Global Camurati Engelmann Disease Treatment Market

Market Size in USD Billion

USD

217.93 Billion

USD

295.96 Billion

2025

2033

USD

217.93 Billion

USD

295.96 Billion

2025

2033

| 2026 - 2033 | |

| USD 217.93 Billion | |

| USD 295.96 Billion | |

| % | |

|

Camurati-Engelmann Disease Treatment Market Size

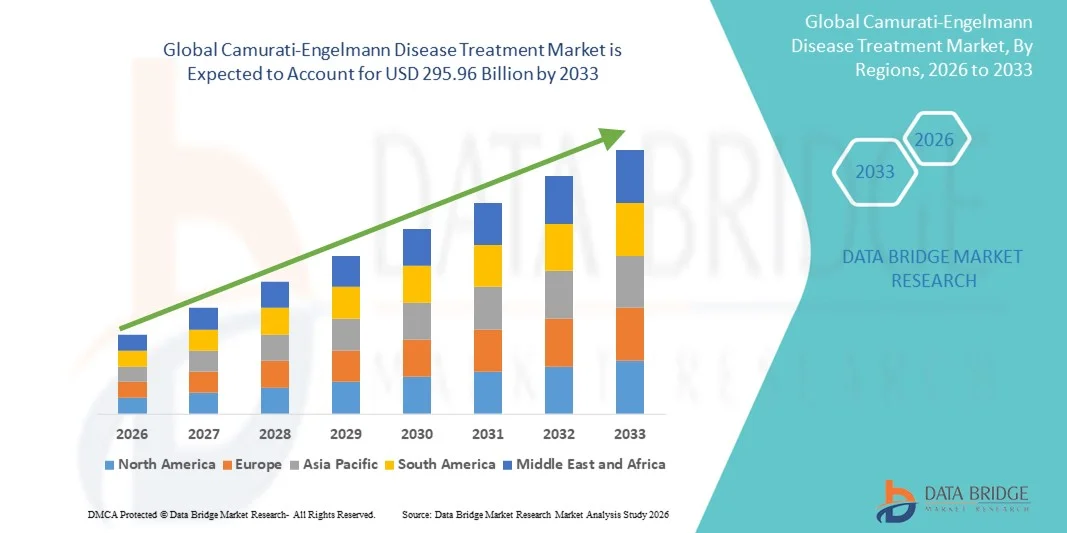

- The global Camurati-Engelmann Disease Treatment market size was valued at USD 217.93 billion in 2025 and is expected to reach USD 295.96 billion by 2033, at a CAGR of 3.90% during the forecast period

- The market growth is largely fueled by increasing awareness of rare genetic disorders, advancements in diagnostic techniques such as genetic testing, and a growing emphasis on early identification of Camurati-Engelmann disease, enabling timely treatment and management. Improved access to specialized healthcare facilities is further supporting market expansion across developed and emerging regions

- Furthermore, rising demand for effective symptomatic management—including corticosteroids, bisphosphonates, pain-relief therapies, and physiotherapy—is driving adoption of Camurati-Engelmann Disease Treatment options. Growing research efforts, improved understanding of TGFB1 gene mutations, and the development of targeted therapies are strengthening clinical outcomes. These converging factors are accelerating the uptake of Camurati-Engelmann Disease Treatment solutions, thereby significantly boosting the industry’s growth

Camurati-Engelmann Disease Treatment Market Analysis

- Camurati-Engelmann Disease Treatment, involving therapies such as corticosteroids, analgesics, physiotherapy, and emerging targeted treatments, is becoming increasingly important in clinical practice due to rising awareness of rare bone disorders, improved genetic testing availability, and earlier diagnosis. Hospitals and specialty clinics are adopting more advanced management approaches to improve patient quality of life and reduce disease progression

- The increasing demand for Camurati-Engelmann Disease Treatment is primarily driven by advancements in molecular diagnostics, higher reporting of TGFB1 gene mutations, growing patient advocacy, and the rising need for effective pain-management and mobility-enhancing therapies. Research into precision medicine and long-term disease-modifying treatments is further accelerating adoption across global healthcare systems

- North America dominated the Camurati-Engelmann Disease Treatment market with the largest revenue share of 38.9% in 2025, supported by strong diagnostic infrastructure, high awareness of rare genetic skeletal disorders, robust healthcare spending, and active research collaborations. The U.S. leads the region due to wide access to genetic screening, availability of orphan-disease specialists, and increased participation in clinical research for rare bone dysplasias

- Asia-Pacific is expected to be the fastest growing region in the Camurati-Engelmann Disease Treatment market during the forecast period, projected to grow at a CAGR from 2026 to 2033. Growth is driven by rapidly expanding healthcare access, increasing focus on rare disease diagnosis, rising medical genetics facilities, and government initiatives to improve early detection of hereditary disorders in countries such as China, Japan, India, and South Korea

- The medication segment held the largest market revenue share of 50.3% in 2025, driven by the widespread reliance on pharmacological management such as corticosteroids, NSAIDs, and bisphosphonates

Report Scope and Camurati-Engelmann Disease Treatment Market Segmentation

|

Attributes |

Camurati-Engelmann Disease Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Camurati-Engelmann Disease Treatment Market Trends

Growing Focus on Targeted and Multimodal Therapies

- A significant trend in the global Camurati-Engelmann Disease Treatment market is the rising adoption of targeted, multimodal treatment approaches that combine pharmacological therapies, physiotherapy, and supportive care to improve patient outcomes

- Recent clinical studies show increased use of corticosteroids and interferon-alpha in managing disease progression and reducing bone pain, reflecting a shift toward evidence-based personalized therapy

- For instance, in 2023, several tertiary care centers in Europe implemented combined corticosteroid and physiotherapy regimens, which helped improve patient mobility and quality of life

- Medical research is also emphasizing early diagnosis and proactive management to slow disease progression and prevent complications

- The trend is further supported by the growing availability of intravenous gamma globulin and sirolimus therapy in specialized centers, expanding treatment options for severe cases

- Patient advocacy groups are increasingly promoting awareness campaigns and standardized treatment protocols, resulting in better patient adherence and clinical outcomes

- Clinicians are also integrating regular monitoring of biochemical markers and imaging studies to guide treatment adjustments, reflecting a data-driven and patient-centric care approach

- Multidisciplinary care involving rheumatologists, orthopedic specialists, and rehabilitation teams is becoming common, enhancing long-term management and functional outcomes

- The overall trend reflects a more systematic, research-backed, and patient-focused approach to managing Camurati-Engelmann Disease globally, improving both clinical efficacy and quality of life for patients

Camurati-Engelmann Disease Treatment Market Dynamics

Driver

Increasing Disease Awareness and Rising Incidence of Rare Genetic Disorders

- The rising awareness of Camurati-Engelmann Disease among healthcare professionals and patients is a key driver for market growth

- For instance, in March 2024, the European Society for Pediatric Rheumatology issued updated guidelines for the diagnosis and management of rare bone disorders, including Camurati-Engelmann Disease, promoting earlier recognition and treatment

- Advances in genetic testing and molecular diagnostics have enabled timely identification of mutations associated with the disease, improving prognosis and treatment planning

- Patients and caregivers are increasingly seeking specialized therapies and supportive care programs, further propelling market demand

- Healthcare infrastructure improvements in emerging regions are also supporting better access to treatments and specialized centers

- Insurance coverage expansions for rare disease therapies in certain countries have encouraged adoption of more advanced and targeted treatments

- The integration of multidisciplinary approaches and improved patient monitoring techniques is driving clinical uptake of therapies such as corticosteroids, interferon-alpha, and sirolimus

- Increasing clinical trials and research studies targeting disease-modifying agents are expected to sustain growth by providing more treatment options

- Overall, enhanced disease awareness, improved diagnostics, and patient advocacy are key factors fueling the Camurati-Engelmann Disease Treatment market globally

Restraint/Challenge

Limited Treatment Options and High Cost of Therapies

- A major restraint in the Camurati-Engelmann Disease Treatment market is the limited availability of approved pharmacological therapies, making management largely symptomatic and supportive

- For instance, intravenous gamma globulin and sirolimus are available only in specialized centers, limiting accessibility for patients in rural or underserved regions

- High treatment costs, particularly for long-term therapies like corticosteroids or interferon-alpha, pose affordability challenges for patients and healthcare systems

- The rarity of the disease also limits large-scale clinical trials, which constrains the development of new therapies

Delayed diagnosis and misdiagnosis in primary care settings often lead to disease progression before effective intervention, reducing treatment efficacy - Managing side effects associated with corticosteroids or immunomodulatory therapies is challenging and requires close monitoring, adding to clinical complexity

- Insurance coverage gaps in several regions can hinder timely access to optimal therapies

- Awareness and expertise are limited in emerging markets, impacting treatment adoption and follow-up care

- Addressing these challenges through new drug development, patient assistance programs, global awareness campaigns will be critical for sustained growth in the Camurati-Engelmann Disease Treatment market

Camurati-Engelmann Disease Treatment Market Scope

The market is segmented on the basis of drug type, treatment, diagnosis, dosage, route of administration, end‑users, and distribution channel.

- By Drug Type

On the basis of drug type, the Camurati‑Engelmann Disease Treatment market is segmented into corticosteroids, non‑steroidal anti‑inflammatory drugs (NSAIDs), losartan, analgesics, and bisphosphonates. The corticosteroids segment dominated the largest market revenue share of 45.7% in 2025, driven by their proven efficacy in reducing bone pain, inflammation, and progressive cortical thickening associated with the disease. Their long track record in clinical practice, strong physician familiarity, and rapid symptomatic relief make them a first-line treatment. Patients often tolerate oral or injectable corticosteroids and prefer them due to accessible dosing regimens. Their integration into standard disease‑management guidelines further strengthens clinical adoption. Corticosteroids remain widely available, cost‑effective relative to newer therapies, and suitable for both pediatric and adult patients. The combination of anti‑inflammatory effect and dosing flexibility supports sustained market dominance. Their broad use in multidisciplinary care settings and inclusion in long‑term treatment protocols ensures consistent demand.

The losartan segment is expected to witness the fastest CAGR of 19.1% from 2026 to 2033, as emerging evidence indicates its potential role in modulating bone remodeling and reducing cortical expansion in Camurati‑Engelmann Disease. Clinical studies increasingly support off-label use of losartan in combination with steroid therapy, which is driving wider adoption. Its oral formulation and favorable safety profile make it attractive for chronic therapy. Growing physician awareness and expanding trial data boost confidence in losartan’s benefits. The drug’s ability to target underlying pathophysiology, rather than just symptoms, positions it as a promising long-term adjunct treatment. Patient advocacy and rare‑disease research funding are accelerating investment in losartan‑based regimens.

- By Treatment

On the basis of treatment, the Camurati‑Engelmann Disease Treatment market is segmented into medication, surgery, and gene therapy. The medication segment held the largest market revenue share of 50.3% in 2025, driven by the widespread reliance on pharmacological management such as corticosteroids, NSAIDs, and bisphosphonates. Medication provides a non‑invasive and accessible way to manage chronic symptoms, including bone pain and inflammation. It is favored for long-term therapy due to its relative safety compared to surgical options. Physicians often use a combination of drugs to tailor treatment to disease severity and patient needs. The availability of multiple classes of drugs supports flexible treatment regimens. Patients benefit from regular outpatient follow‑ups rather than hospital admission. Medication's role in first-line and maintenance therapy secures its dominance in clinical practice.

The gene therapy segment is projected to grow at the fastest CAGR of 22.5% from 2026 to 2033, as advances in molecular biology and viral‑vector technology accelerate the development of curative or disease‑modifying treatments. Gene therapy offers the promise of targeting the root genetic mutation responsible for Camurati‑Engelmann Disease, which could lead to long-term disease stabilization or reversal. Investment from biotechnology companies and academic research labs is increasing rapidly. The potential for one‑time or infrequent dosing is attractive to patients and payers. Early‑phase clinical trials and compassionate use programs further drive interest. As safety and delivery technologies improve, gene therapy adoption is expected to expand across specialty centers.

- By Diagnosis

On the basis of diagnosis, the market is segmented into X‑ray, molecular genetic testing, and others. The X‑ray segment dominated the largest market revenue share of 48.9% in 2025, largely because X‑ray imaging remains the most accessible and cost-effective means to detect characteristic bone thickening, periosteal reaction, and cortical hyperplasia in Camurati‑Engelmann Disease. Clinicians rely on X‑rays for initial diagnosis, monitoring disease progression, and evaluating treatment response. The technology is pervasive in radiology departments globally, including in less‑resourced settings. Its non-invasiveness and low radiation dose make it suitable for repeated use, especially in pediatric populations. Reimbursement coverage and standardized imaging protocols reinforce its widespread clinical adoption.

The molecular genetic testing segment is expected to grow at the fastest CAGR of 20.7% from 2026 to 2033, driven by increasing use of genetic panels targeting TGFB1 and other implicated genes. Genetic testing enables precise diagnosis, informs prognosis, and guides targeted treatment decisions. As sequencing costs decline and testing becomes more integrated into clinical workflows, physicians are more frequently ordering tests for suspected cases. Growing awareness of genotype‑phenotype correlations and patient demand for personalized therapy support growth. Expansion of genetic counseling services and rare disease centers further accelerates adoption.

- By Dosage

On the basis of dosage, the market is segmented into tablet, injection, capsule, and others. The tablet segment dominated the largest market revenue share of 44.5% in 2025, due to patient preference for oral dosing, ease of administration, and the suitability of tablets for long-term maintenance therapy with corticosteroids, losartan, NSAIDs, and bisphosphonates. Tablets are widely manufactured, available in multiple strengths, and easy to store, which supports strong market penetration. They enable flexible dosing adjustments and improved adherence, especially in outpatient settings. Healthcare providers favor tablets for chronic management and follow-up therapy.

The injection segment is expected to witness the fastest CAGR of 18.8% from 2026 to 2033, fueled by growing use of intramuscular or intravenous corticosteroids, bisphosphonates, and potential future injectable therapies in more severe or rapidly progressing cases. Injectable treatments offer rapid onset of action, precise dose control, and are critical when oral absorption is limited or when high doses are needed acutely. Increasing hospital and clinic-based infusions drive adoption, especially for severe flares. Advancements in formulation and safety monitoring support increased use.

- By Route of Administration

On the basis of route of administration, the market is segmented into topical, intramuscular, intravenous, oral, and others. The oral route dominated the largest market revenue share of 46.2% in 2025, driven by its convenience, patient preference, and suitability for long-term therapies such as corticosteroids, losartan, and bisphosphonates. Oral administration allows self-administration at home, minimizing hospital visits and improving patient adherence. Its compatibility with chronic treatment regimens, flexible dosing schedules, and broad availability in pharmacies supports strong market penetration. Patients prefer oral therapy for ease of use, portability, and reduced discomfort compared to injections. The route is widely recommended by physicians for maintenance therapy and symptom management. Moreover, oral formulations are cost-effective, easily stored, and adaptable for both pediatric and adult populations. Health systems favor oral administration for outpatient management and long-term monitoring. The availability of multiple strengths and combination formulations further strengthens adoption.

The intravenous route is expected to witness the fastest CAGR of 17.5% from 2026 to 2033, as IV-administered therapies, including corticosteroids, bisphosphonates, and experimental agents, are increasingly used in severe cases or induction therapy requiring close supervision. Hospitals and specialty clinics are expanding infusion infrastructure to accommodate growing demand. IV administration ensures rapid onset of action, precise dosing, and effective delivery of medications with limited oral absorption. Increasing clinical adoption for acute symptom management and complex cases drives market growth. Improved protocols, safety measures, and patient monitoring systems further support uptake. Emerging therapies requiring hospital-based administration contribute to the fast CAGR. Physician preference for IV therapy in critically ill patients also reinforces adoption.

- By End‑Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. Hospitals dominated the largest market revenue share of 53.8% in 2025, supported by their ability to provide comprehensive care, including diagnostics, surgery, IV therapy, and multidisciplinary management. Hospitals offer access to specialized services such as radiology, molecular genetic testing, and infusion facilities, which are critical for Camurati‑Engelmann Disease patients. Their capacity to manage severe cases, coordinate long-term care, and provide emergency interventions strengthens their market dominance. Moreover, hospitals often participate in clinical trials and offer access to newer therapies, further consolidating their position.

The clinics segment is expected to witness the fastest CAGR of 16.9% from 2026 to 2033, driven by the increasing adoption of outpatient care, follow-up management, and community-based treatment models. Clinics provide convenient access for routine monitoring, prescription refills, and minor interventions, reducing the burden on hospitals. The rise of specialized rare-disease clinics and telemedicine integration accelerates patient reach. Clinics enable cost-effective long-term management while maintaining continuity of care, contributing to faster growth in the segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The retail pharmacy segment dominated the largest market revenue share of 47.6% in 2025, due to wide accessibility, patient familiarity, and availability of chronic medications such as corticosteroids, NSAIDs, losartan, and bisphosphonates. Retail pharmacies offer high-volume dispensing, convenient refill services, and strong patient engagement. Their widespread presence ensures reliable access to medications across urban and rural areas, supporting steady market growth.

The online pharmacy segment is expected to witness the fastest CAGR of 21.3% from 2026 to 2033, fueled by rising digital health adoption, increasing e-commerce penetration, and growing demand for home delivery of prescription medications. Patients with rare and chronic diseases increasingly rely on online pharmacies for convenience, timely access, and privacy. Expanding digital platforms, subscription models, and telemedicine integration further support adoption. Online channels also facilitate access to hard-to-find medications and improve adherence through home delivery, driving rapid growth in this segment.

Camurati-Engelmann Disease Treatment Market Regional Analysis

- North America dominated the Camurati-Engelmann Disease Treatment market with the largest revenue share of 38.9% in 2025, supported by strong diagnostic infrastructure, high awareness of rare genetic skeletal disorders, robust healthcare spending, and active research collaborations

- The U.S. leads the region due to wide access to genetic screening, availability of orphan-disease specialists, and increased participation in clinical research for rare bone dysplasias. Early adoption of advanced therapeutic options such as corticosteroids, NSAIDs, and gene therapy also strengthens market dominance

- Consumers and healthcare providers in the region increasingly value effective, non-invasive, and well-monitored treatment regimens for Camurati-Engelmann Disease. This widespread adoption is further supported by insurance coverage, specialized hospitals, and clinical centers of excellence for rare bone disorders

U.S. Camurati-Engelmann Disease Treatment Market Insight

The U.S. market captured the largest revenue share within North America in 2025, driven by advanced diagnostic facilities, widespread availability of genetic counseling, and the growing number of clinical trials targeting rare skeletal dysplasias. The country benefits from strong funding for orphan diseases, increasing awareness among healthcare professionals, and rising adoption of personalized treatment approaches, such as gene therapy and targeted pharmacological interventions. These factors collectively contribute to rapid market growth.

Europe Camurati-Engelmann Disease Treatment Market Insight

The European market is projected to expand at a CAGR of 7.1% during the forecast period, primarily driven by early diagnosis, increasing availability of genetic testing, and rising investments in rare disease research. Countries such as Germany, the UK, and France are witnessing enhanced adoption of pharmacological and surgical treatment options, supported by robust healthcare systems and reimbursement policies for rare diseases.

U.K. Camurati-Engelmann Disease Treatment Market Insight

The UK market is expected to grow at a notable CAGR of 7.4%, fueled by government initiatives for early detection of hereditary disorders, the availability of specialized clinics for skeletal dysplasias, and increasing awareness of Camurati-Engelmann Disease among healthcare professionals and patients. The adoption of both conventional pharmacological treatments and experimental gene therapies is expected to further support market expansion.

Germany Camurati-Engelmann Disease Treatment Market Insight

Germany’s market is anticipated to expand at a CAGR of 7.2%, supported by well-established diagnostic centers, proactive rare disease screening programs, and ongoing clinical research into bone remodeling therapies. Patients benefit from access to advanced pharmacological therapies, orthopedic interventions, and emerging gene-based treatments.

Asia-Pacific Camurati-Engelmann Disease Treatment Market Insight

The Asia-Pacific market is expected to grow at the fastest CAGR of 8.5% from 2026 to 2033, driven by rapidly expanding healthcare access, increasing focus on rare disease diagnosis, rising medical genetics facilities, and government initiatives to improve early detection of hereditary disorders in countries such as China, Japan, India, and South Korea. Growth is further supported by the expansion of specialty hospitals, increased awareness of rare skeletal disorders, and gradual adoption of gene therapy programs.

Japan Camurati-Engelmann Disease Treatment Market Insight

Japan’s market is gaining momentum due to a well-established healthcare system, high accessibility to genetic testing, and growing research on rare skeletal diseases. The market is further supported by increasing adoption of pharmacological treatments and specialized orthopedic interventions for symptom management. Japan is projected to register a CAGR of 8.1% during the forecast period.

China Camurati-Engelmann Disease Treatment Market Insight

China accounted for the largest revenue share in the Asia-Pacific region in 2025, attributed to rising awareness of rare diseases, expanding healthcare infrastructure, and increasing participation in clinical trials. Government policies promoting early diagnosis and treatment, coupled with growing availability of pharmacological therapies, gene therapy trials, and specialized clinics, are expected to accelerate market growth. The market is projected to grow at a CAGR of 8.7% from 2026 to 2033.

Camurati-Engelmann Disease Treatment Market Share

The Camurati-Engelmann Disease Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- Sobi (Sweden)

- Amgen Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

- Sanofi S.A. (France)

- Shire (Ireland)

- Horizon Therapeutics (U.S.)

- Takeda Pharmaceutical Company (Japan)

- Regeneron Pharmaceuticals (U.S.)

- BioMarin Pharmaceutical Inc. (U.S.)

Latest Developments in Global Camurati-Engelmann Disease Treatment Market

- In March 2023, a case‑based review was published in the European Journal of Rheumatology describing a 20‑year‑old male patient with Camurati‑Engelmann Disease (CED) who was treated with zoledronic acid, showing good clinical response, highlighting the potential benefit of bisphosphonates in disease management

- In May 2022, a case report documented improvement in bone health and initiation of puberty in an 18‑year-old female CED patient treated with a combination of glucocorticoid (prednisone) and losartan over 28 months, suggesting a new therapeutic benefit beyond pain control

- In August 2022, research showed that a bone‑targeted delivery system for TGF‑β type 1 receptor inhibitor dramatically improved bone remodeling in a mouse model of CED, using an alendronate-conjugate to minimize side effects

- In April 2025, a novel TGFB1 gene variant (an in-frame duplication) was reported in a CED patient who responded well to alendronate therapy, expanding the known genotype–phenotype spectrum and suggesting the utility of bisphosphonates in certain genetic subtypes

- In October 2025, a conference presentation reported that infliximab, a TNF-α inhibitor, was used successfully in a 17-year-old adolescent with refractory bone pain due to CED, showing pain reduction where steroids and losartan had limited effect

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.