Global Carbon Capture Materials Market

Market Size in USD Billion

USD

63.12 Billion

USD

326.40 Billion

2025

2033

USD

63.12 Billion

USD

326.40 Billion

2025

2033

| 2026 - 2033 | |

| USD 63.12 Billion | |

| USD 326.40 Billion | |

| % | |

|

Carbon Capture Materials Market Overview

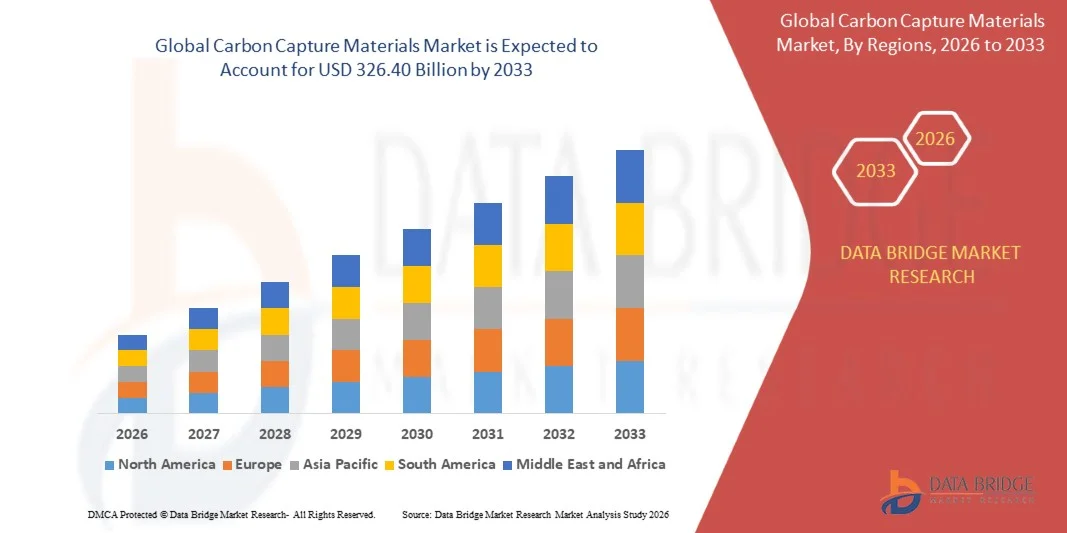

As per Data Bridge Market Research analysis The carbon capture materials market was valued at USD 63.12 billion in 2025 and is projected to reach USD 326.40 billion by 2033, growing at a CAGR of 22.80 % from 2026 to 2033. The market is experiencing consistent growth driven by rising global decarbonization targets, increasing investments in carbon capture, utilization and storage (CCUS) infrastructure, and rapid advancements in high-efficiency capture materials such as solid sorbents, advanced solvents, and metal-organic frameworks (MOFs).

The increasing urgency to reduce industrial carbon emissions, combined with stricter environmental regulations and net-zero commitments from governments and corporations, is compelling power generation, oil & gas, cement, and chemical industries to adopt carbon capture technologies. Advanced liquid amine systems, next-generation solid sorbents, and membrane-based capture solutions are increasingly replacing conventional methods due to higher efficiency, lower energy penalties, and improved scalability for both large-scale industrial facilities and emerging direct air capture applications.

Market Size & Forecast

- Global Market Value (2025): USD 63.12 Billion

- Expected Market Value (2033): USD 326.40 Billion

- Forecast CAGR (2026–2033): 22.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the global carbon capture materials market with the largest revenue share of 35.38% in 2025, supported by strong policy incentives, tax credits such as 45Q, and large-scale deployment of CCUS projects across power generation, oil & gas, and industrial sectors.

- The Solid Sorbents segment led the market with a 34.38% share in 2025, driven by their high CO₂ capture efficiency, lower energy requirements for regeneration, and strong compatibility with both industrial flue gas and direct air capture systems.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.9% from 2026 to 2033, fueled by rapid industrialization, rising emissions reduction targets, and increasing government investments in clean energy and carbon mitigation technologies.

- Advanced Materials are the fastest-growing material type, projected to register a CAGR of 12.5%, reflecting the surge in rapid innovation in Metal–Organic Frameworks (MOFs), hybrid sorbents, and nanostructured capture media.

- The Amine-based Materials segment dominated the material chemistry category with a 30.35% revenue share in 2025, led by their proven commercial viability and widespread use in post-combustion capture systems across power plants and industrial facilities.

- Absorption accounted for 45.50% of the market, preferred by the extensive use of liquid amine-based systems in industrial post-combustion capture applications.

- The Direct Air Capture segment is the fastest-growing capture technology category, with a CAGR of 12.6%, driven by the increasing global focus on negative emissions technologies.

Report Scope and Carbon Capture Materials Market Segmentation

|

Attributes |

Carbon Capture Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Climeworks (Switzerland) · Carbon Engineering Ltd. (Canada) · Occidental Petroleum Corporation (U.S.) · Shell plc (U.K.) · ExxonMobil Corporation (U.S.) · TotalEnergies SE (France) · Equinor ASA (Norway) · Linde plc (Ireland) · Air Liquide S.A. (France) · Mitsubishi Heavy Industries, Ltd. (Japan) · Hitachi Zosen Corporation (Japan) · BASF SE (Germany) · SABIC (Saudi Arabia) · Chevron Corporation (U.S.) · Honeywell International Inc. (U.S.) · Svante Inc. (Canada) · Aker Carbon Capture ASA (Norway) · 3M (U.S.) · Johnson Matthey plc (U.K.) · Heidelberg Materials AG (Germany) |

|

Market Opportunities |

· Rising deployment of Direct Air Capture (DAC) facilities · Expanding industrial decarbonization mandates in cement, steel, and chemicals sectors · Increasing integration of carbon capture with utilization pathways (CCU) |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Carbon Capture Materials Market Trends

Trend: Growth in Direct Air Capture and Industrial Decarbonization Adoption

Industrial sectors are rapidly shifting toward high-efficiency carbon capture materials such as solid sorbents, advanced amine-based solvents, membranes, and next-generation Metal-Organic Frameworks (MOFs) to support large-scale decarbonization efforts. This transition is strongly driven by the need to achieve net-zero targets while maintaining operational continuity in energy-intensive industries such as power generation, cement, steel, and chemicals. Direct Air Capture (DAC) is emerging as a major growth catalyst, requiring highly selective and low-energy materials capable of capturing CO₂ directly from ambient air under varying environmental conditions.

For instance, large-scale DAC demonstration projects in North America and Europe are deploying modular solid sorbent systems integrated with automated regeneration cycles to improve capture efficiency and scalability for industrial deployment.

Carbon Capture Materials Market Dynamics

Key Market Driver: Rising Regulatory Pressure and Net-Zero Commitments

The increasing enforcement of stringent climate policies, carbon taxation frameworks, and mandatory emission reduction targets is significantly accelerating the adoption of carbon capture materials across global industries. Governments and regulatory bodies are incentivizing CCUS deployment through subsidies, tax credits, and compliance-based emission trading systems, making carbon capture integration economically viable for heavy emitters. At the same time, corporate sustainability commitments are pushing industrial operators to adopt scalable capture technologies as part of long-term decarbonization strategies. For instance, policy mechanisms such as carbon credit trading schemes and industrial emission caps are driving large-scale investments in amine solvent-based post-combustion capture systems and solid sorbent technologies across existing refinery and power plant infrastructure.

Key Restraint/Challenge: High Energy Consumption and Material Degradation Issues

Despite technological advancements, the carbon capture materials market faces significant challenges related to high energy consumption during regeneration cycles and gradual degradation of capture efficiency over repeated operational use. These issues increase operational costs and reduce system longevity, making widespread adoption difficult in cost-sensitive or developing markets. Material fouling, thermal instability, and chemical degradation especially in solvent-based systems further impact long-term performance reliability. For instance, industrial carbon capture plants operating with amine-based solvents often require frequent solvent reclamation and replacement due to degradation caused by flue gas impurities, which increases both maintenance downtime and overall lifecycle costs of CCUS installations.

Key Market Opportunity: Expansion of Carbon Utilization and Advanced Material Innovation

The growing integration of carbon capture with utilization pathways presents a major opportunity for advanced material developers, enabling captured CO₂ to be converted into commercially valuable products such as synthetic fuels, green hydrogen derivatives, chemicals, and construction materials. This shift is driving innovation in high-performance sorbents, hybrid membranes, and MOF-based systems designed for higher selectivity, lower energy demand, and continuous operation under industrial conditions. For instance, pilot-scale carbon utilization projects converting captured CO₂ into methanol, e-fuels, and carbonate-based building materials are creating strong demand for next-generation capture materials optimized for high purity output and seamless integration with downstream chemical conversion processes.

Carbon Capture Materials Market Scope

The carbon capture materials market is segmented on the basis of material type, material chemistry, capture technology, and end user.

- By Material Type

On the basis of material type, the carbon capture materials market is segmented into liquid solvents, solid sorbents, membranes, and advanced materials. The Solid Sorbents segment dominated the market with an estimated 34.38% share in 2025, owing to their high CO₂ capture efficiency, lower energy requirements for regeneration, and strong compatibility with both industrial flue gas and direct air capture systems. These materials, including zeolites, activated carbon, and engineered porous structures, are increasingly preferred for next-generation CCUS systems due to their stability and scalability. They also offer modular deployment advantages, making them suitable for both large-scale industrial plants and decentralized carbon capture units. Continuous advancements in material engineering are improving adsorption capacity and selectivity. However, challenges such as moisture sensitivity and long-term degradation still persist in some variants. Their versatility and growing adoption in DAC applications continue to reinforce market dominance.

The Advanced Materials segment is projected to register the fastest growth at a CAGR of 12.5% from 2026 to 2033, driven by rapid innovation in Metal–Organic Frameworks (MOFs), hybrid sorbents, and nanostructured capture media. These materials offer significantly higher surface area, tunable pore structures, and superior CO₂ selectivity compared to conventional materials. Increasing R&D investments by governments, research institutions, and private players are accelerating commercialization efforts. Their ability to operate efficiently under low-concentration CO₂ conditions makes them highly suitable for Direct Air Capture systems. Growing focus on energy-efficient regeneration cycles is further boosting adoption. Pilot-scale deployments in industrial decarbonization projects are validating their commercial potential.

- By Material Chemistry

On the basis of material chemistry, the market is segmented into amine-based materials, zeolites, activated carbon, Metal–Organic Frameworks (MOFs), silica-based materials, and bicarbonates. The Amine-based Materials segment dominated the market with an estimated 30.35% share in 2025, driven by their proven commercial viability and widespread use in post-combustion capture systems across power plants and industrial facilities. These materials are highly effective in selectively absorbing CO₂ from flue gases, making them the most established technology in large-scale CCUS deployment. Their strong industrial maturity ensures reliable performance and integration into existing infrastructure. Continuous optimization in solvent formulations is improving regeneration efficiency and reducing energy penalties. They are also widely supported by existing regulatory compliance frameworks. However, issues such as solvent degradation and corrosion remain key operational challenges.

The Metal–Organic Frameworks (MOFs) segment is expected to witness the fastest growth at a CAGR of 14.7% from 2026 to 2033, due to their ultra-high surface area, tunable chemistry, and exceptional CO₂ adsorption capacity. MOFs enable highly selective capture even at low partial pressures, making them ideal for Direct Air Capture and next-generation industrial applications. Rapid advancements in material synthesis techniques are reducing production costs and improving scalability. Increasing collaborations between research institutions and clean-tech companies are accelerating commercialization. Their structural flexibility allows customization for specific emission sources and operating conditions. Pilot projects in Europe and North America are demonstrating strong long-term potential for industrial deployment.

- By Capture Technology

On the basis of capture technology, the market is segmented into absorption, adsorption, membrane separation, cryogenic capture, and direct air capture. The Absorption segment dominated the market with an estimated 45.50% share in 2025, primarily due to the extensive use of liquid amine-based systems in industrial post-combustion capture applications. This technology is widely deployed in power generation, refining, and chemical industries due to its high CO₂ capture efficiency and established operational track record. It is also compatible with large-scale infrastructure, making it suitable for retrofitting existing plants. Continuous improvements in solvent chemistry are enhancing energy efficiency and reducing operational costs. Regulatory compliance requirements further support its dominance. Despite its maturity, high energy demand for regeneration remains a limitation.

The Direct Air Capture (DAC) segment is projected to register the fastest growth at a CAGR of 12.6% from 2026 to 2033, driven by increasing global focus on negative emissions technologies. DAC systems require highly advanced carbon capture materials capable of extracting CO₂ directly from ambient air at very low concentrations. This is creating strong demand for solid sorbents and MOF-based materials. Government funding and corporate net-zero commitments are accelerating deployment of DAC facilities. Technological advancements in modular capture units are improving scalability and cost efficiency. Pilot projects across North America and Europe are validating long-term commercial viability.

- By End User

On the basis of end user, the market is segmented into power generation, oil & gas, cement & steel, chemicals & fertilizers, transportation & fuels, and direct air capture operators. The Power Generation segment dominated the market with an estimated 30.35% share in 2025, driven by high carbon emissions intensity and strong regulatory pressure to decarbonize coal and gas-based power plants. Carbon capture materials are widely deployed in flue gas treatment systems to reduce emissions at large-scale utility plants. Government mandates and carbon pricing mechanisms are further accelerating adoption. Continuous upgrades in plant infrastructure are supporting integration of CCUS systems. The sector benefits from established capture technologies and large-scale operational feasibility. However, high installation and operating costs remain a challenge for widespread retrofitting.

The Direct Air Capture Operators segment is expected to witness the fastest growth at a CAGR of 15.8% from 2026 to 2033, driven by increasing investment in carbon removal technologies and net-zero commitments from governments and corporations. DAC operators require highly efficient and advanced carbon capture materials to extract CO₂ from ambient air at ultra-low concentrations. This is fueling demand for next-generation MOFs, engineered sorbents, and hybrid materials. Expanding carbon credit markets are improving economic viability for DAC projects. Strategic partnerships between technology providers and energy companies are accelerating deployment. Pilot-scale DAC plants are scaling rapidly across North America and Europe, supporting long-term growth potential.

Carbon Capture Materials Market Regional Analysis

North America dominated the global carbon capture materials market with the largest revenue share of 35.38% in 2025, supported by strong policy incentives, tax credits such as 45Q, and large-scale deployment of CCUS projects across power generation, oil & gas, and industrial sectors. The region also benefits from advanced carbon capture infrastructure, high investment in Direct Air Capture (DAC) facilities, and strong participation from oil & gas, power generation, and industrial sectors. Increasing regulatory pressure for emission reduction and rapid commercialization of next-generation materials such as solid sorbents and MOFs continue to strengthen North America’s leadership position in the global market.

U.S. Carbon Capture Materials Market Insight

The U.S. carbon capture materials market is experiencing robust growth due to strong federal incentives such as 45Q tax credits, large-scale CCUS project investments, and rapid expansion of Direct Air Capture facilities. The country’s advanced industrial base in oil & gas, power generation, cement, and chemicals is driving high demand for amine-based solvents and solid sorbents. Increasing collaboration between government agencies, energy companies, and clean-tech firms is accelerating commercialization of next-generation materials including MOFs and hybrid sorbents. Furthermore, strong focus on net-zero targets and carbon removal technologies is positioning the U.S. as a global leader in carbon capture innovation.

Europe Carbon Capture Materials Market Insight

The Europe carbon capture materials market remains a major contributor to global demand, driven by stringent climate regulations, strong carbon pricing mechanisms, and ambitious net-zero targets across major economies. Widespread deployment of CCUS projects across cement, steel, and chemical industries is supporting steady material consumption. Increasing investment in advanced capture technologies, including solid sorbents and membrane-based systems, is further strengthening the region’s market position. Moreover, strong government funding for clean energy transition and innovation in low-energy capture materials continues to enhance adoption across industrial sectors.

U.K. Carbon Capture Materials Market Insight

The U.K. carbon capture materials market is experiencing steady growth, supported by strong government backing for CCUS clusters, industrial decarbonization programs, and expanding carbon storage infrastructure. Increasing adoption of advanced capture technologies in power generation and heavy industries is driving demand for amine-based solvents and solid sorbents. Furthermore, growing research activities in Direct Air Capture and carbon utilization projects are encouraging innovation in next-generation materials. The country’s focus on achieving net-zero emissions and building integrated CCUS hubs is positioning it as a key innovation center in the region.

Germany Carbon Capture Materials Market Insight

The Germany carbon capture materials market is expanding steadily due to strong industrial emission reduction targets, advanced chemical and manufacturing sectors, and increasing investment in climate technology innovation. Automotive, steel, and chemical industries are actively exploring carbon capture solutions to meet stringent environmental regulations. Rising research in MOFs, adsorption-based systems, and energy-efficient regeneration technologies is further supporting material innovation. In addition, government initiatives promoting industrial decarbonization and circular carbon economy strategies are accelerating adoption across large-scale facilities.

Asia-Pacific Carbon Capture Materials Market Insight

The Asia-Pacific carbon capture materials market is expected to witness rapid growth, driven by increasing industrial emissions, expanding energy demand, and rising government focus on carbon neutrality across major economies such as China, India, and Japan. Growing investments in CCUS infrastructure, alongside rising adoption of clean energy technologies, are boosting demand for both conventional and advanced carbon capture materials. In addition, rapid industrialization and expansion of cement, steel, and power generation sectors are significantly contributing to market growth. Increasing awareness of environmental sustainability is further supporting regional adoption.

Japan Carbon Capture Materials Market Insight

The Japan carbon capture materials market is witnessing steady growth due to strong focus on hydrogen economy development, industrial decarbonization, and advanced environmental technologies. Major industrial players are increasingly adopting high-efficiency capture materials for power generation and chemical processing applications. Rising investments in Direct Air Capture research and CO₂ utilization technologies are further driving innovation in advanced sorbents and membrane systems. Moreover, Japan’s emphasis on energy efficiency and technological precision is supporting the adoption of next-generation carbon capture materials across R&D and industrial sectors.

China Carbon Capture Materials Market Insight

The China carbon capture materials market is growing rapidly, driven by large-scale industrial emissions, strong government policies supporting carbon neutrality goals, and massive investments in CCUS infrastructure. Expanding coal-based power generation, steel, and cement industries are creating significant demand for cost-effective carbon capture solutions. Increasing adoption of solid sorbents and amine-based systems, along with growing research in MOFs and advanced materials, is further accelerating market growth. In addition, rapid industrial modernization and policy-driven emission reduction initiatives are positioning China as one of the fastest-growing markets globally.

Carbon Capture Materials Market Share

The carbon capture materials industry is primarily led by well-established companies, including:

- Climeworks (Switzerland)

- Carbon Engineering Ltd. (Canada)

- Occidental Petroleum Corporation (U.S.)

- Shell plc (U.K.)

- ExxonMobil Corporation (U.S.)

- TotalEnergies SE (France)

- Equinor ASA (Norway)

- Linde plc (Ireland)

- Air Liquide S.A. (France)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Hitachi Zosen Corporation (Japan)

- BASF SE (Germany)

- SABIC (Saudi Arabia)

- Chevron Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- Svante Inc. (Canada)

- Aker Carbon Capture ASA (Norway)

- 3M (U.S.)

- Johnson Matthey plc (U.K.)

- Heidelberg Materials AG (Germany)

Latest Developments in Carbon Capture Materials Market

- In October 2024, Occidental Petroleum progressed its STRATOS Direct Air Capture project in Texas, one of the world’s largest DAC facilities under development using engineered chemical sorbent and solvent-based carbon capture systems. The project focuses on large-scale atmospheric CO₂ removal integrated with industrial decarbonization strategies. It reflects increasing investment from the oil and gas sector in advanced carbon capture materials and technologies

- In May 2024, Climeworks began operations at its “Mammoth” DAC plant in Iceland, marking one of the largest operational Direct Air Capture facilities in the world. The plant utilizes advanced solid sorbent systems designed for higher capture efficiency and reduced energy consumption during CO₂ regeneration cycles. It demonstrates the scaling potential of carbon capture materials in real industrial environments

- In October 2022, Climeworks advanced its “Mammoth” Direct Air Capture project in Iceland, designed to significantly scale CO₂ removal capacity using next-generation solid sorbent technology. The facility integrates modular capture units with improved adsorption materials and optimized regeneration processes to enhance efficiency compared to earlier systems. It represents a major step toward industrial-scale deployment of advanced carbon capture materials

- In November 2021, the United States Department of Energy (DOE) launched the “Carbon Negative Shot” initiative to accelerate breakthrough carbon capture and removal technologies, with a strong focus on advanced materials innovation. The program aims to reduce the cost and improve the efficiency of carbon removal solutions by supporting development of next-generation sorbents, membranes, and Metal–Organic Frameworks (MOFs). It targets gigaton-scale carbon dioxide removal in the coming decades while improving energy efficiency and system durability

- In September 2021, Climeworks launched “Orca,” the world’s first large-scale Direct Air Capture (DAC) and storage plant in Iceland, marking a major milestone in the deployment of solid sorbent-based carbon capture materials. The facility uses advanced adsorption materials to capture CO₂ directly from ambient air and permanently stores it underground through mineralization in basalt formations. This development demonstrated the commercial viability and real-world scalability of engineered sorbents in atmospheric carbon removal applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Carbon Capture Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Carbon Capture Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Carbon Capture Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.