Global C5 Complement Inhibitor Drug Market

Market Size in USD Billion

USD

1.68 Billion

USD

5.93 Billion

2025

2033

USD

1.68 Billion

USD

5.93 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.68 Billion | |

| USD 5.93 Billion | |

| % | |

|

C5 Complement Inhibitor Drug Market Overview

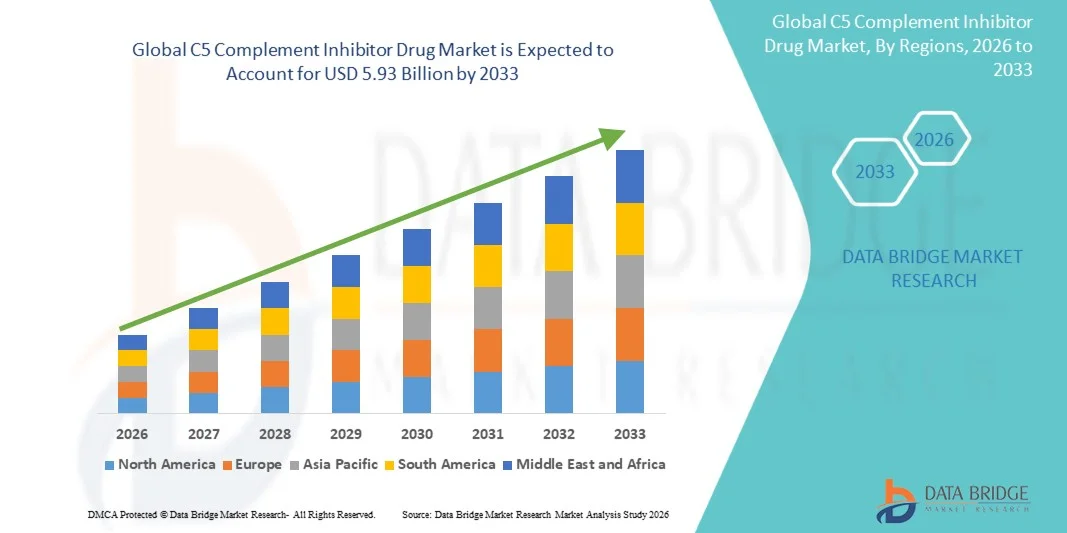

The C5 Complement Inhibitor Drug Market was valued at USD 1.68 billion in 2025 and is projected to reach USD 5.93 billion by 2033, growing at a CAGR of 17.10% from 2026 to 2033. The C5 Complement Inhibitor Drug Market is witnessing strong growth driven by the increasing prevalence of complement-mediated rare diseases such as paroxysmal nocturnal hemoglobinuria (PNH), atypical hemolytic uremic syndrome (aHUS), generalized myasthenia gravis (gMG), and neuromyelitis optica spectrum disorder (NMOSD). Rising awareness among clinicians regarding targeted complement inhibition therapy is significantly improving diagnosis rates and treatment initiation. The growing shift toward precision medicine and biologics-based therapies is further accelerating market expansion.

Increasing approvals of advanced C5 inhibitors such as eculizumab and ravulizumab are enhancing treatment accessibility and clinical adoption. Expanding healthcare expenditure and rare disease funding programs in developed regions are supporting patient access to high-cost therapies. Pharmaceutical companies are heavily investing in next-generation long-acting complement inhibitors to improve dosing convenience and patient compliance. Rising clinical trials focusing on novel complement pathway targets are further strengthening the pipeline. Growing collaboration between biotech firms and research institutions is accelerating innovation. Improved diagnostic capabilities for rare autoimmune and hematologic disorders are increasing patient identification rates. Expanding orphan drug incentives from regulatory agencies are boosting drug development activity. Overall, the market is driven by strong clinical demand and continuous therapeutic innovation in complement biology.

Key Market Trends & Insights

- North America dominated the C5 Complement Inhibitor Drug Market with the largest revenue share of 39.6% in 2025, supported by strong prevalence of rare complement-mediated disorders, advanced biologics manufacturing capabilities, and early adoption of targeted immunotherapies. The region also benefits from robust healthcare reimbursement frameworks, strong presence of leading pharmaceutical companies, and widespread access to specialty treatment centers for diseases such as PNH, aHUS, and gMG.

- The Eculizumab segment dominated the market with a 42.18% share in 2025, owing to its strong clinical efficacy in treating rare complement-mediated disorders such as PNH and aHUS .

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 11.8% from 2026 to 2033, fueled by improving rare disease diagnosis rates, expanding access to biologic therapies, increasing healthcare expenditure, and rising adoption of advanced immunotherapy treatments across China, Japan, South Korea, and India.

- The Paroxysmal Nocturnal Hemoglobinuria (PNH) segment dominated the application category with a 48.7% share in 2025, owing to the high treatment dependence on C5 complement inhibitors, increasing diagnosis rates, and strong clinical demand for long-term disease management therapies.

Market Size & Forecast

- Global Market Value (2025): USD 1.68 Billion

- Expected Market Value (2033): USD 5.93 Billion

- Forecast CAGR (2026–2033): 17.10%

- Leading Region in 2025: Europe

- Fastest Growing Region: Asia-Pacific

Report Scope and C5 Complement Inhibitor Drug Market Segmentation

|

Attributes |

C5 Complement Inhibitor Drug Key Market Insights |

|

· Segments Covered |

· By Drug Type: Eculizumab, Ravulizumab, Zilucoplan, Crovalimab, and Others

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Alexion Pharmaceuticals (U.S.) · AstraZeneca plc (U.K.) · Roche Holding AG (Switzerland) · Amgen Inc. (U.S.) · Regeneron Pharmaceuticals Inc. (U.S.) · Pfizer Inc. (U.S.) · GlaxoSmithKline plc (U.K.) · Apellis Pharmaceuticals Inc. (U.S.) · Biogen Inc. (U.S.) · Samsung Bioepis Co., Ltd. (South Korea) · SOBI (Swedish Orphan Biovitrum AB) (Sweden) · Chugai Pharmaceutical Co., Ltd. (Japan) · Takeda Pharmaceutical Company Limited (Japan) · Akari Therapeutics (U.K./U.S.) · Omeros Corporation (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · Horizon Therapeutics (Ireland/U.S.) · Catalyst Biosciences Inc. (U.S.) · BioCryst Pharmaceuticals Inc. (U.S.) · Ra Pharmaceuticals (acquired by UCB) (Belgium) · UCB S.A. (Belgium) · Regeneron (U.S.) · SOBI Biopharma (Europe) · Cellenkos Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Next-Generation Long-Acting C5 Inhibitors · Rising Adoption in Neurological and Autoimmune Indications · Growth in Orphan Drug Development and Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

C5 Complement Inhibitor Drug Market Trends

Trend: Expanding Use of C5 Complement Inhibitors in Rare Disease and Targeted Immunotherapy

The C5 Complement Inhibitor Drug Market is witnessing strong growth due to increasing adoption of targeted complement pathway inhibition therapies for rare and life-threatening hematologic and neurological disorders. Drugs such as eculizumab and ravulizumab are widely used in the treatment of Paroxysmal Nocturnal Hemoglobinuria (PNH), atypical hemolytic uremic syndrome (aHUS), and generalized myasthenia gravis (gMG), offering improved survival outcomes and reduced disease progression. For instance, long-acting C5 inhibitors have significantly reduced treatment frequency from biweekly to every 8 weeks in certain PNH patients, improving patient compliance and quality of life. The rising focus on precision medicine and increasing regulatory approvals for complement-targeting biologics are further accelerating market expansion.

C5 Complement Inhibitor Drug Market Dynamics

Key Market Driver: Rising Prevalence of Rare Complement-Mediated Disorders and Expansion of Biologic Therapies

A major driver of the C5 complement inhibitor market is the increasing diagnosis and treatment of rare complement-mediated diseases such as PNH, aHUS, and gMG. According to clinical rare disease registries, these conditions, though individually uncommon, collectively affect a growing patient population due to improved diagnostic awareness and genetic testing capabilities.

Pharmaceutical companies are heavily investing in monoclonal antibody and next-generation complement inhibitor development to improve efficacy, extend dosing intervals, and reduce treatment burden. The strong clinical success of eculizumab has established complement inhibition as a validated therapeutic pathway, encouraging further pipeline expansion. In addition, increasing healthcare reimbursement coverage in North America and Europe is supporting broader patient access to these high-cost biologics.

Key Restraint/Challenge: Extremely High Treatment Cost and Limited Accessibility in Emerging Markets

A significant challenge in the global market is the extremely high cost of C5 complement inhibitor therapies, which can exceed hundreds of thousands of dollars per patient annually. This limits accessibility, particularly in low- and middle-income countries where reimbursement systems are limited or absent.

In addition, long-term safety monitoring requirements, intravenous administration logistics, and need for lifelong therapy in many patients increase overall healthcare burden. Delayed diagnosis of rare diseases and lack of specialized treatment centers in emerging regions further restrict timely access to these therapies. Patent protection on leading biologics also delays the entry of biosimilars, maintaining high treatment costs globally.

Key Market Opportunity: Development of Next-Generation Long-Acting and Subcutaneous Complement Inhibitors

The development of next-generation complement inhibitors with improved pharmacokinetics, including subcutaneous and oral formulations, presents a major growth opportunity for the market. Newer agents such as long-acting C5 inhibitors are reducing dosing frequency and improving patient convenience compared to first-generation intravenous therapies.

For instance, pipeline drugs are increasingly targeting upstream components of the complement cascade to improve therapeutic precision and reduce infection risks associated with terminal complement inhibition. The expansion of clinical trials, increasing orphan drug designations, and strong investment in rare disease research by pharmaceutical companies across North America and Europe are expected to drive innovation in this market. In addition, growing adoption of genetic screening programs and improved diagnostic infrastructure in Asia-Pacific is expected to expand the eligible patient pool over the forecast period.

C5 Complement Inhibitor Drug Market Scope

The C5 Complement Inhibitor Drug market is segmented on the basis of drug type and application.

- By Drug Type

On the basis of drug type, the C5 Complement Inhibitor Drug Market is segmented into Eculizumab, Ravulizumab, Zilucoplan, Crovalimab, and Others. The Eculizumab segment dominated the market with a 42.18% share in 2025, owing to its strong clinical efficacy in treating rare complement-mediated disorders such as PNH and aHUS. Its early market entry and extensive regulatory approvals across North America and Europe have established it as a first-line therapy in many treatment guidelines. High physician familiarity and proven long-term safety data further strengthen its dominance in the global market. Increasing adoption in hospital pharmacies and specialty care centers continues to support its revenue contribution. However, high treatment costs and infusion frequency limitations are gradually encouraging a shift toward next-generation therapies.

The Ravulizumab segment is projected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by its extended dosing interval and improved patient compliance compared to Eculizumab. Its long-acting mechanism reduces infusion frequency, significantly improving quality of life for chronic patients requiring lifelong therapy. Expanding approvals across multiple rare disease indications are further accelerating adoption. Pharmaceutical companies are increasingly promoting Ravulizumab as a next-generation standard of care in complement inhibition therapy. Rising healthcare expenditure and reimbursement support in developed markets are also boosting uptake. Continuous clinical expansion studies are expected to further widen its therapeutic applications over the forecast period.

- By Application

On the basis of application, the C5 Complement Inhibitor Drug Market is segmented into Paroxysmal Nocturnal Hemoglobinuria (PNH), Atypical Hemolytic Uremic Syndrome (aHUS), Generalized Myasthenia Gravis (gMG), Neuromyelitis Optica Spectrum Disorder (NMOSD), and Others. The PNH segment dominated the market with a 38.76% share in 2025, owing to the high prevalence of complement-mediated hemolysis and strong dependence on C5 inhibitors as the standard treatment approach. Increasing diagnosis rates and improved awareness among clinicians have significantly boosted treatment adoption. The availability of targeted biologics has transformed PNH management from symptomatic care to disease control. Hospitals and specialty hematology centers remain the primary treatment hubs for this indication. Strong clinical guideline inclusion further reinforces its leading position.

The Generalized Myasthenia Gravis (gMG) segment is expected to witness the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing recognition of complement involvement in neuromuscular disorders. Rising approvals of C5 inhibitors for neurological indications are expanding the patient pool significantly. Improved diagnostic capabilities are enabling earlier disease identification and treatment initiation. Pharmaceutical companies are actively investing in clinical trials to expand label indications for gMG. Growing patient awareness and specialty neurology clinic adoption are further accelerating demand. Expanding biologics pipeline targeting complement pathways is expected to sustain strong growth momentum.

C5 Complement Inhibitor Drug Market Regional Analysis

North America dominated the C5 Complement Inhibitor Drug Market and accounted for the largest revenue share of 39.6% in 2025, supported by strong prevalence of rare complement-mediated disorders, advanced biologics manufacturing capabilities, and early adoption of targeted immunotherapies. The region also benefits from robust healthcare reimbursement frameworks, strong presence of leading pharmaceutical companies, and widespread access to specialty treatment centers for conditions such as Paroxysmal Nocturnal Hemoglobinuria (PNH), atypical hemolytic uremic syndrome (aHUS), and generalized myasthenia gravis (gMG). Increasing clinical awareness, improved diagnostic capabilities, and expanding access to complement-targeting therapies continue to strengthen regional market dominance.

U.S. C5 Complement Inhibitor Drug Market Insight

The U.S. C5 Complement Inhibitor Drug market is witnessing strong growth due to rising prevalence of rare hematologic and autoimmune disorders, alongside increasing uptake of complement-targeted biologics in clinical practice. The country’s well-established specialty pharmacy network, strong pipeline of monoclonal antibodies, and rapid adoption of next-generation complement inhibitors are driving demand across hospital and outpatient settings. In addition, favorable insurance coverage policies and accelerated FDA approvals for orphan drugs are further supporting market expansion.

Europe C5 Complement Inhibitor Drug Market Insight

The Europe C5 Complement Inhibitor Drug market remains a key contributor to global revenue, driven by strong healthcare infrastructure, expanding rare disease screening programs, and increasing availability of advanced biologic therapies. Countries such as Germany, France, and the U.K. are witnessing growing use of complement inhibitors in treating PNH, aHUS, and gMG. Furthermore, collaborative initiatives between regulatory agencies and pharmaceutical companies are accelerating clinical adoption and improving patient access to high-cost biologics.

U.K. C5 Complement Inhibitor Drug Market Insight

The U.K. C5 Complement Inhibitor Drug market is experiencing steady growth, supported by the National Health Service (NHS) expanding access to rare disease therapies and increasing adoption of advanced immunological treatments. Rising awareness among clinicians, coupled with centralized treatment pathways for complement-mediated disorders, is improving diagnosis rates. The integration of specialized immunology centers and ongoing clinical trials for next-generation C5 inhibitors are further strengthening market growth.

Germany C5 Complement Inhibitor Drug Market Insight

The Germany C5 Complement Inhibitor Drug market is expanding steadily due to strong pharmaceutical research capabilities, high diagnosis rates for rare complement disorders, and increasing use of biologics in tertiary care hospitals. The country’s robust biopharmaceutical manufacturing base and strong reimbursement environment are enabling wider patient access to therapies such as eculizumab and ravulizumab. Ongoing clinical research in complement pathway modulation is also supporting innovation in treatment approaches.

Asia-Pacific C5 Complement Inhibitor Drug Market Insight

The Asia-Pacific C5 Complement Inhibitor Drug market is expected to witness rapid growth, driven by improving diagnosis of rare diseases, rising healthcare expenditure, and increasing availability of biologic therapies. Countries such as China, Japan, South Korea, and India are expanding access to complement-targeted treatments through improved hospital infrastructure and growing awareness among healthcare professionals. In addition, increasing government focus on rare disease frameworks and biosimilar development is further supporting regional market expansion.

Japan C5 Complement Inhibitor Drug Market Insight

The Japan C5 Complement Inhibitor Drug market is witnessing consistent growth due to strong clinical research activity, early adoption of advanced biologics, and well-structured rare disease treatment pathways. Japanese pharmaceutical companies are actively involved in complement inhibitor development, while hospitals are increasingly integrating targeted immunotherapies into standard care protocols for PNH and gMG. The country’s aging population is also contributing to higher diagnosis rates and treatment demand.

China C5 Complement Inhibitor Drug Market Insight

The China C5 Complement Inhibitor Drug market is growing rapidly, driven by expanding rare disease diagnosis capabilities, rising healthcare investment, and increasing adoption of innovative biologics in tertiary hospitals. Government initiatives to improve access to orphan drugs and strengthen national rare disease registries are accelerating market development. In addition, collaborations between domestic biotech firms and global pharmaceutical companies are enhancing availability of complement-targeted therapies across major urban healthcare centers.

C5 Complement Inhibitor Drug Market Share

The C5 Complement Inhibitor Drug industry is primarily led by well-established companies, including:

- Alexion Pharmaceuticals (U.S.)

- AstraZeneca plc (U.K.)

- Roche Holding AG (Switzerland)

- Amgen Inc. (U.S.)

- Regeneron Pharmaceuticals Inc. (U.S.)

- Pfizer Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Apellis Pharmaceuticals Inc. (U.S.)

- Biogen Inc. (U.S.)

- Samsung Bioepis Co., Ltd. (South Korea)

- SOBI (Swedish Orphan Biovitrum AB) (Sweden)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Akari Therapeutics (U.K./U.S.)

- Omeros Corporation (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Horizon Therapeutics (Ireland/U.S.)

- Catalyst Biosciences Inc. (U.S.)

- BioCryst Pharmaceuticals Inc. (U.S.)

- Ra Pharmaceuticals (acquired by UCB) (Belgium)

- UCB S.A. (Belgium)

- Regeneron (U.S.)

- SOBI Biopharma (Europe)

- Cellenkos Inc. (U.S.)

Latest Developments in C5 Complement Inhibitor Drug Market

- In December 2021, Alexion Pharmaceuticals (now part of AstraZeneca) continued the global expansion of ravulizumab (Ultomiris) following multiple regulatory approvals across additional indications, including atypical hemolytic uremic syndrome (aHUS) and generalized myasthenia gravis (gMG), strengthening its position as a long-acting next-generation C5 complement inhibitor. The expansion reinforced the shift from short-acting C5 blockade therapies to extended dosing regimens, improving patient compliance and reducing treatment burden

- In October 2023, UCB announced the U.S. FDA approval of zilucoplan (Zilbrysq) for the treatment of generalized myasthenia gravis (gMG) in adult patients who are anti-acetylcholine receptor antibody-positive. Zilucoplan is a subcutaneous C5 complement inhibitor that provides self-administration convenience and rapid complement blockade, marking an important advancement in patient-friendly complement inhibition therapy and expanding the competitive landscape beyond monoclonal antibody-based therapies

- In December 2023, the European Commission granted marketing authorization for zilucoplan (Zilbrysq) for the treatment of gMG, expanding its availability across Europe. This approval represented a key milestone in the commercialization of peptide-based complement C5 inhibitors, highlighting increasing regulatory acceptance of alternative molecular formats beyond traditional monoclonal antibodies in complement-targeted therapy

- In June 2024, Roche received FDA approval for crovalimab (Piasky) for the treatment of paroxysmal nocturnal hemoglobinuria (PNH) in patients aged 13 years and older. Crovalimab is a next-generation recycling anti-C5 antibody designed for subcutaneous administration with extended dosing intervals, reducing infusion burden compared to earlier therapies like eculizumab and ravulizumab

- In March 2024, the U.S. FDA approved ravulizumab (Ultomiris) for neuromyelitis optica spectrum disorder (NMOSD) in adults who are anti-aquaporin-4 antibody positive. This expanded indication strengthened ravulizumab’s position as a multi-disease C5 inhibitor covering PNH, aHUS, gMG, and NMOSD, reinforcing its dominance in the long-acting complement inhibitor segment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.