Global Beer Cans Market

Market Size in USD Billion

USD

14.30 Billion

USD

19.03 Billion

2025

2033

USD

14.30 Billion

USD

19.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.30 Billion | |

| USD 19.03 Billion | |

| % | |

|

Beer Cans Market Overview

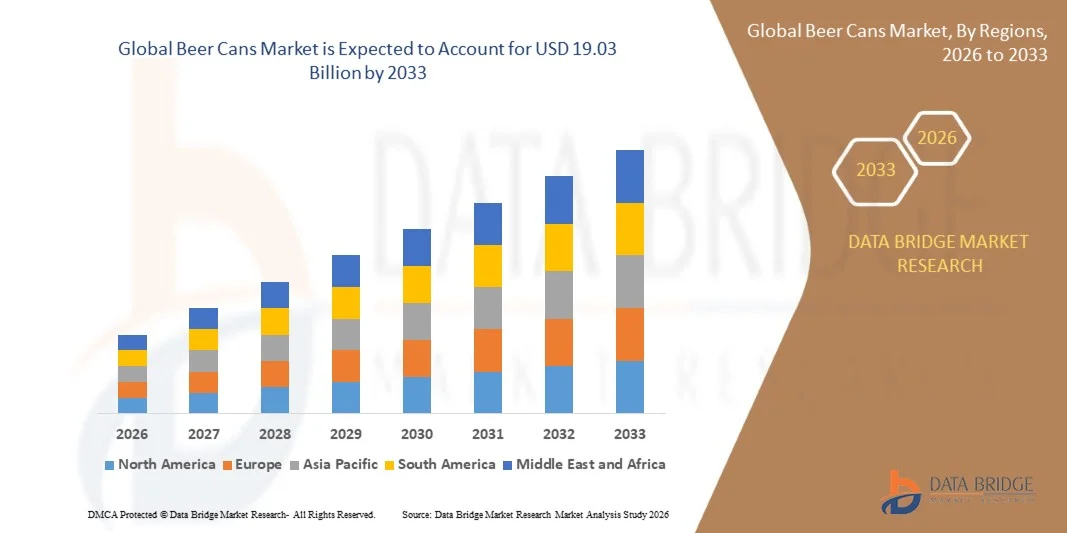

The Beer Cans Market was valued at USD 14.30 Billion in 2025 and is projected to reach USD 19.03 Billion by 2033, growing at a CAGR of 3.64% from 2026 to 2033. The market is experiencing consistent growth driven by rising global beer consumption, increasing demand for lightweight and recyclable beverage packaging, and growing preference for convenient on-the-go consumption formats. Expanding investments in sustainable aluminum packaging solutions and continuous advancements in can manufacturing technologies are further supporting market expansion across developed and emerging economies.

The increasing global focus on sustainable packaging and circular economy initiatives, combined with growing consumer awareness regarding environmental responsibility, is encouraging breweries to adopt highly recyclable beer cans over alternative packaging formats. Beer cans offer advantages such as lower transportation costs, improved product protection, extended shelf life, and enhanced branding opportunities. In addition, the rapid growth of craft breweries, premium beer offerings, and ready-to-drink alcoholic beverages is further driving demand for innovative and efficient beer can packaging solutions worldwide.

Key Market Trends & Insights

- North America dominated the Beer Cans Market with the largest revenue share of 35% in 2025, supported by high beer consumption, strong demand for convenient beverage packaging, and widespread adoption of sustainable aluminum cans

- The aluminum segment led the market with a 74.2% share in 2025, driven by its lightweight nature, excellent recyclability, and strong barrier properties against light and oxygen

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 5.62% from 2026 to 2033, fueled by rising beer consumption, rapid urbanization, and expanding middle-class populations across major economies

- 500ml is the fastest-growing capacity type, projected to register a CAGR of 6.2% from 2026 to 2033, supported by increasing consumer preference for larger serving sizes and value-oriented packaging formats

- The Pressure Filling segment dominated the filling method category with a 72.8% revenue share in 2025, led by its ability to efficiently handle carbonated beverages while preserving product quality and carbonation levels

- 2 piece cans accounted for 68.4% of the market in 2025, preferred by their lightweight structure, superior durability, and cost-efficient manufacturing process

- The vacuum filling segment is the fastest-growing filling method category, with a CAGR of 5.9% from 2026 to 2033, driven by increasing adoption among specialty and craft beer manufacturers seeking enhanced filling precision

Market Size & Forecast

- Global Market Value (2025): USD 14.30 Billion

- Expected Market Value (2033): USD 19.03 Billion

- Forecast CAGR (2026–2033): 3.64%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Beer Cans Market Segmentation

|

Attributes |

Beer Cans Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Crown Holdings, Inc. (U.S.) · Ball Corporation (U.S.) · CAN-PACK S.A. (Poland) · Shenzhen Xin Yuheng Can Co., Ltd. (China) · Daiwa Can Company, Ltd. (Japan) · Kaufman Container (U.S.) · Orora Packaging Australia Pty Ltd (Australia) · Nampak Ltd. (South Africa) · East Asia Beer Packaging Limited (Hong Kong) · Ardagh Metal Packaging S.A. (Luxembourg) · Baosteel Packaging Co., Ltd. (China) · CPMC Holdings Limited (China) · Toyo Seikan Group Holdings, Ltd. (Japan) · Showa Aluminum Can Corporation (Japan) · Envases Universales Group (Mexico) · Massilly Holding SAS (France) |

|

Market Opportunities |

· Expansion of Craft Brewery Packaging in Emerging Markets · Growth of Premium and Customized Digital-Printed Beer Cans · Increasing Demand for High-Recycled-Content Aluminum Beverage Packaging |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Beer Cans Market Trends

Trend: Rising Adoption of Sustainable and Lightweight Aluminum Beer Cans

Beer manufacturers are increasingly shifting toward lightweight aluminum cans as sustainability becomes a key priority across the beverage packaging industry. Aluminum cans offer high recyclability, lower transportation emissions, and improved resource efficiency compared to many alternative packaging formats. Growing consumer preference for environmentally responsible products is encouraging breweries to increase the use of recycled-content packaging while reducing overall material consumption. Advancements in can manufacturing technologies are further enabling thinner and lighter cans without compromising strength or product protection.

Companies such as Ball Corporation and Crown Holdings, Inc. continue to invest in lightweight can innovations and sustainable packaging solutions. According to the Aluminum Association, aluminum beverage cans remain one of the most recycled beverage containers globally, reinforcing their growing adoption across the beer industry.

Beer Cans Market Dynamics

Key Market Driver: Growing Global Consumption of Beer and Ready-to-Drink Alcoholic Beverages

The growing consumption of beer and ready-to-drink alcoholic beverages worldwide is significantly driving demand for beer cans. Consumers increasingly prefer canned beverages due to their convenience, portability, durability, and ability to preserve product freshness. The expansion of premium beer, craft beer, and flavored alcoholic beverage categories is creating sustained demand for high-quality and visually appealing can packaging. Rapid urbanization, changing lifestyles, and increasing participation in outdoor recreational activities are further supporting growth in canned beer sales across major markets.

Major brewing companies such as Anheuser-Busch InBev, Heineken N.V., and Carlsberg Group continue to expand canned beer offerings across international markets. According to industry trade organizations, canned beer accounts for a substantial share of beer packaging in North America and is gaining increasing acceptance across Asia-Pacific and Europe.

Key Restraint/Challenge: Volatility in Aluminum Raw Material Prices and Supply Chains

A major challenge in the Beer Cans market is the volatility of aluminum prices and disruptions across global raw material supply chains. Aluminum production is highly sensitive to fluctuations in energy costs, mining output, trade policies, and geopolitical developments, which can significantly impact packaging manufacturing expenses. Rising input costs place pressure on both can manufacturers and breweries, affecting profit margins and long-term procurement planning. In addition, transportation bottlenecks and supply shortages can create delays in can production and delivery schedules.

The aluminum market experienced significant price fluctuations during recent years due to global supply chain disruptions and energy market volatility, affecting beverage packaging manufacturers worldwide. Companies such as Ardagh Metal Packaging S.A. and CAN-PACK S.A. have increasingly focused on operational efficiency and strategic sourcing initiatives to mitigate the impact of raw material cost volatility.

Key Market Opportunity: Growth of Premium and Customized Digital-Printed Beer Cans

The growing demand for premium beer products and brand differentiation is creating significant opportunities for customized digital-printed beer cans. Breweries are increasingly adopting digitally printed cans to launch limited-edition products, seasonal offerings, and targeted marketing campaigns without the need for large production volumes. Digital printing technology enables enhanced design flexibility, shorter lead times, and improved consumer engagement through visually distinctive packaging. The trend is particularly strong among craft breweries seeking unique branding solutions to compete in crowded retail environments.

Companies such as Ardagh Metal Packaging S.A. have expanded digital printing capabilities through their Hart Print platform, enabling beverage brands to access highly customized aluminum can designs. Similarly, leading brewers and independent craft beer producers are increasingly utilizing premium decorative finishes and specialty can formats to enhance shelf appeal and strengthen brand recognition in the Beer Cans Market.

Beer Cans Market Scope

The beer cans market is segmented on the basis of type, product, capacity, and filling method.

- By Type

On the basis of type, the Beer Cans Market is segmented into 3 Piece Cans and 2 Piece Cans. The 2 Piece Cans segment dominated the market with the largest share of 68.4% in 2025, driven by their lightweight structure, superior durability, and cost-efficient manufacturing process. These cans require fewer raw materials and production stages, enabling beverage manufacturers to achieve higher operational efficiency and lower packaging costs. Their seamless design enhances product integrity and reduces the risk of leakage during transportation and storage. Growing adoption among major breweries for premium and mass-market beer products further supports segment growth. Increasing emphasis on sustainable packaging solutions also contributes to the continued dominance of 2 Piece Cans globally.

The 3 Piece Cans segment is projected to register the fastest growth at a CAGR of 5.8% from 2026 to 2033, driven by rising demand for flexible packaging formats and customized can designs. These cans offer greater versatility in terms of size, shape, and labeling options, making them suitable for specialty and craft beer producers. Expanding consumption of niche alcoholic beverages is encouraging manufacturers to adopt packaging formats that support product differentiation. Technological improvements in welding and coating processes are enhancing product performance and reducing production limitations. Growing penetration of regional breweries and private-label beverage brands is further accelerating demand across emerging markets.

- By Product

On the basis of product, the Beer Cans Market is segmented into Steel/Tin and Aluminum. The Aluminum segment dominated the market with a share of 74.2% in 2025, supported by its lightweight nature, excellent recyclability, and strong barrier properties against light and oxygen. Aluminum cans help preserve beer quality and freshness while reducing transportation costs across supply chains. High recycling rates and increasing environmental awareness among consumers have encouraged breweries to shift toward aluminum packaging solutions. The material also supports advanced printing and branding capabilities, improving shelf appeal and product visibility. Strong investments in circular economy initiatives further reinforce the segment’s market leadership.

The Steel/Tin segment is projected to register the fastest growth at a CAGR of 5.4% from 2026 to 2033, driven by increasing demand for durable and cost-effective packaging alternatives in selected regional markets. Steel cans provide enhanced strength and resistance to physical damage during handling and transportation. Advancements in corrosion-resistant coatings and lightweight steel manufacturing technologies are improving product performance and expanding application potential. Rising focus on material diversification among packaging manufacturers is creating new opportunities for steel-based beer cans. Growth in industrial-scale beverage production across developing economies is further supporting segment expansion.

- By Capacity

On the basis of capacity, the Beer Cans Market is segmented into 330 ml and 500 ml. The 330 ml segment dominated the market with the largest share of 61.7% in 2025, driven by its widespread acceptance across retail, hospitality, and convenience store channels. The format aligns with consumer preferences for portion-controlled consumption and supports affordability across various demographic groups. Breweries extensively utilize 330 ml cans for both mainstream and premium beer offerings due to their strong market acceptance. The compact size improves storage efficiency and transportation convenience for distributors and retailers. Growing demand for ready-to-drink alcoholic beverages continues to strengthen the segment’s leading position.

The 500 ml segment is projected to register the fastest growth at a CAGR of 6.2% from 2026 to 2033, driven by increasing consumer preference for larger serving sizes and value-oriented packaging formats. Rising popularity of social drinking occasions and outdoor recreational activities is supporting demand for higher-capacity beer packaging. Manufacturers are expanding their product portfolios in the 500 ml category to cater to evolving consumer purchasing patterns. Enhanced packaging designs and premium branding strategies are further increasing adoption across developed and emerging markets. Strong growth of modern retail channels and bulk beverage sales is expected to accelerate segment expansion during the forecast period.

- By Filling Method

On the basis of filling method, the Beer Cans Market is segmented into Vacuum Filling and Pressure Filling. The Pressure Filling segment dominated the market with a share of 72.8% in 2025, driven by its ability to efficiently handle carbonated beverages while preserving product quality and carbonation levels. The method minimizes oxygen exposure and ensures consistent filling accuracy, which is critical for maintaining beer flavor and shelf life. Large-scale breweries extensively utilize pressure filling systems due to their high production speed and operational reliability. Continuous advancements in automated filling equipment are improving manufacturing efficiency and reducing product losses. Growing global beer production volumes further support the segment’s dominant position.

The Vacuum Filling segment is projected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, driven by increasing adoption among specialty and craft beer manufacturers seeking enhanced filling precision. Vacuum filling technologies help reduce foam formation and improve product stability during packaging operations. Rising investments in advanced beverage processing equipment are expanding the accessibility of vacuum-based systems across medium-sized breweries. The method is gaining traction in premium beer applications where quality preservation is a key differentiating factor. Growing emphasis on minimizing waste and improving packaging efficiency is expected to accelerate segment growth over the forecast period.

Beer Cans Market Regional Analysis

North America dominated the beer cans market and accounted for the largest revenue share of 35% in 2025, driven by high beer consumption, strong demand for convenient beverage packaging, and widespread adoption of sustainable aluminum cans. The region benefits from a well-established brewing industry, advanced can manufacturing infrastructure, and high recycling rates that support circular packaging initiatives. Major breweries are increasingly utilizing lightweight and recyclable can formats to meet evolving consumer preferences and environmental goals. Growing popularity of craft beer and ready-to-drink alcoholic beverages is further supporting demand for beer cans across retail and hospitality channels. In addition, continuous investments in innovative packaging technologies continue to strengthen North America’s leadership position in the global market.

U.S. Beer Cans Market Insight

The U.S. Beer Cans market is experiencing strong growth driven by rising demand for premium beer products, expanding craft brewery operations, and increasing consumer preference for portable and recyclable packaging solutions. Breweries are actively adopting advanced can designs and sustainable materials to enhance product appeal and reduce environmental impact. The country’s large beer consumption base and extensive distribution network support consistent demand across multiple packaging formats. Strong investments in aluminum recycling infrastructure and lightweight packaging technologies are further improving market competitiveness. In addition, growing demand for canned alcoholic beverages across outdoor and social consumption occasions is accelerating market expansion in the U.S.

Canada Beer Cans Market Insight

The Canada Beer Cans market is witnessing steady growth supported by increasing demand for environmentally friendly beverage packaging and growing consumption of premium and craft beer products. Breweries are increasingly transitioning toward recyclable aluminum cans to align with sustainability objectives and changing consumer preferences. The country’s strong recycling ecosystem and supportive environmental regulations encourage adoption of circular packaging solutions. Rising popularity of locally produced craft beverages is further driving demand for customized and visually appealing can formats. In addition, expanding retail distribution channels and convenience-oriented purchasing behavior continue to contribute to market growth in Canada.

Europe Beer Cans Market Insight

The Europe Beer Cans market is expanding steadily due to strong sustainability initiatives, increasing beer consumption across key markets, and rising adoption of recyclable packaging materials. The region benefits from stringent environmental regulations that encourage manufacturers and breweries to reduce packaging waste and improve recycling efficiency. Demand for lightweight and cost-effective beverage containers is supporting widespread adoption of aluminum can packaging. Growing popularity of premium beer brands and innovative packaging formats is further stimulating market growth across European countries. Rising investments in advanced can production technologies continue to support regional market development.

U.K. Beer Cans Market Insight

The U.K. Beer Cans market is growing steadily, driven by strong consumption of canned beer products, increasing demand for sustainable packaging, and expanding craft beer production. Breweries are focusing on premium packaging solutions that enhance product visibility and convenience for consumers. The country’s well-developed retail sector and growing preference for take-home alcoholic beverages are supporting can sales growth. Rising environmental awareness among consumers is encouraging the use of highly recyclable aluminum packaging. In addition, increasing product launches from independent and regional breweries are strengthening market expansion in the U.K.

Germany Beer Cans Market Insight

The Germany Beer Cans market is expanding due to strong beer production volumes, increasing adoption of sustainable packaging solutions, and growing investments in advanced beverage packaging technologies. Breweries are increasingly utilizing lightweight cans to improve transportation efficiency and reduce packaging-related emissions. The country’s strong manufacturing capabilities and established recycling infrastructure support widespread adoption of aluminum can packaging. Rising demand for premium and specialty beer products is encouraging packaging innovation across the industry. In addition, growing focus on circular economy practices is further accelerating market development in Germany.

Asia-Pacific Beer Cans Market Insight

The Asia-Pacific Beer Cans market is expected to register the fastest growth with a CAGR of 5.62% from 2026 to 2033, driven by rising beer consumption, rapid urbanization, and expanding middle-class populations across major economies. Increasing disposable incomes and changing lifestyle preferences are encouraging greater demand for packaged alcoholic beverages. Countries such as China, India, Japan, South Korea, and Vietnam are witnessing strong investments in brewing capacity and beverage packaging infrastructure. Growing preference for convenient, portable, and recyclable packaging formats is significantly boosting adoption of beer cans. In addition, expanding modern retail networks and e-commerce beverage sales are further accelerating regional market growth.

Japan Beer Cans Market Insight

The Japan Beer Cans market is witnessing steady growth supported by strong consumer preference for canned beverages, advanced packaging technologies, and increasing demand for premium beer products. Breweries are focusing on innovative can designs and high-quality packaging solutions to enhance consumer experience and brand differentiation. The country’s sophisticated retail infrastructure and high convenience store penetration support extensive availability of canned beer products. Strong recycling practices and sustainability initiatives further encourage adoption of aluminum cans. In addition, rising demand for ready-to-drink alcoholic beverages continues to strengthen market growth in Japan.

China Beer Cans Market Insight

The China Beer Cans market is growing rapidly due to rising beer consumption, expanding urban populations, and increasing adoption of modern retail and convenience store channels. Breweries are actively investing in high-capacity canning facilities to meet growing consumer demand for packaged alcoholic beverages. The country’s large manufacturing base and strong aluminum production capabilities support cost-effective beer can production. Growing popularity of premium, imported, and craft beer products is creating additional opportunities for innovative packaging formats. In addition, increasing awareness of recyclable packaging and sustainability initiatives is further driving market growth in China.

Beer Cans Market Share

The beer cans industry is primarily led by well-established companies, including:

- Crown Holdings, Inc. (U.S.)

- Ball Corporation (U.S.)

- CAN-PACK S.A. (Poland)

- Shenzhen Xin Yuheng Can Co., Ltd. (China)

- Daiwa Can Company, Ltd. (Japan)

- Kaufman Container (U.S.)

- Orora Packaging Australia Pty Ltd (Australia)

- Nampak Ltd. (South Africa)

- East Asia Beer Packaging Limited (Hong Kong)

- Ardagh Metal Packaging S.A. (Luxembourg)

- Baosteel Packaging Co., Ltd. (China)

- CPMC Holdings Limited (China)

- Toyo Seikan Group Holdings, Ltd. (Japan)

- Showa Aluminum Can Corporation (Japan)

- Envases Universales Group (Mexico)

- Massilly Holding SAS (France)

Latest Developments in Beer Cans Market

- In April 2026, Crown Holdings commissioned a new beverage can manufacturing facility in Northern India with an annual production capacity of approximately 2.2 billion cans. This expansion strengthens the company’s presence in the rapidly growing Asia-Pacific beverage packaging sector and enhances regional supply capabilities for beer and other canned beverage manufacturers. The development is expected to support increasing demand for sustainable aluminum cans while improving production efficiency and market competitiveness

- In November 2025, Ball Corporation acquired an 80% stake in Benepack’s beverage can manufacturing operations in Belgium and Hungary. The acquisition significantly expands Ball’s production footprint across Europe, enabling the company to strengthen its supply network and better serve growing demand from breweries and beverage producers. The move also reinforces market consolidation and supports long-term capacity expansion in the European beer cans market

- In 2025, Ball Corporation announced an additional investment of USD 60 million to expand its beverage can manufacturing facility in Sri City, India. The expansion increases production capacity to address rising consumption of canned beverages and growing preference for recyclable aluminum packaging across the region. This investment is expected to enhance supply chain resilience and accelerate the adoption of beer cans in emerging markets

- In February 2024, Ardagh Metal Packaging expanded its digital printing capabilities by opening a third Hart Print facility in North America. The development enables beverage brands to access greater customization, shorter production runs, and premium packaging designs, supporting the increasing demand for differentiated beer packaging. It also strengthens innovation within the beer cans market by helping breweries improve brand visibility and consumer engagement

- In February 2024, Ardagh Metal Packaging partnered with Britvic for the launch of Tango Mango in its AMP H!GHEND specialty aluminum cans. The collaboration demonstrates the growing focus on premium can formats and advanced decoration technologies that enhance shelf appeal and product differentiation. This development supports broader adoption of high-value aluminum can packaging and encourages innovation across the Beer Cans Market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Beer Cans Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Beer Cans Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Beer Cans Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.