Global Candida Infections Drugs Market

Market Size in USD Billion

USD

16.86 Billion

USD

23.07 Billion

2025

2033

USD

16.86 Billion

USD

23.07 Billion

2025

2033

| 2026 - 2033 | |

| USD 16.86 Billion | |

| USD 23.07 Billion | |

| % | |

|

Candida Infections Drugs Market Overview

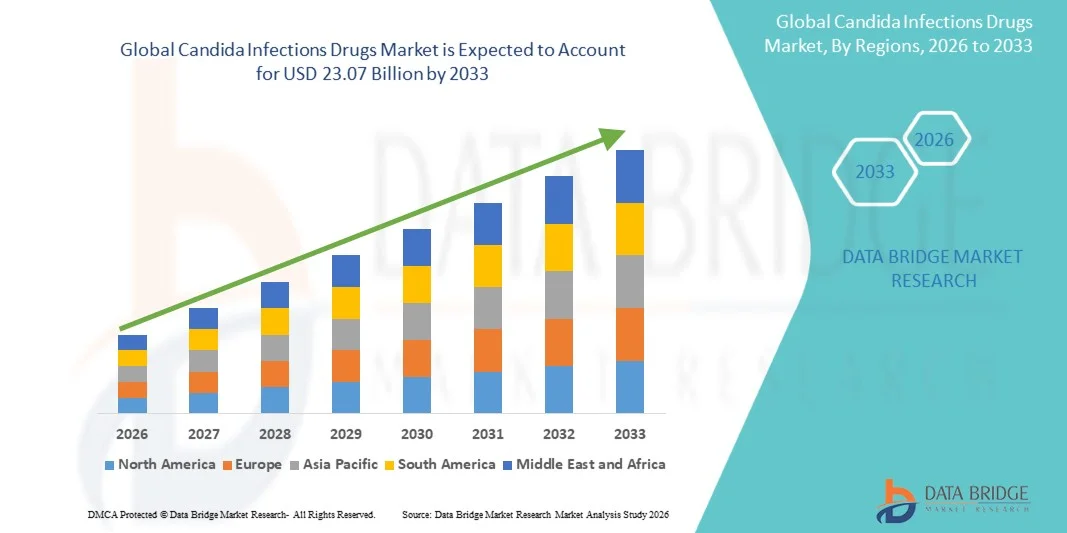

The Candida Infections Drugs Market was valued at USD 16.86 billion in 2025 and is projected to reach USD 23.07 billion by 2033, growing at a CAGR of 4.00% from 2026 to 2033. The market is witnessing steady growth driven by the rising prevalence of fungal infections, increasing incidence of immunocompromised conditions, and continuous advancements in antifungal drug development and treatment strategies.

The growing burden of invasive and mucocutaneous candidiasis worldwide, particularly among patients with cancer, HIV/AIDS, diabetes, organ transplants, and intensive care unit admissions, is driving demand for effective antifungal therapies. In addition, increasing awareness of early diagnosis, expanding healthcare access in emerging economies, and the introduction of novel antifungal agents targeting drug-resistant Candida species are encouraging hospitals, specialty clinics, and healthcare providers to adopt advanced treatment options, improving patient outcomes and supporting market expansion.

Key Market Trends & Insights

- North America dominated the Candida Infections Drugs Market with the largest revenue share of 38.42% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates, and strong availability of antifungal therapies.

- The Vaginal Yeast Infection segment led the market with a 34.82% share in 2025, driven by its high global prevalence among women, frequent recurrence rates, and widespread awareness leading to early diagnosis and treatment.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by increasing healthcare expenditure, growing awareness of fungal infections, and expanding access to antifungal treatments.

- Oral Thrush are the fastest-growing type, projected to register a CAGR of 7.3%, reflecting the surge in prevalence of immunocompromised populations, including cancer patients, transplant recipients, and individuals with HIV/AIDS.

- The Azoles segment dominated the drug type category with a 44.18% revenue share in 2025, led by their broad-spectrum antifungal activity, established clinical effectiveness, and extensive use across multiple Candida infection indications.

- Antibiotics accounted for 48.63% of the market, preferred by its significant association with Candida infection management pathways and its widespread use in healthcare settings where secondary fungal infections frequently occur.

- The Lozenges segment is the fastest-growing dosage form category, with a CAGR of 7.2%, driven by the increasing demand for targeted treatment of oral candidiasis and oral thrush.

Market Size & Forecast

- Global Market Value (2025): USD 16.86 Billion

- Expected Market Value (2033): USD 23.07 Billion

- Forecast CAGR (2026–2033): 4.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Candida Infections Drugs Market Segmentation

|

Attributes |

Candida Infections Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Pfizer Inc. (U.S.) · Merck & Co., Inc. (U.S.) · Gilead Sciences, Inc. (U.S.) · Astellas Pharma Inc. (Japan) · Bayer AG (Germany) · AbbVie Inc. (U.S.) · Novartis AG (Switzerland) · F. Hoffmann-La Roche Ltd (Switzerland) · Sanofi (France) · GSK plc (U.K.) · SCYNEXIS, Inc. (U.S.) · Cidara Therapeutics, Inc. (U.S.) · Basilea Pharmaceutica Ltd. (Switzerland) · Mayne Pharma Group Limited (Australia) · Alkem Laboratories Ltd. (India) · Cipla Ltd (India) · Sun Pharmaceutical Industries Ltd. (India) · Zydus Lifesciences Limited (India) · Dr. Reddy's Laboratories Ltd. (India) · Viatris Inc. (U.S.) |

|

Market Opportunities |

· Development of next-generation antifungal drugs targeting multidrug-resistant Candida species · Expansion of antifungal treatment access in emerging economies · Growing adoption of rapid fungal diagnostic technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Candida Infections Drugs Market Trends

Trend: Rising Focus on Novel Antifungal Therapies and Resistance Management

Healthcare providers and pharmaceutical companies are increasingly focusing on the development of novel antifungal therapies to address growing concerns related to drug-resistant Candida strains and treatment failures. The integration of advanced drug discovery technologies enables the identification of new molecular targets and mechanisms of action. Hospitals and infectious disease specialists are similarly adopting newer antifungal agents to improve clinical outcomes through evidence-based treatment protocols, while combination therapies and precision medicine approaches create more effective strategies that closely address evolving resistance patterns in Candida infections.

For instance, in April 2024, SCYNEXIS continued advancing ibrexafungerp development programs targeting serious fungal infections, reflecting the industry's emphasis on innovative antifungal treatment solutions.

Candida Infections Drugs Market Dynamics

Key Market Driver: Growing Prevalence of Immunocompromised Patient Populations

The increasing prevalence of immunocompromised conditions and chronic diseases has created substantial demand for effective candida infection drugs that can treat invasive and recurrent fungal infections across diverse patient populations. Hospitals, specialty clinics, and healthcare systems are utilizing antifungal therapies as a core component of infection management protocols, improving survival rates, reducing complications, and supporting better long-term patient outcomes through timely therapeutic intervention and disease control measures. For instance, in March 2024, Pfizer Inc. highlighted continued demand for antifungal therapies used in managing serious fungal infections among vulnerable and hospitalized patient groups.

Key Restraint/Challenge: Emergence of Antifungal Drug Resistance Across Healthcare Settings

A significant restraint in the Candida Infections Drugs Market is the increasing emergence of antifungal resistance among Candida species. Resistant infections reduce treatment effectiveness, complicate disease management, and increase healthcare costs associated with prolonged hospitalization and additional therapeutic interventions. The overall burden extends to the need for alternative treatment options, continuous surveillance programs, and expanded diagnostic capabilities, making infection control increasingly challenging for healthcare providers and public health authorities worldwide.

For instance, in 2024, the Centers for Disease Control and Prevention (CDC) continued reporting concerns regarding the spread of drug-resistant Candida auris in healthcare environments, highlighting the growing challenge of antifungal resistance.

Key Market Opportunity: Expansion of Next-Generation Antifungal Drug Development Programs

The development of next-generation antifungal therapies presents a significant market opportunity. Advanced drug candidates can target resistant Candida species, improve treatment efficacy, and support broader management of invasive fungal infections. The expansion of clinical research activities and regulatory support mechanisms is further accelerating innovation across antifungal therapeutics, opening growth opportunities across underserved markets in Asia-Pacific, Latin America, and the Middle East.

For instance, in June 2024, Cidara Therapeutics continued progressing its antifungal candidate portfolio aimed at addressing unmet needs in resistant fungal infection treatment, supporting future market growth potential.

Candida Infections Drugs Market Scope

The candida infections drugs market is segmented on the basis of type, drug type, treatment, dosage form, end-users, and distribution channel.

- By Type

On the basis of type, the Candida Infections Drugs Market is segmented into athletes foot, oral thrush, vaginal yeast infection, nail fungus, jock itch, and diaper rash. The Vaginal Yeast Infection segment dominated the market with an estimated 34.82% share in 2025, owing to its high global prevalence among women, frequent recurrence rates, and widespread awareness leading to early diagnosis and treatment. Hormonal fluctuations, antibiotic use, pregnancy, and diabetes remain major contributing factors driving patient volumes. The availability of numerous prescription and over-the-counter antifungal products has further strengthened treatment accessibility. Growing healthcare awareness campaigns and increasing consultations for women’s health issues continue to support demand. Pharmaceutical companies are also expanding product portfolios specifically targeting recurrent vulvovaginal candidiasis. The segment’s large patient population and recurring treatment requirements continue to sustain its market leadership.

The Oral Thrush segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by the increasing prevalence of immunocompromised populations, including cancer patients, transplant recipients, and individuals with HIV/AIDS. Rising use of immunosuppressive therapies and corticosteroids is contributing to higher incidence rates globally. Improved diagnostic capabilities are enabling earlier identification and treatment initiation. Healthcare providers are increasingly focusing on infection management among vulnerable patient groups. Growing geriatric populations and increasing prevalence of chronic diseases are further supporting market expansion. Continued development of targeted antifungal therapies is expected to accelerate segment growth throughout the forecast period.

- By Drug Type

On the basis of drug type, the Candida Infections Drugs Market is segmented into azoles, echinocandins, and other drugs. The Azoles segment accounted for the largest market share of 44.18% in 2025, driven by their broad-spectrum antifungal activity, established clinical effectiveness, and extensive use across multiple Candida infection indications. Drugs such as fluconazole, itraconazole, and voriconazole remain widely prescribed due to favorable efficacy and accessibility. The segment benefits from strong physician familiarity and comprehensive treatment guidelines supporting their use. Availability in multiple dosage forms further enhances patient compliance and treatment flexibility. Generic availability in many regions also contributes to widespread adoption. Their versatility across both superficial and systemic infections continues to reinforce segment dominance.

The Echinocandins segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing concerns regarding antifungal resistance and the rising prevalence of invasive candidiasis. These drugs offer strong efficacy against resistant Candida species and are increasingly recommended as first-line therapies in severe infections. Growing hospital admissions involving high-risk patients are supporting demand for advanced antifungal treatments. Continuous clinical evidence demonstrating favorable safety profiles is encouraging physician adoption. Expanding healthcare investments in critical care settings are further accelerating utilization. Increasing regulatory approvals and product innovation are expected to sustain rapid segment growth.

- By Treatment

On the basis of treatment, the Candida Infections Drugs Market is segmented into antibiotics, benzodiazepines, contraceptives and hormone replacement therapy. The Antibiotics segment dominated the market with an estimated 48.63% share in 2025 due to its significant association with Candida infection management pathways and its widespread use in healthcare settings where secondary fungal infections frequently occur. Extensive utilization across hospitals and outpatient facilities contributes to the large patient population requiring antifungal interventions. Increased awareness regarding antimicrobial stewardship has improved monitoring and management of fungal complications. Healthcare providers are emphasizing early diagnosis and treatment of opportunistic infections. Growing hospitalization rates and intensive care admissions continue to influence demand patterns. The segment maintains a substantial market presence due to its close relationship with Candida infection occurrence.

The Contraceptives and Hormone Replacement Therapy segment is projected to record the fastest growth at a CAGR of 6.9% from 2026 to 2033, supported by increasing awareness of hormonal influences on recurrent Candida infections. Rising use of hormone-based therapies among women is creating greater focus on preventive monitoring and treatment strategies. Healthcare professionals are increasingly recognizing hormonal factors contributing to infection recurrence. Expanding women's healthcare services are improving access to diagnosis and treatment options. Research activities examining the relationship between hormonal changes and fungal infections are also increasing. Greater patient education and specialized treatment approaches are expected to support future growth.

- By Dosage Form

On the basis of dosage form, the Candida Infections Drugs Market is segmented into gels and creams, lozenges, tablets, liquids, sprays, powders, and ointments. The Tablets segment held the largest market share of 31.74% in 2025, owing to ease of administration, strong patient compliance, and widespread prescription for both localized and systemic Candida infections. Oral antifungal tablets provide convenient dosing schedules and are commonly used in outpatient treatment settings. Their broad availability across healthcare systems further supports market penetration. Pharmaceutical manufacturers continue to invest in improved formulations to enhance therapeutic outcomes. Established clinical evidence and physician preference also contribute to segment leadership. The segment remains a cornerstone of antifungal treatment strategies worldwide.

The Lozenges segment is anticipated to experience the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing demand for targeted treatment of oral candidiasis and oral thrush. These formulations provide localized drug delivery directly to affected tissues, improving treatment effectiveness. Rising diagnosis rates of oral fungal infections among elderly and immunocompromised patients are supporting demand. Improved patient convenience and reduced systemic exposure are encouraging wider adoption. Healthcare professionals increasingly recommend localized therapies for mild to moderate infections. Product innovation and growing awareness of oral health management are expected to further accelerate segment expansion.

- By End-Users

On the basis of end-users, the Candida Infections Drugs Market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the market with a 46.27% share in 2025, driven by the high incidence of invasive candidiasis among hospitalized and critically ill patients. Hospitals serve as the primary treatment centers for severe fungal infections requiring intravenous antifungal administration and continuous monitoring. Increasing admissions to intensive care units contribute significantly to patient volumes. Advanced diagnostic infrastructure enables timely detection and management of complex infections. Growing prevalence of chronic diseases and immunosuppressive therapies further supports demand. Strong availability of specialized healthcare professionals continues to reinforce hospital segment leadership.

The Specialty Clinics segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, supported by increasing demand for specialized infectious disease and women's health services. These facilities provide focused treatment approaches and personalized patient management programs. Growing awareness of recurrent fungal infections is encouraging patients to seek specialist consultations. Improved access to advanced diagnostics and targeted therapies is enhancing treatment outcomes. Expanding healthcare networks and outpatient care models are further contributing to segment growth. The trend toward specialized care delivery is expected to sustain strong expansion throughout the forecast period.

- By Distribution Channel

On the basis of distribution channel, the Candida Infections Drugs Market is segmented into hospital pharmacy, retail pharmacy, online pharmacies, and others. The Hospital Pharmacy segment led the market with a 51.34% share in 2025, owing to the large volume of antifungal medications dispensed for hospitalized patients with invasive and severe Candida infections. Hospital pharmacies play a critical role in ensuring timely access to specialized antifungal therapies. The segment benefits from strong integration with inpatient treatment protocols and critical care services. Increasing utilization of intravenous antifungal drugs further supports hospital-based distribution. Continuous monitoring of medication use and treatment outcomes strengthens clinical effectiveness. The growing burden of hospital-acquired fungal infections continues to support segment dominance.

The Online Pharmacies segment is projected to register the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing digital healthcare adoption and growing consumer preference for convenient medication access. E-commerce platforms enable easier procurement of prescription refills and over-the-counter antifungal products. Expanding internet penetration and smartphone usage are supporting broader market reach. Competitive pricing and home delivery services are improving patient convenience. Regulatory advancements supporting digital healthcare ecosystems are also facilitating growth. The continued expansion of telemedicine services is expected to further accelerate online pharmacy adoption globally.

Candida Infections Drugs Market Regional Analysis

North America dominated the Candida Infections Drugs Market with the largest revenue share of 38.42% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates, and strong availability of antifungal therapies. The region also benefits from strong awareness of fungal infections, widespread availability of antifungal therapies, and growing adoption of advanced diagnostic technologies across hospitals, specialty clinics, and healthcare networks. Increasing prevalence of immunocompromised patient populations and rising incidence of invasive candidiasis continue to drive treatment demand. Ongoing investments in antifungal drug development and infectious disease management programs further strengthen North America’s leadership position in the global market.

U.S. Candida Infections Drugs Market Insight

The e U.S. candida infections drugs market is witnessing strong growth due to rising prevalence of fungal infections, increasing incidence of immunocompromised conditions, and growing investments in advanced antifungal therapies. The country’s well-established healthcare infrastructure, along with increasing adoption of novel antifungal drugs, rapid diagnostic technologies, and evidence-based treatment protocols, is driving demand across hospitals, specialty clinics, and outpatient care settings. In addition, growing emphasis on early diagnosis and management of invasive candidiasis is accelerating antifungal drug utilization across healthcare providers and patient populations.

Europe Candida Infections Drugs Market Insight

The Europe candida infections drugs market remains a major contributor to global revenue, driven by strong healthcare systems, continuous pharmaceutical innovation, and high demand for effective antifungal treatments. The widespread use of advanced antifungal therapies in hospitals, specialty clinics, and infectious disease management programs is supporting market expansion across the region. Increasing investments in fungal infection research, coupled with growing awareness of antifungal resistance and a highly developed healthcare network, continue to enhance the adoption of candida infection drugs throughout Europe.

U.K. Candida Infections Drugs Market Insight

The U.K. candida infections drugs market is experiencing steady growth, supported by rising awareness of fungal diseases, increasing diagnosis rates, and expanding access to advanced antifungal therapies. Growing investments in healthcare infrastructure and increasing demand for effective treatment solutions for recurrent and invasive Candida infections are contributing to market growth. Furthermore, integration of advanced diagnostic technologies and improved clinical management approaches is enhancing treatment outcomes, positioning the U.K. as a key market within the European candida infections drugs industry.

Germany Candida Infections Drugs Market Insight

The Germany candida infections drugs market is expanding steadily due to the country’s strong pharmaceutical sector, advanced healthcare capabilities, and increasing adoption of next-generation antifungal therapies. Healthcare providers, hospitals, and research institutions are increasingly utilizing innovative treatment options for managing invasive and drug-resistant Candida infections. Continuous advancements in antifungal drug development, diagnostic technologies, and infectious disease management, along with strong government focus on healthcare quality and patient safety, are further driving market growth in Germany.

Asia-Pacific Candida Infections Drugs Market Insight

The Asia-Pacific candida infections drugs market is expected to witness rapid growth, driven by increasing healthcare expenditure, expanding patient populations, and rising investments in infectious disease treatment infrastructure across countries such as China, India, and Japan. Growing awareness regarding fungal infections, rising adoption of advanced antifungal therapies, and increasing demand for accessible and effective treatment solutions are supporting regional market expansion. In addition, improving diagnostic capabilities and expanding healthcare access are accelerating antifungal drug adoption across hospitals and specialty care facilities.

Japan Candida Infections Drugs Market Insight

The Japan candida infections drugs market is witnessing consistent growth due to rising investments in healthcare innovation, advanced infectious disease management, and fungal infection treatment programs. Healthcare providers, pharmaceutical companies, and research institutes are increasingly adopting novel antifungal therapies for improved patient outcomes and disease management. Moreover, increasing utilization of advanced diagnostic technologies and the country’s focus on high-quality healthcare delivery are further contributing to market growth.

China Candida Infections Drugs Market Insight

The China candida infections drugs market is growing rapidly, driven by increasing healthcare investments, expanding hospital infrastructure, and rising government focus on infectious disease prevention and treatment. Growing adoption of advanced antifungal therapies and diagnostic technologies across hospitals, specialty clinics, and healthcare networks is significantly boosting market demand. In addition, rising awareness regarding fungal infections, increasing prevalence of immunocompromised patient populations, and rapid pharmaceutical advancements are positioning China as one of the fastest-growing markets for candida infections drugs globally.

Candida Infections Drugs Market Share

The candida infections drugs industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Novartis AG (Switzerland)

- Hoffmann-La Roche Ltd (Switzerland)

- Sanofi (France)

- GSK plc (U.K.)

- SCYNEXIS, Inc. (U.S.)

- Cidara Therapeutics, Inc. (U.S.)

- Basilea Pharmaceutica Ltd. (Switzerland)

- Mayne Pharma Group Limited (Australia)

- Alkem Laboratories Ltd. (India)

- Cipla Ltd (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Zydus Lifesciences Limited (India)

- Reddy's Laboratories Ltd. (India)

- Viatris Inc. (U.S.)

Latest Developments in Candida Infections Drugs Market

- In April 2024, Cidara Therapeutics announced the divestiture of REZZAYO® (rezafungin) to Mundipharma, enabling broader global commercialization of the antifungal therapy for candidemia and invasive candidiasis. The transaction was intended to support continued development and market expansion of one of the newest antifungal treatments targeting serious Candida infections. This development highlights ongoing industry efforts to strengthen access to advanced therapies for invasive fungal diseases

- In December 2023, Cidara Therapeutics announced the completion of patient enrollment in the China portion of its Phase III ReSTORE trial evaluating rezafungin for candidemia and invasive candidiasis. The milestone expanded the clinical development footprint of the drug in Asia and supported efforts to bring innovative antifungal therapies to patients suffering from serious Candida infections. The achievement strengthened the global evidence base for rezafungin

- In June 2023, SCYNEXIS announced the achievement of a major development milestone under its licensing agreement with GSK related to ibrexafungerp, a novel antifungal therapy under evaluation for invasive candidiasis. The progress reflected continued advancement of next-generation treatments designed to address antifungal resistance and improve outcomes in patients with severe Candida infections. The milestone also highlighted growing pharmaceutical investment in antifungal innovation

- In March 2023, Cidara Therapeutics and Melinta Therapeutics announced that the U.S. Food and Drug Administration (FDA) approved REZZAYO® (rezafungin for injection) for the treatment of candidemia and invasive candidiasis in adults with limited or no alternative treatment options. The approval marked the first new echinocandin antifungal approved in more than a decade and introduced a once-weekly dosing regimen for severe Candida infections. This launch reinforced innovation in the antifungal treatment landscape

- In March 2023, GSK and SCYNEXIS announced an exclusive licensing agreement for Brexafemme® (ibrexafungerp), an antifungal therapy approved for vulvovaginal candidiasis and recurrent vulvovaginal candidiasis. The agreement included support for ongoing clinical development of ibrexafungerp in invasive candidiasis, expanding efforts to address unmet needs in Candida infection treatment. The collaboration demonstrated increasing strategic focus on strengthening antifungal drug portfolios globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.