Global Bladder Disorders Market

Market Size in USD Billion

USD

16.16 Billion

USD

38.32 Billion

2025

2033

USD

16.16 Billion

USD

38.32 Billion

2025

2033

| 2026 - 2033 | |

| USD 16.16 Billion | |

| USD 38.32 Billion | |

| % | |

|

Bladder Disorders Market Size

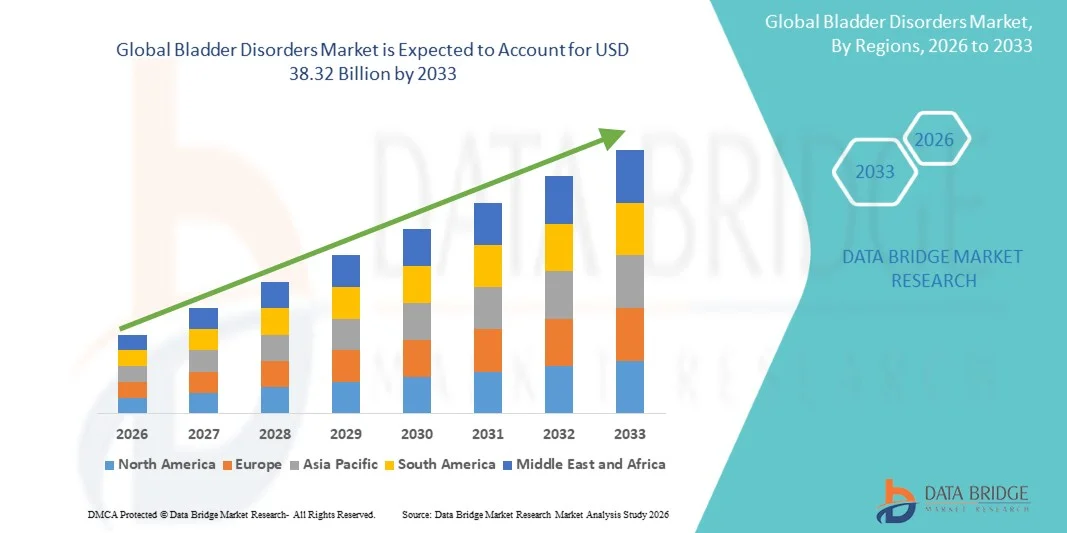

- The global bladder disorders market size was valued at USD 16.16 billion in 2025 and is expected to reach USD 38.32 billion by 2033, at a CAGR of 11.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of bladder-related conditions such as urinary incontinence, overactive bladder, and interstitial cystitis, along with rising awareness regarding urological health, leading to higher demand for effective diagnosis and treatment solutions

- Furthermore, growing adoption of advanced therapeutics, minimally invasive treatment options, and increasing focus on improving patient quality of life are establishing bladder disorder treatments as an essential component of modern healthcare. These converging factors are accelerating the uptake of bladder disorder solutions, thereby significantly boosting the market’s growth

Bladder Disorders Market Analysis

- Bladder disorder treatments, including pharmacological therapies, minimally invasive procedures, and diagnostic solutions, are increasingly important in modern healthcare due to their role in managing conditions such as overactive bladder, urinary incontinence, and interstitial cystitis, thereby improving patient quality of life

- The escalating demand for bladder disorder solutions is primarily driven by the rising geriatric population, increasing prevalence of urological conditions, and growing awareness regarding early diagnosis and treatment

- North America dominated the bladder disorders market with the largest revenue share of approximately 38.6% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates, and strong presence of key pharmaceutical and medical device companies

- Asia-Pacific is expected to be the fastest-growing region in the bladder disorders market during the forecast period, with a projected CAGR of 8.5%, driven by increasing healthcare expenditure, growing patient awareness, and improving access to urological care

- The medication segment dominated the market with a revenue share of approximately 41.5% in 2025, driven by the high adoption of antimuscarinic drugs, beta-3 agonists, and antibiotics for urinary infections

Report Scope and Bladder Disorders Market Segmentation

|

Attributes |

Bladder Disorders Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Pfizer (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Bladder Disorders Market Trends

“Growing Need Due to Rising Prevalence and Increasing Awareness”

- The rising prevalence of bladder disorders, including urinary incontinence, overactive bladder, and interstitial cystitis, is a key driver for market growth. Increasing awareness among patients and healthcare professionals about early diagnosis and effective management is propelling demand for innovative treatments and diagnostic solutions

- For instance, in March 2025, Astellas Pharma launched a new formulation for overactive bladder management in Europe, aiming to improve patient compliance and therapeutic outcomes. Such initiatives by leading pharmaceutical companies are expected to boost the Bladder Disorders market during the forecast period

- The increasing geriatric population, who are more prone to urinary and bladder-related conditions, is further contributing to the market expansion

- Rising female patient population awareness regarding conditions such as stress urinary incontinence is leading to higher adoption of medical interventions. Furthermore, the availability of minimally invasive procedures and advanced therapies is encouraging patients to seek timely treatment

- The growing focus of healthcare providers and governments on improving patient quality of life, alongside educational campaigns highlighting early detection and treatment, is also supporting market growth

- In addition, insurance coverage and reimbursement policies for bladder disorder treatments in developed regions are facilitating wider access to therapies. The expansion of outpatient clinics, urology centers, and specialized healthcare facilities is increasing the reach of diagnosis and treatment options

- Increasing investments in research and development by pharmaceutical companies to introduce novel drugs, devices, and therapies are strengthening the market pipeline

- Telemedicine and remote patient monitoring platforms are also enabling better management of bladder disorders, particularly in regions with limited healthcare access. Combined, these factors are driving heightened demand for effective management and treatment solutions, thereby boosting overall market growth.

Bladder Disorders Market Dynamics

Driver

“Rising Adoption of Advanced Therapeutics and Personalized Care”

- There is a growing trend toward personalized medicine and tailored treatment approaches for bladder disorders, enabling better patient outcomes. Advances in drug formulations, combination therapies, and minimally invasive procedures are transforming standard care protocols

- For instance, neuromodulation devices for overactive bladder are increasingly being tailored to individual patient needs, demonstrating a shift toward personalized, non-pharmacological interventions

- Telehealth and remote monitoring solutions are increasingly being used to track patient progress, provide adherence reminders, and facilitate consultations, particularly for chronic bladder conditions

- Integration of innovative medical devices, such as neuromodulation systems for overactive bladder, is becoming more prevalent, offering non-pharmacological alternatives to patients

- Digital platforms and patient-centric apps are supporting self-management strategies, symptom tracking, and timely intervention, improving long-term treatment adherence

- Collaborations between pharmaceutical companies, research institutions, and healthcare providers are accelerating the development of next-generation therapies

- The increasing focus on quality-of-life outcomes, reduced hospital stays, and minimally invasive interventions is shaping treatment protocols

- Emerging markets are witnessing higher adoption rates due to rising healthcare infrastructure, patient awareness campaigns, and improved access to urology specialists

- Regulatory support for innovative therapies and fast-track approvals in certain regions is fostering the introduction of new treatment options

- Preventive strategies, such as early screening and awareness programs for at-risk populations, are gaining traction

- Overall, the trend toward personalized, technology-enabled, and patient-focused care is expected to drive sustained growth in the Bladder Disorders market over the forecast period

Restraint/Challenge

“Side Effects, High Costs, and Limited Patient Awareness”

- Adverse effects associated with certain bladder disorder therapies, such as anticholinergics or botulinum toxin injections, may limit patient adoption and impede market growth. For instance, reported side effects like dry mouth, urinary retention, or localized pain can discourage continued treatment

- For instance, patients receiving botulinum toxin injections for overactive bladder have reported side effects like urinary retention and localized pain, which may reduce adherence to treatment regimens

- The relatively high cost of advanced therapies, novel pharmacological formulations, and minimally invasive procedures remains a barrier, particularly in developing countries or among price-sensitive patient populations. Patients in regions with limited healthcare coverage may face challenges accessing optimal treatment options

- Limited patient awareness regarding bladder disorders, especially among older adults and rural populations, can delay diagnosis and therapy initiation. Healthcare professionals’ limited focus on early screening in some regions further exacerbates underdiagnosis

- Stringent regulatory approval processes for new drugs and devices can delay product launches and slow market expansion. In addition, competition from generic medications and traditional treatments may restrict adoption of newer, more advanced therapies

- Challenges in patient adherence to long-term treatment regimens, including lifestyle interventions, pharmacotherapy, or device usage, can reduce overall market growth potential. Supply chain constraints and access issues in certain emerging markets may also impact the availability of treatments

- Overcoming these challenges through patient education, affordable treatment options, awareness campaigns, and streamlined regulatory approvals is essential for sustained growth in the Bladder Disorders market

Bladder Disorders Market Scope

The market is segmented on the basis of type, treatment type, end user, and distribution channel.

• By Type

On the basis of type, the Bladder Disorders market is segmented into cystitis, urinary incontinence, overactive bladder, interstitial cystitis, and bladder cancer. The urinary incontinence segment dominated the largest market revenue share of approximately 38.7% in 2025, driven by its high prevalence among aging populations and women post-pregnancy. Rising awareness about available treatments, increasing healthcare accessibility, and social initiatives reducing stigma around incontinence contribute to strong adoption. The segment also benefits from advanced diagnostic tools, patient education programs, and continuous innovation in therapeutic devices. Growing geriatric populations in North America, Europe, and Asia-Pacific further reinforce demand. Technological advancements in non-invasive treatments, wearable monitoring devices, and minimally invasive surgical options are supporting market growth. Moreover, insurance coverage and government programs in developed economies are increasing affordability. Rising prevalence of lifestyle-related bladder conditions, increasing clinical research, and better healthcare infrastructure in emerging economies are also key factors.

The overactive bladder segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, fueled by increasing recognition of the condition and growing use of pharmacological and non-surgical therapies. The rising incidence of diabetes and neurological disorders, which can lead to overactive bladder, is expanding the patient pool. Introduction of newer medications with improved efficacy and safety profiles, along with minimally invasive neuromodulation therapies, is driving adoption. In addition, awareness campaigns by professional associations and patient support groups are encouraging early diagnosis and treatment. Rising demand in emerging regions due to urbanization and lifestyle changes is further accelerating growth. Telemedicine and remote patient monitoring for bladder health also contribute to convenience and market expansion.

• By Treatment Type

On the basis of treatment type, the market is segmented into surgery, medication, and non-surgical therapies. The medication segment dominated the market with a revenue share of approximately 41.5% in 2025, driven by the high adoption of antimuscarinic drugs, beta-3 agonists, and antibiotics for urinary infections. Medication offers non-invasive, cost-effective, and accessible options for patients across age groups. Strong R&D pipelines, generic drug availability, and government reimbursement programs support segment growth. Growing patient preference for home-based and outpatient treatments is also boosting adoption. Pharmaceutical innovations targeting symptom relief and reduced side effects further strengthen this segment. Increasing awareness about self-managed treatments, adherence programs, and the availability of combination therapies contribute to market leadership.

The non-surgical therapies segment is projected to grow at the fastest CAGR of 8.3% from 2026 to 2033, driven by rising preference for minimally invasive options such as neuromodulation, pelvic floor therapy, and bladder training exercises. Increasing geriatric populations, rising awareness of lifestyle management approaches, and technological advances in therapeutic devices are supporting adoption. The growing market for wearable and remote monitoring solutions also enhances convenience. In addition, integration with digital health platforms and telemedicine services accelerates the uptake of non-surgical approaches.

• By End User

On the basis of end user, the Bladder Disorders market is segmented into hospitals, clinics, ambulatory surgery centers, and others. The hospitals segment held the largest market revenue share of approximately 46.3% in 2025, due to the availability of advanced diagnostic and treatment infrastructure, skilled urologists, and comprehensive care facilities. Hospitals handle a high volume of patients requiring both surgical and non-surgical interventions, ensuring broad market coverage. Increasing hospital expansions, investments in urology departments, and integration of advanced technologies such as robotic surgery and imaging devices strengthen the segment. Furthermore, insurance coverage and established referral networks improve accessibility and adoption.

The ambulatory surgery centers segment is expected to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by the growing preference for outpatient procedures that reduce hospital stays and costs. These centers offer minimally invasive surgeries, catheterizations, and bladder training programs with shorter recovery times. Rising demand for convenient, cost-effective, and high-quality urological care in both urban and semi-urban regions supports growth. Enhanced patient awareness, increasing adoption of minimally invasive procedures, and technological advancements in surgical devices are key drivers. The rise of telehealth services for pre- and post-operative monitoring further facilitates market expansion.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into direct and retail channels. The direct segment dominated the market in 2025 with a revenue share of approximately 52%, driven by strong partnerships with hospitals, clinics, and ambulatory surgery centers. Direct distribution allows healthcare institutions to receive devices, medications, and treatment kits in a timely manner, ensuring uninterrupted patient care. Hospitals and clinics often prefer direct procurement due to bulk order advantages, personalized service, and faster delivery timelines. The segment benefits from dedicated after-sales support, installation services for devices, and training programs for medical staff. Strong relationships with key urology specialists, hospitals, and research institutions reinforce loyalty. Direct distribution also facilitates clinical trial collaborations and adoption of new therapies. In addition, contracts and long-term supply agreements with government hospitals enhance revenue stability. The availability of complete product portfolios through direct channels increases trust and encourages repeat procurement. Institutional buying behavior and centralized procurement policies further strengthen the segment’s dominance.

The retail segment is projected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by growing patient preference for convenient pharmacy-based purchases of medications, home-care kits, and supportive devices. Expansion of community pharmacies, increasing penetration of online pharmacies, and rising e-commerce adoption contribute significantly to retail growth. Patients are increasingly seeking over-the-counter solutions for minor bladder issues, non-invasive therapies, and self-management tools, which boosts retail demand. Government initiatives to improve access to medications in emerging regions further accelerate growth. Retail channels also benefit from promotional campaigns, patient awareness programs, and convenient home delivery options. Rising disposable incomes, urbanization, and consumer inclination toward self-care products drive adoption. In addition, partnerships between pharmaceutical manufacturers and retail chains enhance product visibility. Convenience, accessibility, and awareness campaigns combine to make retail the fastest-growing distribution channel.

Bladder Disorders Market Regional Analysis

- North America dominated the bladder disorders market with the largest revenue share of approximately 38.6% in 2025

- Supported by advanced healthcare infrastructure, high diagnosis rates, and strong presence of key pharmaceutical and medical device companies

- The U.S., in particular, accounts for the majority of this market share due to widespread availability of specialized urological care, advanced diagnostic facilities, and high patient awareness regarding bladder-related conditions

U.S. Bladder Disorders Market Insight

The U.S. bladder disorders market captured the largest revenue share within North America, fueled by increasing prevalence of urinary incontinence, overactive bladder, and other urological disorders. For instance, Pfizer’s introduction of a new overactive bladder drug in 2025 improved treatment accessibility and patient compliance, highlighting the active role of pharmaceutical innovation in the region. Strong reimbursement policies, well-established healthcare networks, and rising patient awareness regarding early diagnosis further propel the market growth.

Europe Bladder Disorders Market Insight

The Europe bladder disorders market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare investments, stringent clinical guidelines for urological health, and rising awareness regarding bladder disorders. Countries such as France and Italy are witnessing growing adoption of advanced diagnostics and therapies across hospitals and specialty clinics. The presence of well-established healthcare systems and increasing focus on improving patient outcomes are contributing to market expansion across European countries.

U.K. Bladder Disorders Market Insight

The U.K. bladder disorders market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising number of urological procedures and strong emphasis on patient awareness and preventive care. For instance, the NHS introduced awareness campaigns on urinary incontinence in 2025, which increased patient consultations and early diagnosis rates. Increasing adoption of advanced diagnostic tools and government initiatives aimed at improving healthcare services are supporting market growth in the U.K.

Germany Bladder Disorders Market Insight

The Germany bladder disorders market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, high healthcare expenditure, and focus on technological innovation in urological treatments. For example, Charité – Universitätsmedizin Berlin implemented new minimally invasive procedures for overactive bladder patients in 2025, demonstrating the country’s emphasis on advanced care. Germany’s well-established hospital network and increasing adoption of cutting-edge therapies are driving market growth.

Asia-Pacific Bladder Disorders Market Insight

The Asia-Pacific bladder disorders market is expected to grow at the fastest CAGR of 8.5% during the forecast period, driven by increasing healthcare expenditure, growing patient awareness, and improving access to urological care in countries such as China, India, and Japan. The region’s expanding middle-class population and rising prevalence of bladder-related disorders are accelerating demand for diagnostics and therapies.

Japan Bladder Disorders Market Insight

The Japan bladder disorders market is gaining momentum due to the country’s high healthcare standards, increasing geriatric population, and demand for advanced medical solutions. For instance, Japan introduced reimbursement coverage for novel overactive bladder treatments in 2025, which improved accessibility and adoption among patients. Integration of innovative therapies with standard clinical practice is fueling market growth.

China Bladder Disorders Market Insight

The China bladder disorders market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, and high rates of technological adoption in healthcare. For example, Shanghai Ruijin Hospital launched specialized urology clinics offering advanced bladder diagnostics in 2025, driving awareness and adoption of treatments. The push towards improving healthcare access, coupled with strong domestic pharmaceutical and device manufacturing, is propelling market growth in China.

Bladder Disorders Market Share

The Bladder Disorders industry is primarily led by well-established companies, including:

• Pfizer (U.S.)

• AbbVie (U.S.)

• Astellas Pharma (Japan)

• Ferring Pharmaceuticals (Switzerland)

• Johnson & Johnson (U.S.)

• Medtronic (Ireland)

• Boston Scientific (U.S.)

• GlaxoSmithKline (U.K.)

• Bayer AG (Germany)

• Eli Lilly (U.S.)

• Ipsen (France)

• Recordati (Italy)

• Urovant Sciences (U.S.)

• Coloplast (Denmark)

• Novartis (Switzerland)

• Retrophin (U.S.)

• Theramex (U.K.)

• Pfizer Consumer Healthcare (U.S.)

• Holista Biotech (Australia)

• Sanofi (France)

Latest Developments in Global Bladder Disorders Market

- In April 2024, Glycologix, Inc. announced that results from its Phase 1b trial of GLX‑100 in Interstitial Cystitis/Bladder Pain Syndrome would be presented at the 2025 American Urological Association (AUA) Annual Meeting, underscoring advances in biologic and soft‑tissue targeted therapies in chronic bladder disorder care

- In June 2025, the U.S. Food and Drug Administration approved Zusduri, a gel‑based chemotherapy treatment developed by UroGen Pharma for non‑muscle invasive bladder cancer that has not spread beyond the inner bladder layer, offering patients a non‑surgical intravesical therapy option that significantly reduces tumor recurrence and can be administered in outpatient settings

- In September 2025, top clinical data presented at the European Society for Medical Oncology (ESMO) conference showed that a combination of Padcev (Pfizer/Astellas antibody‑drug conjugate) and Keytruda (Merck immunotherapy) significantly improved survival outcomes—cutting recurrence, progression, or death risk by ~60% in patients with muscle‑invasive bladder cancer unable to undergo standard chemotherapy, representing a major oncology breakthrough in bladder cancer therapy combinations

- In June 2025, Neuspera Medical, Inc. received FDA approval for its integrated sacral neuromodulation (iSNM) system, a neuromodulation device that treats urinary urge incontinence (UUI), a key symptom of overactive bladder (OAB), providing a less‑invasive alternative to traditional neuromodulation therapies and expanding the device‑based therapeutic landscape for bladder disorders

- In July 2025, Eisai Co., Ltd. launched Beova® Tablets, a once‑daily selective β3‑adrenergic receptor agonist designed to relax bladder muscle and alleviate urgency and incontinence symptoms, broadening oral pharmacological treatment options in the overactive bladder segment

- In June 2025, Marksans Pharma Ltd. announced that its UK subsidiary Relonchem Ltd. received **marketing authorization from the Medicines and Healthcare Products Regulatory Agency for its Oxybutynin hydrochloride oral solution, strengthening the availability of established bladder disorder therapies in the UK market

- In April 2025, Amara Therapeutics, an Ireland‑based medical technology company focused on women’s health, announced the initiation of a clinical trial for a digital therapeutic approach targeting overactive bladder in women, signaling an emerging focus on digital health integration for bladder disorder management

- In March 2025, Imbrium Therapeutics (a subsidiary of Purdue Pharma) completed the final patient visit in its Phase 1b clinical trial of sunobinop (V117957)—an investigational oral therapy for interstitial cystitis/bladder pain syndrome (IC/BPS)—advancing a potential new non‑opioid oral option for chronic bladder pain, which remains a major unmet need in bladder disorder therapeutics

- In March 2025, Hyloris reported a positive interim outcome in its ALENURA clinical trial (IC/BPS) with an Independent Data Monitoring Committee recommendation to continue the study, representing progress toward first‑line medical therapy for interstitial cystitis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.