelines. As rare disease management becomes more centralized, hospitals continue to dominate due to their comprehensive facilities and ability to handle critical cases effectively.

The clinic segment is expected to witness the fastest growth rate of 15.8% CAGR from 2026 to 2033, driven by rising demand for accessible outpatient care, early diagnosis, follow-up consultations, and non-invasive treatment interventions for Bean Syndrome. Clinics play a vital role in managing mild to moderate symptoms, performing blood tests, and offering routine monitoring for patients on long-term therapy. Increasing establishment of specialty clinics focusing on rare diseases and vascular anomalies contributes to greater patient footfall. Clinics provide a cost-effective alternative to hospitals, improving accessibility for patients requiring regular follow-up visits and therapeutic adjustments. Growing awareness among healthcare providers and expanding diagnostic capabilities in outpatient settings further encourage clinic-based care. Enhanced patient convenience, reduced waiting time, and closer community reach support increasing preference for clinic services. As early detection programs expand, more patients are expected to seek initial screening and ongoing care through clinics, contributing to strong growth during the forecast period.

- By Distribution Channel

On the basis of distribution channel, the Bean Syndrome Treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The retail pharmacy segment dominated the largest market revenue share of 45.3% in 2025, supported by its extensive presence across urban and rural regions, making it the most accessible platform for obtaining medications used in the ongoing management of Bean Syndrome. Retail pharmacies dispense a wide range of oral and injectable therapies, including corticosteroids, immunomodulators, and supportive medications, ensuring continuous availability for chronic treatment needs. Their ability to offer pharmacist consultations, flexible operating hours, and immediate product access drives high patient reliance. Retail pharmacies also support prescription refills and provide guidance on dosage scheduling, enhancing treatment adherence. Expansion of pharmaceutical chains and improved inventory systems further strengthen their role in treatment accessibility. The increasing volume of outpatient visits and follow-up care supports regular demand for retail-dispensed medications. Strong distribution networks and integration with insurance systems contribute to the segment’s continued dominance.

The online pharmacy segment is anticipated to witness the fastest growth rate of 20.4% CAGR from 2026 to 2033, driven by rising digital adoption, home-delivery preferences, and increasing acceptance of teleconsultation-based prescription services. Online platforms offer significant convenience for chronic condition management, allowing patients to refill prescriptions and access medications without visiting physical stores. Growing internet penetration, secure payment systems, and improved cold-chain logistics enable reliable delivery of temperature-sensitive drugs, including certain immunotherapies. Online pharmacies also provide competitive pricing, subscription-based refill models, and automated reminders, improving adherence for long-term therapy. Increasing trust in accredited e-pharmacy platforms and regulatory support for digital medicine distribution further boost adoption. Patients in remote or underserved regions significantly benefit from online access to specialized medications. As digital healthcare ecosystems expand, the shift toward online procurement of Bean Syndrome therapies is expected to accelerate sharply throughout the forecast period.

Bean Syndrome Treatment Market Regional Analysis

- North America dominated the bean syndrome treatment market with the largest revenue share of 38.5% in 2025, driven by strong clinical networks, established rare-disease research infrastructure, and widespread availability of diagnostic and treatment services across tertiary hospitals and specialty clinics

- Clinicians and caregivers in the region highly value rapid access to standardized pharmacologic regimens (notably corticosteroids and increasingly sirolimus), robust therapeutic monitoring, and integrated multidisciplinary care pathways that support long-term management and pre-procedural stabilization

- This widespread adoption is further supported by comprehensive insurance coverage in many markets, active clinical research programs, and the presence of key pharmaceutical and diagnostic service providers that facilitate access to advanced therapies and clinical trials

U.S. Bean Syndrome Treatment Market Insight

The U.S. bean syndrome treatment market captured the largest revenue share in 2025 within North America, fueled by concentrated expertise at pediatric and vascular-anomaly centers, high rates of genetic testing and advanced imaging use, and rapid clinical uptake of targeted therapies such as sirolimus under specialized monitoring protocols. Leading academic hospitals and collaborative clinical networks have driven early adoption of novel regimens, established standardized dosing and safety pathways, and expanded outpatient infusion and monitoring capacity — all of which support high utilization of both established agents (corticosteroids) and newer targeted drugs. In addition, strong payer engagement for rare-disease management programs and philanthropic/grant support for access initiatives have improved treatment continuity and facilitated broader uptake across both urban and suburban health systems.

Europe Bean Syndrome Treatment Market Insight

The Europe bean syndrome treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by centralized specialty centers, national rare-disease strategies that prioritize early diagnosis, and growing harmonization of clinical guidelines that recommend both conventional agents and targeted therapies for eligible patients. Public healthcare systems in countries such as the U.K. and Germany emphasize referral to centers of excellence, where multidisciplinary protocols (imaging, pharmacology, interventional procedures) are used to optimize outcomes and manage costs.

U.K. Bean Syndrome Treatment Market Insight

The U.K. bean syndrome treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the NHS’s rare-disease frameworks, strong pediatric referral networks, and increasing use of diagnostic pathways (genetic testing and MRI) that facilitate prompt specialist care. The U.K.’s clinical-community linkages and regional centers of expertise promote guideline-driven medication use and access to minimally invasive procedures when appropriate.

Germany Bean Syndrome Treatment Market Insight

The Germany bean syndrome treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by well-resourced hospital systems, advanced imaging and interventional radiology capacity, and coordinated specialist networks that enable safe administration of systemic agents (including sirolimus) with therapeutic drug monitoring. Germany’s emphasis on evidence-based practice and reimbursement support for complex care further underpins adoption.

Asia-Pacific Bean Syndrome Treatment Market Insight

The Asia-Pacific bean syndrome treatment market is poised to grow at the fastest regional CAGR during the forecast period, driven by rapid expansion of tertiary care hospitals, improvements in diagnostic capability (genetic testing and imaging), and rising investments in pediatric specialty services across China, India, Japan, and Australia. Growing awareness, expanding insurance penetration, and center-led adoption of newer targeted therapies are key growth levers in the region.

Japan Bean Syndrome Treatment Market Insight

The Japan bean syndrome treatment market is gaining momentum due to the country’s advanced diagnostic infrastructure, high clinician familiarity with imaging-guided care, and controlled adoption of targeted therapies supported by post-marketing surveillance and rigorous clinical practice guidelines. Japanese centers emphasize safety monitoring and long-term follow-up, which supports uptake of both established and novel therapies.

China Bean Syndrome Treatment Market Insight

The China bean syndrome treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing hospital capacity, growing specialist referral networks, and rapid expansion of diagnostic labs offering genetic testing and MRI. Domestic hospital networks and leading tertiary centers are scaling experience with targeted agents and minimally invasive procedures, driving strong absolute volume growth.

Bean Syndrome Treatment Market Share

The Bean Syndrome Treatment industry is primarily led by well-established companies, including:

- Pfizer (U.S.)

- Novartis (Switzerland)

- Roche (Switzerland)

- Johnson & Johnson (U.S.)

- Sanofi (France)

- Bayer (Germany)

- Merck & Co. (U.S.)

- AbbVie (U.S.)

- Takeda Pharmaceutical (Japan)

- Bristol Myers Squibb (U.S.)

- Amgen (U.S.)

- GlaxoSmithKline (U.K.)

- Eli Lilly (U.S.)

- Thermo Fisher Scientific (U.S.)

- Siemens Healthineers (Germany)

- GE Healthcare (U.S.)

- PerkinElmer (U.S.)

- Fresenius Medical Care (Germany)

- Medtronic (Ireland)

- Grifols (Spain)

Latest Developments in Global Bean Syndrome Treatment Market

- In May 2021, a significant clinical study published in The American Journal of Gastroenterology demonstrated that sirolimus therapy led to a notable reduction in venous malformation size and improved hemoglobin stability in BRBNS patients. This study highlighted sirolimus as a promising long-term therapy, reducing transfusion needs and improving overall quality of life

- In July 2021, a detailed case report and literature review confirmed that sirolimus showed consistent therapeutic benefits in severe BRBNS cases, particularly those with gastrointestinal bleeding. The publication emphasized that sirolimus improved lesion regression and offered a safer alternative to repeated surgeries

- In August 2021, a neonatal BRBNS case study described that long-term sirolimus treatment in a 38-day-old infant led to stable hemoglobin levels, fewer bleeding episodes, and improved lesion control. This was one of the earliest documented successful treatments in a neonatal patient, strengthening sirolimus’s role in pediatric BRBNS management

- In May 2022, two BRBNS cases published in a genetics-linked clinical report showed that low-dose sirolimus was highly effective, particularly in patients with TEK gene mutations. The study suggested that TEK mutation-positive cases may respond better to mTOR inhibition, marking a step toward personalized therapy for BRBNS

- In April 2023, a Frontiers in Pediatrics case report presented a neonate with BRBNS complicated by Kasabach–Merritt phenomenon, who responded rapidly to low-dose sirolimus combined with glucocorticoids. The therapy reversed coagulopathy, improved platelet counts, and significantly reduced vascular lesions, reinforcing sirolimus as a frontline option for complex BRBNS cases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.