Global Carbon Utilization Chemicals Market

Market Size in USD Billion

USD

54.85 Billion

USD

149.99 Billion

2025

2033

USD

54.85 Billion

USD

149.99 Billion

2025

2033

| 2026 - 2033 | |

| USD 54.85 Billion | |

| USD 149.99 Billion | |

| % | |

|

Carbon Utilization Chemicals Market Overview

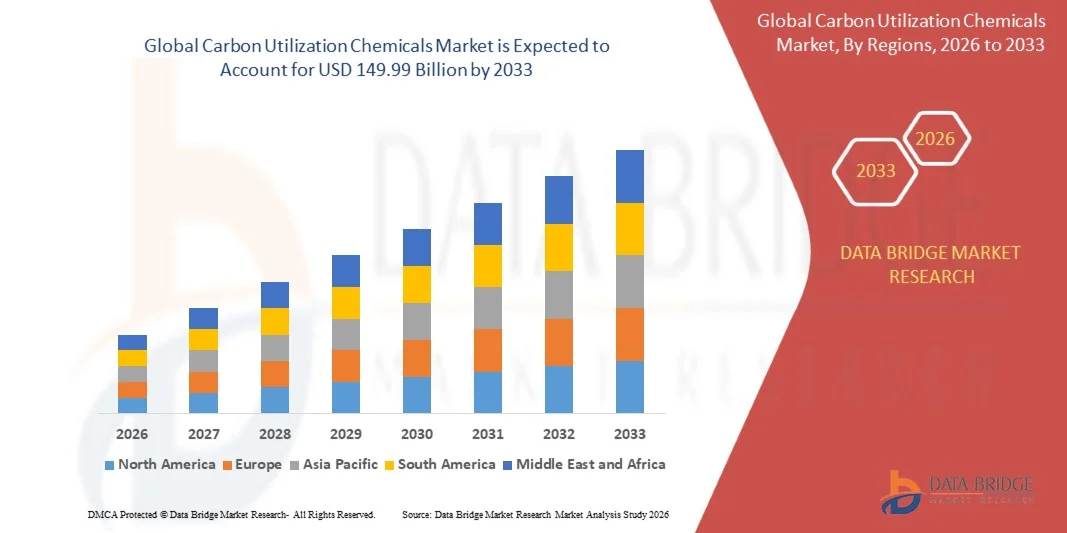

As per Data Bridge Market Research Analysis, the Carbon Utilization Chemicals Market was valued at USD 54.85 Billion in 2025 and is projected to reach USD 149.99 Billion by 2033, growing at a CAGR of 13.40% from 2026 to 2033. Carbon utilization chemicals comprise a broad spectrum of chemical products derived from captured carbon dioxide (CO₂) through various conversion processes, including catalytic hydrogenation, electrochemical reduction, biological fermentation, and mineral carbonation. These processes transform industrial CO₂ emissions into commercially valuable products such as methanol, ethanol, polymers, carbonates, urea, fertilizers, and synthetic fuels, enabling industrial operators to monetize carbon streams while reducing net atmospheric emissions. The market is experiencing robust expansion as governments and industries worldwide intensify efforts to decarbonize the economy and transition toward circular carbon models.

Companies across industries are prioritizing low-carbon and carbon-negative materials as part of their long-term net-zero strategies, leading to rising demand for solutions produced from captured carbon dioxide. The chemicals sector alone is responsible for approximately 5% of CO₂ that needs to be captured by 2030 in the IEA's net-zero emissions scenario, with ammonia, methanol, and high-value chemicals accounting for 45%, 28%, and 27% of primary chemical emissions, respectively. Rapid technological innovation in catalysis, electrolysis, and system integration is lowering costs and improving performance, supporting the market's shift from small-scale demonstrations to full commercial operations.

Market Size & Forecast

- Global Market Value (2025): USD 85 Billion

- Expected Market Value (2033): USD 149.99 Billion

- Forecast CAGR (2026–2033): 13.40%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: Europe

Key Market Trends & Insights

- The Carbon Utilization Chemicals Market is undergoing a significant transition from pilot-scale demonstrations to commercial-scale production, with integrated production models combining renewable hydrogen, concentrated CO₂ sources, and bioenergy systems creating powerful deployment pathways.

- The Alcohols & Platform Chemicals segment accounted for a significant share in 2025 and is projected to grow at a robust CAGR, driven by expanding production of methanol and ethanol derived from captured CO₂ and renewable hydrogen.

- The Catalytic Hydrogenation segment accounted for a significant share in 2025 and is anticipated to grow at a strong CAGR through the forecast period, supported by mature catalyst systems, well-defined process designs, and proven industrial implementation.

- The Construction sector is emerging as a major end-user, with expanding adoption of CO₂-enhanced concrete materials and low-carbon cement driven by stricter specifications for lower-emission building inputs.

- Asia-Pacific accounted for the largest regional share in 2025, with a volume share of 46.13%. driven by rapid industrialization and aggressive government policies promoting carbon capture and utilization technologies.

- Europe is expected to grow at a substantial CAGR, supported by major climate policies, regional initiatives to expand CO₂ storage capacity, and long-term plans to develop a cross-border CO₂ commodity market.

- Rapid technological innovation across catalysis, electrolysis systems, and process integration is driving cost and performance reductions, with new catalyst materials demonstrating increased selectivity, activity, and stability for CO₂

Report Scope and Carbon Utilization Chemicals Market Segmentation

|

Attributes |

Carbon Utilization Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Covestro AG (Germany) · BASF SE (Germany) · LanzaTech Global, Inc. (U.S.) · Air Liquide S.A. (France) · Carbon Clean (U.K.) · Climeworks AG (Switzerland) · Aker Carbon Capture ASA (Norway) · Carbon Recycling International (CRI) (Iceland) · Mitsubishi Chemical Group Corporation (Japan) · SK Innovation Co., Ltd. (South Korea) · TotalEnergies SE (France) · SABIC (Saudi Arabia) · Econic Technologies Ltd. (U.K.) · CarbonCure Technologies Inc. (Canada) · Solidia Technologies, Inc. (U.S.) · Avantium N.V. (Netherlands) · Novomer Inc. (U.S.) · LyondellBasell Industries N.V. (U.S.) · Borealis AG (Austria) · Eastman Chemical Company (U.S.) |

|

Market Opportunities |

· Expansion into green fertilizer and fuel markets through CO₂-derived ammonia, methanol, and synthetic fuels · Industrial symbiosis and waste valorization through integrated carbon utilization networks · Growing demand for sustainable aviation fuel (SAF) driven by mandatory blending targets in the EU, U.K., and U.S. · Development of CO₂-derived polymers and building materials for construction and automotive applications · Leveraging carbon pricing mechanisms and tax incentives (e.g., U.S. Section 45Q) to improve project economics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Carbon Utilization Chemicals Market Trends

Trend: Commercial-Scale Deployment and Integrated Production Models

The carbon utilization chemicals market is experiencing a pivotal shift from pilot-scale demonstrations to full commercial operations. Integrated production models combining renewable hydrogen, concentrated CO₂ sources, and bioenergy systems are creating powerful pathways for deployment. Commercial-scale facilities in multiple regions are producing renewable methanol that serves as a key feedstock for chemical and fuel markets. This trend is accelerated by the growing number of publicly announced carbon management projects across the U.S. value chain, driven by federal investment and supportive policies. As technologies mature and project economics improve, the market is expected to witness a wave of large-scale commercial facilities coming online, transforming carbon utilization from an emerging concept into a mainstream industrial practice.

Carbon Utilization Chemicals Market Dynamics

Key Market Driver: Expanding Carbon Pricing and Net-Zero Mandates

A primary driver of the carbon utilization chemicals market is the expanding implementation of carbon pricing mechanisms and net-zero commitments worldwide. Carbon pricing mechanisms, including the EU Emissions Trading System and emerging schemes in Canada, South Korea, and China, raise the financial cost of emitting CO₂ and increase the relative economic attractiveness of carbon utilization pathways. Industrial operators subject to carbon pricing can offset compliance costs by converting captured emissions into saleable products. National net-zero commitments create regulatory and reputational pressure on heavy industrial emitters to demonstrate active carbon management beyond simple offset procurement. These combined drivers make carbon utilization economically rational and strategically necessary for cement, steel, power, and chemical sector operators.

Key Restraint/Challenge: High Energy Requirements and Lifecycle Carbon Concerns

A significant restraint in the global driving simulator market is the high upfront capital required for advanced simulation systems. Modern platforms integrate high-fidelity graphics, realistic vehicle dynamics engines, motion platforms, and immersive virtual environments, demanding substantial investment in procurement, installation, and ongoing maintenance. The total cost of ownership extends to software licenses, periodic upgrades, and technical support, making adoption difficult for smaller driving schools, research institutions, and emerging-market organizations.

The October 2024 launch of the Dresden Driving Simulator (DDS), a world-first sustained acceleration simulator for ADAS and highly automated driving research developed by AMST and Technische University Dresden, illustrates the scale of capital commitment required for cutting-edge simulation infrastructure, reflecting the broader challenge of adoption beyond well-funded organizations.

Key Market Opportunity: Sustainable Aviation Fuel and Synthetic Fuels

Mandatory sustainable aviation fuel blending targets adopted by the European Union, the United Kingdom, and the United States create structural demand for synthetic fuels produced from captured industrial CO₂. Carbon-based synthetic aviation fuels offer near-term scalability advantages over biofuels constrained by feedstock availability. Airlines face escalating SAF purchase obligations and ESG investor scrutiny that make synthetic fuel offtake agreements commercially attractive. Established industrial CO₂ sources at refineries, chemical plants, and power facilities provide reliable feedstock for co-located synthetic fuel production. Government production tax credits and mandated fuel blending requirements provide revenue certainty for SAF project developers, positioning sustainable aviation fuel as a high-growth application for carbon utilization chemicals.

Carbon Utilization Chemicals Market Scope

The carbon utilization chemicals market is segmented based on product type, technology, and end-use industry.

- By Product Type

On the basis of product type, the Carbon Utilization Chemicals Market is segmented into alcohols & platform chemicals, polymers & resins, carbonates, urea & fertilizers, industrial gases, and others. The alcohols & platform chemicals segment accounted for a significant share in 2025 and is projected to grow at a robust CAGR, driven by expanding production of methanol and ethanol derived from captured CO₂ and renewable hydrogen. Renewable methanol serves as a key feedstock for chemical and fuel markets, with commercial-scale facilities already producing it in multiple regions. The Polymers & Resins segment is gaining traction as CO₂-derived polyols and polycarbonates are increasingly adopted in automotive and construction applications. Urea & fertilizers represent a significant segment, leveraging captured CO₂ for agricultural applications. Industrial gases produced through carbon capture and utilization pathways continue to represent an important market segment, particularly across food processing, beverage carbonation, and industrial applications. The market is also witnessing growing interest in CO₂-derived carbonates and specialty chemicals, reflecting the expanding portfolio of commercially viable CO₂-based products.

- By Technology

On the basis of technology, the Carbon Utilization Chemicals Market is segmented into catalytic hydrogenation, electrochemical reduction, biological fermentation, mineral carbonation, and others. The catalytic hydrogenation segment accounted for a significant share in 2025 and is anticipated to grow at a strong CAGR through the forecast period. This technology is supported by mature catalyst systems, well-defined process designs, and proven industrial implementation. Next-generation methanol synthesis catalysts featuring Cu, ZnO, and Al₂O₃ compositions are reaching selectivity levels above 99% while achieving yields comparable to conventional processes. Catalyst systems based on cobalt and iron enable the conversion of CO₂-derived syngas into synthetic hydrocarbons. Electrochemical reduction is emerging as a promising technology, achieving increased current densities that reduce capital investment through compact system design. Biological fermentation leverages microorganisms to convert CO₂ into ethanol and proteins, while mineral carbonation transforms CO₂ into stable carbonates for construction materials. The diversification of technology pathways is enabling a broader range of CO₂-derived products and applications.

- By End-Use Industry

On the basis of end-use industry, the Carbon Utilization Chemicals Market is segmented into automotive, construction, chemicals & materials, power generation, agriculture, and others. The construction segment held a significant share in 2025 and is projected to grow at a strong CAGR, driven by expanding adoption of CO₂-enhanced concrete materials and low-carbon cement. Increasing investments in infrastructure across major regions are incorporating stricter specifications for lower-emission building inputs. The Automotive segment is adopting CO₂-derived polyols used in vehicle interior components, driven by OEM procurement targets for low-carbon materials. The Chemicals & Materials segment remains the largest end-user, leveraging CO₂-derived feedstocks for a wide range of chemical products. Power Generation facilities are adopting carbon capture and utilization to reduce emissions and generate revenue from CO₂-derived products. The Agriculture segment is emerging as a growth area through CO₂-derived fertilizers and soil amendments. Industrial symbiosis and waste valorization are creating new opportunities across multiple end-use industries.

Carbon Utilization Chemicals Market Regional Analysis

Asia-Pacific Carbon Utilization Chemicals Market Insight

Asia-Pacific accounted for the largest regional share in 2025. The region's leadership is driven by rapid industrialization, aggressive government policies promoting carbon capture and utilization technologies, and the presence of major industrial CO₂ emitters across China, India, Japan, and South Korea. China is at the forefront of carbon utilization deployment, with significant investments in CO₂-to-chemicals projects and strong government support for carbon neutrality goals. The country's eagerness to develop chemical feedstocks that do not depend on imported petroleum is accelerating the adoption of carbon utilization technologies. Japan and South Korea are also witnessing growing investments in carbon utilization infrastructure, supported by government initiatives promoting low-carbon technologies and industrial decarbonization. The region's expanding industrial base, coupled with rising environmental awareness and regulatory pressure, is expected to maintain Asia-Pacific's dominance throughout the forecast period.

Europe Carbon Utilization Chemicals Market Insight

Europe held a significant market share in 2025 and is expected to register one of the fastest growth rates during the forecast period. The region benefits from major climate policies designed to promote large-scale carbon management, including the EU Emissions Trading System, the ReFuelEU Aviation mandate, and the FuelEU Maritime regulation. Regional initiatives aim to expand CO₂ storage capacity to 50 million tons per year by 2030, alongside long-term plans to develop a cross-border CO₂ commodity market by 2040 targeting 280 million tons in annual capture. The European Union's ambitious decarbonization targets and the implementation of the FuelEU Maritime regulation are driving demand for carbon-derived chemicals in the shipping and aviation sectors. Key players such as Covestro AG, BASF SE, and Air Liquide S.A. are headquartered in Europe, supporting regional market growth.

North America Carbon Utilization Chemicals Market Insight

North America represents a significant market for carbon utilization chemicals, supported by strong policy incentives, a mature industrial base, and growing corporate net-zero commitments. The United States is at the forefront of carbon utilization development, driven by the Inflation Reduction Act's Section 45Q tax credit and the One Big Beautiful Bill Act of 2025, which maintains the 45Q tax credit and creates parity between permanent storage and carbon utilization. There are over 270 publicly announced carbon management projects across the U.S. value chain due to federal investment. Key companies supporting regional market growth include LanzaTech Global, Inc., Novomer Inc., along with international technology providers such as Carbon Clean (U.K.). The region's strong venture capital funding for clean technology startups and favorable regulatory environment for carbon utilization innovation are further accelerating market growth. Canada is also investing in carbon capture and utilization infrastructure through federal and provincial initiatives, contributing to the region's overall market expansion.

Latin America Carbon Utilization Chemicals Market Insight

Latin America represents an emerging market for carbon utilization chemicals, with growing demand influenced by increasing investments in renewable energy, government incentives for clean fuel adoption, and the region's abundant bioenergy resources. Countries such as Brazil and Argentina are witnessing significant investments in carbon capture and utilization projects, supported by policies promoting sustainable development and reducing emissions. Brazil's established bioenergy sector provides a foundation for integrating carbon utilization with bioenergy with carbon capture and storage (BECCS) pathways. The region's expanding industrial base and growing awareness of carbon management technologies are creating opportunities for carbon utilization chemicals. However, market growth is currently constrained by limited regulatory frameworks, higher technology costs compared to developed regions, and fragmented policy support. The development of regional supply chains and partnerships with global carbon utilization technology providers is expected to accelerate market growth.

Middle East & Africa Carbon Utilization Chemicals Market Insight

The Middle East and Africa region represents a nascent market for carbon utilization chemicals, with demand primarily concentrated in the GCC countries. Governments across the region are increasing investments in carbon capture and utilization technologies to reduce carbon emissions and diversify their economies away from fossil fuel dependence. Saudi Arabia is expanding its carbon management infrastructure as part of its Vision 2030 initiative, with significant investments in carbon capture and utilization projects. The UAE is investing in clean fuel technologies and sustainable chemical production, positioning itself as a regional hub for carbon utilization innovation. South Africa is gradually adopting carbon management technologies to support the growing demand for cleaner industrial processes. Increasing investments from global technology providers and the availability of low-cost renewable energy in the region are improving the commercial viability of carbon utilization projects. However, relatively low adoption of carbon management technologies, limited regulatory frameworks, and high capital costs continue to restrain market growth.

Carbon Utilization Chemicals Market Share

The Carbon Utilization Chemicals industry is primarily led by well-established companies, including:

- Covestro AG (Germany)

- BASF SE (Germany)

- LanzaTech Global, Inc. (U.S.)

- Air Liquide S.A. (France)

- Carbon Clean (U.K.)

- Climeworks AG (Switzerland)

- Aker Carbon Capture ASA (Norway)

- Carbon Recycling International (CRI) (Iceland)

- Mitsubishi Chemical Group Corporation (Japan)

- SK Innovation Co., Ltd. (South Korea)

- TotalEnergies SE (France)

- SABIC (Saudi Arabia)

- Econic Technologies Ltd. (U.K.)

- CarbonCure Technologies Inc. (Canada)

- Solidia Technologies, Inc. (U.S.)

- Avantium N.V. (Netherlands)

- Novomer Inc. (U.S.)

- LyondellBasell Industries N.V. (U.S.)

- Borealis AG (Austria)

- Eastman Chemical Company (U.S.)

Latest Developments in Carbon Utilization Chemicals Market

- In March 2026, Econic Technologies and Changhua Chemical launched the world's first commercial-scale production facility for polycarbonate ether (PCE) polyols, a new class of sustainable polyols made with carbon dioxide. Branded as Carnol, the polyols are based on Econic's proprietary technology and have a 30% lower carbon footprint versus typical polyols. The facility, located in Lianyungang, Jiangsu province, China, is expected to produce about 80,000 tons of Carnol in 2026, with plans to scale to more than one million tons in the coming years. Econic Technologies is also expanding the global reach of its carbon utilization technology through multiple partnerships, including licensing its polyols technology to Monument in the United States.

- In July 2025, the U.S. Congress passed and President Trump signed the One Big Beautiful Bill Act (OBBBA) into law on July 4, 2025. The legislation includes a critical update to the Section 45Q tax credit that creates parity between carbon dioxide sequestration and CO₂ utilization, while maintaining the Section 45Q tax credit at USD 85 per metric ton for point-source capture and USD 180 per metric ton for direct air capture in dedicated geologic storage.

- In June 2025, FertigHy unveiled plans to build a low-carbon calcium ammonium nitrate (CAN27) production facility in Northern France, utilizing only air, water, and zero-carbon electricity as raw materials. Backed by a $1.3 billion investment, the facility will produce 500,000 metric tonnes annually using ammonia derived from electrolytic hydrogen, replacing conventional natural gas. This represents a significant advancement in low-carbon fertilizer production.

- In January 2025, the U.S. Department of Energy's Office of Fossil Energy and Carbon Management announced $101 million in federal funding for five projects to support the development of carbon dioxide (CO₂) capture, removal, and conversion test centers for cement manufacturing facilities and power plants. The announcement built on the Inflation Reduction Act's Section 45Q tax credit framework.

- In January 2024, Covestro AG introduced Desmopan 37385A, the first thermoplastic polyurethane (TPU) product produced using carbon dioxide technology. The company is developing and marketing a new type of polyether carbonate polyol called cardyon™, which uses carbon dioxide in its production process. Covestro's ongoing commitment to carbon utilization R&D and commercial-scale production capacity strengthened its competitive position.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Carbon Utilization Chemicals Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Carbon Utilization Chemicals Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Carbon Utilization Chemicals Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.