Global Blind Loop Syndrome Market

Market Size in USD Million

USD

250.50 Million

USD

367.29 Million

2024

2032

USD

250.50 Million

USD

367.29 Million

2024

2032

| 2025 - 2032 | |

| USD 250.50 Million | |

| USD 367.29 Million | |

| % | |

|

Blind Loop Syndrome Market Size

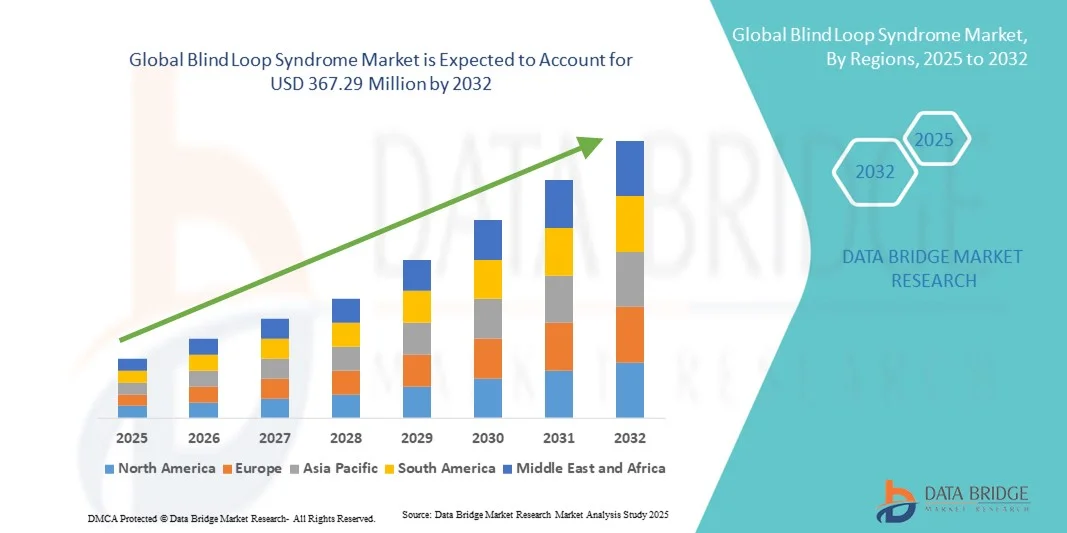

- The global blind loop syndrome market size was valued at USD 250.50 Million in 2024 and is expected to reach USD 367.29 Million by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by increasing awareness of gastrointestinal disorders and advancements in diagnostic techniques and treatment options, leading to improved detection and management of blind loop syndrome in clinical settings

- Furthermore, rising patient demand for effective, safe, and accessible treatment solutions—ranging from pharmacological interventions to minimally invasive procedures—is establishing innovative blind loop syndrome therapies as the preferred choice for clinicians. These converging factors are accelerating the uptake of blind loop syndrome solutions, thereby significantly boosting the industry's growth

Blind Loop Syndrome Market Analysis

- Blind Loop Syndrome, encompassing therapeutic and diagnostic approaches for managing abnormal intestinal bacterial overgrowth, is increasingly vital due to its potential to improve digestion, nutrient absorption, and patient quality of life. Treatments include medical therapies, dietary interventions, and surgical procedures targeting the root causes of bacterial overgrowth and intestinal dysmotility

- The escalating demand for blind loop syndrome treatments is primarily fueled by growing awareness among healthcare providers, rising prevalence of gastrointestinal disorders, and advancements in diagnostic technologies facilitating early detection and intervention

- North America dominated the blind loop syndrome market with the largest revenue share of 39.8% in 2024, characterized by advanced healthcare infrastructure, high healthcare spending, and the presence of key hospitals and research centers specializing in gastrointestinal disorders. The U.S. experienced substantial growth in Blind Loop Syndrome treatment adoption, particularly in urban healthcare facilities, driven by innovations from established pharmaceutical companies and medical technology startups focusing on diagnostic tools and minimally invasive therapies

- Asia-Pacific is expected to be the fastest growing region in the blind loop syndrome market during the forecast period due to increasing healthcare awareness, rising disposable incomes, expanding hospital networks, and growing access to specialized gastroenterology clinics in countries such as India, China, and Japan

- The oral route dominated the blind loop syndrome market with the largest revenue share of 46.7% in 2024, supported by patient preference for convenience and non-invasiveness

Report Scope and Blind Loop Syndrome Market Segmentation

|

Attributes |

Blind Loop Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Blind Loop Syndrome Market Trends

Rising Adoption of Advanced Diagnostic and Minimally Invasive Techniques

- A significant and accelerating trend in the global blind loop syndrome market is the growing adoption of advanced diagnostic techniques and minimally invasive interventions, improving both detection accuracy and patient outcomes

- For instance, capsule endoscopy by Medtronic, widely used in hospitals across the U.S. and Europe, allows for detailed visualization of the small intestine, facilitating early and accurate diagnosis of Blind Loop Syndrome. Similarly, Olympus’ EVIS X1 high-definition endoscopy system is being adopted in Japan and Germany, enhancing the detection of postoperative complications

- Minimally invasive surgical techniques, such as laparoscopic resection and robotic-assisted procedures, are gaining prominence for corrective treatment of blind loops. For instance, Johnson & Johnson’s Ethicon laparoscopic instruments are utilized in leading gastroenterology centers in Europe to reduce recovery times and surgical risks

- The integration of supportive therapies, including targeted nutritional plans and probiotics, is being increasingly incorporated in patient management. For instance, a clinical study at the University of California, San Francisco, demonstrated improved gut microbiota balance and symptom management in post-surgical patients treated with Lactobacillus rhamnosus

- This trend toward earlier diagnosis, precise treatment, and holistic patient care is fundamentally reshaping expectations among gastroenterologists and patients for effective management of Blind Loop Syndrome. Consequently, hospitals and specialized gastroenterology centers are expanding diagnostic services and adopting cutting-edge surgical tools

- The demand for comprehensive treatment solutions is growing rapidly across both developed and emerging markets, driven by increasing awareness, rising prevalence of postoperative complications, and expanding access to advanced healthcare facilities

Blind Loop Syndrome Market Dynamics

Driver

Increasing Awareness and Adoption of Advanced Diagnostic Procedures

- The rising prevalence of gastrointestinal disorders and growing awareness about rare post-surgical complications are key drivers of market growth

- For instance, the American Gastroenterological Association (AGA) launched educational programs in 2022 to increase awareness of postoperative intestinal conditions like Blind Loop Syndrome, leading to higher rates of early screening and diagnosis

- Innovations in imaging and diagnostic technologies are boosting adoption. For example, Olympus’ high-definition endoscopy systems introduced in 2023 provide detailed visualization of blind loops, improving diagnostic confidence and treatment planning

- The expansion of specialized gastroenterology and trichology clinics is improving patient access to comprehensive care. For instance, Mayo Clinic expanded its multidisciplinary gastrointestinal disorder program in 2021, offering coordinated evaluation and management for Blind Loop Syndrome patients

- Personalized medicine approaches are increasingly integrated. For instance, Cleveland Clinic initiated a post-operative monitoring program in 2022 that uses microbiome profiling to tailor nutritional and therapeutic interventions for each patient

Restraint/Challenge

Limited Awareness, Diagnostic Complexity, and High Treatment Costs

- Limited awareness of Blind Loop Syndrome among general practitioners and patients can lead to delayed diagnosis and treatment. For instance, a 2021 study in the Journal of Gastrointestinal Surgery reported that over 30% of cases were initially misdiagnosed as IBS or Crohn’s disease

- High costs of advanced diagnostic tools and surgical procedures restrict market accessibility

- For instance, capsule endoscopy procedures in the U.S. range from USD 1,500 to USD 3,000, limiting use among patients without sufficient insurance coverage

- Standardized treatment protocols are limited, slowing the development of new therapies. For instance, few pharmaceutical companies have invested in clinical trials targeting rare postoperative complications like Blind Loop Syndrome

- Patient adherence to long-term treatment plans remains a challenge. For example, Johns Hopkins Hospital reported in 2022 that approximately 20% of patients discontinued post-operative nutritional and therapeutic regimens

- Overcoming these challenges will require increased physician training, patient education, and the development of cost-effective diagnostic and therapeutic solutions to improve access and outcomes for Blind Loop Syndrome patients

Blind Loop Syndrome Market Scope

The market is segmented on the basis of drug class, treatment, route of administration, and end-users.

- By Drug Class

On the basis of drug class, the blind loop syndrome market is segmented into tetracycline, chlortetracycline, oxytetracycline, chloramphenicol, and other antibiotics. The tetracycline segment dominated the largest market revenue share of 36.5% in 2024, driven by its widespread use as a first-line antibiotic for bacterial overgrowth associated with Blind Loop Syndrome. Its effectiveness in inhibiting bacterial proliferation, broad clinical acceptance, and relatively affordable pricing has ensured consistent usage across hospitals and clinics. Physicians often prefer tetracycline due to its proven efficacy and availability in oral formulations, making it suitable for both acute and long-term management. Furthermore, its well-documented safety profile and adaptability in treatment regimens continue to strengthen its dominant position in the market.

The oxytetracycline segment is anticipated to witness the fastest CAGR of 7.8% from 2025 to 2032, fueled by growing adoption in regions where newer-generation antibiotics are either cost-prohibitive or less available. Its effectiveness in addressing secondary complications of Blind Loop Syndrome, along with emerging clinical data supporting its use, has improved its uptake. In addition, oxytetracycline benefits from availability in multiple formulations, enhancing accessibility for patients. Rising awareness campaigns in developing countries, paired with government initiatives to ensure affordable antibiotics, are expected to accelerate this growth.

- By Treatment

On the basis of treatment, the blind loop syndrome market is segmented into medication, surgery, and others.The medication segment dominated the market with a share of 58.9% in 2024, primarily because antibiotics and supportive drug therapy remain the cornerstone of treatment. Patients and clinicians prefer medical management owing to its non-invasive nature, lower costs compared to surgery, and immediate symptom relief. Antibiotic regimens targeting bacterial overgrowth are well-established, and the continuous introduction of improved antibiotic combinations has further strengthened the dominance of this segment. Increased prescription trends, particularly among hospitals and specialty clinics, ensure the medication category continues to lead.

The surgery segment is projected to record the fastest CAGR of 8.6% during 2025–2032, as severe or refractory cases of Blind Loop Syndrome increasingly require surgical correction. Advances in minimally invasive surgical techniques, shorter recovery times, and better success rates have made surgery a more acceptable option. Surgeons and gastroenterologists are recommending surgical interventions earlier in the disease course for selected patients, leading to higher adoption. Moreover, advancements in hospital infrastructure in emerging economies and improved insurance coverage for gastrointestinal surgeries are boosting this segment’s rapid growth.

- By Route of Administration

On the basis of route of administration, the blind loop syndrome market is segmented into injectable, oral, and parenteral. The oral route dominated the market with the largest revenue share of 46.7% in 2024, supported by patient preference for convenience and non-invasiveness. Most antibiotics used in Blind Loop Syndrome, including tetracycline and chloramphenicol, are widely available in oral formulations, making treatment accessible and easy to administer. Compliance rates are generally higher with oral routes, particularly in outpatient and homecare settings. Pharmaceutical companies also continue to prioritize oral dosage forms due to scalability, affordability, and long-term patient acceptance.

The injectable segment is projected to witness the fastest CAGR of 9.2% from 2025 to 2032, as severe infections and hospitalized cases of Blind Loop Syndrome require rapid and effective drug delivery. Intravenous formulations are particularly crucial for patients unable to tolerate oral medication due to gastrointestinal complications. Rising investments in hospital pharmacy infrastructure, coupled with advancements in injectable drug delivery systems, are expected to sustain the growth of this segment. In addition, healthcare professionals often prefer injectables in acute cases due to their faster onset of action and controlled dosing.

- By End-Users

On the basis of end-users, the blind loop syndrome market is segmented into hospitals, homecare, specialty clinics, oncologist, immunologist, and others. The hospitals segment accounted for the largest share of 41.3% in 2024, driven by the availability of comprehensive diagnostic and treatment facilities. Hospitals remain the primary centers for antibiotic therapy initiation, surgical interventions, and follow-up care. The presence of multidisciplinary teams including gastroenterologists, immunologists, and surgeons ensures holistic management, which strengthens hospitals’ dominance in the market. In addition, higher patient inflow, access to advanced technologies, and better reimbursement structures further consolidate their leading role.

The specialty clinics segment is expected to witness the fastest CAGR of 8.9% from 2025 to 2032, propelled by the rising preference for personalized and outpatient-based care. Specialty gastroenterology and immunology clinics are increasingly adopting advanced diagnostic tools and providing targeted treatment regimens for Blind Loop Syndrome. Their ability to offer quicker consultations, specialized expertise, and lower costs compared to hospitals is driving their popularity. Furthermore, growing investments in standalone specialty healthcare centers across urban and semi-urban regions support their rapid growth trajectory.

Blind Loop Syndrome Market Regional Analysis

- North America dominated the blind loop syndrome market with the largest revenue share of 39.8% in 2024, characterized by advanced healthcare infrastructure, high healthcare spending, and the presence of key hospitals and research centers specializing in gastrointestinal disorders

- The region’s strong focus on early diagnosis, access to minimally invasive treatments, and robust clinical trial networks is driving market growth

- The widespread adoption of modern diagnostic techniques, such as capsule endoscopy and high-definition imaging, along with targeted post-surgical therapies, is further enhancing patient outcomes and reinforcing North America’s leadership in the Blind Loop Syndrome market.

U.S. Blind Loop Syndrome Market Insight

The U.S. blind loop syndrome market captured the largest revenue share of 81% in 2024 within North America, fueled by substantial growth in urban healthcare facilities with better access to specialized gastroenterology clinics. Patients are increasingly seeking advanced diagnostic procedures, including imaging technologies and microbiome profiling, for early detection and effective management of postoperative complications. Moreover, innovations from established pharmaceutical companies and medical technology startups focusing on minimally invasive therapies are significantly contributing to the market’s expansion.

Europe Blind Loop Syndrome Market Insight

The Europe blind loop syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of gastrointestinal disorders, increasing investments in healthcare infrastructure, and government initiatives supporting early diagnosis of post-surgical complications. Hospitals and specialized gastroenterology centers in Germany, France, and Italy are adopting advanced endoscopic techniques and postoperative monitoring programs, fostering better patient outcomes.

U.K. Blind Loop Syndrome Market Insight

The U.K. blind loop syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing healthcare awareness and the growing focus on gastrointestinal disorder management. In addition, expansion of specialized clinics and research programs for rare postoperative conditions is encouraging more patients to seek early diagnosis and effective treatment. The U.K.’s robust healthcare infrastructure, combined with increasing public knowledge about gastrointestinal health, is expected to stimulate market growth.

Germany Blind Loop Syndrome Market Insight

The Germany blind loop syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by the increasing adoption of minimally invasive surgical techniques and innovative postoperative therapies. Germany’s strong healthcare system, emphasis on research and development, and patient preference for advanced, eco-conscious medical solutions are promoting the adoption of improved diagnostic and therapeutic options for Blind Loop Syndrome.

Asia-Pacific Blind Loop Syndrome Market Insight

The Asia-Pacific blind loop syndrome market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare awareness, rising disposable incomes, expanding hospital networks, and growing access to specialized gastroenterology clinics in countries such as India, China, and Japan. The region’s focus on early diagnosis, improved postoperative care, and adoption of minimally invasive treatments is further fueling market growth.

Japan Blind Loop Syndrome Market Insight

The Japan blind loop syndrome market is gaining momentum due to the country’s advanced healthcare infrastructure, high patient awareness, and demand for convenient, effective treatment solutions. Japanese hospitals and gastroenterology clinics are increasingly integrating modern diagnostic tools, postoperative monitoring programs, and evidence-based therapies, driving higher adoption rates. In addition, Japan’s aging population is expected to spur demand for safer and easier-to-administer treatment options for postoperative gastrointestinal complications.

China Blind Loop Syndrome Market Insight

The China blind loop syndrome market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rising healthcare awareness, expanding middle-class population, and increasing access to specialized gastroenterology and trichology clinics. China’s investment in healthcare infrastructure, focus on early diagnosis, and adoption of minimally invasive procedures are key factors propelling the market. Furthermore, domestic pharmaceutical and medical device companies are actively developing cost-effective treatment solutions to cater to a growing patient base, supporting continued market expansion.

Latest Developments in Global Blind Loop Syndrome Market

- In November 2024, a report highlighted that the Blind Loop Syndrome market is expanding due to growing awareness, advancements in treatment, and increasing cases linked to surgical interventions. Trends such as the focus on gastrointestinal health, advancements in nutritional therapy, and the rise of minimally invasive surgical options are driving the market forward

- In September 2025, a case report was published detailing a rare instance of small intestinal obstruction caused by large fecalith formation within a blind loop one year after side-to-side anastomosis. The report emphasized the importance of surgical technique selection and standardization in preventing BLS-related complications, providing valuable insights for clinical practice

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.