Global Bone Power Tools Market

Market Size in USD Billion

USD

36.51 Billion

USD

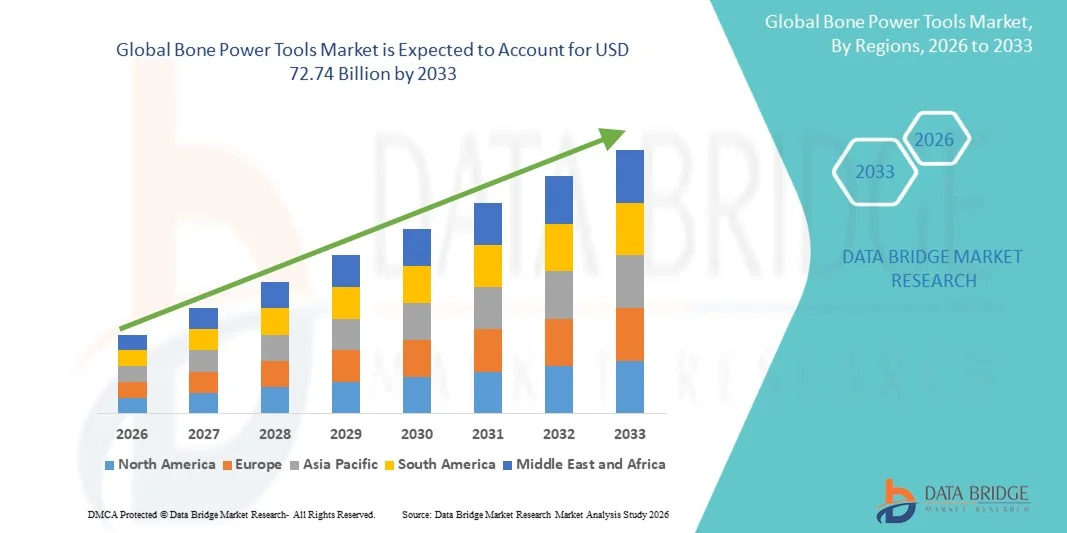

72.74 Billion

2025

2033

USD

36.51 Billion

USD

72.74 Billion

2025

2033

| 2026 - 2033 | |

| USD 36.51 Billion | |

| USD 72.74 Billion | |

| % | |

|

Bone Power Tools Market Overview

The Bone Power Tools Market was valued at USD 36.51 billion in 2025 and is projected to reach USD 72.74 billion by 2033, growing at a CAGR of 9.00% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for advanced orthopedic surgical procedures, increasing prevalence of bone-related disorders and trauma cases, rapid advancements in surgical power tool technologies, and expanding applications across orthopedic surgery, trauma care, and reconstructive procedures.

The growing incidence of musculoskeletal disorders, sports injuries, and age-related bone conditions, combined with increasing demand for minimally invasive and precision-based orthopedic interventions, is encouraging hospitals, ambulatory surgery centers, and specialty clinics to adopt advanced bone power tools. High-speed drills, saws, reamers, and robotic-assisted orthopedic instruments are improving surgical accuracy, reducing procedure time, and enhancing patient outcomes. The integration of battery-powered systems, ergonomic designs, and advanced control technologies is further supporting the adoption of modern bone power tools across global healthcare facilities.

Key Market Trends & Insights

- North America dominated the Bone Power Tools Market with the largest revenue share of 38.2% in 2025, supported by the presence of advanced orthopedic healthcare infrastructure, high adoption of technologically advanced surgical equipment, increasing orthopedic procedures, and strong presence of leading medical device companies. The region benefits from rising demand for minimally invasive orthopedic surgeries, growing geriatric population, and continuous investments in surgical innovation and hospital infrastructure.

- The large bone power tool segment dominated the market with a 42.6% share in 2025, owing to its extensive utilization in major orthopedic procedures such as joint replacement, trauma fixation, fracture repair, and reconstructive surgeries.

- Asia-Pacific is expected to be the fastest-growing region in the Bone Power Tools Market at a CAGR of 7.4% from 2026 to 2033, fueled by increasing healthcare expenditure, expanding orthopedic care facilities, rising prevalence of musculoskeletal disorders, and growing adoption of advanced surgical technologies across countries including China, India, and Japan. Government initiatives to improve healthcare access and increasing medical tourism are further supporting regional market expansion.

- The Battery-Powered Systems segment is projected to be the fastest-growing technology segment, registering a CAGR from 2026 to 2033, driven by increasing preference for cordless surgical instruments, improved mobility during orthopedic procedures, and advancements in battery efficiency. Battery-powered systems reduce dependency on external power sources, improve operating room flexibility, and enhance surgical workflow efficiency.

Market Size & Forecast

- Global Market Value (2025): USD 36.51 Billion

- Expected Market Value (2033): USD 72.74 Billion

- Forecast CAGR (2026–2033): 9.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Bone Power Tools Market Segmentation

|

Attributes |

Bone Power Tools Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Stryker Corporation (U.S.) |

|

Market Opportunities |

· Growing Adoption of Minimally Invasive and Advanced Orthopedic Surgical Procedures · Integration of Battery-Powered, Robotic-Assisted, and Smart Surgical Technologies · Expansion of Orthopedic Healthcare Infrastructure in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Bone Power Tools Market Trends

Trend: Growth in Adoption of Advanced Orthopedic Surgical Technologies

The Bone Power Tools Market is witnessing increasing adoption of advanced powered surgical instruments across orthopedic procedures due to the rising demand for precision, efficiency, and improved surgical outcomes. Hospitals and orthopedic centers are increasingly replacing conventional manual instruments with battery-powered, electric-powered, and pneumatic-powered systems that enable faster bone cutting, drilling, and reaming with enhanced control. The growing prevalence of musculoskeletal disorders, sports injuries, osteoarthritis, and trauma cases is accelerating the demand for orthopedic surgical equipment globally. For instance, the increasing volume of joint replacement procedures, including hip and knee arthroplasty, has encouraged healthcare providers to invest in high-performance bone power tools that improve surgical accuracy and reduce procedure time. In addition, advancements such as lightweight ergonomic designs, improved battery technologies, and integrated safety features are supporting wider adoption among orthopedic surgeons and ambulatory surgical centers.

Bone Power Tools Market Dynamics

Key Market Driver: Increasing Volume of Orthopedic Surgeries and Rising Prevalence of Musculoskeletal Disorders

The growing global burden of orthopedic conditions, including fractures, osteoarthritis, sports-related injuries, and degenerative bone disorders, is a major factor driving demand for Bone Power Tools. The aging population and increasing incidence of lifestyle-related musculoskeletal problems are contributing to a higher number of orthopedic procedures such as joint reconstruction, trauma fixation, and spine surgeries. According to global healthcare trends, the rising geriatric population has significantly increased demand for orthopedic interventions, particularly total joint replacement procedures. Bone power tools enable surgeons to perform precise cutting, drilling, and reaming during complex procedures, improving surgical efficiency and patient outcomes. In addition, hospitals and specialty orthopedic centers are increasingly adopting advanced powered instruments to reduce operative time, enhance workflow efficiency, and support minimally invasive surgical approaches. The growing expansion of orthopedic care infrastructure in emerging economies, along with increasing healthcare expenditure, is further supporting market growth.

Key Restraint/Challenge: High Cost of Advanced Bone Power Tool Systems and Maintenance Requirements

A significant challenge in the Bone Power Tools Market is the high acquisition and maintenance cost associated with advanced surgical power systems. Modern bone power tools incorporate sophisticated technologies such as high-speed motors, rechargeable battery systems, precision control mechanisms, and specialized attachments, resulting in higher procurement costs compared with conventional surgical instruments. Healthcare facilities, particularly smaller hospitals and clinics in developing regions, may face affordability challenges when investing in advanced orthopedic equipment. In addition, these systems require regular maintenance, sterilization processes, battery replacement, and periodic servicing to ensure reliable performance and patient safety. Training requirements for surgeons and operating room staff also increase the overall adoption cost. These factors can limit penetration in cost-sensitive markets despite the clinical advantages offered by advanced bone power tools.

Key Market Opportunity: Expansion of Battery-Powered Systems and Minimally Invasive Orthopedic Procedures

The increasing shift toward cordless surgical technologies and minimally invasive orthopedic procedures presents significant growth opportunities for the Bone Power Tools market. Battery-powered bone tools are gaining traction due to their portability, improved operating room flexibility, and reduced dependency on external power sources. Advancements in lithium-ion battery technology are enabling longer operating times, faster charging, and improved reliability during complex surgical procedures. In addition, the rising adoption of outpatient orthopedic procedures and ambulatory surgery centers is creating demand for compact and efficient surgical equipment. Companies are focusing on developing lightweight ergonomic systems, improved surgical attachments, and digitally integrated tools to enhance precision and workflow. Furthermore, increasing healthcare investments in emerging markets, expansion of orthopedic specialty centers, and growing demand for advanced trauma and reconstructive surgeries are expected to create new opportunities for market growth.

Bone Power Tools Market Scope

The Bone Power Tools market is segmented on the basis of type, technology, and end-user.

- By Type

On the basis of type, the Bone Power Tools Market is segmented into large bone power tools, small bone power tools, high-speed bone power tools, and orthopedic reamers. The large bone power tool segment dominated the market with a 42.6% share in 2025, owing to its extensive utilization in major orthopedic procedures such as joint replacement, trauma fixation, fracture repair, and reconstructive surgeries. Large bone power tools provide high torque, enhanced cutting efficiency, and improved surgical precision, making them essential for procedures involving femur, tibia, and other major bones. Increasing prevalence of orthopedic disorders, rising number of hip and knee replacement surgeries, and growing adoption of advanced surgical instruments across hospitals are supporting segment dominance. Furthermore, increasing investments by healthcare providers in advanced orthopedic operating room infrastructure and surgeon preference for reliable powered systems are strengthening demand for large bone power tools globally.

The high-speed bone power tool segment is expected to witness the fastest growth with a CAGR of 7.8% from 2026 to 2033, driven by increasing adoption in precision-based orthopedic and neurosurgical procedures requiring accurate bone cutting and controlled drilling. High-speed systems offer improved surgical performance, reduced procedure time, and enhanced control during complex interventions. Growing demand for minimally invasive orthopedic surgeries, advancements in motor technology, and integration of ergonomic designs are accelerating segment growth. In addition, increasing use of high-speed bone tools in sports injury treatments, spinal procedures, and reconstructive surgeries is creating significant expansion opportunities.

- By Technology

On the basis of technology, the Bone Power Tools Market is segmented into pneumatic-powered systems, battery-powered systems, and electric-powered systems. The electric-powered systems segment dominated the market with a 39.7% share in 2025, supported by its widespread adoption in hospitals and orthopedic surgical centers due to consistent power output, high operational efficiency, and suitability for complex procedures. Electric-powered systems provide precise control, reliable performance, and compatibility with multiple surgical attachments, making them preferred for joint replacement, trauma, and reconstructive orthopedic surgeries. The growing adoption of advanced surgical technologies, increasing demand for precision instruments, and expansion of orthopedic specialty departments are contributing to segment growth. In addition, healthcare facilities are increasingly upgrading from conventional manual tools to powered electric systems to improve surgical workflow and patient outcomes.

The Battery-Powered Systems segment is projected to register the fastest CAGR of 7.6% from 2026 to 2033, driven by increasing demand for cordless surgical instruments, improved mobility, and enhanced flexibility during orthopedic procedures. Advancements in lithium-ion battery technology are enabling longer operating times, faster charging capabilities, and improved reliability in surgical environments. Battery-powered systems reduce dependency on external power sources and allow surgeons greater maneuverability during complex procedures. Rising adoption across ambulatory surgery centers, trauma care facilities, and hospitals seeking portable surgical solutions is further supporting market expansion. In addition, manufacturers are focusing on lightweight ergonomic designs and rechargeable systems to improve surgical efficiency.

- By End User

On the basis of end user, the Bone Power Tools Market is segmented into Hospitals, orthopedic clinics, ambulatory surgery centres, and others. The Hospitals segment dominated the market with a 54.8% share in 2025, owing to the high volume of orthopedic procedures performed in hospital settings and the availability of advanced surgical infrastructure. Hospitals represent the primary users of bone power tools due to their capability to manage complex orthopedic surgeries, including trauma procedures, joint replacement, and reconstructive operations. Increasing healthcare expenditure, expansion of orthopedic departments, and rising adoption of technologically advanced surgical equipment are supporting market growth. Furthermore, hospitals are investing in powered surgical instruments to improve operational efficiency, reduce surgery duration, and enhance clinical outcomes.

The Ambulatory Surgery Centres (ASCs) segment is expected to be the fastest-growing end-user segment with a CAGR of 7.1% from 2026 to 2033, driven by the growing shift toward outpatient orthopedic procedures, cost-effective surgical models, and shorter patient recovery periods. ASCs are increasingly adopting compact, efficient, and portable bone power tools to perform procedures such as minor orthopedic repairs, sports injury treatments, and selected joint procedures. The expansion of ASC networks, rising demand for minimally invasive surgeries, and increasing preference for same-day discharge procedures are accelerating adoption. In addition, healthcare systems are encouraging outpatient care models to reduce hospitalization costs, creating new opportunities for bone power tool manufacturers.

Bone Power Tools Market Regional Analysis

North America dominated the Bone Power Tools Market and accounted for the largest revenue share of 38.2% in 2025, supported by advanced orthopedic healthcare infrastructure, high adoption of technologically advanced surgical equipment, increasing orthopedic procedure volumes, and the strong presence of leading medical device companies. The region benefits from rising demand for minimally invasive orthopedic surgeries, increasing prevalence of musculoskeletal disorders, and a growing geriatric population requiring joint replacement, trauma care, and reconstructive procedures. Continuous investments in hospital modernization, surgical innovation, and advanced orthopedic technologies are further strengthening North America’s leading position in the Bone Power Tools Market. In addition, favorable healthcare reimbursement systems and rapid adoption of battery-powered and precision surgical instruments are supporting market growth across hospitals and specialty orthopedic centers.

U.S. Bone Power Tools Market Insight

The U.S. bone power tools market is witnessing strong growth due to increasing orthopedic surgeries, rising demand for advanced surgical technologies, and growing adoption of minimally invasive procedures. The country’s well-established healthcare infrastructure, high number of orthopedic specialists, and presence of major medical device manufacturers are driving demand for advanced bone drills, saws, reamers, and powered surgical systems. Increasing cases of sports injuries, trauma-related fractures, and age-associated orthopedic conditions are further supporting market expansion. In addition, continuous investments in robotic-assisted surgery, surgical navigation systems, and technologically advanced orthopedic equipment are accelerating adoption across hospitals, ambulatory surgery centers, and specialty clinics.

Europe Bone Power Tools Market Insight

The Europe bone power tools market remains a significant contributor to global revenue, driven by advanced healthcare systems, increasing orthopedic procedures, and strong focus on surgical innovation. Countries across Europe are adopting advanced bone power tools to improve surgical accuracy, reduce procedure time, and enhance patient outcomes in trauma and reconstructive surgeries. The region benefits from the presence of established medical technology companies, increasing healthcare expenditure, and growing demand for minimally invasive orthopedic treatments. Furthermore, rising awareness regarding advanced surgical solutions and expansion of orthopedic care facilities are supporting market growth throughout Europe.

U.K. Bone Power Tools Market Insight

The U.K. bone power tools market is experiencing steady growth, supported by increasing orthopedic surgical procedures, rising healthcare investments, and growing adoption of advanced surgical instruments. Hospitals and orthopedic centers are increasingly utilizing powered surgical tools for fracture fixation, joint reconstruction, and trauma-related procedures to improve efficiency and surgical precision. The country’s focus on improving healthcare infrastructure and adopting innovative medical technologies is contributing to market expansion. Moreover, increasing demand for minimally invasive procedures and advanced orthopedic solutions is strengthening the adoption of bone power tools across the U.K. healthcare sector.

Germany Bone Power Tools Market Insight

The Germany bone power tools market is expanding steadily due to the country’s strong medical device industry, advanced healthcare infrastructure, and focus on precision surgical technologies. Orthopedic hospitals, surgical centers, and healthcare institutions are increasingly adopting advanced power tools for complex orthopedic procedures, including trauma surgery, joint replacement, and bone reconstruction. Germany’s strong research capabilities, innovation-driven healthcare environment, and presence of leading orthopedic device manufacturers are supporting market growth. In addition, increasing adoption of battery-powered surgical systems and advanced ergonomic designs is enhancing the efficiency and usability of bone power tools.

Asia-Pacific Bone Power Tools Market Insight

The Asia-Pacific bone power tools market is expected to witness rapid growth, driven by increasing healthcare expenditure, expanding orthopedic care facilities, rising prevalence of musculoskeletal disorders, and growing adoption of advanced surgical technologies across countries such as China, India, and Japan. The region is experiencing increased demand for orthopedic procedures due to aging populations, rising sports injuries, and improving access to healthcare services. Government initiatives focused on healthcare modernization, hospital infrastructure development, and medical technology adoption are supporting market expansion. Furthermore, increasing medical tourism and growing availability of advanced surgical treatments are accelerating adoption of Bone Power Tools across the region.

Japan Bone Power Tools Market Insight

The Japan bone power tools market is witnessing consistent growth due to rising demand for advanced orthopedic procedures, aging population trends, and increasing adoption of innovative surgical technologies. Hospitals and orthopedic centers are increasingly using high-precision bone power tools for joint replacement, fracture treatment, and reconstructive surgeries. Japan’s strong healthcare infrastructure, focus on surgical quality improvement, and investment in medical technology development are supporting market growth. Additionally, increasing adoption of battery-powered systems and advanced surgical equipment is improving procedural efficiency and contributing to wider market adoption.

China Bone Power Tools Market Insight

The China bone power tools market is growing rapidly, driven by expanding healthcare infrastructure, increasing orthopedic surgery volumes, and rising investments in advanced medical technologies. The growing prevalence of bone-related disorders, trauma cases, and aging population is increasing demand for orthopedic surgical equipment across hospitals and specialty centers. Government initiatives to improve healthcare access, expand hospital capabilities, and modernize surgical facilities are further supporting market growth. In addition, increasing adoption of minimally invasive orthopedic procedures and rising availability of advanced surgical tools are positioning China as one of the fastest-growing markets for Bone Power Tools globally.

Bone Power Tools Market Share

The Bone Power Tools industry is primarily led by well-established companies, including:

- Stryker Corporation (U.S.)

- Medtronic plc (Ireland/U.S.)

- Johnson & Johnson MedTech (U.S.)

- Zimmer Biomet Holdings Inc. (U.S.)

- Smith+Nephew plc (U.K.)

- DePuy Synthes (U.S.)

- CONMED Corporation (U.S.)

- B. Braun Melsungen AG (Germany)

- Aesculap AG (Germany)

- Arthrex Inc. (U.S.)

- DJO Global (U.S.)

- De Soutter Medical Limited (U.K.)

- Misonix Inc. (U.S.)

- Nouvag AG (Switzerland)

- NSK Nakanishi Inc. (Japan)

- ConMed Linvatec (U.S.)

- Adeor Medical AG (Germany)

- MicroAire Surgical Instruments (U.S.)

- SurgTech Inc. (U.S.)

- Brasseler USA (U.S.)

- Medicon eG (Germany)

- Linvatec Corporation (U.S.)

- Aygun Surgical Instruments (Turkey)

- GPC Medical Ltd. (India)

- OrthoPediatrics Corp. (U.S.)

- Integra LifeSciences (U.S.)

- KLS Martin Group (Germany)

- AtriCure Inc. (U.S.)

- Wright Medical Group (U.S.)

- Sharma Orthopedic (India)

- RWD Life Science (China)

Latest Developments in Bone Power Tools Market

- In November 2021, DePuy Synthes, a Johnson & Johnson MedTech company, announced the launch of the UNIUM System, a next-generation power tools platform designed for trauma and small bone surgical procedures. The system introduced enhanced ergonomic handpieces, improved versatility, and lightweight designs to support precision, efficiency, and surgeon comfort during orthopedic procedures. The UNIUM™ System was developed to address growing demand for compact, reliable, and multifunctional surgical power tools across trauma, sports medicine, spine, and thorax applications, strengthening DePuy Synthes’ orthopedic power tool portfolio

- In March 2023, Zimmer Biomet announced the latest enhancements to its ZBEdge™ Dynamic Intelligence ecosystem, expanding its digital orthopedic technology portfolio through improved integration of robotics, surgical planning, and data-driven solutions. The updates highlighted the company’s focus on connected orthopedic care by combining digital technologies with surgical workflows to improve precision, efficiency, and patient-specific treatment planning. These advancements reflect the broader industry shift toward technology-enabled orthopedic procedures and integrated surgical platforms supporting bone-related interventions

- In March 2023, Zimmer Biomet’s ROSA HIP® with ONE Planner™ Hip received recognition as an Orthopaedic Product Innovation of the Year, highlighting advancements in robotic-assisted orthopedic procedures. The system uses patient-specific planning and real-time feedback technologies to support surgeons during hip replacement procedures, demonstrating the increasing adoption of digital assistance and precision technologies within orthopedic surgery. The development supports market growth for advanced surgical tools and related orthopedic equipment, including powered instrumentation used in complex procedures

- In August 2024, DePuy Synthes, part of Johnson & Johnson MedTech, launched the TriLEAP Lower Extremity Anatomic Plating System to expand its orthopedic trauma solutions portfolio. Although focused on fixation rather than powered instrumentation, the launch supports the broader orthopedic surgery ecosystem by addressing complex foot and ankle reconstruction procedures that frequently utilize bone preparation tools, drilling systems, and surgical power equipment. The introduction reflects continued investment in advanced orthopedic solutions for fracture management and reconstructive procedures

- In October 2024, Johnson & Johnson MedTech announced the launch of the VOLT Variable Angle Optimized Locking Technology Plating System through DePuy Synthes. The system was designed to improve fracture management through enhanced stability, flexibility, and surgical workflow efficiency. The launch highlights continued innovation in orthopedic trauma care, where advanced fixation systems are increasingly used alongside high-performance bone power tools for drilling, cutting, and preparation during surgical procedures

- In January 2025, Zimmer Biomet announced plans to acquire Paragon 28 for approximately USD 1.1 billion to strengthen its orthopedic surgical device portfolio. The acquisition was aimed at expanding Zimmer Biomet’s presence in foot and ankle surgery, trauma care, and extremity procedures. This strategic move reflects ongoing consolidation in the orthopedic market as leading companies seek to broaden their surgical solutions portfolio, including technologies associated with bone preparation and powered surgical applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.