Global Bunyavirus Infections Market

Market Size in USD Billion

USD

1.25 Billion

USD

1.83 Billion

2025

2033

USD

1.25 Billion

USD

1.83 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.25 Billion | |

| USD 1.83 Billion | |

| % | |

|

Bunyavirus Infections Market Overview

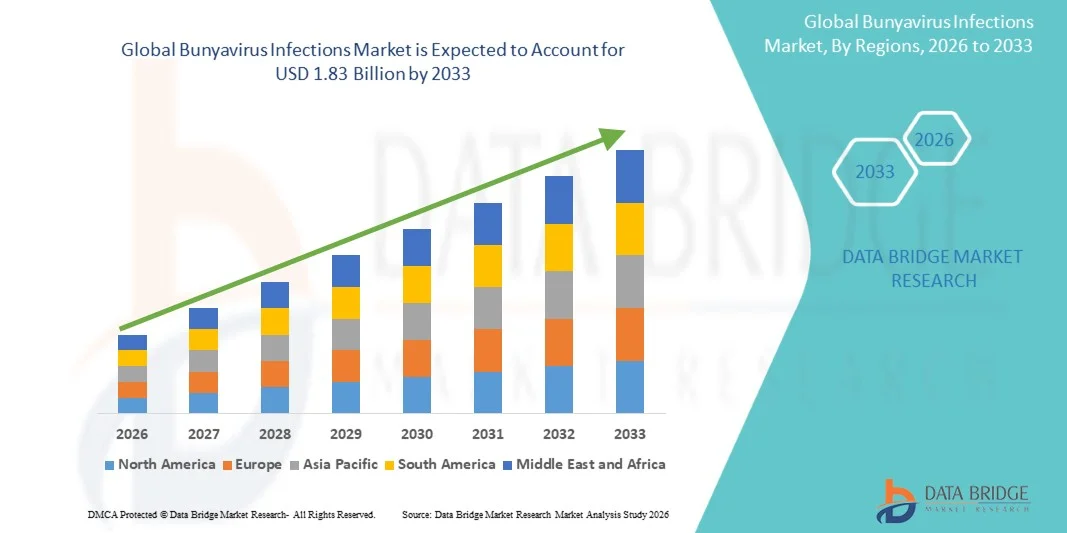

The Bunyavirus Infections Market was valued at USD 1.25 billion in 2025 and is projected to reach USD 1.83 billion by 2033, growing at a CAGR of 4.90% from 2026 to 2033. The market is witnessing steady growth driven by the rising prevalence of bunyavirus-associated diseases, increasing outbreaks of vector-borne infections, and expanding investments in infectious disease surveillance and antiviral research.

The growing global health burden of zoonotic and arthropod-borne viral infections, combined with enhanced diagnostic capabilities and improved epidemic preparedness programs, is accelerating market demand. Governments and healthcare organizations are strengthening early detection systems, vaccine development pipelines, and supportive care infrastructure, which is further contributing to market expansion. Additionally, advancements in molecular diagnostics, next-generation sequencing, and rapid point-of-care testing are improving identification and management of bunyavirus infections across endemic regions.

Key Market Trends & Insights

- North America dominated the Bunyavirus Infections Market with the largest revenue share of 36.5% in 2025, supported by strong infectious disease surveillance systems, advanced diagnostic infrastructure, and high healthcare expenditure

- The Hantavirus segment led the market with a 38.6% share in 2025, driven by its strong association with severe and frequently reported infections such as Hantavirus Pulmonary Syndrome and hemorrhagic fever-related renal complications.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 6.1% from 2026 to 2033, fueled by higher exposure to vector-borne diseases, expanding rural healthcare access, and rising government focus on epidemic preparedness.

- Phlebovirus are the fastest-growing genus type, projected to register a CAGR of 5.6%, reflecting the surge in Rift Valley fever and sandfly fever cases across Africa and the Middle East.

- The Hemorrhagic Fever segment dominated the disease type category with a 42.8% revenue share in 2025, led by its high severity, hospitalization rates, and outbreak-driven surveillance priority.

- Rodents accounted for 44.1% of the market, preferred by epidemiological surveillance programs, public health agencies, and infectious disease research institutions due to their role as the primary reservoir for hantavirus transmission.

- The Antiviral Drugs segment is the fastest-growing treatment category, with a CAGR of 6.2%, driven by increasing research into broad-spectrum antivirals targeting RNA viruses.

Market Size & Forecast

- Global Market Value (2025): USD 1.25 Billion

- Expected Market Value (2033): USD 1.83 Billion

- Forecast CAGR (2026–2033): 4.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Bunyavirus Infections Market Segmentation

|

Attributes |

Bunyavirus Infections Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Merck & Co., Inc. (U.S.) · Pfizer Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Roche Holding AG (Switzerland) · Abbott (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · Bio-Rad Laboratories, Inc. (U.S.) · Siemens Healthineers AG (Germany) · BD (U.S.) · QIAGEN (Germany) · Illumina, Inc. (U.S.) · GSK plc (U.K.) · Sanofi (France) · AstraZeneca (U.K.) · Moderna, Inc. (U.S.) · Emergent BioSolutions Inc. (U.S.) · Inovio Pharmaceuticals, Inc. (U.S.) · Regeneron Pharmaceuticals, Inc. (U.S.) · Takeda Pharmaceutical Company Limited (Japan) · Novavax, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of rapid point-of-care molecular diagnostics in endemic rural regions · Increasing public–private investment in broad-spectrum antiviral research platforms · Growing opportunity in integrated vector surveillance and predictive outbreak modeling systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Bunyavirus Infections Market Trends

Trend: Expansion of Advanced Molecular Surveillance & Outbreak Monitoring

Public health systems are increasingly adopting genomic sequencing and real-time molecular surveillance to detect bunyavirus outbreaks at earlier stages, enabling faster containment and epidemiological mapping of virus transmission patterns across endemic and high-risk regions. The integration of digital disease surveillance platforms is improving data sharing between laboratories, hospitals, and global health agencies, strengthening preparedness and response capabilities for emerging viral threats, while portable diagnostic tools are extending monitoring capacity into remote and resource-limited settings for faster intervention and control. For instance, enhanced sequencing networks during regional hemorrhagic fever outbreaks are improving early identification and strain tracking of bunyavirus species.

Bunyavirus Infections Market Dynamics

Key Market Driver: Rising Burden of Zoonotic and Vector-Borne Viral Outbreaks

The increasing incidence of bunyavirus-related infections driven by expanding vector habitats, climate variability, and human-animal interaction is significantly boosting demand for rapid diagnostics, surveillance systems, and supportive therapeutic solutions across both developed and developing healthcare systems. Governments and global health organizations are intensifying investments in epidemic preparedness, laboratory capacity expansion, and outbreak response frameworks, while pharmaceutical and biotech firms are accelerating antiviral research programs targeting high-risk hemorrhagic fever viruses. For instance, recurring Crimean-Congo hemorrhagic fever outbreaks in endemic regions are driving continuous demand for advanced diagnostic and containment strategies.

Key Restraint/Challenge: Limited Specific Therapeutic Options and Diagnostic Constraints

A major limitation in the bunyavirus infections market is the absence of widely approved virus-specific antiviral therapies, combined with challenges in early-stage diagnosis due to symptom overlap with other febrile illnesses, which often leads to delayed treatment and underreporting of cases. Additionally, dependence on specialized laboratory infrastructure for molecular testing restricts access in low-resource regions where bunyavirus outbreaks are more prevalent, thereby slowing timely intervention and disease management efforts. For instance, delayed confirmation of hantavirus infections in rural healthcare settings continues to hinder rapid outbreak response and containment efforts.

Key Market Opportunity: Expansion of Rapid Diagnostics and Integrated One-Health Surveillance Systems

The growing focus on point-of-care testing technologies and integrated One-Health surveillance frameworks presents a major opportunity for market expansion, enabling faster detection of zoonotic spillover events and improved coordination between human, animal, and environmental health monitoring systems. Increasing adoption of portable molecular diagnostic kits, AI-assisted outbreak prediction tools, and cross-border disease reporting networks is expected to significantly enhance early warning capabilities and response efficiency. For instance, mobile diagnostic deployment during rural outbreak investigations is improving early case detection and transmission control in high-risk regions.

Bunyavirus Infections Market Scope

The Bunyavirus Infections market is segmented on the basis of genus type, disease type, host, treatment, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel.

- By Genus Type

On the basis of genus type, the Bunyavirus Infections Market is segmented into Hantavirus, Nairovirus, Phlebovirus, and Orthobunyavirus. The Hantavirus segment dominated the market with the highest share of 38.6% in 2025, driven by its strong association with severe clinical conditions such as Hantavirus Pulmonary Syndrome (HPS) and Hemorrhagic Fever with Renal Syndrome (HFRS). This dominance is supported by higher diagnostic testing rates, increased awareness in endemic regions, and frequent outbreak reporting in Asia-Pacific and the Americas. Hospitals and reference laboratories prioritize hantavirus detection due to its high mortality risk and need for rapid intervention. Expanding use of PCR-based diagnostics and serological assays further strengthens its market position. Continuous surveillance programs in rodents also contribute to sustained detection rates. The segment remains central to global bunyavirus research and public health response systems.

The Phlebovirus segment is projected to be the fastest-growing at a CAGR of 5.6% from 2026 to 2033, driven by rising cases of sandfly fever and Rift Valley fever infections. Increasing climate change effects and vector expansion are enhancing transmission risk in new geographic regions. Improved diagnostic accessibility is enabling better identification of previously underreported infections. Growing investment in vaccine research for Rift Valley fever is also accelerating segment growth. Public health agencies are expanding vector surveillance programs targeting sandflies and mosquitoes. Additionally, rising travel-associated infections are contributing to global spread awareness. The segment is gaining traction due to its increasing epidemic potential in Africa and the Middle East.

- By Disease Type

On the basis of disease type, the market is segmented into California Encephalitis, Arboviral Encephalitis, Akabane Virus Infection, Rift Valley Fever Infections, Sandfly Fever, Hemorrhagic Fever, Hantavirus Pulmonary Syndrome (HPS), and CCHFV Infections. The Hemorrhagic Fever segment dominated the market with the highest share of 42.8% in 2025, due to its severe clinical outcomes, high hospitalization rates, and strong surveillance focus across endemic regions. Conditions such as CCHFV infections require intensive care and specialized diagnostic support, increasing healthcare utilization. Governments prioritize hemorrhagic fever control due to outbreak risks and high fatality rates. Laboratory testing and outbreak response funding are heavily concentrated in this segment. Clinical research and antiviral development efforts are also primarily focused here. The segment continues to dominate due to its critical public health impact.

The Rift Valley Fever Infections segment is expected to be the fastest-growing at a CAGR of 5.9% from 2026 to 2033, driven by increasing livestock outbreaks and zoonotic transmission risks. Expanding agricultural activities and climate-driven mosquito population growth are increasing infection incidence. International health agencies are strengthening surveillance in Africa and the Middle East. Vaccine development programs for both humans and animals are accelerating interest in this segment. Early warning systems and cross-border disease monitoring are improving case detection. Rising economic losses in livestock industries are further driving preventive investments. The segment is gaining momentum due to its epidemic and economic impact potential.

- By Host

On the basis of host, the market is segmented into mosquitoes, phlebotomine flies, ticks, culicoid flies, and rodents. The Rodents segment dominated the market with the highest share of 44.1% in 2025, as they are the primary reservoirs for hantavirus transmission globally. High rodent population density in rural and peri-urban areas significantly increases exposure risk. Environmental changes and urban expansion are enhancing human-rodent interactions. Public health surveillance programs frequently target rodent populations for early outbreak detection. Diagnostic testing in rodent carriers supports epidemiological tracking. The segment remains critical for understanding disease transmission cycles. Rodent control initiatives are widely implemented in endemic regions.

The Mosquitoes segment is projected to be the fastest-growing at a CAGR of 5.7% from 2026 to 2033, driven by expanding vector-borne disease transmission linked to climate change. Rising temperatures and humidity levels are increasing mosquito breeding habitats globally. Urbanization and poor sanitation are further contributing to vector proliferation. Mosquito-borne bunyavirus infections such as Rift Valley fever are gaining increased attention. Governments are investing in large-scale vector control programs and insecticide campaigns. Advancements in entomological surveillance are improving detection and control strategies. The segment is expanding due to rising global focus on vector-borne disease prevention.

- By Treatment

On the basis of treatment, the market is segmented into antiviral drugs, antihypotensive agents, fluid replacement, supportive therapy, surgery, and others. The Supportive Therapy segment dominated the market with the highest share of 46.3% in 2025, due to the lack of widely approved virus-specific antiviral treatments for bunyavirus infections. Clinical management primarily focuses on symptom relief, fluid management, and organ support in severe cases. Hospital admissions often require intensive care monitoring for hemorrhagic and respiratory complications. Supportive care remains the standard treatment across most endemic regions. Increasing ICU capacity and critical care infrastructure supports this segment. The segment continues to dominate due to limited curative treatment availability.

The Antiviral Drugs segment is expected to be the fastest-growing at a CAGR of 6.2% from 2026 to 2033, driven by increasing research into broad-spectrum antivirals targeting RNA viruses. Pharmaceutical companies are expanding pipelines focused on emerging infectious diseases. Rising outbreak frequency is accelerating clinical trials and regulatory interest. Governments are funding antiviral development programs for biodefense preparedness. Advances in drug repurposing and molecular targeting are improving development timelines. Increasing global collaboration in infectious disease research is strengthening this segment. The segment is expanding due to unmet therapeutic demand.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Blood Tests, Virus Isolation, PCR, Serologic Testing, and Others. The PCR segment dominated the market with the highest share of 49.7% in 2025, driven by its high sensitivity, accuracy, and ability to detect viral RNA in early infection stages. PCR is widely used in hospital laboratories and reference diagnostic centers. It plays a critical role in outbreak detection and confirmation. Increasing availability of automated PCR platforms is enhancing testing efficiency. Government-funded surveillance programs rely heavily on molecular diagnostics. The segment remains the gold standard for bunyavirus detection.

The Serologic Testing segment is expected to be the fastest-growing at a CAGR of 5.8% from 2026 to 2033, driven by increasing use in large-scale epidemiological screening. Serology is cost-effective and suitable for resource-limited settings. It enables detection of past infections and population-level immunity studies. Expanding deployment in rural healthcare systems is increasing accessibility. Rising awareness of zoonotic infections is boosting testing demand. Technological improvements in ELISA-based assays are enhancing accuracy. The segment is growing due to its scalability in public health surveillance.

- By Symptoms

On the basis of symptoms, the market is segmented into plasma viremia, neuronal necrosis, mild febrile illness, hemorrhagic manifestations, kidney failure, pulmonary edema, severe respiratory disease, and others. The Hemorrhagic Manifestations segment dominated the market with the highest share of 41.5% in 2025, due to its strong association with severe bunyavirus infections such as CCHFV and hantavirus-related hemorrhagic conditions. These symptoms often lead to rapid clinical deterioration, requiring intensive hospital care and emergency interventions. High mortality risk associated with hemorrhagic presentations drives priority diagnosis and treatment efforts. Hospitals and surveillance programs focus heavily on early detection of bleeding complications. Increased ICU admissions further reinforce its dominance. The segment remains central to outbreak response frameworks globally.

The Severe Respiratory Disease segment is projected to be the fastest-growing at a CAGR of 6.0% from 2026 to 2033, driven by rising incidence of hantavirus pulmonary syndrome and other respiratory complications. Increasing awareness of respiratory viral outbreaks is improving early clinical recognition. Expanding diagnostic imaging and oxygen therapy infrastructure supports better detection rates. Climate-linked rodent exposure is contributing to higher infection risk. Hospitals are increasingly reporting respiratory-driven bunyavirus cases in endemic and non-endemic regions. Research focus on pulmonary complications is accelerating clinical interest. The segment is growing due to rising respiratory infection surveillance globally.

- By Dosage

On the basis of dosage, the market is segmented into injection, tablets, and others. The Injection segment dominated the market with the highest share of 52.4% in 2025, driven by the clinical requirement for rapid drug delivery in severe bunyavirus infections. Hospitalized patients with hemorrhagic or respiratory complications require intravenous or injectable supportive therapies. Fluid replacement and emergency care are predominantly administered via injection routes. Injectable antivirals (where applicable) are preferred due to faster bioavailability. Critical care settings rely heavily on parenteral administration. The segment remains dominant due to acute disease severity and hospitalization needs.

The Tablets segment is projected to be the fastest-growing at a CAGR of 5.7% from 2026 to 2033, driven by increasing research into oral antiviral formulations and outpatient treatment models. Oral therapies improve accessibility in remote and low-resource settings. Pharmaceutical advancements are enabling better stability and bioavailability of antiviral compounds. Expanding outpatient infectious disease management supports tablet adoption. Governments are encouraging decentralized care to reduce hospital burden. Rising demand for early-stage treatment options is further supporting growth. The segment is expanding due to convenience and improving drug development pipelines.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, and others. The Intravenous segment dominated the market with the highest share of 55.8% in 2025, due to its critical role in managing severe and life-threatening bunyavirus infections. Hospitalized patients with hemorrhagic fever and organ failure require immediate systemic drug and fluid delivery. IV therapy enables rapid stabilization in intensive care units. Supportive treatments such as fluids, electrolytes, and antihypotensive agents are primarily administered intravenously. High hospitalization rates reinforce its dominance. The segment remains essential in acute infectious disease management.

The Oral segment is expected to be the fastest-growing at a CAGR of 5.5% from 2026 to 2033, driven by increasing focus on early-stage outpatient treatment and antiviral development. Oral administration improves patient compliance and accessibility. Advancements in drug formulation are enabling more effective oral antiviral candidates. Expansion of primary healthcare systems supports its adoption in rural regions. Governments are promoting non-hospital-based care to reduce healthcare burden. Rising awareness of early treatment benefits is further boosting demand. The segment is growing due to convenience and expanding therapeutic innovation.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, and others. The Hospitals segment dominated the market with the highest share of 58.9% in 2025, due to the requirement for advanced diagnostic, intensive care, and emergency treatment facilities. Severe bunyavirus infections often require hospitalization for monitoring and supportive care. Hospitals possess specialized laboratories for PCR and serological testing. High patient inflow during outbreaks strengthens hospital demand. Critical care units are essential for managing hemorrhagic and respiratory complications. Government funding for infectious disease preparedness further supports this segment. The segment remains the primary care setting for bunyavirus management.

The Clinics segment is projected to be the fastest-growing at a CAGR of 5.8% from 2026 to 2033, driven by expanding primary healthcare access and early diagnostic adoption. Clinics are increasingly equipped with rapid testing tools for early detection. Decentralization of healthcare services is improving accessibility in rural and semi-urban regions. Growing awareness of infectious disease symptoms is increasing outpatient visits. Governments are strengthening community-level surveillance systems. Early-stage treatment and referral systems are boosting clinic utilization. The segment is expanding due to healthcare decentralization trends.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market with the highest share of 61.2% in 2025, due to high inpatient treatment rates and centralized drug dispensing in critical care settings. Most bunyavirus infection treatments are administered within hospitals, ensuring direct pharmacy supply chain control. Emergency drug availability is crucial for hemorrhagic and severe cases. Hospital pharmacies manage injectable therapies and supportive care drugs efficiently. Integration with hospital treatment protocols strengthens this segment. The segment remains dominant due to high hospitalization dependency.

The Online Pharmacy segment is expected to be the fastest-growing at a CAGR of 6.1% from 2026 to 2033, driven by increasing digital healthcare adoption and expanding telemedicine services. Improved internet penetration is enabling easier access to medications in remote areas. Online platforms support quick procurement of supportive and preventive care drugs. Governments are encouraging e-pharmacy frameworks for healthcare accessibility. Rising consumer preference for home-based care is supporting growth. Logistics and cold-chain improvements are enhancing reliability. The segment is expanding due to digital transformation in healthcare delivery.

Bunyavirus Infections Market Regional Analysis

North America dominated the Bunyavirus Infections Market with the largest revenue share of 36.5% in 2025, supported by strong infectious disease surveillance systems, advanced diagnostic infrastructure, and high healthcare expenditure. The region also benefits from well-established outbreak response frameworks, widespread adoption of molecular diagnostics such as PCR and serological testing, and strong government funding for emerging viral disease preparedness. Increasing research activities in zoonotic and vector-borne infections, along with robust hospital networks and academic collaborations, continue to strengthen North America’s leadership position in the global market.

U.S. Bunyavirus Infections Market Insight

The U.S. Bunyavirus Infections market is witnessing steady growth due to strong investments in infectious disease surveillance, advanced diagnostic infrastructure, and high research activity in emerging zoonotic viral infections. The country’s well-developed healthcare system, along with widespread adoption of molecular diagnostics such as PCR and next-generation sequencing, is driving rapid detection and monitoring of bunyavirus outbreaks. In addition, increasing funding for biodefense programs, academic research collaborations, and public health preparedness initiatives is accelerating demand for advanced testing and surveillance solutions across hospitals and laboratories.

Europe Bunyavirus Infections Market Insight

The Europe Bunyavirus Infections market remains a key contributor to global demand, driven by strong government support for infectious disease control, well-established laboratory networks, and robust epidemiological monitoring systems. The region benefits from coordinated public health programs across multiple countries, enabling efficient outbreak detection and response. Increasing focus on vector-borne disease surveillance, rising investment in molecular diagnostics, and strong participation in global health initiatives continue to support market expansion across Europe. Additionally, research funding for hemorrhagic fever and zoonotic disease studies is further strengthening regional growth.

U.K. Bunyavirus Infections Market Insight

The U.K. Bunyavirus Infections market is experiencing steady growth, supported by strong national health surveillance systems, increasing adoption of advanced diagnostic technologies, and rising research focus on emerging viral diseases. Public health agencies and academic institutions are actively engaged in monitoring zoonotic infections and improving early warning systems. Growing use of PCR-based testing, improved laboratory infrastructure, and integration of digital epidemiology tools are enhancing outbreak detection capabilities. Furthermore, government-backed infectious disease preparedness programs are strengthening the country’s capacity to manage bunyavirus-related health risks.

Germany Bunyavirus Infections Market Insight

The Germany Bunyavirus Infections market is expanding steadily due to advanced healthcare infrastructure, strong biomedical research capabilities, and increasing focus on infectious disease diagnostics. The country’s well-developed laboratory network and high adoption of molecular testing technologies are supporting early detection of bunyavirus infections. Growing investments in virology research, combined with strong government emphasis on public health safety and epidemic preparedness, are further driving market growth. Additionally, collaboration between academic institutions and biotechnology companies is enhancing innovation in diagnostic and surveillance solutions.

Asia-Pacific Bunyavirus Infections Market Insight

The Asia-Pacific Bunyavirus Infections market is expected to witness rapid growth, driven by rising incidence of vector-borne diseases, expanding healthcare infrastructure, and increasing government focus on epidemic preparedness. Countries such as China, India, and Japan are strengthening surveillance systems and investing in advanced diagnostic technologies to improve outbreak detection. Growing awareness of zoonotic infections, rising population exposure to vectors, and improved access to healthcare services are further supporting regional market expansion. Additionally, increasing research activities and international collaborations are accelerating adoption of molecular diagnostic solutions.

Japan Bunyavirus Infections Market Insight

The Japan Bunyavirus Infections market is witnessing consistent growth due to strong healthcare infrastructure, advanced diagnostic capabilities, and high focus on infectious disease control. The country’s well-established laboratory systems and widespread use of PCR and serological testing are enabling early detection of bunyavirus infections. Increasing research in emerging viral pathogens, combined with government support for public health preparedness, is further strengthening market development. Additionally, integration of advanced technologies in epidemiological monitoring is improving outbreak response efficiency.

China Bunyavirus Infections Market Insight

The China Bunyavirus Infections market is growing rapidly, driven by increasing urbanization, rising exposure to vector-borne diseases, and strong government investment in infectious disease surveillance systems. Expanding healthcare infrastructure and growing adoption of molecular diagnostics are significantly improving early detection and outbreak response capabilities. The country is also witnessing increased research activity in virology and vaccine development, supported by academic and government collaborations. Furthermore, rising awareness of zoonotic infections and strengthening public health programs are positioning China as a key growth market in the region.

Bunyavirus Infections Market Share

The Bunyavirus Infections industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Roche Holding AG (Switzerland)

- Abbott (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- BD (U.S.)

- QIAGEN (Germany)

- Illumina, Inc. (U.S.)

- GSK plc (U.K.)

- Sanofi (France)

- AstraZeneca (U.K.)

- Moderna, Inc. (U.S.)

- Emergent BioSolutions Inc. (U.S.)

- Inovio Pharmaceuticals, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Novavax, Inc. (U.S.)

Latest Developments in Bunyavirus Infections Market

- In March 2024, the World Health Organization (WHO) reiterated its prioritization of bunyavirus-related pathogens, including hantavirus and Rift Valley fever virus, within global epidemic preparedness and research and development frameworks. The update emphasized strengthening global surveillance systems, accelerating diagnostic innovation, and supporting vaccine and antiviral development under the One Health approach. It also highlighted the need for coordinated international response mechanisms to manage emerging zoonotic threats

- In June 2024, the U.S. Centers for Disease Control and Prevention (CDC) continued enhanced surveillance and reporting of Hantavirus Pulmonary Syndrome (HPS) cases across endemic regions of the United States, particularly in western states. The update emphasized persistent sporadic infections linked to rodent exposure and reinforced the importance of early diagnosis using molecular testing methods such as PCR. Public health advisories also highlighted preventive measures including rodent control, safe cleaning practices, and occupational safety protocols

- In July 2023, the World Health Organization (WHO) issued updated outbreak communications on Rift Valley Fever activity in select African regions, reporting increased transmission risks following heavy rainfall and expanded mosquito breeding conditions. The update emphasized the zoonotic nature of the disease, with transmission occurring between livestock and humans, particularly in agricultural communities. WHO recommended strengthened vector control programs, livestock vaccination campaigns, and improved human disease surveillance under the One Health framework

- In September 2022, the European Centre for Disease Prevention and Control (ECDC) reported continued monitoring of Crimean-Congo Hemorrhagic Fever (CCHF) cases, particularly in southern and southeastern Europe, driven by the spread of Hyalomma tick populations. The agency noted increasing geographic suitability for tick vectors due to climate change, raising concerns about potential expansion into new regions. Enhanced laboratory preparedness, clinician awareness, and early case detection strategies were recommended across EU member states

- In May 2021, the CDC reinforced public health guidance on hantavirus prevention, focusing on rodent control measures and environmental safety practices in residential and occupational settings. The advisory emphasized minimizing exposure to rodent urine, droppings, and nesting materials as key prevention strategies. It also highlighted the importance of early clinical recognition and supportive care to reduce mortality associated with delayed diagnosis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.