Global Brugada Syndrome Treatment Market

Market Size in USD Billion

USD

1.35 Billion

USD

2.08 Billion

2025

2033

USD

1.35 Billion

USD

2.08 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.35 Billion | |

| USD 2.08 Billion | |

| % | |

|

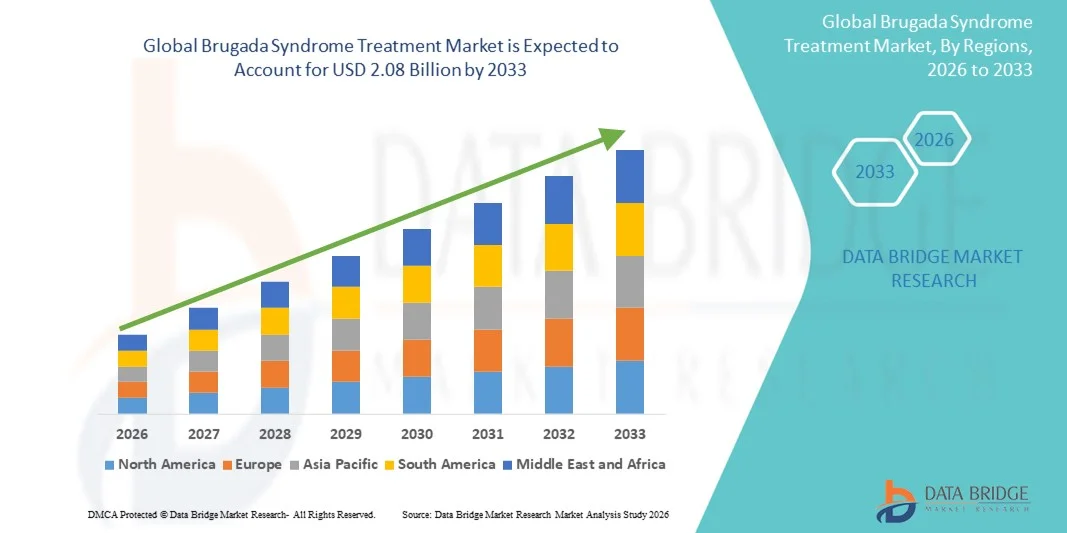

Brugada Syndrome Treatment Market Size

- The global Brugada Syndrome Treatment market size was valued at USD 1.35 billion in 2025 and is expected to reach USD 2.08 billion by 2033, at a CAGR of 5.60% during the forecast period

- The market growth is largely fueled by increasing advancements in cardiac diagnostics and treatment technologies, including improved ECG screening, next-generation electrophysiology systems, and expanded adoption of implantable cardioverter-defibrillators (ICDs), leading to better identification and management of Brugada Syndrome across hospitals and specialty cardiac centers

- Furthermore, rising awareness of inherited cardiac arrhythmias, growing access to genetic testing, and the demand for early-stage risk stratification are establishing Brugada Syndrome treatment solutions as essential components of modern cardiovascular care. These converging factors are accelerating the uptake of Brugada Syndrome Treatment solutions, thereby significantly boosting the industry's growth

Brugada Syndrome Treatment Market Analysis

- Brugada Syndrome Treatment, which includes diagnostic assessments, risk-stratification tools, and therapeutic interventions such as implantable cardioverter-defibrillators (ICDs) and antiarrhythmic medications, is becoming increasingly vital in cardiology due to rising awareness of inherited arrhythmias, improvements in early diagnosis, and advancements in genetic testing and electrophysiology technologies

- The escalating demand for Brugada Syndrome Treatment is primarily fueled by the increasing incidence of sudden cardiac death cases, growing availability of specialized cardiovascular centers, and a rising preference for early intervention through advanced diagnostic tools, family screening programs, and long-term cardiac monitoring solutions

- North America dominated the brugada syndrome treatment market with the largest revenue share of 40.8% in 2025, characterized by strong healthcare infrastructure, high awareness of arrhythmic disorders, significant adoption of ICD therapy, and the presence of leading cardiac device manufacturers. The U.S. experienced substantial growth in Brugada Syndrome diagnosis and treatment, driven by expanded genetic testing programs, improved clinical management guidelines, and increased focus on preventing sudden cardiac arrest

- Asia-Pacific is expected to be the fastest-growing region in the brugada syndrome treatment market during the forecast period, driven by growing healthcare modernization, rising prevalence of inherited cardiac conditions, increased investment in electrophysiology labs, and expanding awareness programs across countries such as Japan, China, India, and South Korea

- The Oral segment dominated the market with a 61.3% share in 2025, owing to the widespread preference for long-term oral antiarrhythmic therapy

Report Scope and Brugada Syndrome Treatment Market Segmentation

|

Attributes |

Brugada Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Brugada Syndrome Treatment Market Trends

Growing Research Focus and Advancements in Genetic & Molecular Diagnostics

- A significant and accelerating trend in the global brugada syndrome treatment market is the rapid expansion of research focused on genetic mutation identification, electrophysiological biomarkers, and advanced molecular diagnostic tools. These innovations are improving early detection accuracy and guiding patient-specific therapeutic decisions

- For instance, ongoing advancements in SCN5A gene mutation screening have made risk stratification more precise, helping clinicians better predict arrhythmic events and sudden cardiac arrest risk in suspected Brugada Syndrome patients

- AI-driven algorithms in ECG interpretation are being adopted in clinical settings to enhance diagnostic accuracy for subtle or intermittent Brugada patterns. These tools help detect high-risk abnormalities earlier than traditional ECG interpretation

- New electrophysiology (EP) lab technologies are enabling more detailed mapping of ventricular arrhythmogenic substrates, improving outcomes in catheter ablation procedures

- Clinical research organizations and major cardiac institutes are increasingly collaborating to standardize diagnostic protocols, improving global consistency and reducing misdiagnosis rates

- The fast-paced integration of molecular diagnostics, enhanced ECG analytics, and EP innovations is reshaping clinician expectations and shifting treatment pathways toward early, precision-based intervention

Brugada Syndrome Treatment Market Dynamics

Driver

Rising Prevalence of Arrhythmias and Growing Focus on Sudden Cardiac Death Prevention

- Increasing incidence of ventricular arrhythmias and heightened global awareness of sudden cardiac death (SCD) risk are major factors driving the demand for Brugada Syndrome Treatment solutions

- For instance, in February 2025, leading cardiovascular research groups reported expanded screening programs for high-risk families, improving early identification and treatment uptake

- As more patients undergo routine ECGs and genetic testing, earlier detection increases the number of individuals requiring treatment or monitoring

- Growing use of implantable cardioverter-defibrillators (ICDs) for high-risk patients is significantly contributing to market growth

- Hospitals are adopting updated clinical guidelines that encourage proactive screening, electrophysiological testing, and preventative therapy in suspected Brugada Syndrome cases

- Rising public health initiatives, patient awareness programs, and cardiology department expansions are collectively boosting treatment adoption across developed and developing healthcare systems

Restraint/Challenge

High Treatment Costs and Limited Awareness in Developing Regions

- The high cost of advanced electrophysiology procedures, genetic testing, and ICD implants presents a major barrier, especially in low- and middle-income regions

- Limited availability of specialized electrophysiology labs and trained cardiologists in certain countries delays diagnosis and treatment

- For instance, several public health reports in 2024 highlighted that many patients in rural areas remain undiagnosed due to lack of access to ECG technology and expert interpretation

- Misinterpretation of Brugada ECG patterns remains common, contributing to delayed or incorrect treatment planning

- In addition, limited insurance coverage for ICD implantation or genetic testing increases the financial burden on patients

- Addressing these challenges through awareness programs, clinician training, healthcare infrastructure development, and policy support will be essential for improving global treatment access

Brugada Syndrome Treatment Market Scope

The market is segmented on the basis of treatment, dosage, route of administration, diagnosis, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Brugada Syndrome Treatment market is segmented into Implantable cardioverter-defibrillator (ICD) and Drug Therapy. The ICD segment dominated the largest market revenue share of 64.8% in 2025, primarily due to its proven clinical effectiveness in preventing sudden cardiac death in high-risk Brugada Syndrome patients. ICDs remain the gold-standard intervention because they can detect and terminate life-threatening ventricular arrhythmias, offering immediate protection and reducing mortality. Growing adoption of ICD implantation guidelines, increased availability of advanced cardiac electrophysiology units, and rising diagnosis rates of inherited arrhythmia syndromes also strengthen segment dominance. Expansion of reimbursement policies and rising healthcare expenditure in developed nations further accelerate ICD utilization. Continuous improvements in device longevity, shock optimization systems, and remote monitoring capabilities are enhancing patient outcomes. The availability of subcutaneous ICDs (S-ICDs), which minimize surgical complications, is also boosting adoption. Increasing awareness of arrhythmia-related risks and proactive preventive care in cardiology centers solidifies ICDs’ leading position.

The Drug Therapy segment is projected to witness the fastest CAGR of 9.6% from 2026 to 2033, driven by increasing clinical acceptance of antiarrhythmic medications such as quinidine, which reduce arrhythmic events in selected patients. Growing research on pharmacological agents that modulate cardiac sodium channels is expanding therapeutic potential for patients unable or unwilling to undergo ICD implantation. Rising demand for non-invasive management, especially in early-stage or lower-risk patients, supports strong growth. Drug therapy adoption is also rising in regions with limited electrophysiology infrastructure where ICD access remains restricted. Increasing focus on combination therapy with electrophysiological monitoring, ongoing clinical trials evaluating novel antiarrhythmic molecules, and cost-effectiveness compared to surgical options contribute to its expansion. Improved distribution networks and rising physician awareness about pharmacological alternatives are also accelerating segment growth.

- By Dosage

On the basis of dosage, the Brugada Syndrome Treatment market is segmented into Tablet, Solution, and Others. The Tablet segment held the largest market revenue share of 57.4% in 2025, primarily due to the widespread use of oral antiarrhythmic medications in long-term management. Tablets offer convenient administration, improved patient compliance, cost-effective chronic therapy, and simpler distribution compared to injectable forms. Their dominance is strengthened by rising use of quinidine tablets, which remain the primary pharmacological option for Brugada patients who require arrhythmia suppression or who experience ICD shocks. Tablets are also preferred for outpatient treatment setups and long-term follow-ups. Expanded availability of generics, supportive regulatory frameworks, and increasing prescribing trends of oral medications ensure continued leadership. Growth in telemedicine consultations that favor oral therapy further supports segment expansion.

The Solution segment is projected to witness the fastest CAGR of 8.8% from 2026 to 2033, driven by increasing use of intravenous antiarrhythmic agents in emergency departments and critical care units for managing acute arrhythmic episodes. Solutions ensure rapid onset of action, precise dose control, and high bioavailability, making them essential for urgent stabilization. Increasing adoption in hospital settings, rising incidence of Brugada-related cardiac events, and advancements in intravenous drug formulations contribute to strong growth. Expanded critical care infrastructure and higher cardiology department capacity in emerging nations further drive demand.

- By Route of Administration

On the basis of route of administration, the Brugada Syndrome Treatment market is segmented into Oral, Intravenous, and Other. The Oral segment dominated the market with a 61.3% share in 2025, owing to the widespread preference for long-term oral antiarrhythmic therapy. Oral administration supports better adherence, flexible dosing, and cost-effectiveness, making it the most commonly prescribed route for chronic management. The dominance is further strengthened by improved access to oral medications, rising patient awareness, and the expanding global pharmaceutical supply chain. Oral drugs remain central to maintenance therapy post-diagnosis, especially for patients monitored remotely or managed through outpatient care.

The Intravenous segment is projected to grow at the fastest CAGR of 9.2% from 2026 to 2033, driven by increasing hospitalization rates for acute arrhythmia management. Intravenous administration provides rapid therapeutic response, making it essential for emergency care. Growth is supported by the expansion of cardiac emergency units, increased adoption of EP testing requiring controlled drug infusions, and rising availability of advanced cardiac life support systems. In addition, the increasing use of IV antiarrhythmic drugs in perioperative care is further accelerating demand. The growing emphasis on rapid stabilization protocols for high-risk Brugada patients is also strengthening the segment's adoption. Moreover, wider integration of IV-based monitoring systems in emergency departments is contributing to sustained market growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Electrocardiogram (ECG), Electrophysiology (EP) Test, Genetic Testing, and Others. The Electrocardiogram (ECG) segment dominated with a 48.7% share in 2025, as ECG remains the primary and most accessible diagnostic tool for identifying Brugada patterns. Its non-invasive nature makes it widely suitable for both emergency and routine evaluations. ECGs provide immediate results, helping clinicians detect hallmark ST-segment elevation associated with Brugada Syndrome. The widespread availability of ECG machines in hospitals, clinics, and even mobile health units strengthens usage rates. Increasing global screening initiatives for inherited arrhythmia disorders further boost segment demand. Growing physician awareness and improved clinical training contribute to accurate interpretation. Technological advancements, including AI-supported ECG reading systems, enhance diagnostic accuracy and early detection. Preventive cardiology programs often begin with ECG screening, increasing adoption. Governments and health organizations promote ECG-based mass screening, especially in high-incidence regions. Reimbursement support for cardiovascular diagnostics encourages higher utilization. Continuous upgrade of ECG devices with digital connectivity and cloud-based storage promotes seamless patient monitoring. Overall, ECG remains indispensable due to reliability, accessibility, and cost-effectiveness.

The Genetic Testing segment is projected to witness the fastest CAGR of 10.4% from 2026 to 2033, driven by rising identification of SCN5A and other associated gene mutations. Growing demand for precision medicine and personalized treatment planning fuels rapid adoption. Genetic testing enables early diagnosis among asymptomatic family members, supporting preventive intervention. Increasing availability of next-generation sequencing (NGS) panels enhances detection accuracy. Falling genetic testing prices make it more accessible to broader populations. Hospitals and cardiology centers are integrating genetic counseling with screening programs, increasing uptake. Research advancements uncovering new pathogenic variants strengthen test utility. Expansion of molecular diagnostic labs in emerging economies promotes growth. Rising patient awareness regarding inherited cardiac disorders contributes significantly to demand. Genetic testing also supports risk stratification, helping clinicians determine need for ICD therapy. Pharmaceutical developments targeting gene-specific pathways further elevate relevance. Overall, expanding clinical guidelines and improved accessibility support strong growth.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment dominated with a 69.1% market share in 2025, due to extensive infrastructure required for Brugada Syndrome management. Hospitals house electrophysiology (EP) labs essential for diagnostic testing and arrhythmia mapping. They provide specialized cardiology units capable of performing ICD implantation procedures. Emergency departments equipped with advanced life-support systems allow immediate intervention during ventricular arrhythmias. Hospitals also manage inpatient monitoring for high-risk Brugada patients. Increased hospital admissions due to sudden cardiac events strengthen segment leadership. Growing availability of cardiac specialists and EP-trained physicians boosts treatment efficacy. Government funding to expand tertiary cardiac care centers supports dominance. Hospitals are often the first point of diagnosis for symptomatic individuals, increasing patient flow. Access to sophisticated diagnostic systems such as programmed electrical stimulation (PES) enhances capabilities. Integration of multidisciplinary care teams improves outcomes and drives preference. Strong reimbursement support for hospital-based cardiac diagnostics and procedures further reinforces segment dominance.

The Clinic segment is projected to experience the fastest CAGR of 7.9% from 2026 to 2033, driven by rising outpatient consultations and follow-up care requirements. Clinics increasingly conduct routine ECG screenings, enabling early detection of Brugada patterns. Growing preference for cost-effective and convenient cardiac evaluation attracts more patients. Expansion of specialty cardiology clinics improves access in urban and semi-urban regions. Follow-up visits for monitoring ICD performance or medication adherence also boost clinic utilization. Clinics provide long-term management for stable Brugada patients, easing hospital burden. Improved availability of digital ECG systems enables point-of-care diagnostics. Telecardiology consultations offered through clinics also enhance reach. As patient awareness rises, more individuals seek periodic checkups, strengthening demand. Clinics often act as referral hubs for hospitals, increasing their strategic role in the care continuum. Lower waiting times compared to hospitals improve patient satisfaction. Growing private-sector healthcare investment expands clinic infrastructure across developing regions.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated with 54.6% share in 2025, supported by centralized distribution of Brugada-related medications and emergency drugs. Hospital pharmacies dispense drugs required during ICD implantation and post-operative recovery. They also ensure availability of antiarrhythmic agents for inpatients experiencing acute arrhythmic episodes. Strong coordination with cardiology and EP departments enhances treatment continuity. Hospital pharmacies maintain high inventory levels of essential medications to support critical care. Integration with electronic medical record (EMR) systems ensures accurate dispensing and monitoring. Rising hospitalization rates for arrhythmia-related events further increase distribution volume. Hospitals also manage controlled medications used in EP testing. Reimbursement-linked drug dispensing boosts hospital pharmacy utilization. Hospitals participate in bulk procurement agreements, reducing drug costs and ensuring continuous supply. The presence of trained clinical pharmacists improves medication safety and counseling. Overall, hospital pharmacies remain the primary distribution point for complex cardiac medications.

The Online Pharmacy segment is expected to see the fastest CAGR of 9.7% from 2026 to 2033, driven by rising digital health adoption and greater reliance on long-term medication therapy. Online pharmacies offer convenience through doorstep delivery of chronic medications needed for Brugada Syndrome management. Rising use of mobile apps and e-prescriptions supports steady growth. Patients benefit from subscription-based refill systems, reducing missed doses. Competitive pricing and discount programs attract cost-sensitive users. Online pharmacies ensure availability of hard-to-find antiarrhythmic drugs, especially in remote areas. Improved regulatory frameworks enhance consumer trust. Expansion of telemedicine platforms strengthens integration between online consultation and medicine delivery. Growing acceptance among elderly and chronic patients boosts demand. Enhanced cold-chain management in e-pharmacy logistics ensures drug quality. Increased investment in digital pharmacy infrastructure across Asia-Pacific supports rapid expansion.

Brugada Syndrome Treatment Market Regional Analysis

- North America dominated the brugada syndrome treatment market with the largest revenue share of 40.8% in 2025, supported by strong healthcare infrastructure, advanced electrophysiology capabilities, and widespread availability of cardiac monitoring technologies

- The region benefits from high awareness of arrhythmic disorders, significant clinical adoption of implantable cardioverter-defibrillators (ICDs), and well-established emergency care systems for managing sudden cardiac arrest

- The rising emphasis on genetic testing, improved risk-stratification guidelines, and early diagnosis initiatives further strengthen market growth, particularly across tertiary cardiac centers

U.S. Brugada Syndrome Treatment Market Insight

The U.S. brugada syndrome treatment market accounted for 81% of the North America market revenue in 2025, driven by strong reimbursement frameworks for ICD implantation, large patient pools undergoing electrophysiology evaluations, and the presence of key cardiac device manufacturers. Growing adoption of next-generation ICDs, advanced EP mapping systems, and increasing integration of artificial intelligence in arrhythmia detection have accelerated the U.S. Brugada Syndrome Treatment market.

Europe Brugada Syndrome Treatment Market Insight

The Europe brugada syndrome treatment market is projected to grow at a substantial CAGR during the forecast period, supported by increasing awareness of sudden cardiac death prevention, expansion of electrophysiology labs, and rising adoption of guideline-based intervention for inherited cardiac disorders. European countries are increasingly focusing on early diagnosis through ECG screening, EP tests, and genetic testing, while rising investments in hospital infrastructure and clinical research on arrhythmias further support growth.

U.K. Brugada Syndrome Treatment Market Insight

The U.K. brugada syndrome treatment market is anticipated to grow at a noteworthy CAGR, backed by national initiatives to improve cardiac care, rising emphasis on hereditary disease screening, and increasing availability of specialized arrhythmia clinics. Growing focus on early identification of high-risk patients and adoption of ICD therapy for sudden cardiac arrest prevention is strengthening market expansion.

Germany Brugada Syndrome Treatment Market Insight

Germany brugada syndrome treatment market is expected to register considerable CAGR growth, driven by a well-developed healthcare system, strong emphasis on clinical innovation, and high adoption of advanced cardiac devices. The country’s robust electrophysiology infrastructure and increasing demand for minimally invasive cardiac procedures contribute significantly to the Brugada Syndrome Treatment market.

Asia-Pacific Brugada Syndrome Treatment Market Insight

The Asia-Pacific brugada syndrome treatment market is projected to grow at the fastest CAGR during 2026–2033, fueled by rapid healthcare modernization, rising prevalence of inherited arrhythmias, and increasing investments in EP labs across Japan, China, India, and South Korea. Growing government initiatives for cardiac screening, greater awareness of sudden cardiac arrest, and rising access to advanced diagnostic tools are driving the adoption of Brugada Syndrome therapies, especially ICDs.

Japan Brugada Syndrome Treatment Market Insight

Japan’s brugada syndrome treatment market is gaining strong momentum due to high technological adoption, expanding use of advanced ECG and EP diagnostic systems, and growing emphasis on hereditary disease management. The country’s aging population and focus on early cardiac risk detection contribute to rising demand for Brugada Syndrome treatment solutions.

China Brugada Syndrome Treatment Market Insight

China brugada syndrome treatment market captured the largest market revenue share in Asia-Pacific in 2025, supported by rapid healthcare digitalization, growing middle-class awareness of cardiac health, and strong domestic manufacturing of cardiac monitoring and diagnostic devices. Government-led cardiac screening initiatives, expansion of electrophysiology departments, and increased adoption of ICD therapy are key growth drivers.

Brugada Syndrome Treatment Market Share

The Brugada Syndrome Treatment industry is primarily led by well-established companies, including:

• Medtronic (Ireland)

• Abbott (U.S.)

• Boston Scientific (U.S.)

• Biotronik (Germany)

• Philips Healthcare (Netherlands)

• GE Healthcare (U.S.)

• Johnson & Johnson (U.S.)

• LivaNova (U.K.)

• MicroPort Scientific (China)

• Sorin Group (Italy)

• Schiller AG (Switzerland)

• Spacelabs Healthcare (U.S.)

• Imricor Medical Systems (U.S.)

• CardioFocus (U.S.)

Latest Developments in Global Brugada Syndrome Treatment Market

- In April 2025, a large international registry reported new evidence supporting the safety and effectiveness of Subcutaneous Implantable Cardioverter-Defibrillators (S-ICDs) in Brugada Syndrome patients, demonstrating reduced complications and lower inappropriate shock rates, strengthening global adoption of S-ICDs for long-term arrhythmia prevention

- In January 2024, experts published a clinical guidance update emphasizing improved risk-stratification and genetic diagnostics for Brugada Syndrome, highlighting the importance of distinguishing true Brugada Syndrome from phenocopies and expanding the clinical use of genetic testing for treatment decisions

- In September 2023, a major review highlighted renewed clinical use of quinidine therapy for preventing ventricular arrhythmias in Brugada Syndrome patients, citing improved global availability and expanding its use among individuals unsuitable for ICD implantation

- In May 2023, advancements in epicardial radiofrequency ablation were reported, showing enhanced mapping and ablation techniques that significantly reduce ventricular fibrillation recurrence in Brugada Syndrome patients, strengthening ablation as an emerging treatment option

- In February 2022, new clinical data from the ongoing BRAVE Trial confirmed the potential of preventive epicardial substrate ablation to reduce life-threatening arrhythmic events in high-risk Brugada Syndrome patients, reinforcing the role of ablation alongside ICD therapy

- In July 2021, updated diagnostic algorithms integrating high-resolution ECG analysis and expanded genetic mutation screening were introduced, improving early detection of Brugada Syndrome and helping clinicians better select patients for ICD implantation and drug therapy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.