Global Biohazard Bags Market

Market Size in USD Billion

USD

499.56 Billion

USD

792.62 Billion

2025

2033

USD

499.56 Billion

USD

792.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 499.56 Billion | |

| USD 792.62 Billion | |

| % | |

|

Biohazard Bags Market Overview

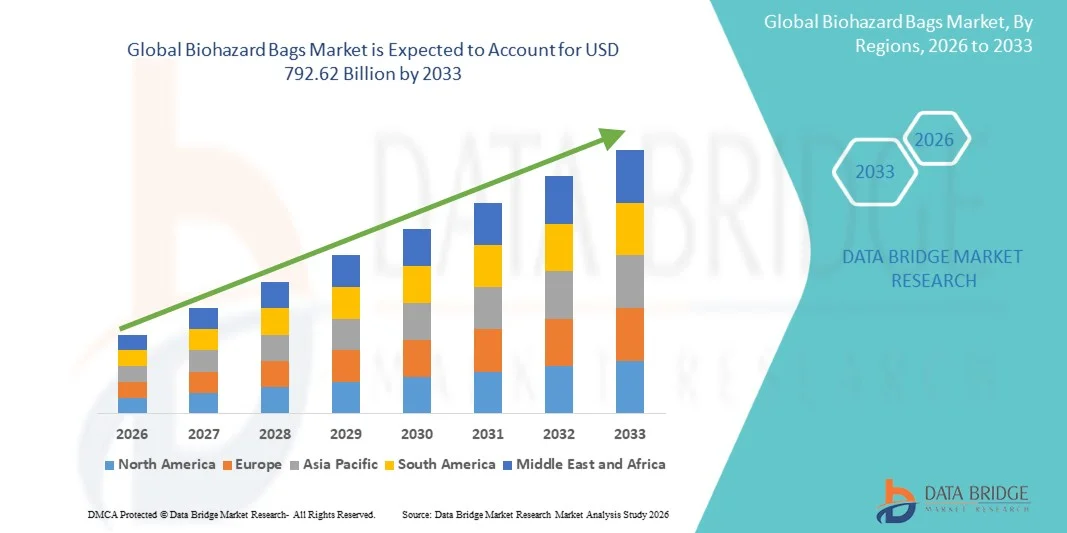

The Biohazard Bags Market was valued at USD 499.56 billion in 2025 and is projected to reach USD 792.62 billion by 2033, growing at a CAGR of 5.94% from 2026 to 2033. The Biohazard Bags market is witnessing steady growth driven by rising demand for safe medical waste disposal solutions, increasing hospital admissions, and strict global regulations for infection control and biomedical waste management. Growing awareness regarding healthcare-associated infections (HAIs) and the need for proper segregation of hazardous waste are further supporting market expansion across hospitals, diagnostic laboratories, and research facilities.

The increasing volume of medical procedures, combined with rising prevalence of infectious diseases and surgical interventions, is compelling healthcare providers, laboratories, and pharmaceutical companies to adopt standardized biohazard waste handling systems. Strong regulatory frameworks from organizations such as WHO and environmental safety agencies are enforcing the use of color-coded and leak-proof biohazard bags for safe containment and disposal. High-density polyethylene (HDPE) and polypropylene-based biohazard bags are increasingly replacing conventional disposal methods, offering puncture resistance, chemical stability, and infection control efficiency in both developed and emerging healthcare markets.

Key Market Trends & Insights

- North America dominated the Biohazard Bags Market with the largest revenue share of 39.18% in 2025, supported by strong healthcare infrastructure, high hospital waste generation, strict biomedical waste management regulations, and widespread adoption of standardized infection control practices across the United States and Canada.

- The Medium segment dominated the market with a 46.73% share in 2025, due to its strong balance between affordability and regulatory compliance

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.8% from 2026 to 2033, fueled by expanding healthcare infrastructure, rising hospital admissions, increasing awareness of biomedical waste management, and rapid urbanization in China, India, and Southeast Asia.

- The HDPE (High-Density Polyethylene) segment is the fastest-growing material type, projected to register a CAGR of 7.1%, owing to its high strength, puncture resistance, and cost-effectiveness in handling infectious and hazardous medical waste.

- The Commercial segment dominates the end-use category with a 46.52% revenue share in 2025, led by hospitals, diagnostic centers, and pharmaceutical companies generating large volumes of biomedical waste requiring safe disposal solutions.

- The Modern Trade Channels segment accounts for a 38.74% market share in 2025, supported by strong procurement from hospitals and institutional buyers through organized medical supply distributors and bulk procurement systems.

- The Highly Infectious Waste segment is the fastest-growing application category, with a CAGR of 7.3%, driven by increasing prevalence of infectious diseases, surgical procedures, and stricter compliance requirements for safe containment and disposal of high-risk biomedical waste.

Market Size & Forecast

- Global Market Value (2025): USD 499.56 Billion

- Expected Market Value (2033): USD 792.62 Billion

- Forecast CAGR (2026–2033): 5.94%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Biohazard Bags Market Segmentation

|

Attributes |

Biohazard Bags Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Thermo Fisher Scientific Inc. (U.S.) |

|

Market Opportunities |

· Rising demand for infection control in healthcare facilities · Expansion of healthcare infrastructure in emerging markets · Growth in pharmaceutical and biotechnology R&D activities |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Biohazard Bags Market Trends

Trend: Rising Demand for Healthcare Waste Management and Infection Control Compliance

The Biohazard Bags Market is witnessing strong growth driven by increasing healthcare waste generation, strict biomedical waste management regulations, and rising emphasis on infection control in hospitals and laboratories. According to the World Health Organization (WHO), approximately 15% of total healthcare waste is considered hazardous, requiring specialized containment and disposal solutions such as biohazard bags. Hospitals, diagnostic laboratories, and pharmaceutical manufacturing units are increasingly adopting color-coded, puncture-resistant, and leak-proof biohazard bags to comply with regulatory frameworks such as WHO biomedical waste guidelines and national hazardous waste management rules. In addition, the expansion of healthcare infrastructure in emerging economies is significantly increasing demand for cost-effective and compliant medical waste disposal solutions.

Biohazard Bags Market Dynamics

Key Market Driver: Rising Healthcare Infrastructure Expansion and Infectious Waste Generation

The Biohazard Bags market is primarily driven by the rapid expansion of healthcare facilities, increasing surgical procedures, and rising incidence of infectious diseases globally. The growth of hospitals, diagnostic centers, and COVID-19-related legacy waste management has significantly increased the volume of biomedical waste requiring safe containment. For example, large hospitals can generate several tons of infectious waste per month, necessitating high-strength HDPE and polypropylene-based biohazard bags for safe disposal. Increasing adoption of strict infection prevention protocols in healthcare institutions, supported by government regulations, is further accelerating market demand. In addition, rising pharmaceutical and biotechnology research activities are increasing the need for safe disposal of chemical and biological waste.

Key Restraint/Challenge: Environmental Concerns and High Cost of Compliant Waste Management Systems

A major challenge in the Biohazard Bags Market is the environmental impact of plastic-based medical waste products and the rising cost of compliant waste management systems. Most biohazard bags are made from HDPE, LDPE, and polypropylene, which contribute to plastic waste accumulation if not properly incinerated or treated. In addition, compliance with stringent biomedical waste disposal regulations requires hospitals and laboratories to invest in segregation systems, color-coded packaging, and certified disposal infrastructure, increasing operational costs. In developing regions, limited access to centralized waste treatment facilities further restricts efficient adoption. For instance, rural healthcare centers often lack proper segregation and disposal systems, leading to improper waste handling practices.

Key Market Opportunity: Adoption of Sustainable and High-Performance Medical Waste Solutions

The integration of biodegradable polymers, recyclable plastics, and antimicrobial-coated biohazard bags presents a significant growth opportunity in the market. Manufacturers are increasingly focusing on eco-friendly materials to reduce environmental impact while maintaining durability and compliance standards. Governments in regions such as Europe and Asia-Pacific are promoting sustainable medical waste management practices, encouraging innovation in green packaging solutions. In addition, increasing investments in smart healthcare systems and hospital automation are enabling better waste tracking, segregation, and disposal efficiency. Growing demand from pharmaceutical manufacturing plants, biotechnology labs, and large hospital networks is further supporting the adoption of advanced, regulation-compliant biohazard bag solutions globally.

Biohazard Bags Market Scope

The Biohazard Bags market is segmented on the basis of simulation type, vehicle type, training application, end user, hardware components, software components, training mode, integration & connectivity, deployment and support & services.

- By Capacity Type

On the basis of capacity type, the Biohazard Bags Market is segmented into Less Than 15 Gallon, 16 Gallon–30 Gallon, and Above 30 Gallon. The 16 Gallon–30 Gallon segment dominated the market with a 42.18% share in 2025, owing to its optimal balance between capacity and usability in hospitals, laboratories, and diagnostic centers. These bags are widely used for routine biomedical waste collection across surgical wards, ICUs, and pathology labs. Their standardized size ensures compliance with biomedical waste segregation rules in major healthcare systems. Increasing hospital admissions and outpatient procedures are further driving demand. Strong adoption in developed healthcare systems such as North America and Europe supports segment dominance. Rising focus on infection control protocols enhances usage consistency. Cost-effectiveness compared to larger capacity bags supports procurement preference. Compatibility with standard hospital waste bins strengthens adoption. The segment benefits from high replacement frequency in healthcare settings. Regulatory mandates for safe waste handling further reinforce demand. Growing healthcare infrastructure in emerging economies is also supporting market expansion.

The Above 30 Gallon segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing biomedical waste generation in large hospitals and multi-specialty healthcare centers. Expansion of tertiary care hospitals is significantly boosting demand for high-capacity waste containment solutions. Rising surgical volumes and critical care admissions are increasing bulk waste output. Pandemic preparedness initiatives are supporting adoption of larger disposal systems. Industrial-scale pharmaceutical and biotech facilities are contributing to demand. Growing healthcare investments in Asia-Pacific are accelerating adoption. Larger capacity bags reduce handling frequency and operational inefficiencies. Improved strength and puncture resistance are enhancing usability. Waste management outsourcing services are expanding usage. Government regulations promoting centralized waste handling are supporting growth. Increasing hospital bed capacity globally is a key driver. Rising awareness of infection prevention is further accelerating adoption.

- By Price Type

On the basis of price type, the market is segmented into Premium, Medium, and Low. The Medium segment dominated the market with a 46.73% share in 2025, due to its strong balance between affordability and regulatory compliance. Hospitals and diagnostic laboratories prefer medium-priced bags for daily biomedical waste disposal. These products meet essential safety and durability standards required in healthcare environments. High adoption in public healthcare systems supports dominance. Cost-sensitive emerging markets significantly contribute to demand. Medium-grade bags are widely available through established distribution channels. Procurement efficiency in bulk purchasing strengthens usage. Standardized production reduces cost variability. Growing hospital networks globally are increasing consumption volume. Government healthcare programs favor cost-effective compliance solutions. Moderate durability makes them suitable for routine applications. Strong replacement cycles in hospitals support steady demand.

The Premium segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by rising demand for advanced infection-control solutions. Premium bags offer superior puncture resistance and leak-proof performance. Increasing use in pharmaceutical manufacturing and biotechnology labs is driving adoption. Hospitals handling high-risk infectious waste prefer premium-grade materials. Antimicrobial-coated biohazard bags are gaining traction. Strict regulatory compliance requirements are supporting premiumization. Growth of specialized surgical procedures is increasing demand. Developed regions such as North America and Europe are major contributors. Advanced healthcare infrastructure supports premium product uptake. Rising awareness of occupational safety is boosting adoption. Innovation in biodegradable premium materials is expanding market scope. Healthcare quality standards are pushing higher-value procurement.

- By Material Type

On the basis of material type, the market is segmented into HDPE, High Molecular Weight HDPE, LDPE, LLDPE, Polymer, Plastic, PP, and Others. The HDPE (High-Density Polyethylene) segment dominated the market with a 39.84% share in 2025, owing to its high strength, chemical resistance, and cost-effectiveness. HDPE bags are widely used in hospitals and laboratories for safe disposal of infectious waste. Their durability ensures leak-proof containment of hazardous materials. Strong puncture resistance makes them suitable for sharp waste handling. High availability of raw materials supports large-scale production. Regulatory acceptance across global healthcare systems strengthens demand. Hospitals prefer HDPE due to low cost and high reliability. Strong usage in public healthcare facilities drives volume. Established manufacturing infrastructure supports supply chain efficiency. Increasing biomedical waste generation supports steady consumption. Easy recyclability in controlled systems enhances adoption. Wide application across healthcare segments reinforces dominance.

The PP (Polypropylene) segment is expected to witness the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by superior thermal resistance and mechanical strength. PP-based bags are increasingly used in high-risk infectious and chemical waste applications. Rising demand from pharmaceutical manufacturing is accelerating growth. Biotechnology labs prefer PP for advanced containment needs. Improved durability compared to conventional plastics supports adoption. Growth in high-temperature waste disposal processes is boosting demand. Increasing focus on advanced infection control is supporting usage. Regulatory push for safer biomedical waste handling is driving adoption. Innovation in multilayer PP films is expanding applications. Healthcare modernization in Asia-Pacific is fueling demand. Rising surgical waste volumes are supporting consumption growth. Environmental compliance requirements are increasing PP usage.

- By Sales Channel

On the basis of sales channel, the market is segmented into Modern Trade Channels, Third Party Online Channels, Direct-to-Customer Online Channels, Wholesalers/Suppliers, and Local Retailers. The Wholesalers/Suppliers segment dominated the market with a 37.26% share in 2025, due to strong bulk procurement by hospitals and laboratories. Centralized purchasing systems in healthcare institutions support large-volume distribution. Established supplier networks ensure regulatory compliance. Strong presence in government healthcare procurement drives demand. Cost advantages in bulk distribution strengthen dominance. Reliable supply chains support consistent availability. Hospitals prefer long-term supplier contracts. Growing healthcare infrastructure enhances bulk purchasing. Strong logistics networks improve delivery efficiency. Standardized pricing models support adoption. Industrial-scale procurement in pharma sector adds demand. High repeat purchase cycles sustain segment leadership.

The Third Party Online Channels segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by increasing digital procurement adoption. Small clinics and laboratories prefer online purchasing platforms. E-commerce expansion in medical supplies is boosting accessibility. Digital supply chain integration is improving efficiency. Faster procurement cycles support adoption. Growing penetration of healthcare e-marketplaces is accelerating growth. Price transparency is attracting buyers. Online platforms offer wider product variety. Rising SME healthcare providers are driving demand. Convenience in ordering is boosting usage. Expansion of B2B medical portals is supporting growth. Technological adoption in procurement systems is increasing rapidly.

- By End Use

On the basis of end use, the market is segmented into Commercial, Industrial, and Residential. The Commercial segment dominated the market with a 58.91% share in 2025, driven by hospitals, clinics, and diagnostic centers generating large volumes of biomedical waste. Increasing patient inflow globally supports demand growth. Strong regulatory enforcement in healthcare waste management is a key driver. Rising surgical procedures are increasing waste output. Expansion of healthcare infrastructure supports consumption. High adoption in urban hospitals strengthens dominance. Government healthcare programs boost procurement. Strict infection control protocols drive usage. Large-scale diagnostic laboratories contribute significantly. Pharmaceutical companies also support demand. Continuous waste generation ensures recurring consumption. Strong institutional procurement systems reinforce leadership.

The Industrial segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by pharmaceutical and biotechnology expansion. Increasing R&D activities are generating hazardous waste. Clinical trial growth is boosting demand. Industrial laboratories require advanced containment systems. Rising production of biologics is increasing waste output. Expansion of manufacturing facilities supports adoption. Strict environmental regulations drive compliance needs. High-volume waste handling requirements support growth. Growing contract manufacturing organizations (CMOs) are contributing demand. Increasing biotech startups are boosting consumption. Industrial healthcare waste management outsourcing is rising. Technological upgrades in industrial waste systems are accelerating adoption.

- By Application

On the basis of application, the market is segmented into Highly Infectious, Other Infectious, Sharps, Chemical and Pharmaceutical, General Healthcare Waste, and Others. The Highly Infectious segment dominated the market with a 34.67% share in 2025, driven by strict infection control protocols in hospitals. Rising prevalence of infectious diseases increases waste generation. COVID-19 legacy waste management continues to support demand. Strong adoption in ICUs and isolation wards drives usage. Regulatory guidelines mandate specialized disposal systems. Hospitals prioritize safety in infectious waste handling. Growing awareness of hospital-acquired infections supports adoption. High-risk waste requires durable containment solutions. Government healthcare policies reinforce usage standards. Expansion of infectious disease treatment centers supports demand. Increased global pandemic preparedness strengthens segment dominance. High replacement cycles in healthcare systems ensure steady consumption.

The Chemical and Pharmaceutical segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by expanding pharmaceutical production and R&D activities. Increasing clinical trials generate chemical waste requiring safe disposal. Biotechnology expansion is accelerating demand. Strict environmental compliance regulations support growth. Rising use of hazardous chemicals in labs increases adoption. Pharmaceutical manufacturing plants are key contributors. Growth in contract research organizations boosts demand. Expansion of drug development pipelines supports usage. Increasing focus on safe chemical waste management drives adoption. Industrial laboratories require specialized containment solutions. Regulatory pressure on chemical disposal is increasing globally. Innovation in chemical-resistant biohazard materials supports expansion.

Biohazard Bags Market Regional Analysis

North America dominated the Biohazard Bags market and accounted for the largest revenue share of 39.18% in 2025, supported by strong healthcare infrastructure, high hospital waste generation, strict biomedical waste management regulations, and widespread adoption of standardized infection control practices across the United States and Canada. The region benefits from advanced hospital networks, high surgical volumes, and well-established waste segregation systems in clinical environments. Increasing focus on infection prevention, regulatory compliance, and safe disposal of hazardous medical waste continues to strengthen North America’s leadership position in the global market.

U.S. Biohazard Bags Market Insight

The U.S. Biohazard Bags market is witnessing strong growth due to rising hospital admissions, increasing surgical procedures, and strict enforcement of biomedical waste disposal regulations. The country’s advanced healthcare infrastructure and high awareness of infection control practices are driving consistent demand for certified and leak-proof biohazard packaging solutions. In addition, expanding pharmaceutical and diagnostic laboratory activities are further supporting market growth across commercial healthcare facilities.

Europe Biohazard Bags Market Insight

The Europe Biohazard Bags market remains a major contributor to global revenue, driven by stringent environmental regulations, strong healthcare systems, and high adoption of standardized medical waste management protocols. The region’s well-developed hospital infrastructure and increasing focus on sustainability in healthcare waste disposal are supporting steady demand. Growing emphasis on infection control and circular economy practices in healthcare systems is further strengthening market expansion across Europe.

U.K. Biohazard Bags Market Insight

The U.K. Biohazard Bags market is experiencing steady growth, supported by rising hospital waste generation, strict NHS waste management guidelines, and increasing awareness of infection prevention protocols. The country’s strong healthcare system and growing demand for compliant and safe medical waste disposal solutions are contributing to market expansion. Integration of advanced waste segregation and traceability systems is further improving efficiency in biomedical waste handling.

Germany Biohazard Bags Market Insight

The Germany Biohazard Bags market is expanding steadily due to strong healthcare infrastructure, high regulatory standards for medical waste management, and increasing hospital and laboratory activities. The country’s focus on environmental safety and strict compliance with biomedical waste disposal laws is driving adoption of high-quality biohazard packaging solutions. Continuous improvements in healthcare efficiency and waste management systems are further supporting market growth.

Asia-Pacific Biohazard Bags Market Insight

The Asia-Pacific Biohazard Bags market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising hospital admissions, increasing awareness of biomedical waste management, and rapid urbanization in countries such as China, India, and Southeast Asia. Growing investments in public healthcare systems and improving waste disposal regulations are supporting strong regional expansion. Additionally, rising healthcare expenditure and increasing adoption of standardized infection control practices are accelerating market growth across the region.

Japan Biohazard Bags Market Insight

The Japan Biohazard Bags market is witnessing consistent growth due to advanced healthcare infrastructure, high hospital efficiency standards, and strict biomedical waste management regulations. The country’s aging population and increasing medical procedures are driving steady demand for safe and compliant waste disposal solutions. Continuous technological improvements in healthcare waste segregation systems are further enhancing operational efficiency in hospitals and clinics.

China Biohazard Bags Market Insight

The China Biohazard Bags market is growing rapidly, driven by expanding healthcare infrastructure, increasing hospital admissions, and rising government focus on biomedical waste management regulations. Growing awareness of infection control and rapid urbanization are significantly boosting demand for standardized biohazard disposal solutions. In addition, rising investments in public health systems and hospital expansion projects are positioning China as one of the fastest-growing markets globally.

Biohazard Bags Market Share

The Biohazard Bags industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Merck KGaA (Germany)

- Avantor, Inc. (U.S.)

- Corning Incorporated (U.S.)

- SABIC (Saudi Arabia)

- Berry Global Inc. (U.S.)

- Mondi Group (Austria)

- Amcor plc (Switzerland)

- Graham Medical (U.S.)

- Dynarex Corporation (U.S.)

- Medline Industries, LP (U.S.)

- Hindalco Industries Ltd. (India)

- Uflex Ltd. (India)

- Cosmo Films Ltd. (India)

- Klöckner Pentaplast (Germany)

- Wipak Group (Finland)

- Coveris Holdings S.A. (Austria)

- Sealed Air Corporation (U.S.)

- Huhtamaki Oyj (Finland)

- Plastipak Holdings, Inc. (U.S.)

- Berry Medical (U.S.)

- Shanghai Zhisheng Packaging (China)

- SinoPack Medical Supplies (China)

- Narang Medical Limited (India)

- Polypak Packaging (South Africa)

- Alpha Pro Tech Ltd. (Canada)

- International Plastics Inc. (U.S.)

- TC Transcontinental (Canada)

- Supermax Corporation Berhad (Malaysia)

- DS Smith Plc (U.K.)

Latest Developments in Biohazard Bags Market

- In March 2026, several healthcare packaging manufacturers introduced next-generation biohazard bags made from high-density recycled HDPE and multi-layer leak-resistant polymer blends, aimed at improving puncture resistance and compliance with updated WHO biomedical waste segregation guidelines. These upgraded products are increasingly being adopted in hospitals and diagnostic laboratories to enhance infection control efficiency and reduce environmental impact through sustainable medical waste management solutions

- In November 2025, leading medical packaging suppliers expanded production capacity for color-coded biohazard waste bags integrated with QR-based traceability systems, enabling real-time tracking of infectious waste from point-of-generation to final disposal. This development is strengthening hospital compliance with stricter biomedical waste auditing regulations and improving transparency in healthcare waste handling processes

- In June 2025, advancements in antimicrobial-coated biohazard bags were commercialized, incorporating silver-ion and chemical-resistant layers designed to reduce pathogen survival on external surfaces. These innovations are being increasingly deployed in high-risk clinical environments such as ICUs, pathology labs, and infectious disease wards to minimize cross-contamination risks

- In February 2025, regulatory updates across Europe and North America led to the introduction of upgraded ASTM and EN-compliant biohazard bag standards, requiring higher tensile strength, enhanced leak-proof sealing, and improved color-coding accuracy. Manufacturers responded by launching reinforced LDPE and LLDPE-based product lines to meet the revised safety requirements

- In August 2024, major healthcare waste management companies adopted automated waste segregation systems integrated with smart biohazard bag identification, using barcode and RFID-enabled tagging to streamline hospital waste tracking and reduce manual handling errors. This innovation improved operational efficiency in large hospital networks and centralized waste treatment facilities

- In December 2023, increasing global demand for sustainable healthcare packaging led to the introduction of biodegradable and partially compostable biohazard bags in pilot healthcare programs across Asia-Pacific and Europe, targeting reduction in plastic waste from medical disposal systems while maintaining infection containment standards

- In May 2022, several emerging market manufacturers expanded exports of low-cost standardized biohazard bags to government hospitals under public healthcare procurement programs, improving access to compliant biomedical waste disposal solutions in developing regions with rising hospital infrastructure growth

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.