Global Bradykinin Mediated Angioedema Market

Market Size in USD Billion

USD

6.97 Billion

USD

10.21 Billion

2025

2033

USD

6.97 Billion

USD

10.21 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.97 Billion | |

| USD 10.21 Billion | |

| % | |

|

Bradykinin Mediated Angioedema Market Size

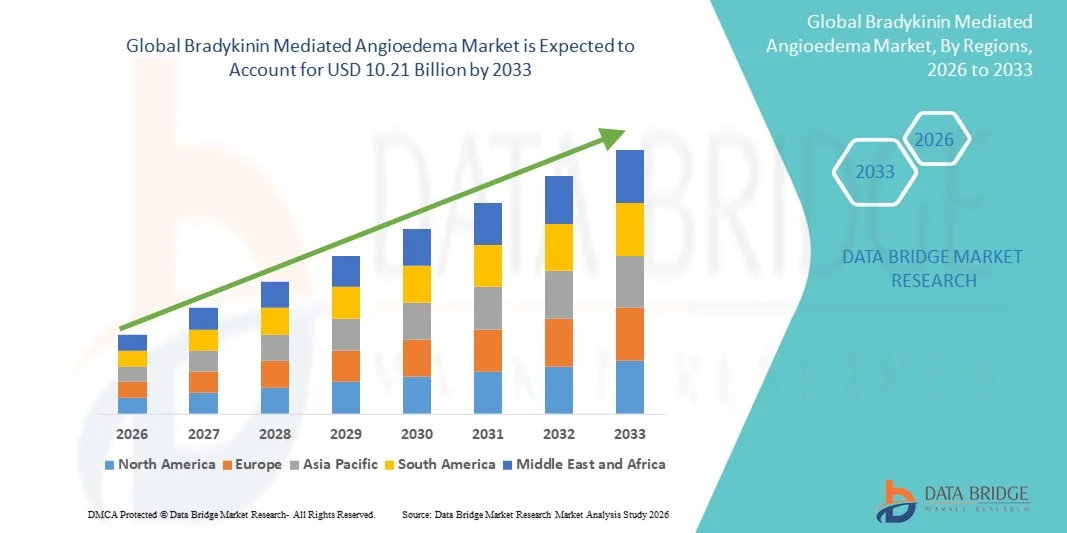

- The global bradykinin mediated angioedema market size was valued at USD 6.97 billion in 2025 and is expected to reach USD 10.21 billion by 2033, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by increasing prevalence of hereditary angioedema (HAE) and other bradykinin-mediated conditions, coupled with rising awareness among healthcare professionals and patients regarding early diagnosis and treatment options

- Furthermore, the growing adoption of innovative therapies, such as C1-inhibitor replacement, bradykinin receptor antagonists, and kallikrein inhibitors, is enhancing patient outcomes and expanding treatment accessibility. These converging factors are accelerating the uptake of Bradykinin Mediated Angioedema solutions, thereby significantly boosting the industry’s growth

Bradykinin Mediated Angioedema Market Analysis

- Bradykinin Mediated Angioedema, a rare genetic condition characterized by recurrent episodes of severe swelling, is increasingly gaining attention due to rising awareness among healthcare professionals and patients, as well as improvements in early diagnosis and management strategies

- The escalating demand for effective therapies is primarily fueled by the growing prevalence of hereditary angioedema, increasing adoption of advanced treatment options such as C1-inhibitor replacement, bradykinin receptor antagonists, and kallikrein inhibitors, and heightened focus on improving patient outcomes

- North America dominated the bradykinin mediated angioedema market with the largest revenue share of 42.7% in 2025, driven by well-established healthcare infrastructure, high awareness of hereditary angioedema, advanced diagnostic programs, and the presence of leading biopharmaceutical companies. The U.S. is witnessing substantial growth in clinical adoption of targeted therapies, enzyme replacement programs, and outpatient treatment initiatives

- Asia-Pacific is expected to be the fastest-growing region in the bradykinin mediated angioedema market during the forecast period, projected to expand at a CAGR of 15.5% from 2026 to 2033. Growth is driven by increasing healthcare modernization, rising awareness of rare genetic disorders, expanded newborn screening programs, and improving access to specialized therapies in countries such as Japan, China, and India

- The Injectable segment dominated the largest market revenue share of 48.3% in 2025, due to rapid onset of action critical for acute attacks

Report Scope and Bradykinin Mediated Angioedema Market Segmentation

|

Attributes |

Bradykinin Mediated Angioedema Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Bradykinin Mediated Angioedema Market Trends

Increasing Focus on Targeted Therapies and Personalized Treatment

- A significant and accelerating trend in the global bradykinin mediated angioedema (BMA) market is the rising adoption of targeted therapies and personalized treatment approaches

- Advances in understanding the genetic and molecular mechanisms of BMA are enabling physicians to offer patient-specific therapies tailored to attack frequency, severity, and triggers

- For instance, in June 2024, a study published in Allergy highlighted the effectiveness of newly optimized bradykinin receptor inhibitors in reducing acute episodes, demonstrating significant improvements in patient outcomes

- This trend reflects the broader move toward precision medicine in rare hereditary and acquired angioedema

- Biopharmaceutical companies are increasingly investing in research and development to produce therapies with improved safety profiles, longer dosing intervals, and oral formulations, responding to patient and clinician demand for more convenient and effective disease management options

- There is growing adoption of prophylactic therapies that help prevent acute attacks, rather than treating symptoms reactively, which improves overall patient quality of life and reduces healthcare burden

- Collaboration between research institutions and pharmaceutical companies is accelerating the discovery of novel small-molecule inhibitors and biologics specifically targeting bradykinin pathways

- Increased patient-centric programs, such as home administration training and mobile monitoring, are being implemented to enhance adherence to treatment plans and provide real-time feedback for personalized care adjustments

Bradykinin Mediated Angioedema Market Dynamics

Driver

Growing Prevalence of Hereditary and Acquired Angioedema

- The rising global incidence of hereditary angioedema (HAE) and acquired bradykinin-mediated angioedema is a key driver of market growth

- Increased disease awareness among healthcare professionals and patients has improved diagnosis rates, prompting higher demand for effective therapies

- For instance, in March 2023, Pharming Group expanded access to Ruconest® across multiple European countries, providing an additional therapeutic option for acute attacks. Expansion of hospital networks and specialized care centers further supports the administration of targeted BMA treatments

- Furthermore, early diagnosis programs, genetic screening, and patient support initiatives are driving adoption of therapies that reduce attack severity and improve quality of life, particularly in pediatric and high-risk adult populations

- The growing focus on patient education and self-management strategies, including home-based treatment administration, is also encouraging treatment adherence and boosting market demand

Restraint/Challenge

High Treatment Costs and Limited Awareness in Emerging Markets

- High costs associated with advanced therapies for BMA remain a significant challenge, limiting access in price-sensitive regions and affecting widespread adoption

- Specialty biologics and bradykinin receptor inhibitors often require significant financial resources, which can be a barrier for healthcare systems and patients alike

- For instance, in January 2024, a report in Orphanet Journal of Rare Diseases emphasized that lack of insurance coverage or reimbursement in developing countries delays timely treatment, increasing the risk of severe or life-threatening attacks

- In addition, limited disease awareness in emerging markets contributes to delayed diagnosis, misdiagnosis, and suboptimal therapy use. Bridging these gaps through awareness campaigns, physician training programs, and cost-reduction strategies is essential for sustained market growth

- Overcoming these challenges requires collaboration between biopharma companies, payers, and healthcare institutions to improve access, affordability, and education, ensuring that more patients can benefit from effective BMA therapies

Bradykinin Mediated Angioedema Market Scope

The market is segmented on the basis of drug class, mode of administration, distribution channel, and end user.

- By Drug Class

On the basis of drug class, the Bradykinin Mediated Angioedema market is segmented into C1-INH Concentrates, Bradykinin B2-Receptor Antagonist, Icatibant, Kallikrein Inhibitor, Ecallantide, and Others. The C1-INH Concentrates segment dominated the largest market revenue share of 42.6% in 2025, driven by its proven efficacy in managing both acute attacks and prophylactic treatment. Longstanding clinical usage, strong physician preference, and regulatory approvals reinforce its dominance. Hospitals and specialty clinics rely heavily on C1-INH due to standardized dosing protocols and well-documented safety profiles. It is also preferred for severe cases where rapid intervention is critical. Continuous patient education, awareness campaigns, and consistent supply in hospitals support its leading position. Additionally, C1-INH products have wide acceptance among hereditary and acquired angioedema patients, ensuring sustained demand. Insurance coverage and reimbursement policies further boost adoption. Frequent updates to clinical guidelines also maintain its prominence in therapy regimens. Research and development efforts continue to improve formulations, stability, and patient convenience. Its established track record makes it a preferred first-line therapy in multiple markets worldwide.

The Bradykinin B2-Receptor Antagonist segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by increasing adoption of targeted therapies. Improved safety profiles and rapid onset of action make it highly suitable for acute attack management. Growing evidence from clinical trials demonstrating effectiveness and tolerability encourages wider use. Hospitals and specialty clinics are expanding the use of these antagonists as they offer patient-specific benefits. The availability of newer formulations with easier administration supports patient compliance. The segment is gaining traction in markets with rising awareness of hereditary angioedema. Expansion of government and insurance reimbursement schemes also facilitates faster adoption. Increasing clinician preference for personalized therapy further accelerates growth. Biopharmaceutical companies are investing in marketing and educational initiatives to promote adoption. Ongoing R&D may introduce oral or self-administered forms, enhancing accessibility. Rising prevalence of angioedema worldwide contributes to higher uptake. Patient advocacy programs support awareness and prescription of these therapies.

- By Mode of Administration

On the basis of mode of administration, the market is segmented into Injectable, Oral, and Others. The Injectable segment dominated the largest market revenue share of 48.3% in 2025, due to rapid onset of action critical for acute attacks. Hospitals and specialty clinics prefer injectable formulations for emergency management. Proven clinical efficacy and well-established dosing guidelines support widespread adoption. Injectable therapies are commonly included in emergency care protocols. Physician familiarity with injectables ensures confidence in administration and patient outcomes. Training programs reinforce correct usage and safety. Long-term prophylactic use in hereditary angioedema enhances reliance on injectables. Regulatory approvals for injectables are well established, ensuring trust. Patients and caregivers also rely on injectables during hospital visits. Continuous supply chains in hospital pharmacies support consistent availability. Evidence from multiple studies confirms high efficacy, reinforcing their dominant market share. Patient outcomes and satisfaction with injectables remain high, maintaining market leadership.

The Oral segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by development of patient-friendly formulations. Oral therapies enable home-based administration and improve adherence. They reduce hospital visits and enhance convenience for chronic management. Patients prefer oral therapy for ease of use and comfort. Biopharmaceutical companies are investing in oral drug R&D to expand availability. Positive clinical trial results on efficacy and tolerability increase acceptance. Increased awareness among patients and caregivers supports adoption. Insurance coverage and affordability improve access. Growing adoption in emerging markets drives faster growth. Integration with telemedicine and homecare support further boosts uptake. Oral options are particularly appealing for pediatric and elderly patients. Educational campaigns on correct usage support safer self-administration. Expansion of prescription networks and retail distribution increases accessibility.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. The Hospital Pharmacies segment accounted for the largest market revenue share of 50.5% in 2025, due to direct physician prescriptions and availability of acute care drugs. Hospitals ensure controlled storage and prompt access for emergency and prophylactic treatments. Hospital pharmacies are preferred for managing severe hereditary angioedema cases. Standardized dosing protocols and trained personnel support safe administration. Physicians rely on hospital pharmacies to ensure timely and quality treatment. High patient trust in hospital-based dispensing reinforces dominance. Hospitals often integrate pharmacy services with specialty angioedema clinics. Insurance coverage and reimbursements are readily applicable to hospital purchases. Established supply chains ensure consistent drug availability. Hospital pharmacies maintain high inventory levels to meet emergency demands. Collaboration with specialists supports adherence to clinical guidelines. Hospitals also facilitate patient monitoring and follow-up for optimal therapy.

The Online Pharmacies segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, driven by rising e-commerce adoption. Online pharmacies offer convenience of home delivery, particularly for chronic and prophylactic therapies. Patients benefit from easy access to medications without hospital visits. Telemedicine prescriptions further accelerate online sales. Growing awareness among patients about availability and convenience supports uptake. Expansion of regulatory approvals for online sale increases market penetration. Online platforms improve accessibility in remote or underserved regions. Digital marketing and patient education campaigns enhance awareness. Secure payment and delivery mechanisms build consumer confidence. Homecare patients particularly prefer online pharmacy access. Integration with insurance and reimbursement policies facilitates affordability. Patient-centric services and customer support encourage repeat orders. Rising global internet penetration contributes to faster growth.

- By End User

On the basis of end user, the market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment dominated with a 52.4% market share in 2025, driven by emergency and acute care needs. Hospitals provide access to trained staff, standardized protocols, and specialized therapies. Severe hereditary angioedema attacks are primarily treated in hospital settings. Integration of hospital-based pharmacies ensures immediate availability of drugs. Physician preference for hospital-based treatment reinforces market share. Established clinical guidelines encourage hospital administration. Hospitals maintain high patient monitoring for treatment efficacy. Hospital-centric clinical trials further support therapy adoption. Insurance and reimbursement schemes often favor hospital-administered therapy. Hospitals provide training and support for caregivers and patients. Hospital end users ensure quality and regulatory compliance. Reputation and trust in hospitals drive adoption over other channels. Consistent supply chain management ensures continuity of therapy.

The Homecare segment is expected to witness the fastest CAGR of 10.5% from 2026 to 2033, driven by patient preference for home-based management. Self-administration of injectable or oral therapies supports independence. Telemedicine and nurse-led homecare services facilitate treatment adherence. Growing awareness of hereditary angioedema management encourages homecare adoption. Improved safety of therapies allows home administration. Homecare reduces hospital visits and overall healthcare costs. Patient comfort and convenience are major adoption drivers. Training programs for caregivers improve compliance. Expansion of insurance coverage for home-administered therapies increases accessibility. Homecare supports chronic prophylactic treatment efficiently. Rising patient demand for personalized therapy accelerates growth. Digital tools for monitoring enhance safety and efficacy. Collaboration with specialty clinics provides ongoing support for patients.

Bradykinin Mediated Angioedema Market Regional Analysis

- North America dominated the bradykinin mediated angioedema market with the largest revenue share of 42.7% in 2025

- Supported by a strong healthcare infrastructure, high awareness of hereditary angioedema, widespread implementation of advanced diagnostic programs, and the presence of leading biopharmaceutical companies actively developing innovative therapies

- The region benefits from extensive patient education, early detection initiatives, and comprehensive treatment networks that facilitate timely interventions

U.S. Bradykinin Mediated Angioedema Market Insight

The U.S. bradykinin mediated angioedema market is the leading country in North America, capturing the largest revenue share of 81% in 2025. Growth is driven by the robust adoption of targeted therapies, enzyme replacement programs, and outpatient care models tailored to hereditary angioedema patients. In addition, strong clinical trial activity, advanced diagnostic adoption in hospitals and specialty clinics, and extensive patient support programs contribute to market expansion. Awareness campaigns and educational initiatives have further enhanced early diagnosis rates and treatment compliance.

Europe Bradykinin Mediated Angioedema Market Insight

Europe bradykinin mediated angioedema market is expected to grow steadily throughout the forecast period, primarily driven by increasing awareness of rare genetic disorders, strong regulatory support for orphan drugs, and growing investment in specialized healthcare infrastructure. The market expansion is also supported by the availability of advanced diagnostic tools, patient education programs, and adoption of novel treatment protocols in clinical settings.

U.K. Bradykinin Mediated Angioedema Market Insight

The U.K. bradykinin mediated angioedema market is projected to expand at a notable CAGR, supported by government-led hereditary angioedema awareness initiatives, improved access to specialty clinics, and high adoption of enzyme replacement therapies. The growing focus on early diagnosis, patient-centric care models, and availability of advanced therapeutics in hospitals and outpatient facilities is further driving market growth.

Germany Bradykinin Mediated Angioedema Market Insight

Germany’s bradykinin mediated angioedema market is expected to experience considerable growth, fueled by extensive national rare disease programs, increasing healthcare expenditure, and the presence of advanced treatment centers. The adoption of targeted therapies, enzyme replacement programs, and proactive screening initiatives in hospitals and specialty clinics is contributing significantly to market expansion.

Asia-Pacific Bradykinin Mediated Angioedema Market Insight

Asia-Pacific bradykinin mediated angioedema market is expected to be the fastest-growing region, projected to expand at a CAGR of 15.5% from 2026 to 2033. Growth is driven by healthcare modernization, increasing awareness of rare genetic disorders, expanding newborn and hereditary screening programs, and improving access to specialized therapies in countries such as Japan, China, and India. Rising investments in healthcare infrastructure, expanding patient support initiatives, and growing adoption of advanced treatment modalities are also key contributors to market growth.

Japan Bradykinin Mediated Angioedema Market Insight

Japan bradykinin mediated angioedema market is witnessing growth due to increasing hereditary angioedema awareness, advanced adoption of diagnostic programs, and rising use of enzyme replacement and targeted therapies in hospitals and specialty clinics. The country’s focus on patient education, coupled with strong government support for rare disease initiatives, is further enhancing early diagnosis and treatment adoption rates.

China Bradykinin Mediated Angioedema Market Insight

China bradykinin mediated angioedema market accounted for the largest revenue share in Asia-Pacific in 2025, supported by healthcare modernization, increasing awareness of rare disorders, improved diagnostic capabilities, and broader access to specialized therapies. Government initiatives promoting rare disease screening, coupled with rising healthcare spending and the expansion of specialty treatment centers, are significantly contributing to market growth.

Bradykinin Mediated Angioedema Market Share

The Bradykinin Mediated Angioedema industry is primarily led by well-established companies, including:

- BioCryst Pharmaceuticals (U.S.)

- Sanofi (France)

- Roche (Switzerland)

- Pfizer (U.S.)

- Hemopharm (Turkey)

- CSL Behring (Australia)

- Sobi (Sweden)

- Ferring Pharmaceuticals (Switzerland)

- Octapharma (Switzerland)

- Pharming Group (Netherlands)

- Hikma Pharmaceuticals (Jordan)

- Takeda Pharmaceutical (Japan)

- Astellas Pharma (Japan)

- Meda Pharma (Sweden)

- Grifols (Spain)

- Mylan (U.S.)

- Argenx (Belgium)

- AbbVie (U.S.)

- Aptevo Therapeutics (U.S.)

Latest Developments in Global Bradykinin Mediated Angioedema Market

- In June 2025, Pharvaris announced clinical data demonstrating that their oral bradykinin B2-receptor antagonist, deucrictibant, provided durable relief with a single dose in many hereditary angioedema (HAE) attacks. The data supported both on-demand and prophylactic use, marking a significant advancement in patient-centric treatment options

- In May 2025, Pharvaris highlighted that abstracts on deucrictibant, including its safety, efficacy, and biomarker data, were accepted for presentation at major angioedema congresses. This reflects growing scientific and clinical interest in novel oral therapies for BMA

- In February 2025, garadacimab, a monoclonal antibody targeting activated factor XIIa to reduce bradykinin production, was approved in the European Union for once-monthly prophylactic treatment of HAE. This offered patients a convenient and long-acting preventive option

- In July 2025, the U.S. FDA approved sebetralstat, an oral plasma kallikrein inhibitor, as the first oral on-demand therapy for acute HAE attacks in patients aged 12 or older. This approval expanded the treatment landscape with a non-injectable, patient-friendly option

- In August 2025, the FDA approved donidalorsen, a subcutaneous antisense oligonucleotide targeting prekallikrein mRNA, for prophylactic prevention of HAE attacks, offering a new mechanism of action for long-term disease management

- In March 2024, BioCryst announced promising proof-of-concept results from their ALPHA-STAR Phase 1b/2 trial of STAR-0215, a long-acting kallikrein inhibitor, which showed up to a 96% reduction in moderate to severe monthly attacks, highlighting progress in long-acting therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.