Global Bio Acetic Acid Market

Market Size in USD Million

USD

3.89 Million

USD

5.97 Million

2025

2033

USD

3.89 Million

USD

5.97 Million

2025

2033

| 2026 - 2033 | |

| USD 3.89 Million | |

| USD 5.97 Million | |

| % | |

|

Bio-Acetic Acid Market Size

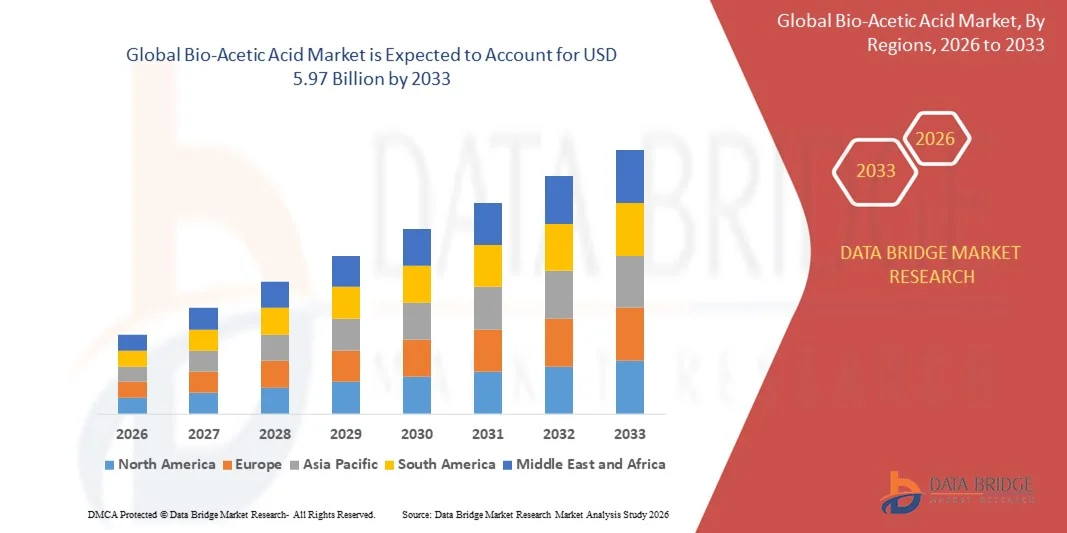

- The global bio-acetic acid market size was valued at USD 3.89 billion in 2025 and is expected to reach USD 5.97 billion by 2033, at a CAGR of 5.5% during the forecast period

- The market growth is largely fueled by increasing adoption of sustainable and bio-based chemicals across industrial, food, and pharmaceutical sectors, driven by rising environmental regulations and consumer preference for eco-friendly products

- Furthermore, growing investments in bio-refineries, advancements in fermentation and bioprocessing technologies, and expansion of feedstock availability such as biomass, corn, and sugar are enabling scalable production of bio-acetic acid. These converging factors are accelerating its adoption across applications such as acetate esters, acetic anhydride, purified terephthalic acid, and vinyl acetate monomer, thereby significantly boosting market growth

Bio-Acetic Acid Market Analysis

- Bio-acetic acid, produced from renewable feedstocks through fermentation or other bio-based processes, is increasingly vital for chemical, food & beverage, pharmaceutical, and personal care industries due to its sustainable sourcing, high purity, and versatility in multiple applications

- The escalating demand for bio-acetic acid is primarily fueled by regulatory emphasis on carbon footprint reduction, growing consumer preference for natural and clean-label ingredients, and the shift from petroleum-derived to renewable chemicals in industrial production, reinforcing its critical role in sustainable manufacturing and green chemical adoption

- Asia-Pacific dominated the bio-acetic acid market with a share of 47.1% in 2025, due to increasing industrialization, expanding chemical and food processing sectors, and growing investments in bio-based chemical production

- North America is expected to be the fastest growing region in the bio-acetic acid market during the forecast period due to strong demand for bio-based chemicals in pharmaceuticals, food & beverage, and industrial applications

- Vinyl acetate monomer segment dominated the market with a market share of 42.9% in 2025, due to growing demand in the polymer and packaging industry. For instance, Celanese Corporation’s expansion of VAM production capacity reflects the increasing consumption of VAM in adhesives, paints, and coatings. Vinyl acetate monomer requires bio-acetic acid as a key feedstock, making the segment highly dependent on the availability of sustainable acetic acid. Rising applications in eco-friendly and high-performance packaging materials further propel the growth of bio-based VAM production, making it a high-potential segment

Report Scope and Bio-Acetic Acid Market Segmentation

|

Attributes |

Bio-Acetic Acid Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Bio-Acetic Acid Market Trends

Rising Adoption of Bio-Based and Sustainable Chemicals

- The growing emphasis on sustainability and environmental responsibility is a major factor driving the adoption of bio-acetic acid across chemical, food & beverage, pharmaceutical, and personal care industries. Companies are increasingly moving away from petroleum-based acetic acid to reduce carbon footprint and comply with stringent environmental regulations

- For instance, Afyren SAS has expanded its NEOXY facility to produce high-purity bio-acetic acid from agricultural byproducts, providing a renewable and environmentally friendly solution for industrial and specialty chemical applications. This expansion supports increased production capacity and meets rising demand across European and global markets

- Technological advancements in fermentation, bioprocessing, and purification methods are significantly improving the yield, quality, and scalability of bio-acetic acid. These improvements enable manufacturers to supply consistent, high-purity products suitable for sensitive applications such as pharmaceuticals and food additives

- The increasing integration of bio-acetic acid in specialty applications such as acetate esters, acetic anhydride, purified terephthalic acid, and vinyl acetate monomer is enhancing its utilization across multiple end-user sectors. This integration strengthens the role of bio-acetic acid as a versatile and sustainable chemical intermediate

- Growing consumer preference for clean-label and eco-friendly products in food, cosmetics, and pharmaceuticals is further driving the adoption of bio-acetic acid. Manufacturers are responding to this demand by investing in bio-based production facilities and promoting sustainable product lines

- Overall, the convergence of technological innovation, sustainability mandates, and rising industrial and consumer demand is accelerating the adoption of bio-acetic acid, encouraging companies to scale production, diversify applications, and strengthen their market position

Bio-Acetic Acid Market Dynamics

Driver

Increasing Industrial and Pharmaceutical Demand for Eco-Friendly Acetic Acid

- Rising industrial usage, particularly in chemical manufacturing, pharmaceuticals, and personal care, is driving the demand for bio-acetic acid as companies prioritize sustainable and renewable alternatives. The increasing regulatory focus on reducing carbon emissions and environmental impact further fuels market expansion

- For instance, GODAVARI BIOREFINERIES LTD expanded its bio-acetic acid production capacity to cater to pharmaceutical intermediates and food-grade applications. Such strategic capacity expansion helps meet rising domestic and export demand while reinforcing the company’s presence in emerging and mature markets

- The shift from petroleum-based chemicals to bio-based feedstocks such as biomass, corn, maize, and sugar is creating new opportunities for manufacturers to supply eco-friendly acetic acid to multiple industrial applications. In addition, these renewable feedstocks help companies achieve sustainability targets and improve environmental compliance

- Increasing investments in bio-refineries and technological infrastructure are enabling manufacturers to meet growing demand efficiently. Companies are focusing on process optimization, production scalability, and supply chain resilience to ensure consistent delivery of high-quality bio-acetic acid

- Rising awareness among consumers and industrial buyers regarding environmental sustainability, coupled with government incentives supporting renewable chemical production, is further driving market adoption. These factors collectively ensure a steady growth trajectory for bio-acetic acid in industrial, food, and pharmaceutical applications

Restraint/Challenge

High Production Costs and Feedstock Dependence

- The high production costs of bio-acetic acid, including fermentation processes, purification, and capital-intensive equipment, present a significant barrier to market growth. These costs make bio-acetic acid less competitive compared to petroleum-derived acetic acid in price-sensitive markets

- For instance, smaller-scale manufacturers often face challenges competing due to higher operational expenses and limited access to cost-efficient technology. Such limitations can restrict market penetration, particularly in regions where raw material supply is inconsistent

- Dependence on raw materials such as biomass, corn, maize, and sugar exposes producers to fluctuations in availability and price volatility. In addition, seasonal variations, agricultural yield changes, and logistics issues can disrupt production schedules and affect profitability

- Technical complexity in scaling up bio-acetic acid production to maintain high purity and yield requires advanced infrastructure and skilled personnel. Companies must invest in R&D, process optimization, and quality control measures to overcome these operational challenges

- While ongoing technological improvements are gradually reducing production costs, achieving cost parity with conventional acetic acid remains a significant hurdle. Overcoming these challenges through strategic partnerships, process innovation, and investment in renewable feedstock sourcing is crucial for sustained market growth

Bio-Acetic Acid Market Scope

The market is segmented on the basis of raw material, applications, and end user.

- By Raw Material

On the basis of raw material, the Bio-Acetic Acid market is segmented into biomass, corn, maize, and sugar. The biomass segment dominated the market with the largest revenue share in 2025, driven by its sustainable and eco-friendly production process that aligns with increasing environmental regulations and consumer preference for green chemicals. Biomass-based acetic acid offers a higher yield and is often favored for large-scale industrial production due to its consistent quality and availability. The market also sees strong adoption of biomass-derived acetic acid in applications where renewable sourcing and carbon footprint reduction are critical, enhancing its market appeal among manufacturers.

The corn segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its wide availability and relatively lower production cost compared to other raw materials. For instance, companies such as Cargill are investing in corn-based acetic acid production to cater to growing demand in the food and beverage sector. Corn-derived acetic acid also provides scalability advantages and compatibility with fermentation-based technologies, making it an attractive choice for emerging markets. The increasing integration of corn as a feedstock in bio-refineries further supports its rapid adoption and market expansion.

- By Applications

On the basis of applications, the Bio-Acetic Acid market is segmented into acetate esters, acetic anhydride, purified terephthalic acid (PTA), and vinyl acetate monomer (VAM). The VAM segment dominated the market with the largest share of 42.9% in 2025 due to growing demand in the polymer and packaging industry. For instance, Celanese Corporation’s expansion of VAM production capacity reflects the increasing consumption of VAM in adhesives, paints, and coatings. Vinyl acetate monomer requires bio-acetic acid as a key feedstock, making the segment highly dependent on the availability of sustainable acetic acid. Rising applications in eco-friendly and high-performance packaging materials further propel the growth of bio-based VAM production, making it a high-potential segment.

The acetate esters segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its extensive usage in solvents, coatings, adhesives, and flavoring agents across multiple industries. Acetate esters offer versatile chemical properties that enhance their adoption in both industrial and consumer-facing applications, driving consistent demand. The segment also benefits from rising demand in pharmaceuticals and personal care products where high-purity acetic acid derivatives are required for formulation stability and performance.

- By End User

On the basis of end user, the Bio-Acetic Acid market is segmented into chemical, food & beverage, personal care, and pharmaceutical industries. The chemical industry dominated the market in 2025 with the largest revenue share due to its extensive use of acetic acid in producing various derivatives such as acetate esters, anhydrides, and solvents. The chemical sector relies heavily on high-purity and consistent-quality bio-acetic acid for industrial reactions, which drives sustained demand and large-scale adoption. In addition, stringent environmental regulations have encouraged chemical manufacturers to shift from petroleum-derived to bio-based acetic acid, further reinforcing its market dominance.

The food & beverage segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising consumer preference for natural and clean-label ingredients. For instance, Tate & Lyle has been actively promoting bio-acetic acid in vinegar and flavoring applications to meet increasing health-conscious consumer demand. Bio-acetic acid offers safe and sustainable alternatives to synthetic additives in food production, which drives its rapid adoption. Growing consumption in emerging regions and expanding functional food trends contribute significantly to the segment’s accelerated market growth.

Bio-Acetic Acid Market Regional Analysis

- Asia-Pacific dominated the bio-acetic acid market with the largest revenue share of 47.1% in 2025, driven by increasing industrialization, expanding chemical and food processing sectors, and growing investments in bio-based chemical production

- The region’s cost-effective production landscape, rising adoption of sustainable feedstocks, and expanding exports of bio-acetic acid are accelerating market expansion

- The availability of skilled labor, favorable government policies, and rapid growth of emerging economies are contributing to increased consumption of bio-acetic acid across chemical, food & beverage, and pharmaceutical sectors

China Bio-Acetic Acid Market Insight

China held the largest share in the Asia-Pacific Bio-Acetic Acid market in 2025, owing to its position as a global leader in chemical manufacturing and extensive bio-refinery infrastructure. The country’s strong industrial base, favorable government policies supporting renewable chemical production, and large-scale export capabilities for bio-based chemicals are major growth drivers, while ongoing investments in high-purity acetic acid for industrial, pharmaceutical, and food applications further strengthen demand.

India Bio-Acetic Acid Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by a rapidly expanding chemical and pharmaceutical sector, increasing production of bio-based chemicals, and rising investments in sustainable manufacturing. Government initiatives promoting renewable chemicals, growing domestic demand, export potential, expanding R&D capabilities, and adoption of eco-friendly production methods are collectively contributing to robust market expansion.

Europe Bio-Acetic Acid Market Insight

The Europe Bio-Acetic Acid market is expanding steadily, supported by stringent environmental regulations, growing demand for bio-based chemicals, and increasing investments in sustainable and specialty chemical production. The region places strong emphasis on product quality, environmental compliance, and adoption of renewable feedstocks, particularly in chemical and pharmaceutical applications, while rising use of bio-acetic acid in acetate esters, purified terephthalic acid, and specialty chemicals further drives growth.

Germany Bio-Acetic Acid Market Insight

Germany’s market is driven by its leadership in high-precision chemical manufacturing, strong industrial infrastructure, and export-oriented production. Well-established R&D networks, collaborations between academic institutions and chemical manufacturers, and strong demand for pharmaceuticals, industrial solvents, and specialty chemical applications are fostering continuous innovation and market growth.

U.K. Bio-Acetic Acid Market Insight

The U.K. market is supported by a mature chemical and pharmaceutical sector, growing focus on sustainability, and increasing adoption of bio-based feedstocks. Rising investment in R&D, partnerships, and production of high-purity bio-acetic acid are enabling the U.K. to maintain a significant role in specialty chemical markets.

North America Bio-Acetic Acid Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by strong demand for bio-based chemicals in pharmaceuticals, food & beverage, and industrial applications. A focus on sustainability, advancements in production technologies, reshoring of chemical manufacturing, and increasing collaboration between chemical manufacturers and end-user industries are supporting market expansion.

U.S. Bio-Acetic Acid Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its expansive chemical and pharmaceutical industry, robust R&D infrastructure, and significant investment in bio-based chemical production. The country’s emphasis on innovation, sustainability, high-purity product standards, and a mature distribution network is encouraging adoption across industrial and consumer applications, solidifying its leading position in the region.

Bio-Acetic Acid Market Share

The bio-acetic acid industry is primarily led by well-established companies, including:

- Airedale Chemicals (U.K.)

- Bio‑Corn Products EPZ Ltd. (India)

- GODAVARI BIOREFINERIES LTD (India)

- Sucroal SA (Spain)

- Novozymes A/S (Denmark)

- Cargill, Inc. (U.S.)

- LanzaTech (U.S.)

- Afyren SAS (France)

- BTG Bioliquids (Netherlands)

- Celanese Corporation (U.S.)

- Wacker Chemie AG (Germany)

- Eastman Chemical Company (U.S.)

- SEKAB Biofuels & Chemicals AB (Sweden)

- Zea2 LLC (U.S.)

- Lenzing AG (Austria)

- INEOS Group (U.K.)

- ADM (Archer Daniels Midland) (U.S.)

Latest Developments in Global Bio-Acetic Acid Market

- In July 2025, Godavari Biorefineries reported a notable increase in ethanol production and reaffirmed its commitment to bio-based chemical manufacturing, including acetic acid. The improved feedstock availability directly supports higher bio-acetic acid output, enabling the company to meet rising demand in chemical, pharmaceutical, and food sectors. This development also signals growing confidence in bio-based processes in emerging markets, further encouraging investments in sustainable chemical production

- In June 2025, AFYREN announced that its NEOXY plant achieved continuous industrial production of bio-based acids, including bio-acetic acid, marking a significant scale-up in commercial operations. This achievement enables faster delivery to industrial, food, and personal care sectors and also strengthens AFYREN’s position as a leader in sustainable chemistry. The ability to secure multi-year supply contracts enhances customer confidence and positions the company to capture a larger share of the growing bio-acetic acid market

- In January 2025, AFYREN secured a €10 million sustainability-linked loan for its NEOXY subsidiary, where the credit terms are tied to environmental and CSR performance. This strategic financial support facilitates production scale-up and underscores investor confidence in bio-based chemical technologies. It also highlights the increasing importance of sustainability metrics in market acceptance, signaling to industrial and commercial buyers that bio-acetic acid is a reliable, eco-friendly alternative to petrochemical-derived products

- In January 2025, LanzaTech announced the formation of a spin-off, LanzaX, through a joint venture aimed at accelerating the development of specialty bio-chemicals, including acetic acid derivatives. By separating its fermentation-based operations from innovation-focused ventures, LanzaTech can focus on commercial-scale bio-acetic acid production, while LanzaX drives technological advancements. This strategic move is expected to expand production capacity, foster innovation in high-purity bio-acids, and enhance adoption across pharmaceutical, food, and industrial applications

- In September 2024, AFYREN successfully produced its first commercial batches of bio-based acids at the NEOXY plant. This milestone allows consistent supply to customers in food, cosmetics, and life sciences, reinforcing the market credibility of bio-acetic acid as a sustainable alternative. Early commercial production also enables customer trials, adoption in specialty applications, and positioning of bio-acetic acid as a scalable, environmentally friendly solution, setting the stage for accelerated market growth

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Bio Acetic Acid Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Bio Acetic Acid Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Bio Acetic Acid Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.