Global Cancer Spit Test Market

Market Size in USD Million

USD

665.06 Million

USD

1,394.80 Million

2025

2033

USD

665.06 Million

USD

1,394.80 Million

2025

2033

| 2026 - 2033 | |

| USD 665.06 Million | |

| USD 1,394.80 Million | |

| % | |

|

Cancer Spit Test Market Overview

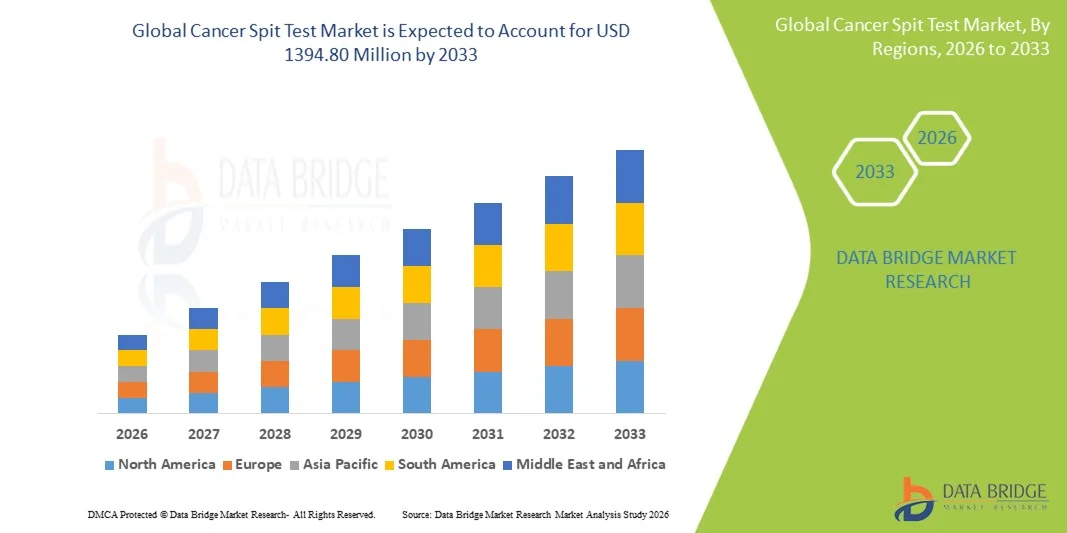

The Cancer Spit Test Market was valued at USD 665.06 Million in 2025 and is projected to reach USD 1394.80 Million by 2033, growing at a CAGR of 9.70% from 2026 to 2033. The Cancer Spit Test Market is experiencing steady growth driven by increasing demand for non-invasive, early-stage cancer screening solutions and rapid advancements in liquid biopsy and saliva-based diagnostic technologies. Rising awareness about early cancer detection, coupled with growing preference for painless and easily accessible diagnostic methods, is accelerating the adoption of spit-based testing across clinical laboratories, diagnostic centers, and home-testing platforms. Expanding applications in oral cancer, lung cancer, and emerging multi-cancer early detection panels are further strengthening market growth.

The increasing global cancer burden, along with government-led screening initiatives and expanding preventive healthcare programs, is significantly driving demand for rapid and cost-effective diagnostic alternatives. Saliva-based cancer testing is gaining traction due to its simplicity, lower cost compared to blood-based biopsies, and potential for large-scale population screening. In addition, continuous innovation in molecular diagnostics, including biomarker identification, PCR-based saliva assays, and next-generation sequencing integration, is enabling higher accuracy and broader clinical utility, positioning spit-based cancer testing as an emerging segment within the global oncology diagnostics landscape.

Key Market Trends & Insights

- North America dominated the Cancer Spit Test Market with the largest revenue share of 34.2% in 2025, supported by advanced molecular diagnostics infrastructure, high adoption of non-invasive cancer screening technologies, strong presence of key diagnostic companies, and favorable reimbursement frameworks for early cancer detection tests. The region also benefits from extensive use of saliva-based diagnostics in oncology screening programs and precision medicine initiatives.

- The Adult segment dominated the market in 2025 with 72.9% share, driven by higher cancer prevalence in adult populations and widespread screening initiatives targeting middle-aged and elderly individuals.

- Asia-Pacific is expected to be the fastest-growing region in the Cancer Spit Test Market, projected to expand at a CAGR of 8.1% from 2026 to 2033, fueled by rising cancer incidence, expanding diagnostic infrastructure, increasing awareness of non-invasive screening methods, and growing investments in healthcare modernization across China, India, and Japan.

- Oral Swab-based collection methods are the fastest-growing segment, projected to register a CAGR of 7.6% from 2026 to 2033, due to their low cost, high patient compliance, and suitability for large-scale population screening programs.

- The Sub-Mandibular/Sub-Lingual Gland collection site segment dominated the market with a 41.3% share in 2025, owing to higher saliva yield quality and strong biomarker concentration used for cancer detection assays.

- Hospitals dominated the End User segment with a revenue share in 2025, driven by increasing integration of saliva-based diagnostic testing into routine oncology screening and pre-treatment evaluation workflows.

- The Colon and Rectal Cancer application segment accounted for the largest share in 2025, supported by rising global prevalence of colorectal cancer and increasing demand for early, non-invasive detection methods.

Market Size & Forecast

- Global Market Value (2025): USD 665.06 Million

- Expected Market Value (2033): USD 1394.80 Million

- Forecast CAGR (2026–2033): 9.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Cancer Spit Test Market Segmentation

|

Attributes |

Cancer Spit Test Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Illumina Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Non-Invasive Multi-Cancer Early Detection (MCED) Programs · Integration of AI and Molecular Biomarker Discovery Platforms · Rising Adoption of Home-Based and Point-of-Care Testing Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Cancer Spit Test Market Trends

Trend: Rising Adoption of Non-Invasive Liquid Biopsy and Saliva-Based Cancer Detection

The Cancer Spit Test Market is witnessing strong growth due to increasing adoption of non-invasive diagnostic techniques based on saliva biomarkers, including DNA methylation patterns, circulating tumor DNA (ctDNA), microRNA profiling, and exosomal biomarkers. Saliva-based diagnostics are gaining traction as an alternative to blood-based liquid biopsy due to their painless collection, low cost, and suitability for large-scale screening programs. Studies have shown that saliva contains more than 1,000 detectable proteins and nucleic acids linked to systemic diseases, making it a viable medium for early cancer detection. Increasing clinical research in cancers such as oral, lung, breast, and pancreatic cancer is accelerating commercialization of saliva-based diagnostic kits. For instance, companies like Viome and Grail-type liquid biopsy developers are actively exploring multi-cancer early detection (MCED) approaches, including saliva-derived biomarker platforms in R&D pipelines, highlighting strong innovation momentum in this segment.

Cancer Spit Test Market Dynamics

Key Market Driver: Expansion of At-Home and Decentralized Cancer Screening

The Cancer Spit Test Market is experiencing strong growth due to the rapid expansion of at-home saliva-based sample collection kits and decentralized diagnostic models, allowing patients to collect samples without hospital visits. This shift gained significant momentum post-2021, driven by rising demand for preventive healthcare, early cancer detection, and remote diagnostic solutions. Clinical pilot programs and screening initiatives have shown that saliva-based testing can achieve patient compliance rates exceeding 85–90%, significantly higher than traditional invasive biopsy or hospital-based sampling methods. This high acceptance rate is encouraging diagnostic companies to expand direct-to-consumer (DTC) testing models, mail-in saliva kits, and home-based cancer screening services, particularly across North America and Europe, where healthcare infrastructure and consumer awareness are highly developed.

Key Restraint/Challenge: Limited Clinical Validation and Regulatory Standardization

A major restraint in the Cancer Spit Test Market is the lack of large-scale clinical validation and standardized regulatory approval frameworks for saliva-based cancer diagnostics. While saliva contains promising biomarkers such as DNA methylation markers, microRNAs, and tumor-derived exosomes, many diagnostic platforms are still in early-to-mid clinical development stages, limiting widespread clinical adoption. In addition, variability in sample collection methods (passive drool, oral swab, gland-specific collection) and differences in biomarker expression across populations create challenges in achieving consistent diagnostic accuracy. Regulatory agencies such as the FDA and EMA require extensive multi-phase clinical trials, increasing time-to-market and development costs. This lack of harmonization continues to slow commercialization and restricts adoption in routine oncology screening programs, particularly in cost-sensitive healthcare systems.

Key Market Opportunity: Integration of AI and Multi-Cancer Early Detection Platforms

The integration of artificial intelligence (AI) and machine learning into saliva-based cancer diagnostics presents a major growth opportunity in the Cancer Spit Test market. AI-enabled diagnostic platforms can analyze complex salivary biomarker patterns, improve classification accuracy, and enable early-stage multi-cancer risk prediction from a single non-invasive sample. Recent research studies have demonstrated that AI-driven biomarker interpretation models can improve diagnostic accuracy by 15–25% compared to conventional analytical methods, particularly in early cancer detection applications. Furthermore, advancements in multi-cancer early detection (MCED) technologies, combined with expanding investments in precision oncology, digital pathology, and tele-diagnostics, are enabling broader adoption of saliva-based testing. Increasing healthcare digitization in Asia-Pacific, along with strong DTC diagnostic adoption in North America and Europe, is further accelerating market expansion and creating new commercial opportunities for next-generation cancer screening platforms.

Cancer Spit Test Market Scope

The Global Cancer Spit Test Device Market is segmented on the basis of product type, site of collection, application, age group, method of collection, end user, and distribution channel.

- By Product Type

On the basis of product type, the global Cancer Spit Test Device market is segmented into saliva collection kits, fluid-specific devices, oral swabs, bar-code labels, saliva cryostorage boxes, and others. The Saliva Collection Kits segment dominated the market in 2025 with 38.6% share, owing to its standardized design, ease of use, and high compatibility with molecular diagnostic workflows. These kits are widely adopted in hospitals, diagnostic laboratories, and cancer research institutes for large-scale screening programs. Increasing demand for non-invasive sample collection methods has significantly strengthened their dominance. Integration with PCR and next-generation sequencing platforms further enhances clinical utility. Rising adoption in population-wide cancer screening initiatives is boosting volume demand. Strong preference for self-collection kits in home-based diagnostics is supporting market penetration. In addition, improved sample stability and reduced contamination risk make them highly reliable. Regulatory approvals for saliva-based diagnostic kits are expanding globally. Pharmaceutical and biotech companies are investing heavily in kit innovation. Automation in sample processing is further increasing efficiency.

The Oral Swab segment is expected to grow at the fastest CAGR of 11.4%, driven by increasing demand for low-cost, rapid, and minimally invasive sampling methods. Growing adoption in decentralized and point-of-care testing is accelerating usage. Expanding cancer screening awareness programs in emerging economies is supporting uptake. Improved biomarker detection accuracy in oral swab technologies is enhancing clinical acceptance. Rising use in at-home testing kits and telehealth diagnostics is boosting accessibility. Integration with AI-based diagnostic platforms is improving result interpretation. Portable testing kits using oral swabs are gaining traction in rural healthcare systems. Demand for rapid cancer risk assessment tools is increasing globally. Pharmaceutical companies are expanding product pipelines in this category. Technological improvements in DNA/RNA extraction are improving sensitivity. Cost-effectiveness compared to traditional biopsy methods supports adoption. Increasing consumer-driven diagnostics is further strengthening growth momentum.

- By Site of Collection

On the basis of site of collection, the market is segmented into sub-mandibular/sub-lingual gland, parotid gland, and minor salivary gland. The Sub-Mandibular/Sub-Lingual Gland segment dominated the market in 2025 with 44.2% share due to its high saliva output and rich biomarker concentration, making it ideal for cancer detection assays. This site provides consistent and high-quality samples suitable for genomic and proteomic analysis. It is widely preferred in clinical diagnostics due to ease of access and minimal patient discomfort. Increasing adoption in oral and systemic cancer screening programs is supporting its dominance. Strong clinical validation of biomarkers derived from sub-lingual saliva is reinforcing usage. Integration with automated collection devices improves sample standardization. Hospitals and diagnostic labs prefer this site for routine testing. Research institutions rely on it for biomarker discovery studies. Growing use in large-scale epidemiological screening is further boosting demand. Regulatory acceptance of standardized saliva collection protocols is increasing.

The Minor Salivary Gland segment is expected to grow at the fastest CAGR of 10.6%, driven by its increasing use in specialized cancer biomarker detection. These glands provide highly localized molecular signatures useful in early-stage cancer identification. Rising R&D activity in precision oncology is fueling adoption. Advanced micro-sampling techniques are improving feasibility. Increasing focus on early oral cancer detection supports demand. Improved diagnostic sensitivity from localized gland sampling is boosting clinical interest. Academic research in salivary diagnostics is expanding rapidly. Adoption in personalized medicine applications is increasing. Technological advancements in microfluidic sampling devices are supporting growth. Rising investment in biomarker discovery is strengthening innovation pipelines. Expanding oncology research funding is accelerating development. Growing precision diagnostics adoption is reinforcing segment expansion.

- By Application

On the basis of application, the global Cancer Spit Test Device market is segmented into liver-lung cancer, breast cancer, colon and rectal cancer, prostate cancer, pancreatic cancer, oral cancer, thyroid cancer, endometrial cancer, kidney cancer, leukemia, melanoma, non-Hodgkin lymphoma, and others. The Oral Cancer segment dominated the market in 2025 with 31.8% share, owing to direct relevance of saliva-based diagnostics in detecting oral epithelial abnormalities and precancerous lesions. High global prevalence of oral cancer, especially in Asia-Pacific, is significantly driving demand. Saliva provides direct exposure to oral biomarkers, improving diagnostic accuracy. Government-led oral cancer screening programs are boosting adoption. Increasing tobacco and alcohol-related cancer risk is supporting screening expansion. Dental clinics and ENT specialists widely use spit-based tests. Early detection initiatives are strengthening clinical acceptance. Integration with AI-based imaging and molecular profiling is improving sensitivity. Rising awareness campaigns are increasing patient participation. Hospital-based screening programs are expanding globally.

The Pancreatic Cancer segment is expected to grow at the fastest CAGR of 12.1%, driven by extremely high mortality and urgent demand for early detection tools. Lack of effective early-stage diagnostics is driving innovation in saliva-based biomarker discovery. Increasing R&D funding in liquid biopsy technologies is accelerating development. Pharmaceutical companies are investing in early detection panels. AI-enabled multi-cancer detection platforms are supporting progress. Growing focus on non-invasive screening for high-risk populations is increasing adoption. Clinical trials are expanding globally for saliva-based pancreatic markers. Rising precision oncology initiatives are boosting research funding. Technological advancements in proteomic profiling are improving detection accuracy. Multi-omics integration is enhancing diagnostic sensitivity. Expanding cancer genomics research is strengthening innovation. Unmet clinical need is driving strong commercialization momentum.

- By Age Group

On the basis of age group, the market is segmented into adult and pediatric populations. The Adult segment dominated the market in 2025 with 72.9% share, driven by higher cancer prevalence in adult populations and widespread screening initiatives targeting middle-aged and elderly individuals. Adults are more frequently exposed to lifestyle-related cancer risk factors such as smoking, diet, and environmental exposure. Most clinical trials and diagnostic programs are adult-focused. Hospitals prioritize adult cancer screening programs. Insurance coverage is higher for adult diagnostic procedures. Saliva-based tests are widely adopted in workplace screening programs. Rising awareness of preventive oncology among adults is increasing participation. Diagnostic companies focus product development on adult biomarkers. Government screening programs target adult populations for early detection. Aging global population is further strengthening dominance.

The Pediatric segment is expected to grow at the fastest CAGR of 10.2%, driven by increasing focus on early detection of genetic and rare cancers in children. Advances in pediatric oncology diagnostics are enabling safer testing alternatives. Non-invasive saliva testing is preferred over blood-based methods in children. Rising incidence of pediatric leukemia and lymphoma is supporting demand. Governments are investing in childhood cancer screening programs. Research institutions are developing pediatric-specific biomarkers. Awareness campaigns in pediatric hospitals are increasing adoption. Technological advancements in low-volume sampling are improving feasibility. Increasing parental preference for painless diagnostics is boosting growth. Expanding pediatric oncology research networks are strengthening innovation. Rising genomic screening in children is supporting adoption. Clinical pipeline expansion is accelerating growth.

- By Method of Collection

On the basis of method of collection, the market is segmented into passive drool, oral swab, and others. The Passive Drool segment dominated the market in 2025 with 46.7% share due to its high sample purity and minimal contamination risk, making it ideal for molecular and genomic testing. It provides consistent saliva volume, improving diagnostic accuracy. Widely used in laboratory-based cancer research and clinical validation studies. Strong adoption in large-scale population screening programs. Compatibility with automated diagnostic systems supports efficiency. Hospitals prefer passive drool for standardized testing. Research institutes rely on it for biomarker discovery. Increasing use in biobanking applications is supporting growth. High reproducibility strengthens clinical reliability. Regulatory guidelines support its standardized usage.

The Oral Swab segment is expected to grow at the fastest CAGR of 11.0%, driven by convenience, affordability, and suitability for at-home testing. Increasing adoption in decentralized diagnostics is driving demand. Rapid sample collection makes it ideal for mass screening. Growing telehealth integration is supporting usage. Rising consumer preference for self-testing kits is boosting adoption. Technological improvements in swab-based DNA extraction are enhancing accuracy. Expansion of point-of-care testing infrastructure is accelerating growth. Pharmaceutical companies are focusing on swab-based diagnostic innovations. Increasing rural healthcare penetration supports uptake. Digital health ecosystems are enabling wider distribution. Consumer-driven preventive testing is strengthening demand.

- By End User

On the basis of end user, the market is segmented into hospitals, diagnostic laboratories, oncology specialty clinics, cancer research institutes, and others. The Diagnostic Laboratories segment dominated the market in 2025 with 39.4% share, driven by high testing volumes, advanced molecular diagnostic infrastructure, and strong adoption of liquid biopsy technologies. Laboratories handle large-scale cancer screening programs efficiently. Integration with automated sequencing platforms enhances throughput. Rising outsourcing of diagnostic testing supports demand. Strong presence of centralized lab networks boosts efficiency. High accuracy requirements in cancer detection favor lab-based testing. Partnerships with biotech firms are increasing. Expansion of reference laboratory chains is supporting dominance. Investment in high-throughput screening technologies is rising. Government screening programs rely heavily on diagnostic labs.

The Cancer Research Institutes segment is expected to grow at the fastest CAGR of 10.8%, driven by increasing investment in oncology research and biomarker discovery. Rising focus on early cancer detection technologies is accelerating adoption. Academic collaborations with biotech companies are expanding. Government funding for cancer research is increasing globally. Development of multi-cancer detection panels is boosting usage. Clinical trials for saliva-based diagnostics are rising. Precision oncology research is expanding rapidly. Adoption of AI-based molecular analysis is improving research outcomes. Increasing availability of genomic databases supports innovation. Translational research initiatives are strengthening commercialization. Rising biotech partnerships are accelerating discovery pipelines.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tenders, retail sales, and others. The Direct Tenders segment dominated the market in 2025 with 52.1% share due to large-scale procurement by hospitals, government health programs, and diagnostic networks. Bulk purchasing agreements ensure cost efficiency and supply consistency. Strong adoption in public healthcare screening initiatives supports dominance. Hospitals prefer direct procurement for standardized testing kits. Government cancer screening programs rely heavily on tender-based distribution. Long-term contracts with manufacturers stabilize supply chains. High-volume diagnostic deployment strengthens market share. Regulatory compliance requirements favor structured procurement systems. Institutional demand from laboratories supports growth. Strategic partnerships between manufacturers and healthcare systems are increasing.

The Retail Sales segment is expected to grow at the fastest CAGR of 11.6%, driven by rising consumer awareness and expansion of at-home cancer testing kits. Increasing availability of saliva-based kits in pharmacies and e-commerce platforms is driving accessibility. Growth of direct-to-consumer diagnostic models is accelerating adoption. Rising demand for preventive health screening supports retail expansion. Telehealth integration is boosting kit distribution. Online healthcare platforms are expanding rapidly. Consumer preference for privacy in cancer testing is increasing demand. Subscription-based diagnostic models are emerging. Improved affordability of test kits supports penetration. Digital health ecosystems are enabling rapid scaling. Preventive healthcare awareness is strengthening adoption globally.

Cancer Spit Test Market Regional Analysis

North America dominated the Cancer Spit Test Market and accounted for the largest revenue share of 34.2% in 2025, supported by advanced molecular diagnostics infrastructure, high adoption of non-invasive cancer screening technologies, strong presence of key diagnostic companies, and favorable reimbursement frameworks for early cancer detection tests. The region also benefits from extensive integration of saliva-based diagnostics into oncology screening programs, precision medicine initiatives, and multi-cancer early detection workflows. Increasing investment in liquid biopsy technologies, DNA methylation-based assays, and saliva biomarker validation studies is further strengthening market leadership. The presence of well-established clinical laboratories and strong regulatory pathways from agencies such as the U.S. FDA continues to accelerate commercialization of saliva-based cancer diagnostic solutions.

U.S. Cancer Spit Test Market Insight

The U.S. Cancer Spit Test market is witnessing strong growth due to rising adoption of early cancer screening programs and non-invasive diagnostic technologies. The country has a highly developed molecular diagnostics ecosystem, with increasing utilization of saliva-based testing in oral, colorectal, and multi-cancer screening applications. Strong presence of diagnostic leaders and biotech innovators is driving R&D in salivary DNA, microRNA, and exosome-based cancer detection platforms. In addition, favorable reimbursement structures and growing preventive healthcare awareness are accelerating adoption across hospitals, diagnostic laboratories, and oncology clinics.

Europe Cancer Spit Test Market Insight

Europe remains a key contributor to the Cancer Spit Test Market, driven by strong healthcare systems, rising cancer screening initiatives, and increasing adoption of non-invasive diagnostic technologies. Countries such as Germany, France, and the U.K. are actively expanding population-based cancer screening programs, supporting demand for saliva-based diagnostic solutions. The region benefits from strong regulatory oversight by the European Medicines Agency (EMA), ensuring high-quality validation of diagnostic tests. Increasing focus on early detection of oral, breast, and colorectal cancers is further supporting market expansion.

U.K. Cancer Spit Test Market Insight

The U.K. Cancer Spit Test market is growing steadily due to increasing emphasis on early cancer detection under public healthcare systems such as the NHS. Rising adoption of non-invasive saliva-based diagnostic tools is supporting screening for oral and systemic cancers.

The country is also witnessing increased research collaborations between academic institutions and biotech firms focused on liquid biopsy and salivary biomarker discovery, strengthening innovation in cancer diagnostics.

Germany Cancer Spit Test Market Insight

Germany represents one of the most advanced oncology diagnostics markets in Europe, driven by strong healthcare infrastructure and high adoption of precision medicine-based cancer screening approaches. Increasing prevalence of cancer and strong demand for early detection tools are driving uptake of saliva-based diagnostic tests. The country is also investing heavily in biomarker research, molecular diagnostics platforms, and AI-assisted cancer detection systems, supporting long-term market growth.

Asia-Pacific Cancer Spit Test Market Insight

The Asia-Pacific region is expected to be the fastest-growing market, projected to expand at a CAGR of 8.1% from 2026 to 2033, driven by rising cancer incidence, expanding diagnostic infrastructure, and increasing awareness of non-invasive screening methods. Rapid healthcare modernization in countries such as China, India, and Japan is significantly boosting adoption of saliva-based cancer testing solutions. Growing investments in hospital diagnostics, private laboratory networks, and at-home screening programs are accelerating market penetration. In addition, increasing government initiatives focused on early cancer detection and preventive healthcare are further supporting regional growth.

Japan Cancer Spit Test Market Insight

Japan’s Cancer Spit Test market is expanding steadily due to its aging population and high focus on early disease detection and preventive healthcare. Increasing adoption of advanced molecular diagnostic tools is supporting saliva-based testing in cancer screening programs. Strong R&D activity in biomarker discovery and liquid biopsy technologies is further enhancing the development of next-generation cancer diagnostic solutions in the country.

China Cancer Spit Test Market Insight

China is emerging as one of the fastest-growing markets for Cancer Spit Test diagnostics, driven by rising cancer burden, expanding healthcare infrastructure, and increasing investment in precision oncology and molecular diagnostics. The country is witnessing rapid adoption of saliva-based screening tools, AI-enabled diagnostic platforms, and large-scale population screening programs, supported by government healthcare modernization initiatives. Increasing awareness of early cancer detection is significantly boosting demand across hospitals and diagnostic laboratories.

Cancer Spit Test Market Share

The Cancer Spit Test industry is primarily led by well-established companies, including:

- Illumina Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Qiagen N.V. (Germany)

- Roche Diagnostics (Switzerland)

- Bio-Rad Laboratories Inc. (U.S.)

- Agilent Technologies Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Danaher Corporation (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Guardant Health Inc. (U.S.)

- Exact Sciences Corporation (U.S.)

- GRAIL Inc. (U.S.)

- Natera Inc. (U.S.)

- Myriad Genetics Inc. (U.S.)

- PerkinElmer Inc. (U.S.)

- BGI Genomics Co. Ltd. (China)

- Burning Rock Biotech Limited (China)

- Bio-Techne Corporation (U.S.)

- Hologic Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Cepheid (U.S.)

- Epigenomics AG (Germany)

- OPKO Health Inc. (U.S.)

- Lucence Diagnostics (Singapore)

- Chronix Biomedical (U.S.)

- Freenome Holdings Inc. (U.S.)

- DELFI Diagnostics Inc. (U.S.)

- Precipio Inc. (U.S.)

- Angle PLC (U.K.)

- Genomic Health (U.S.)

- NeoGenomics Laboratories Inc. (U.S.)

Latest Developments in Cancer Spit Test Market

- In July 2022, multiple oncology diagnostic companies increased investment in liquid biopsy technologies, with a strong focus on expanding sample types to include saliva alongside blood and urine. The period saw rising commercialization activity in minimally invasive cancer detection tools, driven by demand for early screening and precision oncology applications across hospitals and diagnostic laboratories

- In February 2023, scientific reviews and clinical research publications reinforced the role of liquid biopsy, including saliva-based diagnostics, in early cancer detection and monitoring. Studies emphasized the growing clinical adoption of non-solid biological samples for identifying tumor biomarkers, supporting the shift toward non-invasive cancer screening approaches in global healthcare systems

- In November 2023, advancements in salivary diagnostics highlighted the detection of circulating tumor DNA and RNA in saliva using next-generation molecular techniques, strengthening the scientific foundation for saliva-based cancer testing platforms. These developments supported ongoing innovation in multi-cancer early detection and precision oncology tools

- In May 2024, global cancer diagnostics companies accelerated development of saliva-based testing kits as part of broader liquid biopsy expansion, supported by rising demand for non-invasive, at-home, and point-of-care cancer screening solutions. The market also saw increasing integration of AI-based analytics to improve biomarker interpretation accuracy and early detection capabilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.