Global Capillary Blood Collection And Sampling Devices Market

Market Size in USD Billion

USD

2.77 Billion

USD

3.96 Billion

2024

2032

USD

2.77 Billion

USD

3.96 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.77 Billion | |

| USD 3.96 Billion | |

| % | |

|

Capillary Blood Collection and Sampling Devices Market Size

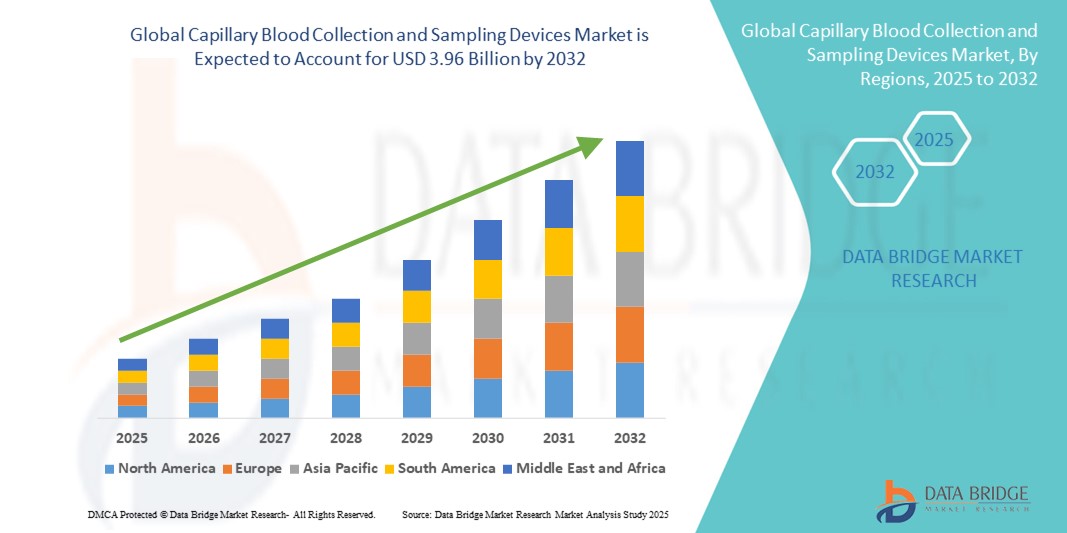

- The global capillary blood collection and sampling devices market size was valued at USD 2.77 billion in 2024 and is expected to reach USD 3.96 billion by 2032, at a CAGR of 4.55% during the forecast period

- The market growth is largely driven by increasing prevalence of chronic diseases, rising demand for point-of-care testing, and advancements in minimally invasive diagnostic technologies, enabling faster and more accurate blood sampling in clinical and home settings

- Furthermore, growing awareness among healthcare providers and patients about the benefits of capillary blood collection, such as reduced pain, ease of use, and convenience, is establishing these devices as a preferred method for routine blood testing. These converging factors are accelerating the adoption of capillary blood collection and sampling solutions, thereby significantly enhancing the industry's growth.

Capillary Blood Collection and Sampling Devices Market Analysis

- Capillary blood collection and sampling devices, designed for minimally invasive collection of blood from capillaries, are increasingly essential in modern diagnostic, point-of-care, and home testing applications due to their ease of use, reduced pain, and rapid sample processing capabilities

- The growing adoption of these devices is primarily fueled by the rising prevalence of chronic diseases, increased demand for point-of-care diagnostics, and the need for convenient, patient-friendly sampling methods in both clinical and home healthcare settings

- North America dominated the capillary blood collection and sampling devices market with the largest revenue share of 39% in 2024, driven by advanced healthcare infrastructure, high healthcare expenditure, and the presence of key market players, with the U.S. witnessing significant adoption in hospitals, diagnostic labs, and home health monitoring programs, supported by innovations in micro-collection devices and automated sampling systems

- Asia-Pacific is expected to be the fastest-growing region in the capillary blood collection and sampling devices market during the forecast period due to increasing healthcare awareness, rising prevalence of chronic and infectious diseases, and expanding access to diagnostic facilities in urban and semi-urban areas

- Capillary Blood Collection Devices segment dominated the capillary blood collection and sampling devices market with a share of 42.5% in 2024, driven by their convenience, compatibility with point-of-care and laboratory testing, and minimal invasiveness compared to conventional blood collection methods

Report Scope and Capillary Blood Collection and Sampling Devices Market Segmentation

|

Attributes |

Capillary Blood Collection and Sampling Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Capillary Blood Collection and Sampling Devices Market Trends

Rising Adoption of Point-of-Care and Remote Sampling Solutions

- A major trend in the global capillary blood collection and sampling devices market is the increasing adoption of point-of-care (POC) testing and remote blood sampling technologies, enabling faster diagnostics and patient monitoring outside traditional laboratory settings

- For instance, remote capillary blood collection devices allow patients to collect small blood samples at home and send them to labs for analysis, reducing the need for frequent hospital visits. Similarly, wearable capillary blood collection devices are being developed to continuously monitor biomarkers for chronic conditions such as diabetes and cardiovascular diseases

- Technological advancements are enhancing device accuracy, ease of use, and integration with digital health platforms. Devices such as micro-collection kits and automated sampling units can now provide real-time sample validation and track patient data through mobile applications

- The integration of capillary sampling devices with telehealth and mobile diagnostic platforms facilitates centralized patient monitoring, allowing healthcare providers to track test results, trends, and anomalies remotely

- Companies such as Tasso, Inc. and Seventh Sense Biosystems are focusing on developing smart, user-friendly blood collection devices with features such as minimal invasiveness, automated sampling, and secure data transmission

- This trend towards more convenient, connected, and patient-centric blood collection solutions is reshaping diagnostic practices, driving adoption across hospitals, laboratories, and home healthcare sectors

Capillary Blood Collection and Sampling Devices Market Dynamics

Driver

Increasing Demand Due to Chronic Disease Prevalence and Home-Based Diagnostics

- The rising prevalence of chronic diseases, coupled with the growing emphasis on home-based and minimally invasive diagnostics, is a key driver for the market

- For instance, in March 2024, Seventh Sense Biosystems expanded its remote blood collection offerings for chronic disease monitoring, highlighting the convenience and accuracy of their micro-sampling technology

- Patients and healthcare providers are increasingly favoring capillary blood sampling due to its reduced pain, smaller sample volume requirements, and suitability for frequent monitoring of conditions such as diabetes, cardiovascular disease, and infectious diseases

- The convenience of home collection, rapid sample processing, and compatibility with point-of-care and laboratory testing workflows further propels adoption across both clinical and home healthcare environments

- Growing prevalence of chronic diseases and the need for minimally invasive, home-based diagnostics is driving the market

- Capillary blood sampling offers reduced pain, smaller sample volume requirements, and suitability for frequent monitoring, making it attractive for both patients and healthcare providers

Restraint/Challenge

Sample Accuracy, Standardization, and Regulatory Compliance

- Concerns regarding sample accuracy, proper collection techniques, and regulatory compliance pose significant challenges to broader market adoption. Improper capillary blood collection can lead to hemolysis, contamination, or insufficient sample volume, affecting test reliability

- For instance, high variability in results from at-home blood collection kits has raised questions about standardization and quality assurance, prompting regulatory authorities to set stricter guidelines for device approval

- Addressing these challenges requires improved device design, clear user instructions, and integration with automated or volumetric sampling technologies to reduce human error. Companies such as Becton Dickinson and Sarstedt emphasize quality control, user training, and adherence to regulatory standards to ensure reliable testing outcomes

- In addition, the relatively higher cost of advanced automated or wearable sampling devices compared to traditional finger-prick kits can limit adoption in price-sensitive regions

- Variability in sample quality and collection technique can affect test reliability, raising concerns among users and healthcare professionals

- Regulatory compliance and the relatively higher cost of advanced automated or wearable devices can limit adoption in price-sensitive regions

- Overcoming these barriers through enhanced device accuracy, regulatory compliance, and user education will be crucial for sustained growth in the global capillary blood collection and sampling devices market

Capillary Blood Collection and Sampling Devices Market Scope

The market is segmented on the basis of product, modality, mode of administration, application, platform, procedure, age group, test type, technology, material, end user, and distribution channel.

- By Product

On the basis of product, the capillary blood collection and sampling devices market is segmented into blood sampling devices, capillary blood collection devices, rapid test cassette, remote capillary blood collection device, and wearable capillary blood collection device. The Capillary Blood Collection Devices segment dominated the market with a 42.5% share in 2024, due to its widespread use in hospitals, diagnostic laboratories, and point-of-care testing. These devices offer minimally invasive sample collection, reduce patient discomfort, and ensure accurate small-volume blood sampling. Their compatibility with multiple test types such as whole blood, plasma, and dried blood spot tests makes them ideal for clinical applications. The growing prevalence of chronic diseases and the need for regular monitoring further support the dominance of this segment.

The remote capillary blood collection device segment is expected to witness the fastest growth from 2025 to 2032, fueled by the increasing adoption of home-based diagnostics and telemedicine solutions. Remote devices allow patients to collect samples at home and send them to laboratories, reducing hospital visits and improving patient compliance. Technological advancements such as automated tracking, user-friendly interfaces, and compatibility with telehealth platforms enhance adoption. Rising awareness of patient-centric care models and the convenience of home-based testing accelerate growth.

- By Modality

On the basis of modality, the capillary blood collection and sampling devices market is segmented into manual sampling and automated/autoinjection sampling. The Manual Sampling segment dominated with a 60.7% share in 2024, due to simplicity, low cost, and widespread use in home and clinical settings. Manual devices allow healthcare providers to control sample collection, ensuring accuracy and reliability in routine testing. They are particularly preferred in low-resource settings where automated systems may not be feasible. Manual sampling is compatible with multiple age groups and test types, enhancing its utility. This segment benefits from the large installed base of conventional collection devices. It is widely used in laboratories, clinics, and home care environments for daily monitoring.

The Automated/Autoinjection Sampling segment is expected to witness the fastest growth, driven by the increasing demand for high-throughput, precise, and low-error sample collection. Hospitals and diagnostic labs are adopting automation to improve efficiency and workflow integration. Automated systems reduce human errors, standardize sample volume, and enhance reproducibility. Integration with digital health platforms and laboratory information systems further supports adoption. The growth is accelerated by rising awareness of quality control and standardization requirements.

- By Mode of Administration

On the basis of mode of administration, the capillary blood collection and sampling devices market is segmented into Puncture and Incision. The Puncture segment dominated with a 68.4% share in 2024, as it is minimally invasive, causes less discomfort, and is suitable for adults, pediatric, and geriatric patients. Puncture-based devices, including finger-prick and heel-prick systems, are widely used in routine diagnostics and point-of-care applications. Their simplicity and low risk of complications make them highly preferred in both hospitals and home care. Puncture methods are compatible with multiple test types and platforms, including ELISA and PCR. They support rapid collection and immediate analysis, improving patient compliance. Rising demand for minimally invasive solutions for chronic disease monitoring also strengthens dominance.

The Incision segment is expected to witness the fastest growth during forecast period, due to its application in specialized diagnostics requiring larger blood volumes. Innovations in safety and efficiency have increased adoption in hospitals and research labs. Incision devices allow accurate sample collection for molecular analysis and high-sensitivity testing. Growth is supported by the rising prevalence of rare diseases and research-driven sample collection needs. Increasing laboratory automation and adoption of standardized procedures further fuel growth.

- By Application

On the basis of application, the capillary blood collection and sampling devices market is segmented into cardiovascular disease, infection and infectious disease, respiratory diseases, cancers, rheumatoid arthritis, and others. The Cardiovascular Disease segment dominated with a 29.6% share in 2024, due to high disease prevalence and frequent biomarker monitoring requirements. Capillary blood collection devices allow minimally invasive testing for cholesterol, glucose, and cardiac enzymes. Routine monitoring in hospitals and home care settings drives adoption. Patients prefer capillary sampling for ease, convenience, and reduced discomfort. The segment also benefits from integration with chronic disease management programs. Rising awareness of cardiovascular health and early diagnosis contributes to growth.

The Infection and Infectious Disease segment is expected to witness the fastest growth during forecast period, driven by outbreaks, increasing demand for rapid diagnostics, and point-of-care testing. Devices enabling quick and reliable sample collection for infectious disease testing at home or clinics are gaining traction. Emerging economies with limited laboratory infrastructure are particularly driving demand. Growth is supported by rising telehealth initiatives, epidemiological studies, and government screening programs. The convenience of remote sample collection enhances patient compliance.

- By Platform

On the basis of platform, the capillary blood collection and sampling devices market is segmented into ELISA, PCR, Lateral Flow Immunoassay, ELTABA, and Others. The ELISA Platform dominated with a 33.2% share in 2024, due to high accuracy, reproducibility, and wide applicability for biomarker detection from capillary blood samples. It is used in hospitals, laboratories, and research facilities for routine and high-throughput testing. Compatibility with multiple collection devices and test types ensures widespread adoption. ELISA platforms support chronic disease monitoring, infectious disease testing, and clinical research. Training and standardization make it the preferred platform for laboratories globally. Technological integration with VAMS and DBS methods further strengthens its position.

The PCR Platform segment is expected to witness the fastest growth during forecast period, due to increasing demand for molecular diagnostics and infectious disease detection. Capillary blood samples are suitable for PCR due to small sample volume requirements. Home-based, point-of-care, and telehealth solutions enhance PCR adoption. Rising awareness of early diagnosis for viral infections supports growth. PCR’s high sensitivity and specificity make it a preferred platform for laboratories and research institutions. Increasing government and private funding in molecular diagnostics accelerates growth.

- By Procedure

On the basis of procedure, the capillary blood collection and sampling devices market is segmented into Conventional and Point of Care Testing. The Point of Care Testing (POCT) segment dominated with a 57.1% share in 2024, due to rising adoption of rapid diagnostics, home-based testing, and near-patient testing solutions. POCT enables faster results, reduces reliance on centralized laboratories, and improves patient management. The segment is increasingly used for chronic disease monitoring and infectious disease detection. Compatibility with capillary blood collection devices supports ease of use and patient compliance. Integration with digital health platforms enhances monitoring and reporting. The convenience, accuracy, and speed make POCT highly preferred across healthcare settings.

The Conventional Testing segment is expected to witness the fastest growth during forecast period, particularly in emerging markets where centralized laboratory infrastructure is expanding. Conventional testing requires standardized workflows, and capillary blood collection devices support sample integrity for these analyses. Adoption is driven by expanding hospital and laboratory networks. Conventional testing continues to dominate routine diagnostics in several regions. Growth is also supported by increasing demand for chronic disease and cardiovascular testing. Integration with laboratory automation further boosts adoption.

- By Age Group

On the basis of age group, the capillary blood collection and sampling devices market is segmented into geriatrics, infant, pediatric, and adult. The Adult segment dominated with a 46.8% share in 2024, driven by high prevalence of chronic diseases, routine monitoring, and frequent diagnostic testing. Adults require blood sampling for cardiovascular, metabolic, and infectious disease management. Hospitals, labs, and home care settings widely adopt devices designed for adults. Minimally invasive, accurate, and easy-to-use devices enhance compliance. Integration with telehealth and remote monitoring platforms further supports adoption. Growing chronic disease prevalence globally reinforces the segment’s dominance.

The Infant segment is expected to witness the fastest growth, fueled by neonatal screening programs and rising awareness for early detection of metabolic and genetic disorders. Heel-prick and finger-prick devices are minimally invasive and safe for newborns. Adoption is supported by hospitals and pediatric clinics for routine infant testing. Remote and home-based collection kits improve compliance and accessibility. Technological innovations make devices easier for caregivers to use. Government initiatives in infant screening further drive growth.

- By Test Type

On the basis of test type, the capillary blood collection and sampling devices market is segmented into Whole Blood Test, Dried Blood Spot Tests, Plasma/Serum Protein Tests, Liver Panel, CMP Tests, and Others. The Whole Blood Test segment dominated with a 38.5% share in 2024, due to its widespread use in routine diagnostics and clinical applications. Whole blood collection allows testing for multiple analytes, including glucose, cholesterol, and infectious disease markers. Hospitals, labs, and home care services prefer whole blood tests for their reliability and accuracy. Capillary blood collection devices are compatible with whole blood analysis, supporting rapid results. Patients benefit from reduced sample volume requirements and minimal discomfort. Rising prevalence of chronic and infectious diseases further strengthens adoption.

The Dried Blood Spot (DBS) Tests segment is expected to witness the fastest growth during forecast period, driven by suitability for remote collection, storage stability, and telehealth-based diagnostics. DBS allows home collection, minimizes handling errors, and supports infectious disease monitoring. Technological improvements in DBS sample analysis enhance accuracy and reproducibility. Adoption is increasing in population studies, epidemiology, and chronic disease management. Patients prefer DBS for convenience and reduced invasiveness. Growth is supported by increasing availability of DBS collection kits through online and retail channels.

- By Technology

On the basis of technology, the capillary blood collection and sampling devices market is segmented into Volumetric Absorptive Microsampling (VAMS), Capillary Electrophoresis-Based Chemical Analysis, and Others. The VAMS segment dominated with a 31.4% share in 2024, due to precision in small-volume blood collection, compatibility with multiple platforms, and minimal handling errors. It is widely used in hospitals, labs, and research facilities. VAMS supports both point-of-care and home-based diagnostics. Accuracy, reproducibility, and ease of use drive adoption. Integration with telehealth and remote monitoring enhances its utility. R&D investment in VAMS further strengthens its position.

The Capillary Electrophoresis-Based Chemical Analysis segment is expected to witness the fastest growth during forecast period, driven by adoption in laboratories and research facilities for detailed molecular and biochemical analysis. Small-volume capillary samples allow high-precision testing. This technology is used in drug development, biomarker research, and specialized diagnostics. Automation integration reduces human errors and increases efficiency. Rising adoption of personalized medicine and advanced diagnostics supports growth. Funding in advanced research accelerates market expansion.

- By Material

On the basis of material, the capillary blood collection and sampling devices market is segmented into Plastic, Glass, Stainless Steel, and Ceramic. The Plastic segment dominated with a 52.6% share in 2024, due to cost-effectiveness, disposability, lightweight design, and safety. Plastic devices reduce contamination risk and are widely adopted for home and clinical use. Compatibility with multiple test types, including whole blood and DBS, supports adoption. Plastic devices are easier to transport and store. They are ideal for single-use, point-of-care applications. Growing demand for affordable devices globally strengthens this segment.

The Stainless Steel segment is expected to witness the fastest growth during forecast period, driven by durability, precision, and suitability for high-throughput labs and automated sampling systems. Stainless steel supports repeated use in professional settings. It integrates with autoinjection and automated systems for accuracy. Hospitals and research labs prefer stainless steel for its reliability and long-term use. Increasing investments in advanced laboratory infrastructure enhance adoption. Rising awareness of quality and safety standards supports growth.

- By End User

On the basis of end user, the capillary blood collection and sampling devices market is segmented into Laboratories and Home Care Settings. The Laboratories segment dominated with a 61.2% share in 2024, as most capillary blood samples are processed in hospitals, diagnostic, and research labs. Laboratories demand high-accuracy, standardized devices compatible with automation and high-throughput workflows. Integration with analytical platforms such as ELISA, PCR, and VAMS ensures efficiency. Institutional procurement contracts and direct tenders further reinforce dominance. Capillary devices are essential for chronic disease, infectious disease, and research testing. Laboratories prefer reliable, reproducible, and compliant solutions.

The Home Care Setting segment is expected to witness the fastest growth during forecast period, due to rising telemedicine adoption, chronic disease self-monitoring, and patient-centric care. Home devices allow convenient and minimally invasive blood collection. Patients and caregivers prefer easy-to-use, reliable devices for remote sample collection. Growth is supported by wearable and remote collection technologies. Increasing awareness of home diagnostics and online kit availability fuels adoption. Chronic disease prevalence and government initiatives further accelerate growth.

- By Distribution Channel

On the basis of distribution channel, the capillary blood collection and sampling devices market is segmented into Direct Tender, Retail Sales, and Others. The Direct Tender segment dominated with a 49.8% share in 2024, due to large-scale procurement by hospitals, laboratories, and clinics. Institutional tenders ensure quality, compliance, and favorable bulk pricing. Hospitals prefer this channel for consistent supply and secure sourcing. Direct tender contracts support integration with automated systems and high-throughput workflows. Long-term agreements with suppliers reinforce dominance. Developed regions with established healthcare infrastructure drive market strength.

The Retail Sales segment is expected to witness the fastest growth during forecast period, fueled by online availability, growing consumer awareness, and demand for home-based diagnostic kits. Retail channels allow patients to access devices directly for self-collection, supporting telehealth and home diagnostics. E-commerce expansion and smartphone-based health platforms enhance adoption. Home-based testing kits, wearables, and remote devices benefit from retail distribution. Patient preference for convenience, minimal invasiveness, and fast results accelerates growth. Rising adoption in emerging markets further supports retail sales expansion.

Capillary Blood Collection and Sampling Devices Market Regional Analysis

- North America dominated the capillary blood collection and sampling devices market with the largest revenue share of 39% in 2024, driven by advanced healthcare infrastructure, high healthcare expenditure, and the presence of key market players

- Consumers and healthcare providers in the region increasingly prefer minimally invasive, reliable, and rapid blood collection solutions for hospitals, laboratories, and home care settings. High awareness of telemedicine and point-of-care testing further supports market adoption

- The dominance is reinforced by strong government initiatives promoting early disease detection, routine health monitoring, and remote patient management programs. In addition, increasing investments by key players in R&D and innovation for advanced collection devices contribute to the market’s growth in North America

U.S. Capillary Blood Collection and Sampling Devices Market Insight

The U.S. capillary blood collection and sampling devices market captured the largest revenue share of 42% in 2024, driven by advanced healthcare infrastructure, widespread adoption of telemedicine, and high awareness of minimally invasive diagnostic solutions. Hospitals, laboratories, and home care providers are increasingly prioritizing patient-friendly collection devices for routine monitoring of chronic and infectious diseases. The growing demand for point-of-care testing, coupled with integration of remote sampling technologies, further propels market growth. Moreover, strong government initiatives for early disease detection and preventive healthcare programs contribute significantly to the expansion of the market. Increasing availability of automated and wearable devices enhances convenience and adoption among patients and healthcare providers.

Europe Capillary Blood Collection and Sampling Devices Market Insight

The Europe capillary blood collection and sampling devices market is projected to expand at a significant CAGR during the forecast period, primarily driven by increasing adoption of advanced diagnostic tools and stringent healthcare regulations. Rising awareness regarding chronic disease monitoring and minimally invasive sampling methods is fostering market growth. European healthcare providers and laboratories increasingly prefer capillary blood collection devices for reliability, accuracy, and patient comfort. The market benefits from established distribution networks, government-backed screening programs, and reimbursement policies supporting routine diagnostics. Countries such as Germany, the U.K., and France are witnessing rising adoption across both hospital and home care settings. Continuous technological innovation, including automated and remote collection devices, is further fueling market expansion.

U.K. Capillary Blood Collection and Sampling Devices Market Insight

The U.K. capillary blood collection and sampling devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing prevalence of chronic and infectious diseases, coupled with rising awareness of home-based diagnostics. Healthcare providers and patients are showing a growing preference for minimally invasive, reliable, and easy-to-use capillary blood collection devices. The strong e-commerce and retail infrastructure in the country facilitates widespread availability of home-use kits. Government health initiatives promoting early disease detection and preventive care further stimulate adoption. Integration with telehealth platforms and point-of-care testing technologies is accelerating market growth. The focus on convenience, patient comfort, and timely diagnostics underpins continued demand in both residential and clinical segments.

Germany Capillary Blood Collection and Sampling Devices Market Insight

The Germany capillary blood collection and sampling devices market is expected to expand at a considerable CAGR, fueled by rising awareness of preventive healthcare, early diagnostics, and advanced laboratory infrastructure. Capillary blood collection devices are increasingly preferred for routine monitoring of cardiovascular, metabolic, and infectious diseases. Germany’s emphasis on innovation, quality standards, and sustainability encourages adoption of high-precision and reusable devices. Hospitals, diagnostic centers, and research laboratories are implementing these devices to enhance workflow efficiency and reduce patient discomfort. Increasing integration with automated and digital platforms for sample collection and reporting is supporting market growth. Consumer demand for safe, reliable, and eco-conscious devices further strengthens adoption.

Asia-Pacific Capillary Blood Collection and Sampling Devices Market Insight

The Asia-Pacific capillary blood collection and sampling devices market is poised to grow at the fastest CAGR of 25% from 2025 to 2032, driven by rapid urbanization, rising disposable incomes, and increasing healthcare accessibility in countries such as China, Japan, and India. The adoption of telemedicine and home-based diagnostics is rising, encouraging the use of capillary blood collection devices. Government initiatives supporting maternal and infant health, infectious disease monitoring, and chronic disease management are accelerating demand. Technological advancements in remote and wearable devices improve convenience and accuracy. APAC is also emerging as a manufacturing hub for these devices, making them more affordable and accessible to a broader population. Growing awareness of patient-centric care and preventive healthcare is a key driver for the region.

Japan Capillary Blood Collection and Sampling Devices Market Insight

The Japan capillary blood collection and sampling devices market is gaining momentum due to the country’s high-tech healthcare infrastructure, aging population, and emphasis on convenience and patient safety. Adoption is driven by the increasing number of smart hospitals, connected clinics, and home-based diagnostic solutions. Capillary blood collection devices integrated with automated and wearable technologies are widely used for chronic disease monitoring and infectious disease testing. Government programs promoting preventive healthcare, along with a strong focus on research and development, further support market growth. The elderly population benefits from minimally invasive and easy-to-use devices. Rising awareness of telehealth solutions is also enhancing adoption in both residential and clinical sectors.

India Capillary Blood Collection and Sampling Devices Market Insight

The India capillary blood collection and sampling devices market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, expanding middle-class population, and rising awareness of telemedicine and home-based testing solutions. Capillary blood collection devices are increasingly used in hospitals, diagnostic labs, and home care settings for routine monitoring of chronic diseases and infectious conditions. Government initiatives supporting smart healthcare and digital health programs boost market adoption. Affordable device options and strong domestic manufacturing capabilities further drive growth. Increasing demand in residential, commercial, and remote care applications contributes to rapid expansion. Telehealth integration and point-of-care testing solutions are enhancing convenience and accessibility for Indian consumers.

Capillary Blood Collection and Sampling Devices Market Share

The Capillary Blood Collection and Sampling Devices industry is primarily led by well-established companies, including:

- BD (U.S.)

- Tasso, Inc. (U.S.)

- YourBio Health, Inc. (U.S.)

- Neoteryx LLC (U.S.)

- Greiner Bio-One International GmbH (Austria)

- Owen Mumford Limited (U.K.)

- VMG (Denmark)

- HemaXis (Switzerland)

- Drawbridge Health, Inc. (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- SARSTEDT AG & Co. KG (Germany)

- MEDIpoint International, Inc. (U.S.)

- Capillary Technologies India Limited. (Singapore)

- Radiometer Medical ApS (Denmark)

- Bio-Rad Laboratories, Inc. (U.S.)

- Kent Scientific Corporation (U.S.)

What are the Recent Developments in Global Capillary Blood Collection and Sampling Devices Market?

- In March 2025, BD reported that its new fingertip blood collection device demonstrated equivalent testing accuracy to traditional venous blood draws for certain analytes. This device aims to improve patient access to diagnostic testing by offering a less invasive and more convenient alternative, potentially reducing the need for multiple needle sticks

- In February 2025, Tasso, Inc., the leading provider of patient-centric, clinical grade blood collection solutions, announced the launch of its next generation technology for dried blood spot (DBS) sample collection. The novel collection system combines Tasso’s new Tile-T20 dried whole blood cartridge with a Tasso Mini device, enabling the precise, convenient collection of DBS samples for clinical trials and sports anti-doping testing

- In December 2023, Becton Dickinson (BD) announced that its BD MiniDraw Capillary Blood Collection System received FDA 510(k) clearance. This device enables healthcare providers to obtain lab-quality blood samples using a patient's finger, offering a less invasive alternative to traditional venous blood collection methods. It aims to expand access to blood collection in various settings, including retail pharmacies

- In October 2023, YourBio Health announced that its TAP Micro Select blood collection device received expanded regulatory approval with CE Marking certification. This device facilitates remote, virtually painless capillary blood collection, supporting applications such as Myriad Genetics' SneakPeek Tests. The approval enables broader use in Europe, enhancing access to non-invasive testing

- In September 2024, Tasso, Inc. announced that its Tasso+ device received FDA 510(k) Class II medical device clearance. This single-use, patient-centric blood collection product is designed to provide a minimally invasive alternative to traditional blood collection methods, enabling easier access to blood testing in various healthcare settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.