Global Biosimilars Manufacturing Market

Market Size in USD Billion

USD

8.43 Billion

USD

16.30 Billion

2025

2033

USD

8.43 Billion

USD

16.30 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.43 Billion | |

| USD 16.30 Billion | |

| % | |

|

Biosimilars Manufacturing Market Overview

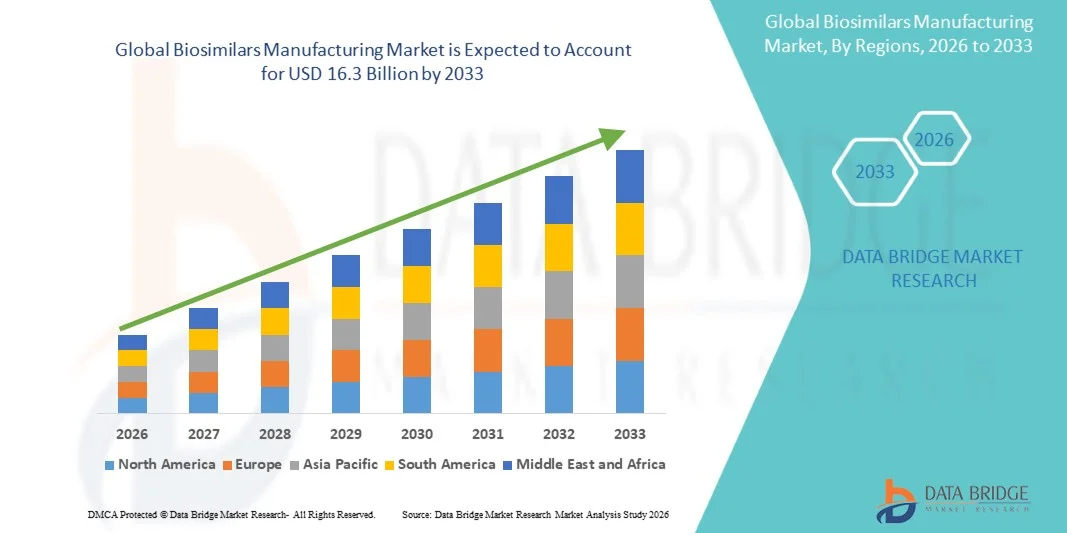

As per Data Bridge Market Research Analysis The biosimilars manufacturing market was valued at USD 8.43 billion in 2025 and is projected to reach USD 16.3 billion by 2033, growing at a CAGR of 8.60% from 2026 to 2033 during the forecast period.

Biosimilars manufacturing involves the contract development and production of biologic medicines that are highly similar to already approved reference biologics. These products offer cost-effective alternatives to expensive branded biologics used in treating chronic diseases such as cancer, autoimmune disorders, and diabetes. The complex manufacturing processes involved in biosimilar production require advanced biologic expertise, regulatory compliance, and specialized facilities, which have led many pharmaceutical companies to partner with contract development and manufacturing organizations (CDMOs) to streamline production. The market is experiencing growth driven by patent expirations of blockbuster biologics, increasing demand for affordable biologic therapies, supportive regulatory frameworks, and the rising prevalence of chronic diseases worldwide.

Market Size & Forecast

- Global Market Value (2025): USD 8.43 Billion

- Expected Market Value (2033): USD 16.3 Billion

- Forecast CAGR (2026–2033): 8.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America accounted for the largest revenue share of the biosimilars manufacturing market in 2025, holding approximately 37% of the global market, supported by a strong biopharmaceutical ecosystem, advanced manufacturing infrastructure, and robust regulatory support for biosimilars from the U.S. FDA.

- Europe maintained a significant market share in 2025, driven by early biosimilar adoption, strong regulatory support from the European Medicines Agency (EMA), and established biologics manufacturing capabilities across the region.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 14.5% from 2025 to 2033, fueled by rapid expansion of biomanufacturing capabilities, increasing biosimilar development activities, and favorable government policies in countries such as China, India, and South Korea.

- The mammalian cell culture segment led the source segment with a 58% share in 2024, driven by its ability to produce complex proteins with proper folding and post-translational modifications for monoclonal antibodies.

- The recombinant non-glycosylated proteins segment dominated the service segment with a 55.21% revenue share in 2024, due to streamlined production processes, lower manufacturing costs, and broad therapeutic applications including insulin, growth hormones, and cytokines.

- The rheumatoid arthritis segment held the largest revenue share in the therapeutic area category in 2024, driven by the high global prevalence of rheumatoid arthritis and escalating treatment costs of reference biologics such as adalimumab, infliximab, and etanercept.

Report Scope and Biosimilars Manufacturing Market Segmentation

|

Attributes |

Biosimilars Manufacturing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Biosimilars Manufacturing Market Trends

Trend: Technological Advancements in Bioprocessing

Advancements in bioprocessing technologies, including single-use systems, high-throughput cell line development, and process analytical technology (PAT), are revolutionizing biosimilar contract manufacturing. Contract manufacturing organizations are heavily investing in advanced biomanufacturing technologies, including single-use systems, high-capacity bioreactors, and continuous processing, to meet the rising demand for biosimilars. Single-use bioreactors allow flexible and scalable production while minimizing contamination risks and operational costs, enabling CDMOs to quickly adjust production capacities based on market demand. The adoption of continuous bioprocessing is also transforming the industry, allowing for real-time monitoring and reducing production costs compared to traditional batch processing.

For instance, the biopharmaceutical industry is undergoing a fundamental transformation from traditional batch manufacturing to continuous manufacturing for recombinant drugs and biosimilars, driven by regulatory support through ICH Q13 guidance. Continuous manufacturing offers substantial benefits, including a reduced equipment footprint of up to 70%, a 3- to 5-fold increase in volumetric productivity, enhanced product quality consistency, and facility cost reductions of 30–50% compared to traditional batch processes.

Biosimilars Manufacturing Market Dynamics

Key Market Driver: Patent Expirations of Blockbuster Biologics

Patent expirations for blockbuster biologics such as monoclonal antibodies, insulin analogs, and growth factors have created significant opportunities for biosimilar manufacturers. Due to high production complexity, many companies rely on CDMOs with specialized expertise in biologics development, scale-up, and regulatory compliance, accelerating outsourcing partnerships and enabling faster biosimilar launches. Biologics losing patents—including Humira, Eylea, Keytruda, Stelara, Revlimid, and Eliquis expected to lose patents by 2030—are expected to promote biosimilar demand.

For instance, over the next five years, 88 biologics—including blockbuster agents like Eliquis, Keytruda, Opdivo, and Darzalex—are facing loss of exclusivity, representing an estimated market of more than USD 100 billion. Johnson & Johnson's Stelara generated approximately USD 10.4 billion in revenue in 2024.

Key Restraint/Challenge: High Initial Investment and Manufacturing Costs

Biosimilar manufacturing requires significant capital expenditure for specialized facilities, equipment, and skilled personnel. Development costs remain substantially higher than small-molecule generics—approximately USD 250 million compared to USD 2 million for generics. Additionally, maintaining strict quality standards and regulatory compliance adds to operational costs.

For instance, Celltrion announced plans to invest 700 billion won (approximately USD 503 million) for the acquisition of a biopharmaceutical manufacturing facility in the U.S., underscoring the substantial capital requirements for biosimilar manufacturing capacity expansion.

Key Market Opportunity: Expansion in Emerging Markets

Emerging markets, particularly Asia-Pacific, offer significant growth opportunities for biosimilar manufacturing. Rapid expansion of biomanufacturing capabilities in China, India, and South Korea, combined with favorable government policies and lower production costs, is attracting pharmaceutical companies to outsource biosimilar production to these regions. China is expected to grow at 18.7% CAGR and India at 17.3% CAGR.

For instance, China's "Made in China 2025" initiative emphasizes biosimilars as a strategic industry. Germany (15.9%), France (14.6%), and the United Kingdom (13.2%) reinforce Europe's position as a high-quality biomanufacturing cluster, while the United States (11.8%) grows steadily through large-scale commercial manufacturing.

Biosimilars Manufacturing Market Scope

The Biosimilars Manufacturing market is segmented on the basis of source, service, therapeutic area, end use, and region.

- By Source

On the basis of source, the market is segmented into mammalian and non-mammalian. Mammalian cell culture represented the largest source segment, with a share of 58% in 2024, driven by its ability to produce complex proteins with proper folding and post-translational modifications. Mammalian cells offer advantages including proper protein folding, post-translational modifications, and high product yields, making them the preferred choice for biosimilar production. Most biosimilars rely on complex mammalian cell culture systems for production. Non-mammalian sources, including microbial and yeast systems, are also used for producing simpler biologics and are expected to grow steadily.

- By Service

On the basis of service, the market is segmented into process development, analytical & QC studies, manufacturing, and packaging. Process development and manufacturing are the largest service segments, as pharmaceutical companies increasingly outsource these activities to CDMOs with specialized expertise and infrastructure. Analytical & QC studies are critical for ensuring product quality, safety, and comparability with reference biologics. Packaging services are also essential for maintaining product integrity and meeting regulatory requirements.

- By Therapeutic Area

On the basis of therapeutic area, the market is segmented into oncology, blood disorders, autoimmune diseases, and others. The rheumatoid arthritis segment held the largest revenue share in 2024, driven by the high global prevalence of rheumatoid arthritis coupled with escalating treatment costs of reference biologics such as adalimumab, infliximab, and etanercept. Oncology represents a significant segment, driven by the increasing number of biosimilar developments targeting cancer therapies and the patent expirations of blockbuster oncology biologics. Blood disorders and autoimmune diseases are also significant segments, with growing biosimilar pipelines targeting conditions such as psoriasis and inflammatory bowel disease. The oncology segment is expected to grow at the fastest CAGR during the forecast period.

- By End Use

On the basis of end use, the market is segmented into pharmaceutical & biopharmaceutical companies and contract research organizations. Pharmaceutical & biopharmaceutical companies are the largest end users, as these organizations conduct the majority of biosimilar development and require comprehensive manufacturing services to support their product pipelines. A significant number of small- and medium-sized biopharmaceutical companies lack infrastructure for manufacturing biosimilars. Furthermore, big pharmaceutical companies try to focus on their core competencies, such as research and marketing, owing to which they outsource manufacturing services. Contract research organizations are also significant end users, as they manage biosimilar development on behalf of pharmaceutical sponsors and require specialized manufacturing capabilities.

Biosimilars Manufacturing Market Regional Analysis

North America Biosimilars Manufacturing Market Insight

North America held the largest revenue share of the biosimilars manufacturing market in 2025, accounting for approximately 37% of the global market. The region's dominance is supported by a strong biopharmaceutical ecosystem, advanced manufacturing infrastructure, and robust regulatory support for biosimilars. The U.S. biosimilar contract manufacturing market generated a revenue of USD 2,054.7 million in 2024 and is expected to reach USD 6,769.9 million by 2033, growing at a CAGR of 14.2%. The U.S. accounted for 26.2% of the global biosimilar contract manufacturing market in 2024. The FDA's streamlined approval pathways for biosimilars, which have approved over 80 biosimilars as of 2026, have encouraged investment in biosimilar development, driving demand for high-quality manufacturing partners.

Europe Biosimilars Manufacturing Market Insight

Europe represents a significant market for biosimilars manufacturing, supported by strong pharmaceutical research, advanced healthcare infrastructure, and stringent regulatory frameworks. The European Medicines Agency has established comprehensive guidelines for biosimilar development and approval, fostering a favorable environment for biosimilar manufacturing. Countries such as Germany, Switzerland, the U.K., and France are major contributors to the European market, with well-established biopharmaceutical industries and CDMO networks. The region's focus on regulatory compliance and quality standards drives demand for specialized manufacturing services.

Asia-Pacific Biosimilars Manufacturing Market Insight

Asia-Pacific is expected to witness the fastest growth during the forecast period, with a projected CAGR of 14.5% from 2025 to 2033. The region generated a revenue of USD 2,242.1 million in 2024 and is expected to reach USD 7,572.0 million by 2033. The region accounted for 28.6% of the global biosimilar contract manufacturing market in 2024. Growth is driven by rapid expansion of biomanufacturing capabilities, increasing biosimilar development activities, and favorable government policies in countries such as China, India, and South Korea. China (18.7% CAGR) and India (17.3% CAGR) are emerging as dominant manufacturing hubs due to cost competitiveness, expanding biopharma infrastructure, and favorable regulatory reforms. Major market participants actively operating in the Asia-Pacific region include Samsung Biologics, WuXi Biologics, Biocon, and Boehringer Ingelheim BioXcellence.

Middle East & Africa Biosimilars Manufacturing Market Insight

The Middle East and Africa region represents an emerging market for biosimilars manufacturing, with demand primarily concentrated in the Gulf Cooperation Council countries and South Africa. The MEA biosimilar contract manufacturing market is expected to reach a projected revenue of US$ 585.2 million by 2033, growing at a CAGR of 14% from 2025 to 2033. Governments across the region are increasing investments in healthcare infrastructure and research capabilities to diversify their economies and improve healthcare access. The region offers advantages such as growing pharmaceutical markets and increasing biosimilar adoption, but limited manufacturing infrastructure and regulatory complexity continue to restrain market growth.

South America Biosimilars Manufacturing Market Insight

South America represents an emerging market for biosimilars manufacturing, with growing demand influenced by increasing healthcare investments, expanding pharmaceutical markets, and rising biosimilar adoption. Brazil dominates the South American market, driven by the country's large economy, growing healthcare sector, and increasing government focus on expanding access to affordable biologic therapies. However, market growth is currently constrained by limited manufacturing infrastructure and economic volatility compared to more developed regions.

Biosimilars Manufacturing Market Share

The biosimilars manufacturing industry is primarily led by well-established companies, including:

- Boehringer Ingelheim Biopharmaceuticals GmbH (Germany)

- Lonza Group Ltd (Switzerland)

- Catalent, Inc. (U.S.)

- Samsung Biologics Co., Ltd. (South Korea)

- WuXi Biologics (Cayman) Inc. (China)

- Biocon Limited (India)

- Thermo Fisher Scientific Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Merck KGaA, Darmstadt, Germany (Germany)

- AbbVie Inc. (U.S.)

- FUJIFILM Diosynth Biotechnologies (U.S.)

- AGC Biologics, Inc. (U.S.)

- Polpharma Biologics S.A. (Poland)

- Siegfried Holding AG (Switzerland)

- Eurofins Scientific SE (Luxembourg)

- OneSource Specialty Pharma Limited (India)

- Xbrane Biopharma AB (publ) (Sweden)

- Rezon Bio (Poland)

- Enzene Biosciences Limited (India)

- Tanvex BioPharma, Inc. (Taiwan)

- EirGenix, Inc. (Taiwan)

Latest Developments in Biosimilars Manufacturing Market

- In November 2025, Polpharma Biologics announced its demerger into two independent companies, including a biosimilars business that will keep the original brand name and be operated from Switzerland, and a new CDMO offering end-to-end services from cell line development through to GMP manufacturing and commercial supply.

- In September 2025, Rezon Bio launched as a European CDMO for biologics, establishing itself as a new player in the European biologics manufacturing landscape with two state-of-the-art facilities in Gdańsk and Duchnice-Warsaw, Poland, offering end-to-end services from cell line development through GMP manufacturing and commercial supply.

- In July 2025, Celltrion, Inc. was selected as the preferred bidder to acquire a biopharmaceutical manufacturing facility in the U.S., with plans to invest 700 billion won (approximately $503 million) for the acquisition. The company aims to mitigate potential tariff risks and secure a local manufacturing base for its flagship biosimilars.

- In June 2025, OneSource Specialty Pharma and Xbrane Biopharma announced a partnership focused on the commercial manufacturing of Xbrane's biosimilar portfolio for global markets. As part of the agreement, Xbrane will transfer its select product(s) to OneSource's integrated drug substance and drug product facility in Bengaluru, India.

- In May 2025, FAMAR Group signed an agreement to acquire a sterile manufacturing site in Homburg, Germany, from MiP Pharma, expanding its presence in the European biologics and biosimilars manufacturing market. The acquisition strengthens FAMAR's footprint in high-value dosage forms and expands its capabilities in aseptic and lyophilized fill & finish.

- In 2024, Samsung Biologics announced two manufacturing deals with Pfizer worth a combined $897 million, bringing the year's total orders from Pfizer to $1.08 billion. Samsung Biologics provides additional capacity to support Pfizer's multi-product biosimilar portfolio, including treatments for oncology, inflammation, and immunology.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.