Global Bulk Bag Divider Market

Market Size in USD Billion

USD

6.20 Billion

USD

9.30 Billion

2025

2033

USD

6.20 Billion

USD

9.30 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 6.20 Billion |

Market Size (Forecast Year) |

USD 9.30 Billion |

CAGR |

% |

Major Markets Players |

|

Bulk Bag Divider Market Overview

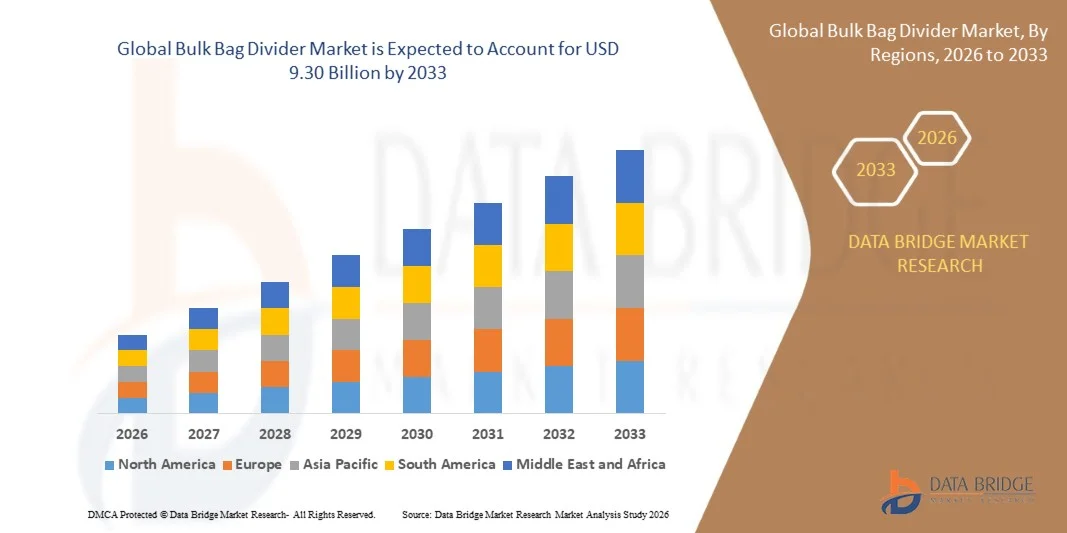

The Bulk Bag Divider Market was valued at USD 6.20 billion in 2025 and is projected to reach USD 9.30 billion by 2033, growing at a CAGR of 5.20% from 2026 to 2033. The market is witnessing steady expansion driven by increasing demand for efficient bulk material handling systems, rising adoption of standardized industrial packaging solutions, and growing focus on safe, contamination-free storage and transportation across logistics-intensive industries.

The expansion of global supply chains, coupled with rising industrialization in emerging economies, is significantly boosting the use of bulk bag divider systems across chemicals, agriculture, food and beverage, and warehousing sectors. In addition, increasing emphasis on operational efficiency, space optimization, and cost-effective packaging solutions is encouraging manufacturers and logistics operators to adopt advanced divider configurations within bulk bags. Growing investments in automated warehousing systems and export-oriented manufacturing are further strengthening market growth across developed and developing regions.

Key Market Trends & Insights

- North America dominated the bulk bag divider market with the largest revenue share of 38.7% in 2025, supported by a well-established logistics infrastructure, strong industrial packaging demand, and high adoption of advanced bulk handling systems across chemicals, agriculture, and warehousing applications.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 6.4% from 2026 to 2033. Growth is driven by rapid industrialization, expanding agricultural production, increasing export-oriented manufacturing, and rising investments in logistics and supply chain infrastructure across emerging economies such as China and India.

- The Plastic segment held the largest market revenue share of approximately 58.4% in 2025 driven by its lightweight structure, high durability, cost-effectiveness, and wide compatibility with flexible bulk packaging systems used in logistics and storage operations. Plastic-based dividers are widely preferred in industries such as chemicals, agriculture, and food handling due to their resistance to moisture and ease of integration within bulk bags.

- The Paper segment accounted for around 12.3% share, supported by rising demand for eco-friendly and recyclable packaging solutions in retail and food applications. It is increasingly preferred in industries focused on sustainability targets and reduced plastic usage across supply chains. Growing regulatory pressure on single-use plastics is further encouraging adoption of paper-based divider solutions in bulk packaging systems. In addition, advancements in moisture-resistant and coated paper materials are improving durability and expanding application scope. The segment is also gaining traction in cost-sensitive markets where lightweight packaging is prioritized.

- The Block segment held the largest market revenue share of approximately 52.6% in 2025 driven by its superior load stability, ease of stacking, and widespread adoption in bulk material handling across agriculture, chemicals, and warehousing applications. Block-style dividers are preferred for standardized bulk bag configurations due to their structural strength and uniform load distribution

- The Stringer segment accounted for around 31.8% share supported by its flexible design and suitability for intermediate load applications in transportation and storage operations. It offers improved adaptability in bulk bag configurations, making it suitable for varied industrial packaging requirements. Rising demand for efficient load stabilization in logistics and warehousing is boosting its adoption across supply chains. Stringer designs also help optimize space utilization during storage and transit, reducing handling costs. Furthermore, increasing use in export-oriented packaging operations is supporting steady segment growth.

- The Chemicals segment held the largest market revenue share of approximately 24.5% in 2025 driven by extensive use of bulk packaging systems for safe handling and transport of powders, granules, and industrial raw materials.

- The Agriculture and Allied Products segment accounted for around 18.2% share supported by large-scale storage and distribution of grains, fertilizers, and seeds. The segment benefits from the growing need for safe and contamination-free bulk handling in agricultural supply chains. Expanding global food demand and increasing mechanization in farming practices are further driving usage of bulk bag divider systems. These dividers help maintain product integrity during long-distance transportation and storage. In addition, rising investments in agri-logistics infrastructure in emerging economies are strengthening segment adoption.

Market Size & Forecast

- Global Market Value (2025): USD 6.20 Billion

- Expected Market Value (2033): USD 9.30 Billion

- Forecast CAGR (2026–2033): 5.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Bulk Bag Divider Market Segmentation

|

Attributes |

Bulk Bag Divider Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• A and M Jumbo Bags (India) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Bulk Bag Divider Market Trends

Trend: Growth In Safe Bulk Handling And Advanced Load Stabilization Solutions

Increasing demand for efficient, safe, and contamination-free bulk material handling systems across agriculture, chemicals, food processing, construction, and mining industries is driving the adoption of bulk bag dividers. Traditional bulk storage methods often face challenges such as bag deformation, uneven load distribution, and product contamination, encouraging industries to adopt divider-based stabilization systems that improve structural integrity and handling efficiency.

In chemical and mineral packaging, bulk bag dividers are increasingly used to separate layered materials within FIBC bags, For instance in mining operations in Australia and Chile where bulk ores are transported over long distances requiring stable load distribution to prevent shifting and material loss. In the food processing industry, these dividers are being used to separate powdered ingredients such as flour, sugar, and starch within bulk containers to maintain product purity and reduce cross-contamination risks during transportation and storage.

The expansion of global trade in bulk commodities and increasing demand for export-grade packaging solutions is also supporting adoption, particularly in Asia-Pacific where large-scale agricultural exports such as grains, rice, and fertilizers require secure and stable bulk packaging systems. In addition, increasing automation in packaging lines is accelerating the integration of structured divider systems that enhance stacking efficiency and warehouse optimization.

Bulk Bag Divider Market Dynamics

Key Market Driver: Rising Demand For Efficient And Safe Bulk Material Handling

Industries worldwide are facing increasing pressure to improve logistics efficiency, reduce product loss, and enhance safety during storage and transportation of bulk materials. Bulk bag dividers help maintain compartmentalization inside FIBC bags, reducing shifting loads and improving structural stability during handling and shipping operations.

Industries such as agriculture, chemicals, construction, and food processing are increasingly adopting bulk bag dividers, For instance in fertilizer packaging facilities in India and Brazil where large volumes of granular products are stored and transported in flexible intermediate bulk containers requiring improved stability and reduced leakage risk.

The growing global trade of bulk commodities is also driving adoption, with increasing exports of grains, cement, and powdered chemicals requiring standardized packaging solutions. Industrial logistics studies in 2024 across European distribution hubs indicated that structured bulk bag systems reduced material loss by nearly 12–18% during long-haul transportation compared to conventional bulk packaging methods.

Key Restraint/Challenge: Limited Standardization And Compatibility Issues With Existing Packaging Systems

Despite operational advantages, bulk bag dividers face challenges related to lack of standardized designs and limited compatibility with different FIBC bag configurations. Variations in bag size, load capacity, and material type often require customized divider solutions, increasing complexity for manufacturers and end users.

In addition, additional manufacturing steps and material costs associated with reinforced divider systems increase overall packaging expenses, making adoption less attractive for low-margin industries such as agriculture and commodity trading. Limited awareness among small and medium-scale packaging operators further restricts widespread implementation in emerging markets.

Industry evaluations indicate that customized bulk bag divider systems can increase overall packaging costs by approximately 15–25% compared to standard FIBC bags, creating cost sensitivity issues in price-competitive bulk logistics operations.

Key Market Opportunity: Expansion In Automated Warehousing And Export-Oriented Bulk Logistics

Rising automation in warehousing, increasing global commodity trade, and expansion of export-oriented agricultural and industrial supply chains are creating strong opportunities for bulk bag divider manufacturers. Growing demand for efficient stacking, reduced product loss, and improved warehouse optimization is driving adoption in large-scale logistics operations.

Logistics companies are increasingly using bulk bag dividers, For instance in grain export terminals in the U.S. and Ukraine where structured bulk packaging systems are used to improve handling efficiency and reduce spoilage during long-duration storage and transport cycles.

In addition, increasing investment in smart warehouses and automated packaging systems in Asia-Pacific is accelerating demand for advanced bulk handling solutions. Pilot logistics programs in 2025 across China and India reported up to 20% improvement in storage efficiency and reduced material shifting after integrating structured divider-based bulk packaging systems in automated supply chains.

Bulk Bag Divider Market Scope

The market is segmented on the basis of model, type, functionality, offering, and end-use application.

• By Material Type

On the basis of material type, the Bulk Bag Divider Market is segmented into Plastic, Paper, Metal, Stainless Steel, Aluminum, Tinplate, and Others. The Plastic segment held the largest market revenue share of approximately 58.4% in 2025 driven by its lightweight structure, high durability, cost-effectiveness, and wide compatibility with flexible bulk packaging systems used in logistics and storage operations. Plastic-based dividers are widely preferred in industries such as chemicals, agriculture, and food handling due to their resistance to moisture and ease of integration within bulk bags.

The Paper segment accounted for around 12.3% share, supported by rising demand for eco-friendly and recyclable packaging solutions in retail and food applications. It is increasingly preferred in industries focused on sustainability targets and reduced plastic usage across supply chains. Growing regulatory pressure on single-use plastics is further encouraging adoption of paper-based divider solutions in bulk packaging systems. In addition, advancements in moisture-resistant and coated paper materials are improving durability and expanding application scope. The segment is also gaining traction in cost-sensitive markets where lightweight packaging is prioritized.

• By Structure Design

On the basis of structure design, the market is segmented into Block, Stringer, and Customized. The Block segment held the largest market revenue share of approximately 52.6% in 2025 driven by its superior load stability, ease of stacking, and widespread adoption in bulk material handling across agriculture, chemicals, and warehousing applications. Block-style dividers are preferred for standardized bulk bag configurations due to their structural strength and uniform load distribution

The Stringer segment accounted for around 31.8% share supported by its flexible design and suitability for intermediate load applications in transportation and storage operations. It offers improved adaptability in bulk bag configurations, making it suitable for varied industrial packaging requirements. Rising demand for efficient load stabilization in logistics and warehousing is boosting its adoption across supply chains. Stringer designs also help optimize space utilization during storage and transit, reducing handling costs. Furthermore, increasing use in export-oriented packaging operations is supporting steady segment growth.

• By End Use

On the basis of end use, the market is segmented into Pharmaceuticals, Chemicals, Textile and Handicraft, Agriculture and Allied Products, Electronics and Consumer Appliances, Transportation and Warehousing, Food and Beverage, Retail, and Others. The Chemicals segment held the largest market revenue share of approximately 24.5% in 2025 driven by extensive use of bulk packaging systems for safe handling and transport of powders, granules, and industrial raw materials.

The Agriculture and Allied Products segment accounted for around 18.2% share supported by large-scale storage and distribution of grains, fertilizers, and seeds. The segment benefits from the growing need for safe and contamination-free bulk handling in agricultural supply chains. Expanding global food demand and increasing mechanization in farming practices are further driving usage of bulk bag divider systems. These dividers help maintain product integrity during long-distance transportation and storage. In addition, rising investments in agri-logistics infrastructure in emerging economies are strengthening segment adoption.

Bulk Bag Divider Market Regional Analysis

North America Bulk Bag Divider Market Insight

North America dominated the Bulk Bag Divider Market with the largest revenue share of 38.7% in 2025, supported by a highly developed logistics infrastructure, strong industrial packaging demand, and increasing adoption of advanced bulk material handling systems. The region benefits from widespread use of bulk packaging solutions across chemicals, agriculture, food processing, and warehousing sectors. Companies in North America prioritize operational efficiency, product safety, and cost optimization, driving the adoption of high-performance bulk bag dividers. In addition, the presence of established manufacturing facilities and growing investments in automated supply chain systems further strengthen regional market dominance.

U.S. Bulk Bag Divider Market Insight

The U.S. bulk bag divider market captured the largest revenue share in 2025 within North America, driven by strong demand from chemicals, agriculture, and food & beverage industries. The country’s advanced warehousing and distribution networks support large-scale usage of bulk packaging systems for efficient storage and transportation. Increasing emphasis on product protection, contamination control, and supply chain optimization is accelerating adoption. Furthermore, rising industrial automation and expansion of e-commerce logistics operations are boosting the integration of standardized bulk bag divider solutions across multiple end-use sectors.

Europe Bulk Bag Divider Market Insight

The Europe Bulk Bag Divider Market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent sustainability regulations, increasing demand for recyclable packaging materials, and expanding industrial manufacturing activities. The region’s strong focus on circular economy practices is encouraging the use of eco-friendly bulk packaging components across multiple industries. Growth is also supported by rising investments in pharmaceutical, food processing, and chemical manufacturing sectors. Moreover, modernization of logistics infrastructure and adoption of standardized bulk handling systems are further contributing to market expansion.

U.K. Bulk Bag Divider Market Insight

The U.K. bulk bag divider market is expected to witness strong growth from 2026 to 2033, supported by increasing demand for efficient warehousing solutions and safe bulk material handling systems. Growing concerns regarding supply chain efficiency and packaging waste reduction are encouraging adoption across food, agriculture, and retail sectors. The expansion of e-commerce and third-party logistics services is further boosting demand for standardized bulk packaging components. In addition, technological advancements in packaging design and rising focus on operational safety are supporting market growth in the country.

Germany Bulk Bag Divider Market Insight

The Germany bulk bag divider market is expected to witness steady growth from 2026 to 2033, driven by strong industrial manufacturing capabilities and a high emphasis on precision engineering and sustainability. The country’s chemical, pharmaceutical, and automotive supply chains extensively utilize bulk packaging systems for safe material handling. Increasing adoption of automated logistics systems and eco-efficient packaging solutions is further enhancing market penetration. In addition, Germany’s regulatory focus on waste reduction and sustainable industrial practices is encouraging wider use of recyclable and durable divider materials.

Asia-Pacific Bulk Bag Divider Market Insight

The Asia-Pacific Bulk Bag Divider Market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding agricultural output, and growing logistics infrastructure in countries such as China, India, and Japan. Rising demand for cost-effective and efficient bulk packaging solutions is driving adoption across multiple industries. The region also benefits from increasing manufacturing activities and export-oriented trade expansion, which require standardized packaging systems. Furthermore, government initiatives supporting industrial modernization and supply chain efficiency are accelerating market growth.

Japan Bulk Bag Divider Market Insight

The Japan bulk bag divider market is expected to witness steady growth from 2026 to 2033, driven by high demand for precision packaging systems, advanced manufacturing practices, and strong focus on quality control. The country’s industrial sectors prioritize contamination-free and highly organized bulk material handling solutions. Increasing automation in logistics and warehousing is further supporting adoption of structured divider systems. Moreover, Japan’s emphasis on space optimization and efficient storage practices is encouraging the use of advanced bulk bag divider designs across industries.

China Bulk Bag Divider Market Insight

The China bulk bag divider market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid industrial expansion, large-scale agricultural production, and strong growth in chemical and manufacturing industries. The country’s extensive logistics network and export-oriented economy are driving significant demand for bulk packaging solutions. Increasing urbanization and infrastructure development are further boosting usage across warehousing and transportation sectors. In addition, the availability of cost-effective manufacturing capabilities and strong domestic production of packaging materials is supporting market expansion.

Bulk Bag Divider Market Share

The Bulk Bag Divider industry is primarily led by well-established companies, including:

• A and M Jumbo Bags (India)

• Schoeller Allibert (Netherlands)

• CABKA Group (Germany)

• Brambles (Australia)

• PalletOne (U.S.)

• Craemer Holding (Germany)

• Rehrig Pacific Company (U.S.)

• Innova Maquinaria Industrial (Spain)

• Amatech Inc. (U.S.)

• Corrugated Pallets Company (U.K.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Bulk Bag Divider Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Bulk Bag Divider Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Bulk Bag Divider Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.