Global Byler Disease Market

Market Size in USD Billion

USD

1.75 Billion

USD

2.70 Billion

2024

2032

USD

1.75 Billion

USD

2.70 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.75 Billion | |

| USD 2.70 Billion | |

| % | |

|

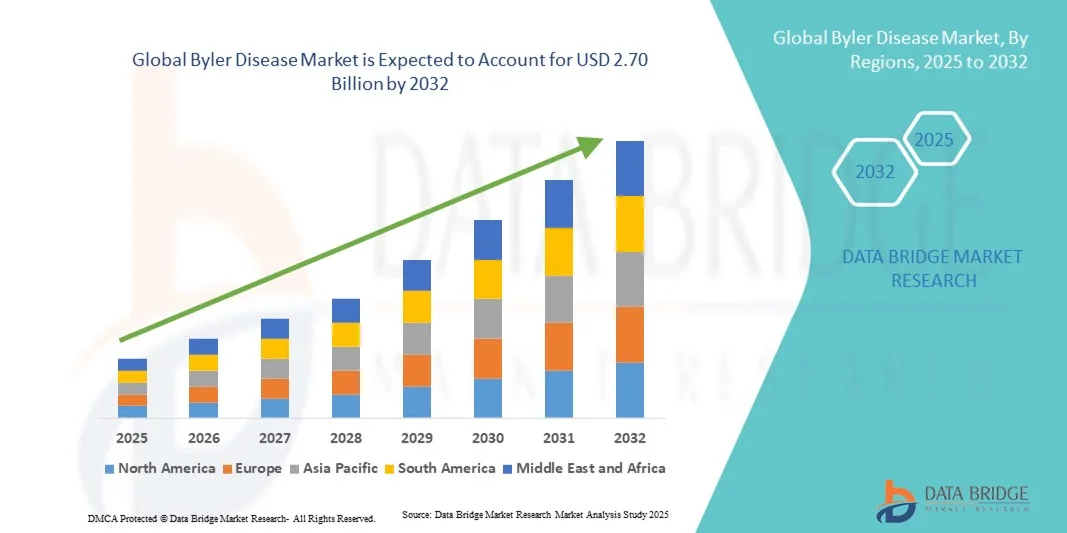

Byler Disease Market Size

- The global Byler Disease market size was valued at USD 1.75 billion in 2024 and is expected to reach USD 2.70 billion by 2032, at a CAGR of 5.60% during the forecast period

- The Byler Disease market growth is largely fueled by the increasing prevalence of genetic liver disorders, growing advancements in genomic research and diagnostic technologies, and improved awareness regarding early detection and management of rare hepatic diseases

- Furthermore, rising investments in novel therapeutic approaches, including gene therapy, targeted drug delivery, and precision medicine, are establishing new standards for the treatment of Byler Disease. These converging factors are significantly accelerating research and clinical development efforts, thereby boosting the overall growth of the Byler Disease market.

Byler Disease Market Analysis

- Byler Disease, a rare hereditary liver disorder also known as Progressive Familial Intrahepatic Cholestasis (PFIC), is increasingly gaining research attention due to advances in genetic testing, disease awareness, and improved diagnostic capabilities. The market for its diagnosis and treatment is expanding across both developed and emerging regions, supported by the introduction of novel therapeutic options and patient advocacy initiatives

- The rising demand for advanced diagnostic tools, targeted therapies, and gene-based treatments is primarily fueling the growth of the Byler Disease market. In addition, increased investment from biotechnology and pharmaceutical companies in rare liver disease research is accelerating innovation and expanding treatment pipelines

- North America dominated the Byler Disease market with the largest revenue share of 42.5% in 2024, driven by strong R&D funding, well-established healthcare infrastructure, and favorable regulatory frameworks supporting orphan drug development. The U.S. continues to lead market expansion due to growing patient registries, clinical trial activity, and collaborations among research institutes and pharma companies

- Asia-Pacific is expected to be the fastest-growing region in the Byler Disease market during the forecast period, owing to rising awareness, expanding access to genetic testing, and increasing healthcare investments in countries such as Japan, China, and India

- The medical treatment segment dominated the market with the largest revenue share of 68.5% in 2024, primarily driven by the rising adoption of pharmacological interventions aimed at managing symptoms, improving bile flow, and preventing liver damage

Report Scope and Byler Disease Market Segmentation

|

Attributes |

Byler Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Byler Disease Market Trends

Advancements in Gene Editing and Molecular Diagnostic Technologies

- A major and accelerating trend in the global Byler Disease market is the growing integration of gene-editing platforms, molecular diagnostics, and precision medicine tools to enhance diagnosis and therapeutic development. Innovations in next-generation sequencing (NGS), CRISPR-based research, and omics-driven approaches are allowing researchers to better understand the genetic mutations and molecular pathways underlying the disease

- For instance, in March 2024, uniQure N.V. announced the expansion of its preclinical gene therapy pipeline targeting rare cholestatic liver disorders, including Byler Disease, leveraging its proprietary AAV platform to improve long-term liver function and reduce bile acid accumulation. Similarly, Mirum Pharmaceuticals and Travere Therapeutics have been investing in gene and bile acid transporter modulation strategies aimed at correcting the root cause of the disorder

- The use of AI-based analytics in the Byler Disease landscape has further strengthened research efficiency by accelerating biomarker identification and predicting therapeutic response patterns. AI models trained on patient genetic profiles and clinical histories are being increasingly applied to design personalized treatment approaches

- Moreover, advancements in liquid biopsy and non-invasive molecular diagnostic tests are simplifying early detection and disease monitoring. Such technologies reduce the need for invasive liver biopsies, making long-term patient management more efficient and safer

- This convergence of molecular biology, artificial intelligence, and digital health technologies is redefining the Byler Disease research ecosystem, enabling faster drug discovery, early intervention, and precision-tailored therapeutic regimens. Consequently, leading pharmaceutical and biotech companies are increasingly investing in genomic medicine partnerships and data-driven diagnostic collaborations to develop more effective, patient-specific therapies

- The trend toward personalized hepatology solutions is expected to reshape market growth, making molecularly guided interventions the new standard for managing Byler Disease and related cholestatic conditions

Byler Disease Market Dynamics

Driver

Rising Research Focus on Genetic Liver Disorders and Expanding Therapeutic Pipeline

- The growing scientific understanding of rare inherited liver disorders, combined with increasing government and private funding for orphan disease research, is driving momentum in the Byler Disease market

- For instance, in April 2024, Mirum Pharmaceuticals announced promising updates on its bile acid transport inhibitor Maralixibat, which continues to demonstrate efficacy in improving pruritus and bile flow among pediatric Byler Disease patients. Such advancements in targeted therapeutic candidates are anticipated to propel market growth over the forecast period

- In addition, the rising number of clinical trials focused on gene replacement and small-molecule therapies is expanding the treatment landscape. The FDA’s Orphan Drug and Fast Track designations have encouraged biopharmaceutical firms to prioritize rare liver diseases, further strengthening innovation

- Advancements in newborn screening programs, combined with the availability of genetic counseling and molecular diagnostics, are also improving early diagnosis rates—facilitating timely treatment intervention and better long-term outcomes

- Moreover, increasing collaboration between academic research centers and pharmaceutical developers is fostering knowledge exchange and technology transfer, accelerating the discovery of disease-modifying treatments. As awareness of cholestatic liver disorders continues to grow, patient advocacy organizations and public health agencies are also playing a crucial role in improving diagnosis and care access

Restraint/Challenge

High Cost of Advanced Therapies and Limited Access to Specialized Care

- Despite technological progress, the high cost of novel gene therapies and rare disease medications poses a significant challenge to the Byler Disease market. The development, regulatory approval, and distribution of precision treatments for small patient populations require substantial investment, making these therapies prohibitively expensive for many healthcare systems

- For instance, gene-based treatments and bile acid transport inhibitors often exceed several hundred thousand dollars per patient annually, creating financial barriers to adoption, especially in developing or resource-limited regions

- Another major challenge lies in the limited availability of specialized hepatology centers and experts experienced in managing rare pediatric liver diseases. This lack of clinical infrastructure often results in delayed diagnosis and inconsistent patient management

- In addition, there are concerns surrounding the long-term safety and durability of emerging gene and molecular therapies. Since many are in early clinical phases, questions remain regarding immune responses, vector delivery efficiency, and the potential need for re-administration

- Addressing these issues requires multi-stakeholder collaboration, including public–private partnerships, cost-sharing frameworks, and expanded patient support programs to improve affordability and access. Furthermore, enhanced regulatory guidance and data-sharing initiatives can ensure that safety and efficacy insights are continuously monitored and optimized

- Overcoming these challenges through cost optimization, global clinical trial expansion, and enhanced patient education will be essential for achieving sustained market growth in the Byler Disease landscape

Byler Disease Market Scope

The market is segmented on the basis of treatment and end-user.

- By Treatment

On the basis of treatment, the Byler Disease market is segmented into medical treatment and surgical treatment. The medical treatment segment dominated the market with the largest revenue share of 68.5% in 2024, primarily driven by the rising adoption of pharmacological interventions aimed at managing symptoms, improving bile flow, and preventing liver damage. Ursodeoxycholic acid (UDCA) remains the cornerstone therapy for reducing cholestasis, while rifampicin and bile acid-binding resins are widely prescribed to alleviate pruritus. Advances in gene-based therapies and hepatoprotective drugs are enhancing treatment outcomes and extending patient survival. The availability of targeted therapies and ongoing clinical research on FXR agonists and bile acid modulators further strengthen this segment’s position. In addition, the non-invasive nature, affordability, and early-stage applicability of medical therapy make it the preferred option among pediatric and adult patients. The increasing prevalence of progressive familial intrahepatic cholestasis (PFIC) cases and growing diagnostic awareness contribute to the sustained dominance of this segment.

The surgical treatment segment is projected to witness the fastest CAGR of 10.9% from 2025 to 2032, fueled by the increasing demand for curative and advanced interventional approaches in severe Byler disease cases. Surgical interventions such as partial external biliary diversion (PEBD), liver transplantation, and ileal bypass are recommended for patients who do not respond adequately to pharmacological therapy. The growing availability of specialized transplant centers, improved postoperative survival rates, and advancements in minimally invasive surgical techniques are driving adoption. In addition, the expanding donor pool, coupled with innovations in immunosuppressive therapy, has enhanced graft survival and reduced complications. Favorable reimbursement policies for critical liver surgeries and the introduction of pediatric-specific surgical protocols also accelerate market growth. Furthermore, growing investments in regenerative medicine and tissue engineering hold long-term potential to reshape the surgical treatment landscape for Byler disease.

- By End-User

On the basis of end-user, the Byler Disease market is segmented into research centers, hospitals, clinics, and others. The hospital segment held the largest market revenue share of 54.1% in 2024, attributed to the concentration of advanced diagnostic infrastructure, specialized hepatology departments, and skilled surgical teams. Hospitals serve as the primary hubs for diagnosis, pharmacological management, and surgical interventions such as liver transplantation and biliary diversion. The presence of multidisciplinary care teams enables comprehensive management of complications such as jaundice, liver fibrosis, and portal hypertension. Furthermore, hospitals benefit from strong collaborations with pharmaceutical firms and academic institutions for clinical trials and drug evaluation programs. The availability of dedicated pediatric hepatology units and increasing government funding for rare disease treatment centers further enhance hospital-based treatment delivery. High patient inflow and integrated patient monitoring systems support continued dominance of this segment.

The research centers segment is projected to record the fastest CAGR of 11.4% from 2025 to 2032, driven by the growing focus on genetic and molecular research to develop disease-modifying therapies. Academic and biotechnology research institutes are increasingly investing in studying ABCB11 and ATP8B1 gene mutations associated with Byler disease, aiming to advance precision medicine approaches. The rise in global rare disease research funding and collaborations between universities, biotech firms, and public health organizations support this growth trajectory. Research centers also play a crucial role in preclinical testing, biomarker discovery, and the development of gene-editing technologies such as CRISPR-based therapies. Increasing grants from initiatives like the NIH and EU Horizon programs are expanding experimental pipelines for pediatric cholestatic liver diseases. Furthermore, growing biobank networks and advanced sequencing platforms enhance diagnostic capabilities, ensuring strong future expansion of this segment.

Byler Disease Market Regional Analysis

- North America dominated the Byler Disease market with the largest revenue share of 42.5% in 2024, driven by strong R&D funding, a well-established healthcare infrastructure, and favorable regulatory frameworks supporting orphan drug development

- The region’s leadership is further strengthened by advanced genomic research capabilities, the growing prevalence of rare liver disorders, and the active involvement of patient advocacy groups promoting early diagnosis and access to care

- The rising number of collaborations among pharmaceutical companies, biotech startups, and academic institutions is also fostering innovation in gene therapy and bile acid modulation research. The U.S. continues to lead market expansion due to growing patient registries, clinical trial activity, and research partnerships aimed at developing disease-modifying treatments

U.S. Byler Disease Market Insight

The U.S. Byler Disease market captured the largest revenue share within North America in 2024, fueled by extensive clinical trial activity and significant advancements in molecular diagnostics. Increased awareness of rare pediatric liver diseases and a supportive reimbursement framework for orphan drugs have strengthened the market’s foundation. Moreover, the presence of key biopharmaceutical players, such as Mirum Pharmaceuticals and Travere Therapeutics, is accelerating therapeutic progress through ongoing R&D and regulatory approvals. The growing adoption of next-generation sequencing (NGS) technologies and precision medicine platforms is also enhancing diagnostic accuracy and facilitating early intervention, positioning the U.S. as a global leader in Byler Disease research and treatment innovation.

Europe Byler Disease Market Insight

The Europe Byler Disease market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by favorable government policies supporting orphan disease research, rising adoption of advanced diagnostic technologies, and increased investment in rare disease clinical trials. European regulatory initiatives, such as the European Medicines Agency (EMA) Orphan Designation Program, continue to encourage innovation and patient access to novel treatments. Growing awareness among healthcare professionals and patient organizations is further promoting earlier diagnosis and treatment adoption. The region also benefits from a strong academic research base, particularly in countries such as Germany, France, and the U.K., where cross-border collaborations are enhancing the pace of clinical development.

U.K. Byler Disease Market Insight

The U.K. Byler Disease market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by an expanding focus on genomic medicine and national rare disease frameworks. Government-backed initiatives such as Genomics England’s 100,000 Genomes Project have improved the early detection of genetic liver conditions, supporting patient identification and targeted therapy research. In addition, partnerships between the National Health Service (NHS) and pharmaceutical innovators are strengthening clinical trial infrastructure. The increasing availability of newborn screening programs and genetic counseling services is enabling earlier intervention, thereby improving patient outcomes and fueling steady market growth in the country.

Germany Byler Disease Market Insight

The Germany Byler Disease market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare system, emphasis on biotechnology innovation, and growing support for rare disease research. Germany’s regulatory and funding ecosystem actively promotes collaboration between academic institutions and pharmaceutical developers, resulting in a robust clinical trial pipeline for liver-based genetic therapies. Furthermore, the rising adoption of molecular diagnostic platforms and the establishment of specialized hepatology centers are facilitating improved disease management. With strong government initiatives supporting patient registries and precision medicine integration, Germany is emerging as one of Europe’s leading contributors to Byler Disease research and therapy development.

Asia-Pacific Byler Disease Market Insight

The Asia-Pacific Byler Disease market is poised to grow at the fastest CAGR during the forecast period (2025–2032), driven by rising awareness of genetic disorders, expanding access to advanced diagnostic tools, and increasing healthcare investments across countries such as Japan, China, and India. The region’s growing participation in international clinical trials and government-led initiatives to enhance rare disease care infrastructure are accelerating progress. Emerging economies are strengthening genetic testing availability and establishing patient registries to improve diagnostic accuracy and care coordination. Moreover, expanding collaborations with Western biopharma companies are enabling technology transfer and clinical research capacity building, making APAC a critical region for future growth in Byler Disease management.

Japan Byler Disease Market Insight

The Japan Byler Disease market is gaining momentum due to the country’s advanced biotechnology capabilities, high adoption of genetic testing, and strong focus on rare disease policy reform. Japan’s healthcare system is increasingly emphasizing early detection and precision treatment approaches for inherited liver disorders. Collaborations between research institutes and pharmaceutical firms are leading to the development of gene-targeted and bile acid-modulating therapies. Furthermore, Japan’s aging population and highly developed healthcare infrastructure are contributing to the demand for efficient, patient-centric diagnostic solutions. Continuous government support for rare disease funding and inclusion of innovative treatments in reimbursement frameworks are expected to sustain market growth in the coming years.

China Byler Disease Market Insight

The China Byler Disease market accounted for the largest market revenue share within Asia-Pacific in 2024, supported by a rapidly expanding middle class, rising healthcare expenditure, and the government’s focus on genetic disease awareness and treatment. China is becoming a key hub for rare disease research, supported by national programs promoting genomic medicine and clinical trial expansion. Local biotechnology companies are actively collaborating with global firms to develop accessible diagnostic kits and gene therapy solutions tailored for the regional population. In addition, public–private partnerships are improving access to advanced treatment options and fostering the establishment of specialized hepatology and genetic research centers. The ongoing policy shift toward early screening and rare disease inclusion under national insurance schemes is expected to further accelerate market growth in the years ahead.

Byler Disease Market Share

The Byler Disease industry is primarily led by well-established companies, including:

- Mirum Pharmaceuticals (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Intercept Pharmaceuticals (U.S.)

- Travere Therapeutics (U.S.)

- GlaxoSmithKline plc (U.K.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Johnson & Johnson (U.S.)

- Vertex Pharmaceuticals Incorporated (U.S.)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Sanofi S.A. (France)

- Bayer AG (Germany)

- Genfit SA (France)

- Apteeus (France)

- Canbridge Pharmaceuticals Inc. (China)

Latest Developments in Global Byler Disease Market

- In July 2021, the U.S. Food and Drug Administration (FDA) approved odevixibat (Bylvay), developed by Albireo Pharma, as the first ileal bile acid transport inhibitor indicated for pruritus in patients with progressive familial intrahepatic cholestasis (PFIC) aged three months and older. This milestone marked the first approved pharmacologic therapy for Byler disease/PFIC

- In September 2021, the FDA approved maralixibat (Livmarli) for the treatment of cholestatic pruritus in patients with Alagille syndrome, a development that paved the way for expanding IBAT inhibitor use to PFIC and similar cholestatic disorders

- In October 2022, Albireo Pharma presented long-term results from the PEDFIC trials for odevixibat, showing sustained reductions in serum bile acids and improvements in pruritus and sleep among PFIC patients, supporting the drug’s long-term efficacy and safety profile

- In March 2023, Mirum Pharmaceuticals announced positive Phase 3 MARCH-PFIC study results for maralixibat, demonstrating significant improvement in cholestatic pruritus and serum bile acid reduction, which strengthened its position as a leading therapy in the Byler disease market

- In March 2024, the U.S. FDA approved an expanded indication for Livmarli (maralixibat) to include the treatment of cholestatic pruritus in patients with PFIC aged five years and older, broadening patient access to targeted therapy

- In July 2024, the European Commission granted marketing authorization for Livmarli for PFIC patients aged three months and older, following the successful outcomes of the MARCH-PFIC study, making it the first IBAT inhibitor approved in the European Union for this indication

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.