Global Blue Hydrogen Market

Market Size in USD Billion

USD

2.39 Billion

USD

4.73 Billion

2025

2033

USD

2.39 Billion

USD

4.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.39 Billion | |

| USD 4.73 Billion | |

| % | |

|

Blue Hydrogen Market Size

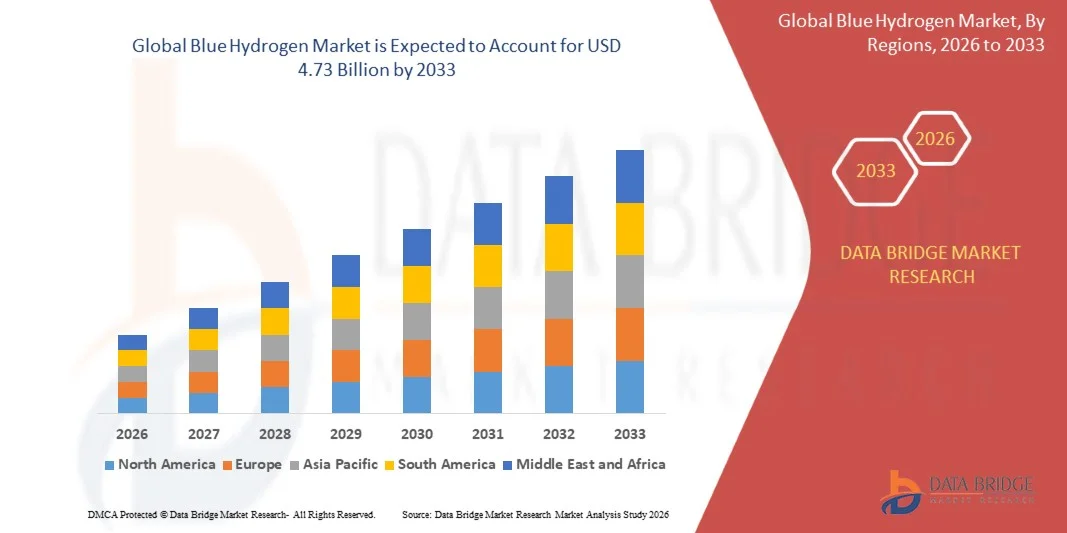

- The global blue hydrogen market size was valued at USD 2.39 billion in 2025 and is expected to reach USD 4.73 billion by 2033, at a CAGR of 8.90% during the forecast period

- The market growth is largely fuelled by the increasing global focus on low-carbon energy solutions, rising investments in carbon capture and storage (CCS) technologies, and the growing demand for clean hydrogen in industrial and power generation applications

- Expanding government initiatives and policies supporting hydrogen adoption, along with collaborations between energy companies and technology providers, are further accelerating market growth

Blue Hydrogen Market Analysis

- The market is witnessing increased research and development in blue hydrogen production technologies, including steam methane reforming integrated with carbon capture, utilization, and storage (CCUS) systems

- Strategic partnerships, joint ventures, and government incentives are shaping the competitive landscape and encouraging large-scale deployment of blue hydrogen infrastructure

- North America dominated the blue hydrogen market with the largest revenue share in 2025, driven by increasing investments in low-carbon energy, government incentives for decarbonization, and a growing focus on hydrogen adoption across industrial and power generation sectors

- Asia-Pacific region is expected to witness the highest growth rate in the global blue hydrogen market, driven by increasing investments in hydrogen infrastructure, rising focus on decarbonization, and expansion of industrial hydrogen applications

- The pipeline segment held the largest market revenue share in 2025, driven by the cost-efficiency and safety of transporting hydrogen over long distances for industrial and refinery applications. Pipelines also enable continuous supply for large-scale plants, ensuring steady operations and reducing dependency on local production

Report Scope and Blue Hydrogen Market Segmentation

|

Attributes |

Blue Hydrogen Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Blue Hydrogen Market Trends

“Rise of Low-Carbon Hydrogen Production Technologies”

• The growing emphasis on low-carbon energy sources is transforming the blue hydrogen market by enabling hydrogen production with carbon capture, utilization, and storage (CCUS) technologies. This allows industries to reduce carbon emissions while meeting energy demands, particularly in power generation and heavy industry sectors. In addition, the integration of CCUS into existing hydrogen plants supports regulatory compliance and contributes to regional decarbonization initiatives. Widespread adoption of these technologies is also creating opportunities for specialized engineering and service providers in the energy sector

• Increasing demand for clean energy solutions in regions with stringent emissions regulations is accelerating the adoption of blue hydrogen. These technologies are particularly relevant where natural gas is abundant, and where industries aim to transition away from coal and conventional fossil fuels. Governments and private stakeholders are collaborating to develop supportive frameworks, enabling large-scale deployment of blue hydrogen solutions. The trend also stimulates investment in complementary infrastructure such as pipelines, storage facilities, and hydrogen refueling stations

• The scalability and integration of blue hydrogen with existing natural gas infrastructure make it an attractive solution for energy producers. Large-scale plants allow cost-effective hydrogen production while minimizing environmental impact. Moreover, this approach reduces the need for entirely new infrastructure, accelerating project timelines and lowering capital expenditures. The compatibility of blue hydrogen with industrial processes further enhances its adoption across sectors such as refining, chemicals, and steel production

• For instance, in 2024, several industrial clusters in Europe and North America announced new blue hydrogen facilities incorporating CCUS, enabling large-scale decarbonization of power and chemical production. These projects demonstrated significant reductions in CO2 emissions while maintaining industrial output. In addition, the initiatives have encouraged collaboration between energy companies, technology providers, and research institutions, driving innovation and operational efficiencies in the sector

• While blue hydrogen adoption is increasing, market growth depends on continued technological innovation, investment in carbon capture infrastructure, and policy support to ensure competitiveness with green and grey hydrogen alternatives. Market players must focus on reducing production costs, optimizing capture efficiency, and developing scalable solutions. Furthermore, cross-border partnerships and knowledge-sharing initiatives are becoming essential to accelerate global adoption and integrate blue hydrogen into broader energy transition strategies

Blue Hydrogen Market Dynamics

Driver

“Increasing Demand for Low-Carbon Hydrogen and Government Support”

• Rising global focus on reducing greenhouse gas emissions is pushing governments and industries to adopt low-carbon hydrogen solutions. Sectors such as power generation, refining, and chemicals are prioritizing blue hydrogen to meet carbon reduction targets. Industrial players are investing in large-scale projects to align with net-zero commitments and strengthen their ESG credentials, which in turn attracts funding and stakeholder support

• Public sector incentives, including subsidies, tax credits, and carbon pricing mechanisms, are boosting investments in hydrogen production facilities and CCUS technologies. These financial frameworks reduce upfront costs and encourage private-sector participation. In addition, government-backed research grants are fostering technological advancements and improving efficiency in hydrogen production and carbon capture processes

• Industry initiatives for energy transition and decarbonization are further accelerating adoption, as companies aim to align with net-zero commitments and ESG goals. Collaborations across the energy value chain, from natural gas suppliers to hydrogen end-users, are facilitating project execution. This collaborative approach also ensures best practices, standardized safety protocols, and regulatory compliance across the emerging blue hydrogen market

• For instance, in 2023, the U.S. Department of Energy provided funding for multiple large-scale blue hydrogen projects, supporting both hydrogen production and carbon capture deployment. These initiatives demonstrated the feasibility of integrating blue hydrogen into existing industrial operations. In addition, pilot projects under these programs are providing real-world data to optimize technology deployment and inform policy frameworks

• While policy support and industrial demand drive the market, cost competitiveness, availability of natural gas, and CCUS infrastructure remain key factors for sustained adoption. Market players must focus on reducing operational costs, improving supply chain efficiency, and expanding production capacity. Strategic partnerships and regional collaborations also play a critical role in overcoming technical and financial barriers

Restraint/Challenge

“High Production Costs and Carbon Capture Infrastructure Limitations”

• The high capital and operational costs of producing blue hydrogen, particularly the integration of carbon capture and storage systems, limit adoption, especially in regions with smaller industrial capacity. Smaller firms may struggle to invest in CCUS technology, leading to slower deployment in emerging markets. In addition, the cost of monitoring and maintaining capture systems adds ongoing operational burdens that impact project feasibility

• Many areas lack adequate CO2 transportation and storage infrastructure, restricting the deployment of blue hydrogen projects and delaying large-scale implementation. Developing pipelines, storage sites, and monitoring systems requires substantial investment and long-term planning. The absence of such infrastructure also limits regional scalability and deters private investors from committing to large projects

• Market growth is also hindered by fluctuating natural gas prices and competition from green hydrogen produced from renewable electricity, which is gaining policy preference in several regions. Energy market volatility can increase production costs, affecting the overall competitiveness of blue hydrogen. In addition, regulatory uncertainty in certain regions creates risk for long-term investments

• For instance, in 2024, several blue hydrogen projects in Southeast Asia faced delays due to limited CO2 storage sites and high project costs, slowing adoption despite growing energy demand. Operational challenges, such as sourcing qualified workforce and obtaining environmental permits, further impacted project timelines. These issues underscore the importance of robust planning and policy support to mitigate market risks

• While technology continues to improve, addressing cost barriers, expanding CCUS networks, and ensuring regulatory clarity remain crucial to unlock the full market potential. Innovation in capture efficiency, modular plant designs, and financing solutions can further reduce barriers. Regional collaborations and cross-industry partnerships are also key to creating a sustainable and scalable blue hydrogen market

Blue Hydrogen Market Scope

The market is segmented on the basis of application, transportation mode, and technology.

• By Application

On the basis of application, the blue hydrogen market is segmented into chemical, refinery, power generation, and auto thermal reforming. The chemical segment held the largest market revenue share in 2025, driven by the widespread use of hydrogen in ammonia production, methanol synthesis, and petrochemical processes. Hydrogen demand in chemical industries is increasing due to regulatory pressure to reduce carbon emissions and the adoption of cleaner energy solutions.

The power generation segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the growing integration of hydrogen with low-carbon energy projects. Blue hydrogen is increasingly being utilized in combined heat and power plants and industrial energy systems, offering a cleaner alternative to conventional natural gas and coal-based energy generation. This segment benefits from government incentives promoting decarbonization and the transition to sustainable power solutions.

• By Transportation Mode

On the basis of transportation mode, the blue hydrogen market is segmented into pipeline and cryogenic liquid tankers. The pipeline segment held the largest market revenue share in 2025, driven by the cost-efficiency and safety of transporting hydrogen over long distances for industrial and refinery applications. Pipelines also enable continuous supply for large-scale plants, ensuring steady operations and reducing dependency on local production.

The cryogenic liquid tankers segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the need for flexible distribution solutions and expanding cross-border hydrogen trade. Cryogenic transport allows hydrogen to reach regions without pipeline connectivity, supporting emerging markets and decentralized hydrogen applications. The growth is further supported by advancements in liquefaction and insulation technologies that improve storage efficiency.

• By Technology

On the basis of technology, the blue hydrogen market is segmented into steam methane reforming (SMR) technology, gas partial oxidation, and auto thermal reforming (ATR). The steam methane reforming segment held the largest market revenue share in 2025, driven by its widespread adoption and proven efficiency in producing hydrogen at scale. SMR plants integrated with carbon capture and storage systems are increasingly being deployed to meet low-carbon hydrogen targets.

The auto thermal reforming segment is expected to witness the fastest growth rate from 2026 to 2033, due to its higher hydrogen yield, lower energy consumption, and compatibility with carbon capture technologies. ATR technology is gaining traction in industrial clusters where integration with existing natural gas infrastructure enables cost-effective, large-scale hydrogen production.

Blue Hydrogen Market Regional Analysis

• North America dominated the blue hydrogen market with the largest revenue share in 2025, driven by increasing investments in low-carbon energy, government incentives for decarbonization, and a growing focus on hydrogen adoption across industrial and power generation sectors

• Industries in the region highly value the integration of blue hydrogen with existing natural gas infrastructure, as well as its potential to reduce carbon emissions while supporting energy transition goals

• This widespread adoption is further supported by strong regulatory frameworks, technological advancements, and strategic initiatives for sustainable energy, establishing blue hydrogen as a preferred solution for chemical, refinery, and power generation applications

U.S. Blue Hydrogen Market Insight

The U.S. blue hydrogen market captured the largest revenue share in 2025 within North America, fueled by substantial investments in hydrogen production and carbon capture, utilization, and storage (CCUS) projects. Industrial and power sectors are increasingly prioritizing low-carbon hydrogen to meet decarbonization targets. The growing development of pipeline networks and cryogenic transportation, combined with supportive policies and incentives, is driving market expansion. Moreover, integration of blue hydrogen into existing industrial processes and the push for cleaner fuel alternatives is significantly contributing to market growth.

Europe Blue Hydrogen Market Insight

The Europe blue hydrogen market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent emissions regulations, government funding for CCUS projects, and ambitious net-zero targets. Rising industrial and energy sector demand, coupled with technological advancements in steam methane reforming and gas partial oxidation, is accelerating adoption. The region is seeing strong development across chemical, refinery, and power generation applications, supported by collaborative industrial initiatives and EU-wide hydrogen strategies.

U.K. Blue Hydrogen Market Insight

The U.K. blue hydrogen market is expected to witness significant growth from 2026 to 2033, driven by national initiatives promoting low-carbon hydrogen and investments in carbon capture infrastructure. Industrial hubs and energy-intensive sectors are adopting blue hydrogen to reduce greenhouse gas emissions and align with net-zero targets. The U.K.’s focus on innovative hydrogen production technologies and the integration of hydrogen into power and chemical sectors is expected to further stimulate market expansion.

Germany Blue Hydrogen Market Insight

The Germany blue hydrogen market is expected to witness rapid growth from 2026 to 2033, fueled by increasing demand for decarbonized industrial energy and government incentives for CCUS deployment. Germany’s well-established industrial base and emphasis on sustainable energy solutions promote adoption across chemical, refinery, and power generation sectors. Integration with existing natural gas infrastructure and advancements in auto thermal reforming technology are also enhancing market prospects, supporting both residential and industrial energy applications.

Asia-Pacific Blue Hydrogen Market Insight

The Asia-Pacific blue hydrogen market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising energy demand, increasing industrialization, and supportive government policies in countries such as China, Japan, and India. The region’s abundant natural gas reserves and growing focus on low-carbon solutions are encouraging adoption in chemical, refinery, and power sectors. Furthermore, technological advancements in blue hydrogen production and the expansion of transportation networks are improving accessibility and cost efficiency, broadening market potential.

Japan Blue Hydrogen Market Insight

The Japan blue hydrogen market is expected to witness strong growth from 2026 to 2033 due to the country’s high focus on energy transition, low-carbon technologies, and industrial decarbonization. Adoption is driven by the integration of hydrogen into power generation and industrial applications, supported by government incentives and technology innovation. Japan’s emphasis on sustainable energy and energy security is also promoting the development of CCUS-based hydrogen projects.

China Blue Hydrogen Market Insight

The China blue hydrogen market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s rapid industrialization, growing demand for low-carbon energy, and extensive natural gas infrastructure. Industrial sectors, power generation, and chemical plants are increasingly utilizing blue hydrogen to reduce emissions. The government’s push for hydrogen economy development, along with cost-efficient production technologies and domestic manufacturing capabilities, are key factors propelling market growth in China.

Blue Hydrogen Market Share

The Blue Hydrogen industry is primarily led by well-established companies, including:

- Linde plc (U.K.)

- Shell Group of Companies (U.K.)

- Air Liquide (France)

- Air Products and Chemicals, Inc. (U.S.)

- Engie (France)

- Equinor ASA (Norway)

- SOL Group (Spain)

- Iwatani Corp. (Japan)

- INOX Air Products Ltd. (India)

- Exxon Mobil Corp. (U.S.)

- Blue H (U.K.)

Latest Developments in Global Blue Hydrogen Market

- In March 2025, Aramco completed the acquisition of a 50% stake in Air Products Qudra-owned Blue Hydrogen Industrial Gases Company (BHIG) in Jubail, Saudi Arabia. The development aims to produce low-carbon blue hydrogen using carbon capture and storage (CCUS) to power a hydrogen network in the Eastern Province, supplying refining and petrochemical industries. This strategic move is expected to enhance regional hydrogen infrastructure, support decarbonization efforts, and strengthen Aramco’s position in the global low-carbon energy market.

- In November 2023, Air Products and Chemicals announced the construction of a next-generation CO2 capture and treatment facility at its hydrogen plant in Rotterdam, Netherlands. The facility is expected to begin operations in 2026, delivering blue hydrogen to ExxonMobil’s Rotterdam refinery and other customers via its pipeline network. The project will increase low-carbon hydrogen supply in Europe, support emission reduction targets, and boost the company’s market leadership in sustainable hydrogen solutions.

- In December 2023, SK E&S signed a global memorandum of understanding (MoU) during COP28 to build South Korea’s largest low-carbon hydrogen plant in collaboration with local government and international partners. The initiative focuses on mass-producing low-carbon hydrogen and developing a domestic hydrogen ecosystem, promoting carbon neutrality, supporting global decarbonization goals, and strengthening SK E&S’s strategic position in the international hydrogen market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Blue Hydrogen Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Blue Hydrogen Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Blue Hydrogen Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.