Global Bio Surgical Agents Market

Market Size in USD Billion

USD

16.35 Billion

USD

29.39 Billion

2025

2033

USD

16.35 Billion

USD

29.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 16.35 Billion | |

| USD 29.39 Billion | |

| % | |

|

Bio Surgical Agents Market Overview

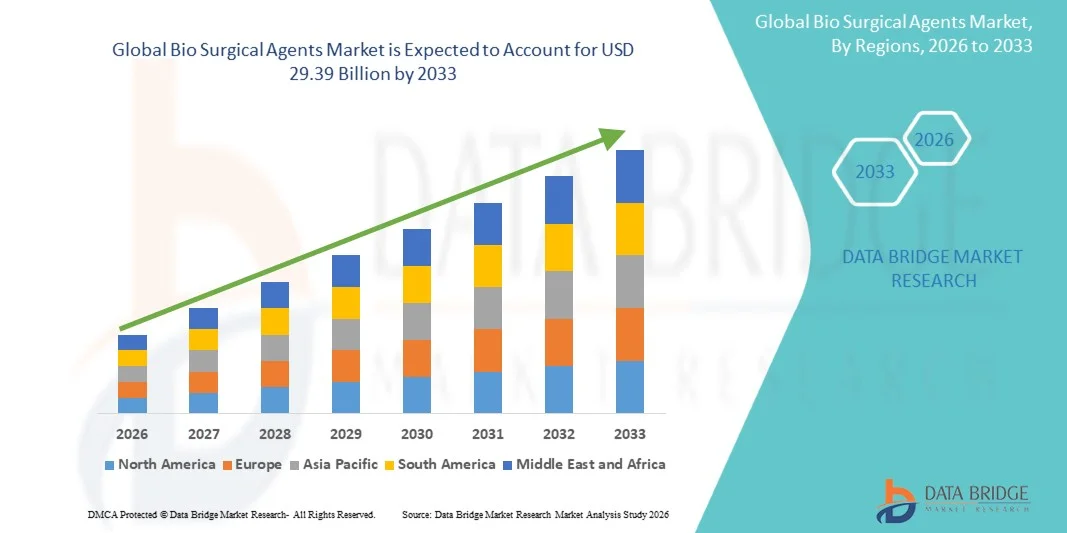

The Bio Surgical Agents Market was valued at USD 16.35 billion in 2025 and is projected to reach USD 29.39 billion by 2033, growing at a CAGR of 7.61% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for advanced hemostatic and tissue sealing solutions, increasing surgical procedure volumes, and rapid advancements in bioengineered surgical technologies across healthcare facilities globally. Growing prevalence of chronic diseases, rising trauma and emergency surgeries, and expanding adoption of minimally invasive surgical procedures are significantly increasing demand for bio surgical agents in hospitals and specialty surgical centers.

The increasing focus on reducing surgical blood loss, minimizing post-operative complications, and improving patient recovery outcomes is compelling healthcare providers and surgeons to adopt advanced bio surgical agents during complex surgical procedures. Hemostatic agents, surgical sealants, adhesion barriers, and tissue repair products are increasingly replacing conventional wound management approaches in many healthcare settings, offering faster bleeding control, reduced infection risk, and improved surgical efficiency. In addition, ongoing advancements in biomaterials, regenerative medicine technologies, and bioactive surgical products are further accelerating the adoption of bio surgical agents across cardiovascular, orthopedic, neurological, and general surgery applications globally.

Key Market Trends & Insights

- North America dominated the Bio Surgical Agents Market with the largest revenue share of 38.46% in 2025, supported by advanced healthcare infrastructure, high surgical procedure volumes, strong adoption of minimally invasive surgeries, and the presence of leading biotechnology and medical device companies.

- The Hemostatic Agents segment led the market with a 32.84% share in 2025, driven by increasing demand for rapid bleeding control solutions during trauma, cardiovascular, orthopedic, and general surgical procedures, along with rising adoption in emergency and minimally invasive surgeries.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by expanding healthcare infrastructure, rising surgical volumes, increasing healthcare expenditure, and growing adoption of advanced surgical technologies across China, India, and Japan.

- The Surgical Sealants and Adhesives segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, reflecting increasing demand for effective wound closure solutions, reduced surgical complications, and improved post-operative recovery outcomes.

- The Orthopedic Surgery segment dominates the application category with a 24.73% revenue share in 2025, supported by rising incidences of fractures, sports injuries, osteoporosis-related conditions, and increasing adoption of bone graft substitutes and tissue repair products in orthopedic procedures.

- Hospitals and specialty surgical centers remain the primary end users of bio surgical agents due to the increasing number of complex surgeries, growing patient admissions, and strong demand for advanced hemostatic and tissue sealing solutions during critical surgical procedures.

- The Bone-Graft Substitutes segment is among the fastest-growing product categories, driven by rising demand for regenerative medicine solutions, increasing spinal fusion and joint replacement surgeries, and growing adoption of synthetic and biologically derived graft materials globally.

Market Size & Forecast

- Global Market Value (2025): USD 16.35 Billion

- Expected Market Value (2033): USD 29.39 Billion

- Forecast CAGR (2026–2033): 7.61%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Bio Surgical Agents Market Segmentation

|

Attributes |

Bio Surgical Agents Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Johnson & Johnson (U.S.) |

|

Market Opportunities |

· Rising demand for minimally invasive and advanced surgical procedures · Growing prevalence of chronic diseases and increasing number of orthopedic · Technological advancements in bioengineered sealants |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Bio Surgical Agents Market Trends

Trend: Increasing Adoption of Advanced Hemostatic and Sealant Technologies

Hospitals and surgical centers are increasingly adopting advanced bio surgical agents such as fibrin sealants, absorbable hemostats, and tissue adhesives to reduce intraoperative blood loss, shorten surgical time, and improve patient recovery outcomes. The growing preference for minimally invasive and robotic-assisted surgeries has accelerated the use of bio surgical products that provide rapid hemostasis and enhanced tissue sealing capabilities. In orthopedic and cardiovascular procedures, surgeons are increasingly utilizing collagen-based and thrombin-based agents to minimize complications and reduce hospital stays.

For instance, in 2024, several healthcare providers across North America and Europe expanded the use of fibrin sealants and adhesion barriers in laparoscopic and reconstructive surgeries to lower post-operative complications and improve surgical efficiency. In addition, the increasing integration of bioactive and regenerative biomaterials in surgical procedures is supporting long-term tissue healing and reducing revision surgery rates.

Bio Surgical Agents Market Dynamics

Key Market Driver: Rising Volume of Surgical Procedures Worldwide

The growing global burden of chronic diseases, trauma injuries, cardiovascular disorders, and orthopedic conditions is significantly driving demand for bio surgical agents. Increasing surgical volumes, particularly among aging populations, are accelerating the need for effective hemostatic products, surgical sealants, and adhesion barriers. According to global healthcare estimates, millions of major surgical procedures are performed annually worldwide, with cardiovascular and orthopedic surgeries accounting for a substantial share of bio surgical agent utilization.

The increasing adoption of minimally invasive surgeries is also boosting market growth, as these procedures require highly efficient bleeding control and tissue management solutions. In addition, rising healthcare expenditure and expansion of hospital infrastructure in emerging economies are supporting broader adoption of advanced surgical products.

Key Restraint/Challenge: High Cost of Advanced Bio Surgical Products

A major challenge in the Bio Surgical Agents Market is the high cost associated with advanced biologic sealants, hemostatic matrices, and regenerative surgical materials. Premium products such as fibrin-based sealants and synthetic adhesion barriers involve complex manufacturing processes, stringent regulatory approvals, and specialized storage requirements, increasing overall treatment costs.

Smaller hospitals and healthcare facilities in developing regions often face budget limitations that restrict adoption of high-end bio surgical products. In addition, reimbursement challenges in certain healthcare systems further limit widespread utilization. Product recalls and concerns regarding biocompatibility and infection risks associated with animal-derived materials also create operational and regulatory hurdles for manufacturers.

Key Market Opportunity: Expansion of Regenerative and Bioengineered Surgical Solutions

The development of regenerative biomaterials and bioengineered surgical agents presents significant growth opportunities for market players. Companies are increasingly investing in next-generation tissue sealants, synthetic hemostats, and bioactive scaffolds that promote faster tissue regeneration and improved wound healing outcomes.

The growing application of bio surgical agents in neurosurgery, reconstructive surgery, and sports medicine is expanding the market scope beyond traditional procedures. In addition, advancements in nanotechnology, biodegradable polymers, and stem-cell-compatible biomaterials are enabling the development of innovative surgical products with enhanced performance and reduced adverse reactions.

Emerging economies across Asia-Pacific, Latin America, and the Middle East are also witnessing increasing investments in healthcare infrastructure and surgical capabilities, creating favorable opportunities for manufacturers to expand their global footprint.

Bio Surgical Agents Market Scope

The Bio Surgical Agents market is segmented on the basis of product and application.

By Product

On the basis of product, the Bio Surgical Agents Market is segmented into bone-graft substitutes, soft-tissue attachments, hemostatic agents, surgical sealants & adhesives, adhesion barriers, and staple-line reinforcement agents. The Hemostatic Agents segment led the market with a 32.84% share in 2025, driven by increasing demand for rapid bleeding control solutions during trauma, cardiovascular, orthopedic, and general surgical procedures, along with rising adoption in emergency and minimally invasive surgeries. Increasing surgical volumes globally, rising prevalence of chronic diseases requiring surgical intervention, and growing demand for rapid blood loss management solutions are significantly supporting segment growth. Hospitals and surgical centers are increasingly adopting advanced absorbable hemostats, thrombin-based products, and flowable hemostatic matrices to improve surgical efficiency and patient safety. In addition, the rising number of minimally invasive and robotic-assisted surgeries is increasing demand for effective intraoperative bleeding control products. Continuous product innovations by leading companies such as Baxter International, Johnson & Johnson, and Pfizer are further accelerating adoption. The growing geriatric population, rising emergency surgeries, and increasing healthcare expenditure are also contributing to the dominance of the hemostatic agents segment globally.

The Surgical Sealants & Adhesives segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing demand for minimally invasive surgeries, faster wound closure technologies, and enhanced postoperative healing solutions. Surgical sealants are increasingly being used in cardiovascular, thoracic, pulmonary, and reconstructive surgeries to reduce leakage, prevent infections, and improve tissue sealing efficiency. Technological advancements in biodegradable adhesives, fibrin sealants, and synthetic polymer-based products are improving product performance and expanding clinical applications. In addition, growing adoption of robotic-assisted and laparoscopic surgeries is increasing the need for precise tissue bonding and sealing solutions. Rising healthcare investments, increasing awareness regarding surgical complication reduction, and expanding product approvals across developed and emerging healthcare markets are further supporting segment expansion. Increasing R&D activities focused on bioengineered adhesives and regenerative surgical technologies are also expected to create strong future growth opportunities for this segment globally.

By Application

On the basis of application, the Bio Surgical Agents Market is segmented into general surgery, cardiovascular surgery, orthopedic surgery, neurological surgery, reconstructive surgery, gynecological surgery, thoracic surgery, and urological surgery. The Orthopedic Surgery segment dominated the market with a share of 28.46% in 2025 due to the rising incidence of bone fractures, osteoarthritis, spinal disorders, sports injuries, and increasing joint replacement procedures globally. Bone-graft substitutes, surgical sealants, and soft-tissue fixation products are extensively used in orthopedic procedures to improve healing outcomes, reduce recovery time, and enhance surgical precision. Increasing aging population, growing prevalence of musculoskeletal disorders, and rising demand for minimally invasive orthopedic surgeries are significantly driving segment growth. In addition, advancements in regenerative biomaterials, bioactive scaffolds, and synthetic bone graft technologies are improving surgical success rates and expanding product adoption across hospitals and specialty orthopedic centers. Growing healthcare infrastructure development and rising investments in advanced orthopedic care solutions are further reinforcing the dominance of the orthopedic surgery segment in the global market.

The Cardiovascular Surgery segment is projected to register the fastest CAGR of 8.4% from 2026 to 2033, driven by the increasing global burden of cardiovascular diseases, rising cardiac surgery volumes, and growing adoption of advanced hemostatic and tissue sealing technologies. Surgical sealants, adhesion barriers, and staple-line reinforcement agents are increasingly being used in complex cardiac and vascular procedures to minimize bleeding complications and improve surgical outcomes. Rising demand for minimally invasive cardiac surgeries, increasing elderly population, and growing prevalence of coronary artery disease and heart valve disorders are significantly accelerating segment growth. In addition, technological advancements in bioresorbable surgical agents and improved biocompatibility materials are expanding the use of biosurgical products in high-risk cardiovascular procedures. Increasing investments in specialized cardiac care infrastructure, favorable reimbursement policies, and rising adoption of robotic-assisted cardiovascular surgeries are further expected to support rapid expansion of this segment globally.

Bio Surgical Agents Market Regional Analysis

North America dominated the Bio Surgical Agents market and accounted for the largest revenue share of 38.46% in 2025, supported by advanced healthcare infrastructure, high surgical procedure volumes, strong adoption of minimally invasive surgeries, and the presence of leading biotechnology and medical device companies. The region also benefits from rising demand for advanced wound management solutions, increasing prevalence of chronic diseases requiring surgical intervention, and growing use of hemostatic agents, sealants, and adhesion barriers across hospitals and ambulatory surgical centers. Increasing investments in surgical innovation and regenerative medicine technologies continue to strengthen North America’s leadership position in the global market.

U.S. Bio Surgical Agents Market Insight

The U.S. Bio Surgical Agents market is witnessing strong growth due to increasing surgical procedure volumes, rising prevalence of cardiovascular and orthopedic disorders, and growing adoption of minimally invasive surgical techniques. The country’s advanced healthcare ecosystem, along with the strong presence of leading biotechnology and medical device manufacturers, is driving demand for hemostatic agents, surgical sealants, adhesion barriers, and bone-graft substitutes across hospitals and specialty surgical centers. In addition, increasing investments in robotic-assisted surgeries, regenerative medicine, and advanced wound care technologies are accelerating market expansion in the U.S.

Europe Bio Surgical Agents Market Insight

The Europe Bio Surgical Agents market remains a major contributor to global revenue, driven by strong healthcare infrastructure, increasing surgical procedure demand, and high adoption of advanced biosurgical technologies. The widespread use of surgical sealants, tissue adhesives, and hemostatic products in cardiovascular, orthopedic, neurological, and reconstructive surgeries is supporting market expansion across the region. Increasing investments in minimally invasive surgery technologies, combined with favorable reimbursement policies and rising healthcare modernization initiatives, continue to enhance the adoption of Bio Surgical Agents throughout Europe.

U.K. Bio Surgical Agents Market Insight

The U.K. Bio Surgical Agents market is experiencing steady growth, supported by rising demand for advanced surgical care, increasing prevalence of chronic diseases, and growing adoption of minimally invasive procedures. Increasing investments in hospital modernization, surgical efficiency improvement programs, and advanced patient care technologies are contributing to market growth. Furthermore, growing use of bioengineered hemostats, tissue sealants, and adhesion prevention products in complex surgical procedures is improving patient outcomes and strengthening the country’s position in the Bio Surgical Agents industry.

Germany Bio Surgical Agents Market Insight

The Germany Bio Surgical Agents market is expanding steadily due to the country’s strong medical technology industry, advanced surgical infrastructure, and increasing adoption of next-generation biosurgical products. Hospitals and specialty surgical centers are increasingly utilizing hemostatic agents, bone-graft substitutes, and surgical adhesives to improve surgical precision, reduce complications, and enhance postoperative recovery. Continuous advancements in biomaterials, regenerative medicine, and minimally invasive surgical technologies, along with strong government focus on healthcare innovation, are further driving market growth in Germany.

Asia-Pacific Bio Surgical Agents Market Insight

The Asia-Pacific Bio Surgical Agents market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising surgical procedure volumes, and increasing healthcare expenditure across countries such as China, India, and Japan. Growing awareness regarding advanced surgical care, rising adoption of minimally invasive surgeries, and increasing demand for cost-effective surgical solutions are supporting regional market expansion. In addition, the growing presence of medical device manufacturers, improving hospital facilities, and increasing investments in healthcare modernization are accelerating the adoption of Bio Surgical Agents across commercial and public healthcare sectors.

Japan Bio Surgical Agents Market Insight

The Japan Bio Surgical Agents market is witnessing consistent growth due to rising demand for advanced surgical technologies, increasing aging population, and growing prevalence of chronic diseases requiring surgical intervention. Hospitals and healthcare providers are increasingly adopting high-performance hemostatic agents, surgical sealants, and bone regeneration products to improve surgical outcomes and patient safety. Moreover, increasing integration of regenerative medicine technologies and the country’s focus on high-quality healthcare delivery are further contributing to market growth.

China Bio Surgical Agents Market Insight

The China Bio Surgical Agents market is growing rapidly, driven by expanding healthcare infrastructure, rising surgical procedure volumes, and increasing government investments in advanced healthcare technologies. Growing adoption of minimally invasive surgeries, increasing demand for advanced wound closure and bleeding management products, and rising healthcare awareness are significantly boosting market demand. In addition, rapid expansion of hospitals, increasing medical tourism, and continuous advancements in biotechnology and biomaterials are positioning China as one of the fastest-growing markets for Bio Surgical Agents globally.

Bio Surgical Agents Market Share

The Bio Surgical Agents industry is primarily led by well-established companies, including:

- Johnson & Johnson (U.S.)

- Baxter International Inc. (U.S.)

- Becton, Dickinson and Company (U.S.)

- Medtronic plc (Ireland)

- Stryker Corporation (U.S.)

- B. Braun SE (Germany)

- Integra LifeSciences Holdings Corporation (U.S.)

- CryoLife Inc. (U.S.)

- Cohera Medical Inc. (U.S.)

- Tissuemed Ltd. (U.K.)

- Sanofi S.A. (France)

- Pfizer Inc. (U.S.)

- CSL Limited (Australia)

- Zimmer Biomet Holdings Inc. (U.S.)

- Smith & Nephew plc (U.K.)

- 3M Company (U.S.)

- Ethicon Inc. (U.S.)

- Cardinal Health Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- Aroa Biosurgery Limited (New Zealand)

- SeaSpine Holdings Corporation (U.S.)

- Anika Therapeutics Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- Advanced Medical Solutions Group plc (U.K.)

- Gelita Medical GmbH (Germany)

Latest Developments in Bio Surgical Agents Market

- In November 2023, Johnson & Johnson through its Ethicon division received European approval for the launch of the ETHIZIA hemostatic sealing patch, designed to control internal organ bleeding and improve surgical efficiency in complex procedures. The development strengthened the company’s biosurgery and advanced wound management portfolio across Europe

- In December 2022, Integra LifeSciences Holdings Corporation announced the acquisition of Surgical Innovation Associates, a company specializing in bioengineered surgical reconstruction technologies. The acquisition expanded Integra’s regenerative medicine and reconstructive surgery capabilities within the Bio Surgical Agents Market

- In March 2024, Johnson & Johnson introduced upgraded versions of its SURGIFLO and EVARREST hemostatic products with enhanced shelf life and improved operating-room usability. The development aimed to strengthen efficiency in minimally invasive and high-volume surgical procedures

- In February 2025, Becton, Dickinson and Company received FDA PMA supplement approvals for key enhancements to its Tridyne vascular sealant platform, including reduced particulate testing requirements and supplier qualification modifications. The approvals improved operational flexibility and regulatory efficiency for vascular surgery applications

- In January 2025, Johnson & Johnson presented updated clinical data for its EVICEL fibrin sealant at a major thoracic surgery conference, demonstrating significant reduction in post-operative chest tube drainage in cardiovascular surgery patients compared with conventional treatment approaches

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.