Global Canine Influenza Vaccine Market

Market Size in USD Billion

USD

1.50 Billion

USD

2.23 Billion

2024

2032

USD

1.50 Billion

USD

2.23 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.50 Billion | |

| USD 2.23 Billion | |

| % | |

|

Canine Influenza Vaccine Market Size

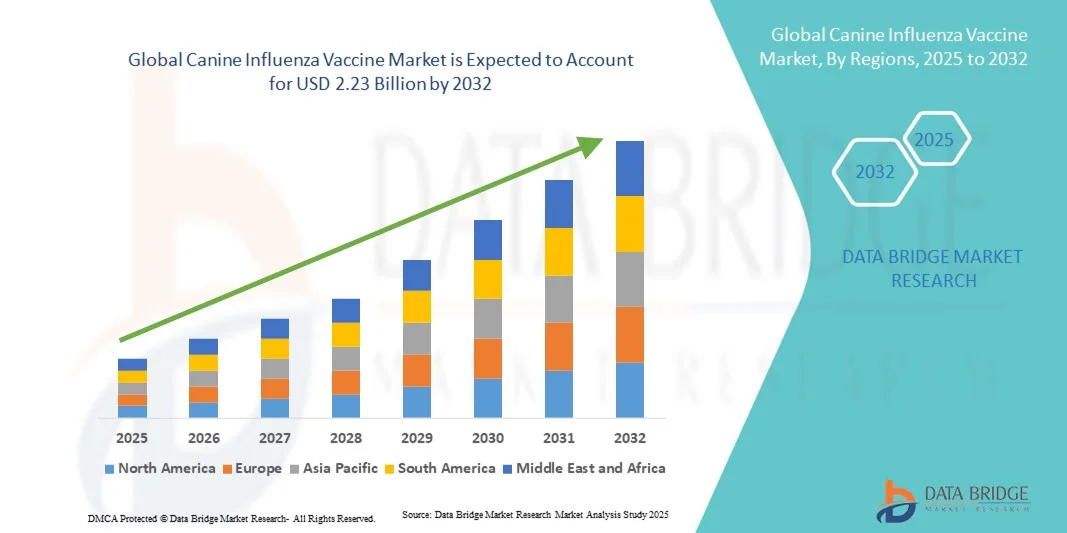

- The global canine influenza vaccine market size was valued at USD 1.50 billion in 2024 and is expected to reach USD 2.23 billion by 2032, at a CAGR of 5.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of canine influenza among domestic dogs, along with growing awareness among pet owners and veterinarians regarding preventive vaccination

- Furthermore, advancements in vaccine technology, including the development of more effective and safer immunization solutions, coupled with rising pet adoption rates globally, are accelerating the uptake of canine influenza vaccine solutions, thereby significantly boosting the industry's growth

Canine Influenza Vaccine Market Analysis

- Canine Influenza Vaccines are critical preventive measures for protecting dogs from highly contagious influenza strains, reducing the risk of severe respiratory infections, and minimizing outbreaks in kennels, shelters, and veterinary practices

- The increasing adoption of pet healthcare services, rising awareness among pet owners about canine influenza, and expanding veterinary infrastructure are driving the growing demand for Canine Influenza Vaccines globally

- North America dominated the canine influenza vaccine market with the largest revenue share of 43.5% in 2024, characterized by high pet ownership, advanced veterinary infrastructure, and a strong presence of leading vaccine manufacturers. The U.S. witnessed significant growth due to increased vaccination awareness, routine veterinary checkups, and innovations in vaccine formulations targeting multiple influenza strains. Leading veterinary hospitals and pet clinics have contributed to higher adoption rates, and regional campaigns promoting preventive pet healthcare support market dominance. Furthermore, strong distribution networks and accessible veterinary services in urban and suburban areas ensure widespread availability

- Asia-Pacific is expected to be the fastest growing region in the canine influenza vaccine market during the forecast period, driven by rising pet adoption, increasing disposable incomes, and growing awareness about preventive pet healthcare. Expansion of veterinary clinics, rising urbanization, and government initiatives supporting animal health further boost market growth

- The H3N8 Virus segment dominated the canine influenza vaccine market with the largest market revenue share of 47.1% in 2024, fueled by higher prevalence in equine populations, extensive vaccination programs, and strong clinical efficacy of available vaccines

Report Scope and Canine Influenza Vaccine Market Segmentation

|

Attributes |

Canine Influenza Vaccine Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Canine Influenza Vaccine Market Trends

Rising Adoption of Advanced Canine Influenza Vaccines

- A notable trend in the global canine influenza vaccine market is the increasing adoption of next-generation vaccines that provide broader immunity against multiple strains of canine influenza virus

- Pet owners and veterinary clinics are prioritizing vaccines that offer improved efficacy, longer-lasting protection, and reduced side effects, driving demand for advanced formulations

- For instance, in March 2023, Zoetis launched its updated canine influenza vaccine, CIV H3N2/H3N8, which provides protection against both major circulating strains, highlighting the focus on multi-strain coverage

- Growing awareness among pet owners about the health risks associated with canine influenza, particularly in urban areas and regions with high pet population density, is further fueling adoption

- Veterinary associations and pet health campaigns are actively promoting regular vaccination programs, contributing to the steady increase in vaccine uptake

- Pharmaceutical companies are investing in research to develop combination vaccines that protect against multiple canine respiratory diseases, reflecting a shift toward more comprehensive preventive healthcare for dogs

- The trend towards enhanced vaccine accessibility is also supported by the expansion of veterinary networks, online distribution channels, and community pet care initiatives, ensuring wider reach across urban and rural areas

- In addition, increasing international travel and participation in dog shows and kennels are driving the need for standardized preventive vaccination protocols, boosting the overall adoption of canine influenza vaccines globally

Canine Influenza Vaccine Market Dynamics

Driver

Growing Need Due to Rising Awareness of Canine Health and Disease Prevention

- The increasing prevalence of canine influenza outbreaks, coupled with rising awareness among pet owners about canine health and preventive care, is a significant driver for the heightened demand for canine influenza vaccines

- For instance, in April 2024, Zoetis, Inc. expanded its vaccine portfolio by launching updated canine influenza vaccines targeting both H3N2 and H3N8 strains. Such initiatives by key companies are expected to drive the Canine Influenza Vaccine industry growth in the forecast period

- As pet owners become more conscious of potential health threats to their dogs, canine influenza vaccines offer advanced protection against virus strains, reducing disease spread and minimizing treatment costs

- Furthermore, the growing number of veterinary clinics and hospitals, combined with the rising trend of regular vaccination schedules, is promoting the adoption of canine influenza vaccines. These vaccines are increasingly being incorporated into routine veterinary check-ups and wellness programs

- The convenience of availability through veterinary networks, pet specialty clinics, and animal hospitals, along with education on the benefits of vaccination, are key factors propelling the adoption of canine influenza vaccines in both urban and rural regions. The trend towards preventive care and increasing availability of multi-strain vaccine options further contribute to market growth

Restraint/Challenge

Concerns Regarding Vaccine Accessibility and Costs

- Concerns surrounding the accessibility of canine influenza vaccines, especially in remote regions or areas with limited veterinary infrastructure, pose a significant challenge to broader market penetration

- For instance, some pet owners may face difficulties obtaining vaccines due to limited supply chains or the unavailability of certain vaccine types in smaller veterinary clinics

- Addressing these accessibility challenges through expanded distribution networks, mobile veterinary clinics, and awareness programs is crucial for increasing vaccination coverage

- In addition, the relatively high cost of some advanced canine influenza vaccines compared to standard vaccines can be a barrier to adoption for price-sensitive pet owners, particularly in developing regions

- While multi-strain and combination vaccines offer broader protection, their perceived premium can still hinder widespread adoption, especially for owners who do not perceive an immediate risk of infection in their pets

- Overcoming these challenges through improved vaccine distribution, government-supported vaccination campaigns, and development of cost-effective vaccine options will be vital for sustained market growth

Canine Influenza Vaccine Market Scope

The market is segmented on the basis of vaccine type, product type, administration, virus type, end-users, and distribution channel.

- By Vaccine Type

On the basis of vaccine type, the canine influenza vaccine market is segmented into powder and dry vaccines. The powder segment dominated the largest market revenue share of 46% in 2024, driven by its wide adoption among veterinary clinics and pet owners. Powder vaccines offer ease of storage, cost-effectiveness, and compatibility with multiple administration methods. They maintain potency during transport and allow for flexible dosing, which is especially beneficial in large-scale vaccination programs. Clinics prefer powder vaccines for mass immunization campaigns in shelters, kennels, and breeding facilities due to their reliability and ease of use. The segment’s dominance is supported by strong manufacturer supply chains, regulatory approvals, and proven clinical efficacy. Educational initiatives on preventive pet healthcare encourage adoption. Their affordability compared to dry vaccines enhances adoption in urban and rural areas alike. Veterinary professionals also favor powder formulations for multi-dose sessions, while consistent quality and availability drive market share growth.

The dry vaccine segment is expected to witness the fastest CAGR of 24.5% from 2025 to 2032, driven by the growing demand for ready-to-use, portable vaccines. Dry vaccines offer longer shelf life, improved thermal stability, and minimal preparation before administration, making them ideal for homecare and mobile veterinary services. Pet clinics are increasingly adopting dry vaccines to quickly immunize multiple dogs with minimal logistical challenges. Rising awareness of preventive care among pet owners further supports growth. Technological advancements in formulation and packaging enhance stability and convenience. Expansion of veterinary networks in emerging markets and rising pet ownership contribute to accelerated adoption. Regulatory support for innovative delivery formats and easier administration encourages faster growth. Homecare programs and mobile veterinary units favor dry vaccines due to portability. The segment’s increasing adoption is also fueled by growing e-commerce distribution and direct-to-consumer availability.

- By Product Type

On the basis of product type, the canine influenza vaccine market is segmented into inactivated virus vaccines, live attenuated virus vaccines, and recombinant virus vaccines. The Inactivated Virus Vaccines segment dominated the largest market revenue share of 46.2% in 2024, driven by their proven safety profile, ease of storage and handling, and high efficacy in preventing influenza infections in animals. Veterinary hospitals and clinics widely use inactivated vaccines due to established protocols and strong regulatory approvals. Their long shelf life and minimal side effects enhance adoption across commercial farms and equine facilities. Continuous research and periodic updates to vaccine strains strengthen market confidence. Government vaccination programs and mandatory immunization in certain regions further support dominance. Availability in both single-dose and multi-dose formats improves flexibility for veterinarians.

The Recombinant Virus Vaccines segment is expected to witness the fastest CAGR of 11.4% from 2025 to 2032, driven by technological advancements, improved immune response, and growing demand for safer, next-generation vaccines. Recombinant vaccines allow for targeted protection and rapid development against emerging virus strains. Rising awareness among livestock owners and equine facility managers encourages adoption. Regulatory approvals in key regions expand availability. Integration with veterinary health monitoring programs ensures timely vaccination schedules. Cost reductions through scalable production methods stimulate faster uptake. Partnerships between biotech firms and veterinary service providers enhance distribution. The segment benefits from increasing focus on preventive animal health.

- By Administration Route

On the basis of administration route, the canine influenza vaccine market is segmented into intramuscular, subcutaneous, and intranasal vaccines. The Intramuscular segment dominated the largest market revenue share of 44.8% in 2024, due to its wide acceptance among veterinarians, high efficacy, and compatibility with most vaccine formulations. Intramuscular administration ensures uniform dosage delivery, optimal immune response, and minimal adverse reactions. Veterinary hospitals and large-scale farms prefer intramuscular injections for ease of mass vaccination programs. Its established use in both routine and outbreak scenarios reinforces dominance. Comprehensive training programs for veterinary staff enhance adoption. High patient compliance in animals reduces disease incidence.

The Intranasal segment is expected to witness the fastest CAGR of 10.9% from 2025 to 2032, driven by non-invasive delivery, improved mucosal immunity, and increasing adoption in equine and companion animals. Intranasal vaccines reduce stress for animals, ensuring better compliance. Rising demand for needle-free alternatives and faster onset of immunity supports growth. Integration with herd health management programs accelerates adoption. Veterinary research studies highlighting efficacy boost confidence. Expanding use in preventive vaccination strategies further drives market penetration.

- By Virus Type

On the basis of virus type, the canine influenza vaccine market is segmented into H3N8 Virus and H3N2 Virus. The H3N8 Virus segment dominated the largest market revenue share of 47.1% in 2024, fueled by higher prevalence in equine populations, extensive vaccination programs, and strong clinical efficacy of available vaccines. Veterinary practitioners rely on H3N8 vaccines for outbreak prevention, particularly in racing and breeding facilities. Regulatory approvals and inclusion in regional vaccination schedules reinforce adoption. Awareness campaigns among horse owners enhance coverage. Established cold chain logistics and distribution networks ensure consistent vaccine availability. Continuous monitoring of circulating strains supports timely updates.

The H3N2 Virus segment is expected to witness the fastest CAGR of 11.2% from 2025 to 2032, due to emerging infection trends, rising awareness of cross-species transmission risks, and growing demand for effective preventive solutions. Veterinary clinics and equine hospitals are increasingly focusing on dual-protection strategies. Expansion of large-scale breeding and equestrian facilities boosts adoption. Technological advancements in vaccine formulations improve immunity and reduce adverse effects. Government-led immunization initiatives and private vaccination campaigns accelerate uptake. Education programs for animal owners highlight the importance of early vaccination. Increasing integration of H3N2 vaccines with herd health protocols supports growth.

- By End-Users

On the basis of end-users, the canine influenza vaccine market is segmented into home, pet clinics, and others. The pet clinic segment dominated with a market revenue share of 52% in 2024, as most vaccinations are administered under professional supervision to ensure correct dosage and safety. Clinics provide trained staff, sterile environments, and proper cold-chain storage, ensuring vaccine efficacy. The dominance is supported by preventive healthcare programs, routine wellness check-ups, and awareness campaigns by veterinary associations. Urban pet populations and high clinic density contribute to the segment’s large share. Clinics often offer combination vaccination programs, encouraging adoption of multiple vaccines at a single visit. Brand trust and professional advice further strengthen this segment. The established distribution network and accessibility also play key roles. Veterinarians recommend clinic-based vaccinations for high-risk breeds and community pets. Quality control, post-vaccination monitoring, and standardized dosing add to the reliability of clinic administration. Pet owners prefer clinics for both preventive care and emergency situations, solidifying market dominance.

The home segment is expected to witness the fastest CAGR of 22% from 2025 to 2032, fueled by the rising trend of at-home pet care and convenience-focused solutions. Home administration allows vaccination in familiar surroundings, reducing stress for pets. Ready-to-use kits and guidance from veterinary professionals facilitate adoption. Growth is supported by e-commerce platforms offering direct delivery and online veterinary consultations. Awareness campaigns and education about preventive healthcare increase confidence in home vaccinations. Rural and suburban pet owners benefit from the convenience of home delivery. Rising smartphone penetration and tele-veterinary services enhance accessibility. Subscription-based vaccine programs for at-home use are also gaining popularity. Innovations in pre-measured doses ensure safe administration without professional supervision. The segment is increasingly preferred for pets with mobility or behavioral challenges, driving CAGR.

- By Distribution Channel

On the basis of distribution channel, the canine influenza vaccine market is segmented into retail pharmacy, online pharmacy, and others. The retail pharmacy segment dominated with a revenue share of 48% in 2024, due to well-established networks, accessibility, and direct purchase options. Pharmacies maintain cold-chain facilities and provide guidance on storage and administration. Brand recognition and trust play significant roles in consumer preference. Retail pharmacies are widely available in urban and semi-urban regions, offering convenience for routine vaccine purchases. Availability of multi-dose packs and combination vaccines further supports adoption. They often collaborate with veterinary clinics for proper administration advice. Retail chains provide promotional campaigns and loyalty programs, boosting sales. Widespread presence and familiarity make retail pharmacies the dominant distribution channel.

The online pharmacy segment is expected to witness the fastest CAGR of 25% from 2025 to 2032, driven by growing e-commerce adoption, doorstep delivery, and convenience for tech-savvy pet owners. Online platforms provide detailed product information, subscription services, and home delivery, increasing accessibility. Tele-veterinary consultations complement online sales for guidance on administration. Rising internet penetration in emerging markets and COVID-19-driven e-commerce growth further fuel this segment. Homecare adoption and mobile veterinary programs also support online distribution growth. User-friendly interfaces, secure payment options, and quick delivery enhance adoption. Digital marketing campaigns and targeted promotions increase awareness. Convenience of comparing prices and accessing multiple brands online encourages higher sales. Subscription models and bundle offers make online pharmacies increasingly popular. The segment’s growth is also driven by expanding logistics infrastructure and cold-chain capabilities.

Canine Influenza Vaccine Market Regional Analysis

- North America dominated the canine influenza vaccine market with the largest revenue share of 43.5% in 2024, characterized by high pet ownership, advanced veterinary infrastructure, and a strong presence of leading vaccine manufacturers

- The market witnessed significant growth due to increased vaccination awareness, routine veterinary checkups, and innovations in vaccine formulations targeting multiple influenza strains. Leading veterinary hospitals and pet clinics have contributed to higher adoption rates, and regional campaigns promoting preventive pet healthcare support market dominance

- Furthermore, strong distribution networks and accessible veterinary services in urban and suburban areas ensure widespread availability

U.S. Canine Influenza Vaccine Market Insight

The U.S. canine influenza vaccine market captured the largest revenue share in 2024 within North America, fueled by increasing vaccination rates, rising pet ownership, and adoption of advanced vaccine formulations. The growing focus on preventive pet healthcare, along with robust veterinary infrastructure and well-established distribution networks, further propels the Canine Influenza Vaccine industry. Moreover, regional initiatives promoting routine vaccinations and multi-strain vaccines are significantly contributing to market expansion.

Europe Canine Influenza Vaccine Market Insight

The Europe canine influenza vaccine market is projected to expand at a substantial CAGR throughout the forecast period, driven by growing awareness about preventive pet healthcare and stringent regulations on veterinary vaccinations. Increasing pet ownership and the adoption of advanced veterinary care are fostering the demand for canine influenza vaccines. European pet owners are also drawn to vaccines that provide broad protection against multiple strains. The region is experiencing notable growth across private veterinary clinics, pet hospitals, and animal care centers.

U.K. Canine Influenza Vaccine Market Insight

The U.K. canine influenza vaccine market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising pet adoption, awareness about infectious diseases, and preventive healthcare practices. Additionally, initiatives by veterinary associations encouraging routine vaccination are contributing to market growth. The country’s growing veterinary infrastructure, coupled with the increasing availability of multi-strain vaccines, is expected to continue to stimulate market expansion.

Germany Canine Influenza Vaccine Market Insight

The Germany canine influenza vaccine market is expected to expand at a considerable CAGR during the forecast period, fueled by increased pet healthcare awareness and demand for high-quality veterinary products. Germany’s well-developed veterinary services, combined with a strong focus on preventive care, promotes the adoption of canine influenza vaccines in both urban and rural regions. The integration of advanced multi-strain vaccines and strong distribution networks is further enhancing market growth.

Asia-Pacific Canine Influenza Vaccine Market Insight

The Asia-Pacific canine influenza vaccine market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by rising pet adoption, increasing disposable incomes, and growing awareness about preventive pet healthcare. Expansion of veterinary clinics, rising urbanization, and government initiatives supporting animal health further boost market growth. Emerging markets in China, India, and Southeast Asia are witnessing rapid development in pet healthcare services, contributing to the region’s high CAGR.

Japan Canine Influenza Vaccine Market Insight

The Japan canine influenza vaccine market is gaining momentum due to the country’s high rate of pet ownership, strong emphasis on preventive veterinary care, and increasing urbanization. The adoption of multi-strain vaccines and the expansion of veterinary clinics and animal hospitals are fueling market growth. Japan’s focus on innovative healthcare solutions and the availability of advanced vaccines ensures increasing uptake in both urban and suburban regions.

China Canine Influenza Vaccine Market Insight

The China canine influenza vaccine market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding middle class, rising pet ownership, rapid urbanization, and increasing awareness about preventive pet healthcare. China is one of the largest markets for canine vaccines, with multi-strain formulations gaining popularity in private veterinary clinics, animal hospitals, and pet care centers. Government initiatives supporting animal health, along with strong domestic manufacturers and distribution networks, are key factors driving market growth.

Canine Influenza Vaccine Market Share

The canine influenza vaccine industry is primarily led by well-established companies, including:

- Zoetis Inc. (U.S.)

- Elanco (U.S.)

- Merck & Co., Inc. (U.S.)

Latest Developments in Global Canine Influenza Vaccine Market

- In June 2024, Merck Animal Health announced the USDA approval of NOBIVAC NXT Canine Flu H3N2, the first and only canine influenza vaccine utilizing RNA-particle technology. This nonadjuvanted, low-volume 0.5 mL dose vaccine harnesses the natural ability of the immune system to generate a robust response without compromising comfort or safety. The product became available at veterinary clinics and hospitals nationwide later that summer

- In July 2025, Elanco Animal Health received USDA approval for TruCan Ultra CIV H3N2/H3N8, a bivalent canine influenza vaccine offering broad protection against both H3N2 and H3N8 strains. This vaccine demonstrated 100% virus neutralization against 33 current field isolates and showed zero lung lesions in vaccinated dogs post H3N2 challenge. It is the only ½ mL bivalent vaccine targeting both major CIV strains

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.