Global Bio Based Packaging Materials Market

Market Size in USD Billion

USD

92.30 Billion

USD

199.29 Billion

2025

2033

USD

92.30 Billion

USD

199.29 Billion

2025

2033

| 2026 - 2033 | |

| USD 92.30 Billion | |

| USD 199.29 Billion | |

| % | |

|

Bio-Based Packaging Materials Market Overview

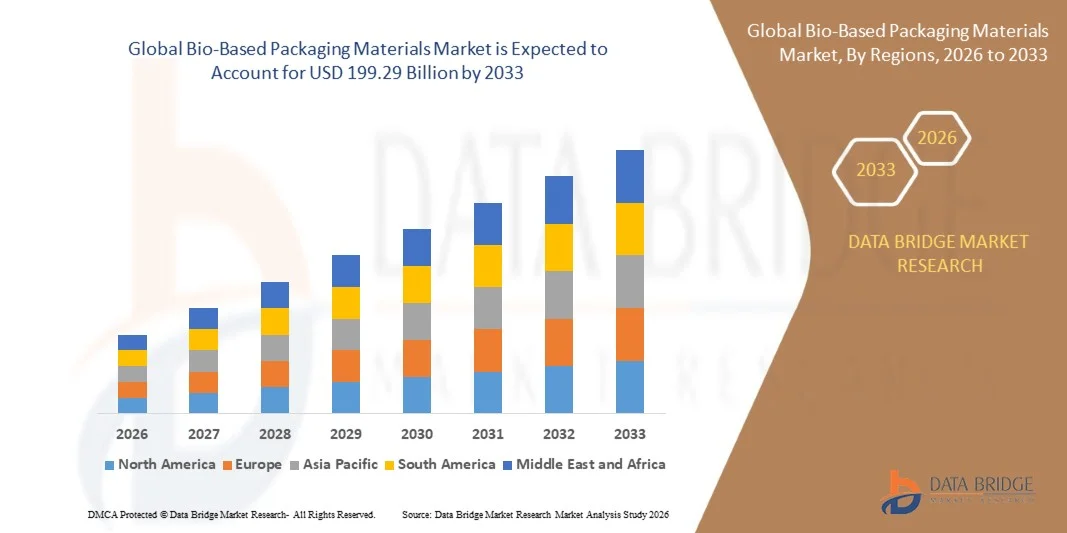

The global bio-based packaging materials market was valued at USD 92.30 billion in 2025 and is projected to reach USD 199.29 billion by 2033, growing at a CAGR of 10.10% from 2026 to 2033. The market is witnessing strong growth driven by increasing demand for sustainable and eco-friendly solutions, rapid industrial adoption of next-generation materials, and expanding regulatory focus on environmental compliance across packaging and manufacturing industries.

The growing shift toward bio-based and biodegradable alternatives to conventional materials is reshaping product development strategies across end-use sectors. Rising concerns regarding plastic waste pollution, coupled with stringent government regulations on single-use plastics, are encouraging manufacturers and brands to adopt renewable packaging solutions. In addition, advancements in biopolymer technologies and improved scalability of production processes are further supporting market expansion across food and beverage, personal care, healthcare, and retail applications.

Key Market Trends & Insights

- North America dominated the bio-based packaging materials market with the largest revenue share of 38.7% in 2025, supported by strong demand for sustainable packaging solutions, stringent environmental regulations, and rapid adoption of circular economy practices across FMCG and food service industries.

- Asia-Pacific bio-based packaging materials market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, rising disposable incomes, and increasing environmental awareness in countries such as China, India, and Japan.

- The Polylactic Acid (PLA) segment held the largest market revenue share of approximately 32.6% in 2025 driven by its wide adoption in food packaging, disposable containers, and flexible packaging films due to its compostability, transparency, and ease of processing. PLA is extensively used by FMCG companies and food service providers for sustainable packaging alternatives.

- The Polyhydroxyalkanoates (PHA) segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by increasing demand for fully biodegradable packaging materials with marine biodegradability and high environmental compatibility. Rising investments in microbial fermentation technologies and scaling production by companies such as Danimer Scientific are accelerating commercial adoption across food packaging and agricultural film applications.

- The Flexible Packaging segment held the largest market revenue share of approximately 58.3% in 2025 driven by rising demand for lightweight, cost-effective, and sustainable packaging formats used in snacks, beverages, and personal care products. Flexible bio-based films and wraps are increasingly replacing conventional plastic laminates due to improved recyclability and reduced material consumption.

- The Rigid Packaging segment is projected to register the fastest growth at a CAGR of 9.7% from 2026 to 2033, driven by increasing adoption of molded fiber trays, bio-based bottles, and compostable containers in food delivery, pharmaceuticals, and retail packaging applications. Expansion of sustainable supply chain initiatives by global brands is further supporting segment growth.

- The Food & Beverages segment held the largest market revenue share of approximately 41.9% in 2025 driven by high consumption of packaged food products and rising demand for sustainable takeaway and ready-to-eat packaging solutions. Major food chains and beverage manufacturers are increasingly shifting toward compostable packaging formats to meet sustainability goals.

- The E-Commerce Packaging segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by rapid expansion of online retail platforms and increasing demand for eco-friendly protective packaging materials such as molded fiber, bio-based cushioning, and compostable mailers. Growth of cross-border e-commerce is further accelerating adoption of sustainable packaging solutions.

- The Food Industry segment held the largest market revenue share of approximately 38.4% in 2025 driven by large-scale usage of biodegradable trays, wraps, and containers in processed and packaged food distribution networks.

- The Retail & E-Commerce segment is projected to register the fastest growth at a CAGR of 10.9% from 2026 to 2033, driven by increasing sustainability commitments from online retailers and growing consumer preference for plastic-free packaging solutions in delivery and logistics operations.

- The Direct Sales segment held the largest market revenue share of approximately 55.2% in 2025 driven by strong procurement relationships between bio-based material manufacturers and large FMCG, food processing, and packaging companies requiring bulk supply contracts.

- The Online Channels segment is projected to register the fastest growth at a CAGR of 13.1% from 2026 to 2033, driven by increasing digitalization of B2B procurement platforms and rising accessibility of specialty bio-based packaging materials for small and medium-sized enterprises seeking sustainable packaging alternatives.

Market Size & Forecast

- Global Market Value (2025): USD 92.30 Billion

- Expected Market Value (2033): USD 199.29 Billion

- Forecast CAGR (2026–2033): 10.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Bio-Based Packaging Materials Market Segmentation

|

Attributes |

Bio-Based Packaging Materials Key Market Insights |

|

Segments Covered |

• By Material Type: Polylactic Acid (PLA), Starch-Based Materials, Polyhydroxyalkanoates (PHA), Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Cellulose-Based Materials, and Other Bio-Based Materials • By Packaging Type: Flexible Packaging and Rigid Packaging • By Application: Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Consumer Goods, Industrial Packaging, E-Commerce Packaging, and Other Applications • By End User: Food Industry, Beverage Industry, Healthcare Industry, Personal Care Industry, Retail & E-Commerce, and Industrial Sector • By Distribution Channel: Direct Sales, Distributors & Wholesalers, and Online Channels |

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• NatureWorks LLC (U.S.) |

|

Market Opportunities |

Expansion Of Sustainable Packaging Demand Growth In Circular Economy Initiatives |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Bio-Based Packaging Materials Market Trends

Trend: Growth In Sustainable Materials And Bio-Based Packaging Adoption

Increasing demand for environmentally sustainable, renewable, and low-carbon packaging solutions across food and beverage, personal care, healthcare, and e-commerce sectors. Conventional plastic-based packaging materials are increasingly being restricted due to environmental regulations, microplastic pollution concerns, and rising corporate sustainability commitments, encouraging industries to shift toward bio-based alternatives such as PLA, PHA, starch blends, and cellulose-based materials.

In modern food and beverage packaging systems, manufacturers are increasingly adopting compostable bio-based films, For instance PLA-based packaging used by major global brands such as Nestlé and Danone for single-use containers and wrappers, to reduce plastic footprint and meet ESG targets while maintaining product shelf life and barrier performance. In retail and e-commerce packaging, companies are deploying molded fiber and starch-based cushioning materials to replace expanded polystyrene, improving recyclability and reducing environmental waste across supply chains.

The rapid expansion of sustainable packaging mandates across Europe and Asia-Pacific is also increasing demand for bio-based materials capable of meeting EU Single-Use Plastics Directive requirements and extended producer responsibility frameworks. In addition, increasing investment in biopolymer production facilities, such as NatureWorks’ Ingeo PLA plant expansions in Thailand, is strengthening global supply chain capacity and reducing production costs. Growing industrial validation through large-scale commercial adoption in 2025 across FMCG and food delivery sectors is demonstrating significant reductions in lifecycle carbon emissions, with bio-based packaging showing up to 30–60% lower greenhouse gas emissions compared to conventional petroleum-based plastics under standardized lifecycle assessments.

Global Bio-Based Packaging Materials Market Dynamics

Key Market Driver: Rising Regulatory Push And Consumer Demand For Sustainable Packaging

Governments worldwide are implementing stringent regulations to reduce single-use plastic consumption and promote circular economy practices, significantly driving demand for bio-based packaging materials. Policies such as the European Green Deal, U.S. state-level plastic bans, and India’s restrictions on single-use plastics are accelerating the shift toward compostable and renewable packaging alternatives.

Major FMCG and food companies are increasingly integrating bio-based packaging solutions into product lines to comply with sustainability targets and reduce environmental impact. For instance, Unilever and PepsiCo have introduced bio-based and recyclable packaging initiatives across multiple product categories, aiming to achieve 100% recyclable or reusable packaging in key markets by 2030.

In addition, rising consumer awareness regarding plastic pollution and preference for eco-friendly products is further strengthening market demand, particularly in urban retail and online grocery segments. Industry reports indicate that over 60–70% of consumers in Europe and North America prefer sustainable packaging options when available, directly influencing brand packaging strategies and procurement decisions

Key Restraint/Challenge: High Production Costs And Limited Scalability Of Bio-Based Materials

Bio-based packaging materials currently face cost competitiveness challenges compared to conventional plastic packaging due to expensive raw materials, limited large-scale production infrastructure, and complex biopolymer processing technologies. Feedstock dependency on agricultural sources such as corn starch and sugarcane also introduces price volatility and supply chain constraints.

In addition, limited industrial-scale composting and recycling infrastructure restricts end-of-life management of bio-based packaging in several regions, reducing overall system efficiency. Performance limitations such as lower moisture resistance and reduced thermal stability in certain bio-based polymers further restrict their use in high-barrier or long-shelf-life applications.

Commercial benchmarking studies indicate that PLA-based packaging materials can be 20–50% more expensive than conventional PET plastics depending on production scale and region, creating affordability challenges for small and medium-sized manufacturers despite increasing demand from large multinational brands.

Key Market Opportunity: Expansion Of Advanced Biopolymers And Circular Economy Infrastructure

Advancements in next-generation biopolymers and hybrid material technologies are creating significant opportunities for performance-enhanced bio-based packaging solutions across global markets. Innovations in PHA production through microbial fermentation and improved cellulose nanofiber processing are enhancing material strength, flexibility, and barrier properties, making them suitable for broader industrial applications.

Packaging manufacturers are increasingly investing in closed-loop recycling systems and compostable packaging ecosystems to support circular economy models. For instance, large-scale pilot projects in Europe are integrating industrial composting facilities with retail packaging return systems, improving waste recovery efficiency and reducing landfill dependency.

In addition, rapid expansion of bio-refinery capacity in Asia-Pacific, particularly in China and India, is improving raw material availability and reducing production costs. Growing adoption in pharmaceutical blister packaging, premium cosmetics, and organic food sectors is further accelerating commercialization. Industry pilots conducted in 2025 across EU retail chains demonstrated up to 40% reduction in packaging waste accumulation when switching to fully compostable bio-based packaging formats across selected product categories.

Global Bio-Based Packaging Materials Market Scope

The market is segmented on the basis of material type, packaging type, application, end user, and distribution channel.

• By Material Type

On the basis of material type, the bio-based packaging materials market is segmented into Polylactic Acid (PLA), Starch-Based Materials, Polyhydroxyalkanoates (PHA), Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Cellulose-Based Materials, and Other Bio-Based Materials. The Polylactic Acid (PLA) segment held the largest market revenue share of approximately 32.6% in 2025 driven by its wide adoption in food packaging, disposable containers, and flexible packaging films due to its compostability, transparency, and ease of processing. PLA is extensively used by FMCG companies and food service providers for sustainable packaging alternatives.

The Polyhydroxyalkanoates (PHA) segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by increasing demand for fully biodegradable packaging materials with marine biodegradability and high environmental compatibility. Rising investments in microbial fermentation technologies and scaling production by companies such as Danimer Scientific are accelerating commercial adoption across food packaging and agricultural film applications.

• By Packaging Type

On the basis of packaging type, the market is segmented into Flexible Packaging and Rigid Packaging. The Flexible Packaging segment held the largest market revenue share of approximately 58.3% in 2025 driven by rising demand for lightweight, cost-effective, and sustainable packaging formats used in snacks, beverages, and personal care products. Flexible bio-based films and wraps are increasingly replacing conventional plastic laminates due to improved recyclability and reduced material consumption.

The Rigid Packaging segment is projected to register the fastest growth at a CAGR of 9.7% from 2026 to 2033, driven by increasing adoption of molded fiber trays, bio-based bottles, and compostable containers in food delivery, pharmaceuticals, and retail packaging applications. Expansion of sustainable supply chain initiatives by global brands is further supporting segment growth.

• By Application

On the basis of application, the market is segmented into Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Consumer Goods, Industrial Packaging, E-Commerce Packaging, and Other Applications. The Food & Beverages segment held the largest market revenue share of approximately 41.9% in 2025 driven by high consumption of packaged food products and rising demand for sustainable takeaway and ready-to-eat packaging solutions. Major food chains and beverage manufacturers are increasingly shifting toward compostable packaging formats to meet sustainability goals.

The E-Commerce Packaging segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by rapid expansion of online retail platforms and increasing demand for eco-friendly protective packaging materials such as molded fiber, bio-based cushioning, and compostable mailers. Growth of cross-border e-commerce is further accelerating adoption of sustainable packaging solutions.

• By End User

On the basis of end user, the market is segmented into Food Industry, Beverage Industry, Healthcare Industry, Personal Care Industry, Retail & E-Commerce, and Industrial Sector. The Food Industry segment held the largest market revenue share of approximately 38.4% in 2025 driven by large-scale usage of biodegradable trays, wraps, and containers in processed and packaged food distribution networks.

The Retail & E-Commerce segment is projected to register the fastest growth at a CAGR of 10.9% from 2026 to 2033, driven by increasing sustainability commitments from online retailers and growing consumer preference for plastic-free packaging solutions in delivery and logistics operations.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Sales, Distributors & Wholesalers, and Online Channels. The Direct Sales segment held the largest market revenue share of approximately 55.2% in 2025 driven by strong procurement relationships between bio-based material manufacturers and large FMCG, food processing, and packaging companies requiring bulk supply contracts.

The Online Channels segment is projected to register the fastest growth at a CAGR of 13.1% from 2026 to 2033, driven by increasing digitalization of B2B procurement platforms and rising accessibility of specialty bio-based packaging materials for small and medium-sized enterprises seeking sustainable packaging alternatives.

Global Bio-Based Packaging Materials Market Regional Analysis

North America Bio-Based Packaging Materials Market Insight

North America dominated the bio-based packaging materials market with the largest revenue share of 38.7% in 2025, supported by strong demand for sustainable packaging solutions, stringent environmental regulations, and rapid adoption of circular economy practices across FMCG and food service industries. Consumers in the region increasingly prefer eco-friendly packaging formats such as compostable films, molded fiber, and bio-based plastics due to rising awareness of plastic waste reduction and corporate sustainability initiatives. This widespread adoption is further supported by high disposable incomes, advanced recycling infrastructure, and strong presence of leading packaging manufacturers, establishing bio-based packaging as a key alternative to conventional plastics in both retail and industrial applications.

U.S. Bio-Based Packaging Materials Market Insight

The U.S. bio-based packaging materials market captured the largest revenue share in 2025 within North America, driven by rapid adoption of sustainable packaging by major food chains, e-commerce platforms, and consumer goods companies. Increasing regulatory pressure from state-level plastic bans, such as restrictions in California and New York, is accelerating the shift toward compostable and recyclable packaging solutions. Major corporations including Amazon and Walmart are actively integrating bio-based mailers, corrugated fiber packaging, and starch-based cushioning materials across supply chains to reduce environmental impact and meet ESG targets. In addition, strong innovation in biopolymer production and investment in domestic manufacturing capacity are further strengthening market growth.

Europe Bio-Based Packaging Materials Market Insight

The Europe bio-based packaging materials market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent environmental regulations such as the EU Single-Use Plastics Directive and strong enforcement of extended producer responsibility frameworks. The region is experiencing rapid transition toward compostable and biodegradable packaging across food, beverage, and retail sectors. European consumers are highly inclined toward sustainable products, increasing demand for bio-based alternatives in supermarkets and online retail channels. Growth is also supported by strong government funding for circular economy initiatives and increasing adoption of industrial composting systems across major economies such as Germany, France, and Italy.

U.K. Bio-Based Packaging Materials Market Insight

The U.K. bio-based packaging materials market is expected to witness strong growth from 2026 to 2033, driven by rising consumer awareness regarding plastic pollution and increasing corporate commitments toward net-zero packaging targets. Retailers and food delivery companies are increasingly shifting toward compostable packaging formats such as bagasse containers and starch-based films. The country’s strong e-commerce ecosystem and growing demand for sustainable takeaway packaging are further accelerating adoption. In addition, government initiatives aimed at reducing single-use plastics and improving recycling rates are supporting the expansion of bio-based packaging solutions across commercial and residential applications.

Germany Bio-Based Packaging Materials Market Insight

The Germany bio-based packaging materials market is expected to witness robust growth from 2026 to 2033, fueled by strong environmental regulations, advanced recycling infrastructure, and high consumer preference for eco-friendly packaging solutions. Germany’s emphasis on sustainability and engineering innovation is driving adoption of high-performance bio-based materials in food, pharmaceuticals, and industrial packaging. Companies are increasingly investing in cellulose-based and PLA-based packaging formats to align with strict environmental standards. In addition, strong R&D activity in biopolymer development and collaboration between packaging manufacturers and chemical companies is enhancing material performance and scalability.

Asia-Pacific Bio-Based Packaging Materials Market Insight

The Asia-Pacific bio-based packaging materials market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, rising disposable incomes, and increasing environmental awareness in countries such as China, India, and Japan. The region is also emerging as a major manufacturing hub for biopolymers, improving cost efficiency and supply chain availability of bio-based packaging materials. Government initiatives promoting plastic waste reduction and sustainable development are further accelerating adoption across food delivery, retail, and e-commerce sectors. Expanding middle-class consumption and strong growth in online retail platforms are significantly boosting demand for eco-friendly packaging solutions.

Japan Bio-Based Packaging Materials Market Insight

The Japan bio-based packaging materials market is expected to witness steady growth from 2026 to 2033 due to strong emphasis on environmental sustainability, technological advancement, and high demand for premium packaging solutions. Japan’s aging population and urban lifestyle trends are increasing demand for convenient, lightweight, and easy-to-dispose packaging formats. Companies are integrating bio-based materials into food packaging, electronics packaging, and healthcare applications to improve sustainability performance. In addition, strong innovation in material science and government support for waste reduction initiatives are supporting gradual but consistent market expansion.

China Bio-Based Packaging Materials Market Insight

The China bio-based packaging materials market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid industrialization, expanding e-commerce sector, and strong government push toward plastic pollution control. China is one of the largest consumers and producers of packaging materials, with increasing adoption of bio-based alternatives across food delivery platforms, retail packaging, and logistics operations. Leading domestic manufacturers are investing heavily in PLA and starch-based production facilities to meet rising demand. In addition, national policies promoting green manufacturing and carbon neutrality targets are significantly accelerating market penetration of bio-based packaging solutions.

Global Bio-Based Packaging Materials Market Share

The Bio-Based Packaging Materials industry is primarily led by well-established companies, including:

• NatureWorks LLC (U.S.)

• TotalEnergies Corbion (Netherlands)

• Novamont S.p.A. (Italy)

• BASF SE (Germany)

• Danimer Scientific (U.S.)

• Mitsubishi Chemical Group (Japan)

• Toray Industries Inc. (Japan)

• Braskem (Brazil)

• Amcor plc (Switzerland)

• Sealed Air Corporation (U.S.)

• Stora Enso (Finland)

• Tetra Pak (Sweden)

• Mondi Group (U.K.)

• Huhtamaki Oyj (Finland)

• Smurfit Kappa (Ireland)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Bio Based Packaging Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Bio Based Packaging Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Bio Based Packaging Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.