Global Carcinoembryonic Antigen Cea Market

Market Size in USD Billion

USD

2.31 Billion

USD

3.62 Billion

2025

2033

USD

2.31 Billion

USD

3.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.31 Billion | |

| USD 3.62 Billion | |

| % | |

|

Carcinoembryonic Antigen (CEA) Market Overview

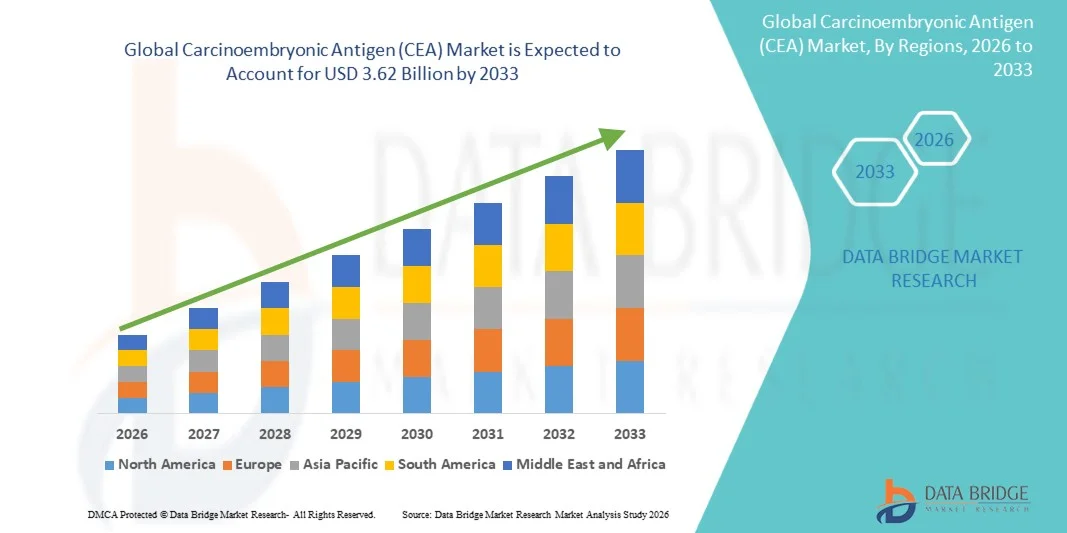

The Carcinoembryonic Antigen (CEA) Market was valued at USD 2.31 billion in 2025 and is projected to reach USD 3.62 billion by 2033, growing at a CAGR of 5.80% from 2026 to 2033. The Carcinoembryonic Antigen (CEA) Market is experiencing steady growth driven by the rising global burden of cancer, particularly colorectal, pancreatic, gastric, and breast cancers, where CEA is widely used as a tumor marker for diagnosis, prognosis, and treatment monitoring.

Increasing adoption of early cancer screening programs and routine tumor marker testing is significantly boosting demand for CEA testing across hospitals and diagnostic laboratories. Growing awareness of early cancer detection and improved survival outcomes is encouraging physicians to incorporate biomarker-based testing into standard oncology workflows. Rapid advancements in immunoassay technologies, including chemiluminescence immunoassays (CLIA), ELISA-based platforms, and automated analyzers, are enhancing the sensitivity, accuracy, and turnaround time of CEA detection. These technological improvements are supporting high-throughput testing in modern diagnostic laboratories.

Key Market Trends & Insights

- North America dominated the Carcinoembryonic Antigen (CEA) Market with the largest revenue share of 34% in 2025, supported by advanced training infrastructure and strong government investments in simulation technology.

- The Serology Tests segment dominated the market with a 57.84% share in 2025, owing to its cost-effectiveness, rapid turnaround time, and wide availability across diagnostic laboratories and hospitals.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR from 2026 to 2033, fueled by rising urbanization, increasing training infrastructure investments, and growing adoption in China, India, and Japan.

- The CD66e (CEACAM5) product type segment held the largest share of 38.9% in 2025, driven by its strong clinical relevance as the primary biomarker used in CEA testing for colorectal and gastrointestinal cancers.

- The Male patient segment accounted for a 52.1% revenue share in 2025, attributed to a higher prevalence of colorectal and gastrointestinal cancers in male populations and increased screening uptake in high-risk groups.

- The Colorectal Cancer application segment dominated the market with a 44.7% share in 2025, supported by rising global incidence rates, strong clinical reliance on CEA as a monitoring biomarker, and expanding use in post-treatment recurrence detection.

- The Hospitals segment led the end-user category with a 48.6% revenue share in 2025, driven by high patient inflow, availability of advanced diagnostic infrastructure, and integration of CEA testing into routine oncology diagnostic workflows.

Market Size & Forecast

- Global Market Value (2025): USD 2.31 Billion

- Expected Market Value (2033): USD 3.62 Billion

- Forecast CAGR (2026–2033): 5.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Carcinoembryonic Antigen (CEA) Market Segmentation

|

Attributes |

Carcinoembryonic Antigen (CEA) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Roche Diagnostics (Switzerland) |

|

Market Opportunities |

· Rising demand for early cancer diagnostics · Expansion of personalized and companion diagnostics · Technological advancements in immunoassay and biomarker testing |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Carcinoembryonic Antigen (CEA) Market Trends

Trend: Expanding Use of Carcinoembryonic Antigen (CEA) in Early Cancer Detection and Disease Monitoring

The Carcinoembryonic Antigen (CEA) Market is witnessing strong growth due to increasing adoption of tumor biomarkers for early cancer detection, prognosis assessment, and post-treatment monitoring. CEA testing is widely used in colorectal, gastrointestinal, pancreatic, breast, and lung cancers to evaluate disease progression and recurrence risk. For instance, clinical oncology guidelines in several regions recommend CEA testing as part of routine follow-up for colorectal cancer patients, where elevated CEA levels can indicate tumor recurrence before radiological evidence becomes visible. The rising global cancer burden, with colorectal cancer among the most commonly diagnosed malignancies worldwide, is significantly increasing demand for reliable and cost-effective tumor marker testing across hospitals and diagnostic laboratories.

Carcinoembryonic Antigen (CEA) Market Dynamics

Key Market Driver: Rising Cancer Prevalence and Increasing Adoption of Tumor Biomarker-Based Diagnostics

A major driver of the CEA market is the increasing global incidence of cancer, particularly colorectal and gastrointestinal cancers, which are strongly associated with elevated CEA levels. According to the World Health Organization, cancer remains one of the leading causes of mortality globally, with millions of new cases reported annually, creating sustained demand for early diagnostic and monitoring tools.

CEA testing plays a critical role in oncology workflows by supporting treatment monitoring, recurrence detection, and therapy response evaluation. Hospitals and diagnostic centers are increasingly integrating tumor marker panels, including CEA, into routine cancer screening programs for high-risk patients. In addition, the expansion of oncology screening programs, growing awareness of early cancer detection, and increasing adoption of automated immunoassay analyzers are improving testing accessibility and turnaround times. The growing use of CEA in combination with imaging techniques and other biomarkers further enhances diagnostic accuracy and clinical decision-making in cancer management.

Key Restraint/Challenge: Limited Specificity and Variability in Clinical Interpretation of CEA Levels

A significant challenge in the global CEA market is the limited specificity of the biomarker, as elevated CEA levels can also occur in non-cancerous conditions such as smoking, inflammation, liver disease, and gastrointestinal disorders. This reduces its standalone diagnostic reliability and necessitates confirmation through additional imaging and diagnostic tests.

In addition, variability in laboratory standards, assay methods, and cutoff values across regions can lead to inconsistent clinical interpretation. In low-resource settings, limited access to advanced immunoassay platforms and skilled laboratory personnel further restricts widespread adoption. Reimbursement limitations for tumor marker testing in certain healthcare systems also pose barriers to routine use, particularly for screening asymptomatic populations.

Key Market Opportunity: Integration of Multi-Biomarker Panels and AI-Assisted Oncology Diagnostics

The integration of CEA testing into multi-biomarker cancer panels and AI-assisted diagnostic platforms presents a significant growth opportunity for the market. Combining CEA with other tumor markers such as CA 19-9, CA-125, and AFP improves diagnostic sensitivity and supports more accurate cancer profiling.

For instance, hospitals are increasingly adopting automated immunoassay systems capable of running multiplex biomarker panels for faster and more comprehensive cancer evaluation. In addition, artificial intelligence and machine learning algorithms are being used to analyze longitudinal CEA level trends, helping clinicians predict recurrence risk and treatment response more effectively.

The expansion of precision oncology programs, rising investments in cancer screening infrastructure across North America and Europe, and growing healthcare access in Asia-Pacific are expected to further accelerate adoption of advanced CEA-based diagnostic solutions over the forecast period.

Carcinoembryonic Antigen (CEA) Market Scope

The Carcinoembryonic Antigen (CEA) market is segmented on the basis of test type, product type, gender, application, and end user.

- By Test Type

On the basis of test type, the Carcinoembryonic Antigen (CEA) Market is segmented into molecular tests and serology tests. The Serology Tests segment dominated the market with a 57.84% share in 2025, owing to its cost-effectiveness, rapid turnaround time, and wide availability across diagnostic laboratories and hospitals. These tests are extensively used for routine cancer screening and monitoring of treatment response in colorectal and gastrointestinal cancers. High adoption in both developed and emerging healthcare systems is further supported by ease of use and established clinical workflows. Growing awareness regarding early cancer detection is strengthening demand. Increasing hospital-based testing volumes is also contributing to dominance. Strong integration into standard oncology diagnostics pathways supports segment leadership. Expanding reimbursement coverage in several countries is further accelerating adoption. Rising geriatric population is increasing diagnostic demand. Continuous technological improvements are enhancing sensitivity and accuracy. Overall accessibility makes serology testing the preferred choice globally.

The Molecular Tests segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by increasing demand for precision oncology and early-stage cancer detection. These tests enable highly accurate genetic and biomarker-level analysis, improving diagnostic reliability. Rising adoption of personalized medicine is significantly boosting demand. Increasing integration of PCR and sequencing-based technologies is accelerating market penetration. Growing investment in advanced oncology diagnostics is supporting expansion. Hospitals and cancer centers are rapidly adopting molecular platforms. Higher sensitivity compared to traditional methods is driving preference. Technological advancements are reducing cost barriers. Expanding clinical research in oncology is further strengthening growth. Government initiatives supporting cancer screening programs are boosting adoption. Increasing use in companion diagnostics is accelerating demand. Overall, molecular diagnostics is emerging as the fastest-evolving segment.

- By Product Type

On the basis of product type, the global CEA market is segmented into CD66a, CD66b, CD66c, CD66d, CD66e, and CD66f. The CD66e segment dominated the market with a 38.92% share in 2025, as it is most strongly associated with tumor cell adhesion and widely used in colorectal cancer diagnostics. High clinical relevance in gastrointestinal malignancies is a key growth driver. Strong adoption in hospital diagnostic panels supports dominance. Extensive use in oncology biomarker testing further strengthens demand. Established commercial availability across reagent kits enhances penetration. Growing use in cancer monitoring applications is increasing utilization. Rising global cancer burden is supporting segment expansion. Strong research validation improves clinical confidence. Increasing inclusion in diagnostic workflows boosts adoption. Pharmaceutical collaborations for biomarker research are rising. Expanding laboratory infrastructure is reinforcing usage. Overall clinical utility makes CD66e the leading segment.

The CD66c segment is expected to register the fastest CAGR of 7.8% from 2026 to 2033, driven by its emerging role in tumor progression and metastasis research. Increasing focus on advanced cancer biomarker profiling is supporting demand. Rising adoption in breast and lung cancer diagnostics is accelerating growth. Expanding research funding in oncology is boosting utilization. Growing use in precision medicine applications is strengthening market expansion. Development of advanced immunoassay kits is improving accessibility. Increasing academic research is supporting validation studies. Rising pharmaceutical interest in targeted therapy development is driving demand. Technological improvements in antibody engineering are enhancing accuracy. Growing integration into multiplex diagnostic panels is increasing adoption. Expanding clinical trials is further supporting usage. Overall, CD66c is emerging as the fastest-growing biomarker segment.

- By Gender

On the basis of gender, the global CEA market is segmented into male and female. The Male segment dominated the market with a 52.63% share in 2025, owing to higher incidence rates of colorectal and gastrointestinal cancers among men. Lifestyle risk factors such as smoking and alcohol consumption contribute significantly to higher diagnostic volumes. Strong screening participation in male populations further supports dominance. Increasing hospital-based cancer detection programs are boosting demand. Higher occupational exposure risks also contribute to elevated incidence. Growing awareness campaigns targeting male cancer screening are supporting uptake. Rising geriatric male population is increasing testing needs. Strong adoption of routine oncology diagnostics is reinforcing segment leadership. Expanding insurance coverage is improving accessibility. Government screening initiatives are strengthening participation. Increasing clinical focus on early detection in men is boosting demand. Overall epidemiological trends favor this segment.

The Female segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing incidence of breast, ovarian, and gastrointestinal cancers. Rising awareness regarding early cancer detection among women is supporting demand. Expanding screening programs in women’s health is accelerating adoption. Increasing availability of non-invasive diagnostic options is boosting participation. Growing healthcare access in emerging economies is strengthening uptake. Rising investment in oncology research focused on female cancers is driving growth. Increasing use of biomarkers in reproductive-age women is expanding applications. Government-led awareness campaigns are improving screening rates. Technological advancements in diagnostics are enhancing accuracy. Rising hospital visits for preventive testing are increasing volumes. Expanding insurance coverage for cancer diagnostics is supporting adoption. Overall, female oncology diagnostics is growing rapidly.

- By Application

On the basis of application, the global CEA market is segmented into gastrointestinal cancer, colorectal cancer, pancreatic cancer, breast cancer, lung cancer, thyroid cancer, ovarian cancer, and others. The Colorectal Cancer segment dominated the market with a 34.18% share in 2025, due to the strong clinical association of CEA as a primary biomarker. High global incidence of colorectal cancer is a major growth driver. Routine use of CEA in post-treatment monitoring supports dominance. Strong integration in oncology diagnostic guidelines enhances adoption. Increasing screening programs worldwide are boosting demand. Growing hospital diagnostic volumes are reinforcing usage. High recurrence monitoring requirements further support segment growth. Expanding geriatric population increases risk prevalence. Rising awareness of early detection improves testing rates. Strong reimbursement support in developed markets enhances accessibility. Continuous advancements in oncology diagnostics strengthen utilization. Overall, colorectal cancer remains the core application segment.

The Lung Cancer segment is projected to witness the fastest CAGR of 8.3% from 2026 to 2033, driven by rising global incidence and increasing environmental risk factors. Growing adoption of CEA alongside other biomarkers is improving diagnostic accuracy. Expanding use in combination cancer panels is supporting demand. Increasing focus on early-stage lung cancer detection is accelerating growth. Rising smoking-related disease burden is boosting testing requirements. Advancements in liquid biopsy technologies are enhancing clinical adoption. Growing investment in respiratory oncology research is strengthening applications. Increasing hospital-based screening programs are supporting uptake. Rising use in treatment monitoring is expanding utility. Technological improvements in diagnostic sensitivity are enhancing performance. Expanding healthcare infrastructure is increasing accessibility. Overall, lung cancer diagnostics is emerging as the fastest-growing application.

- By End User

On the basis of end user, the global CEA market is segmented into hospitals, diagnostic centers, cancer centers, and research & academic institutes. The Hospitals segment dominated the market with a 46.27% share in 2025, owing to high patient inflow and strong diagnostic infrastructure. Hospitals serve as primary points for cancer diagnosis and monitoring. Integrated laboratory facilities support high testing volumes. Strong adoption of routine oncology screening programs drives demand. Availability of advanced diagnostic technologies enhances accuracy. Increasing hospitalization rates for cancer patients boosts usage. Strong reimbursement systems in hospitals improve accessibility. Rising oncology department expansions support growth. Continuous adoption of automated testing platforms strengthens efficiency. Growing collaborations with diagnostic companies enhance capabilities. High trust in hospital-based diagnostics supports dominance. Overall, hospitals remain the central testing hub globally.

The Cancer Centers segment is expected to register the fastest CAGR of 7.6% from 2026 to 2033, driven by increasing specialization in oncology care. Rising adoption of advanced biomarker testing is supporting demand. Expansion of dedicated cancer treatment facilities is boosting utilization. Increasing focus on precision oncology is accelerating growth. Strong integration of molecular diagnostics enhances capabilities. Growing investment in cancer research infrastructure is supporting adoption. Rising patient preference for specialized care centers is increasing volumes. Technological advancements in oncology diagnostics are improving efficiency. Expanding clinical trials in cancer centers are boosting testing demand. Government funding for cancer treatment facilities is strengthening growth. Increasing multidisciplinary treatment approaches are supporting adoption. Overall, cancer centers are emerging as the fastest-growing end user segment.

Carcinoembryonic Antigen (CEA) Market Regional Analysis

North America dominated the Carcinoembryonic Antigen (CEA) Market and accounted for the largest revenue share of 34% in 2025, supported by advanced oncology diagnostic infrastructure, strong adoption of tumor biomarker testing, and the presence of well-established hospital and clinical laboratory networks. The region also benefits from high prevalence of colorectal and gastrointestinal cancers, strong awareness of early cancer screening, and robust reimbursement frameworks supporting routine diagnostic testing. Increasing integration of automated immunoassay analyzers and expanding use of multi-biomarker cancer panels continue to strengthen North America’s leadership position in the global market.

U.S. Carcinoembryonic Antigen (CEA) Market Insight

The U.S. Carcinoembryonic Antigen (CEA) market is witnessing strong growth due to rising incidence of colorectal and gastrointestinal cancers, increasing adoption of early cancer screening programs, and strong presence of advanced diagnostic laboratories. The country’s well-established healthcare infrastructure, widespread use of tumor marker testing in oncology workflows, and growing adoption of automated and high-throughput immunoassay systems are driving demand across hospitals and diagnostic centers. In addition, increasing focus on precision oncology and early detection initiatives is further supporting market expansion.

Europe Carcinoembryonic Antigen (CEA) Market Insight

The Europe Carcinoembryonic Antigen (CEA) market remains a major contributor to global revenue, driven by strong government-backed cancer screening programs, advanced diagnostic capabilities, and increasing adoption of tumor biomarker testing. Widespread use of CEA testing for colorectal cancer monitoring and post-treatment surveillance is supporting regional growth. In addition, strong healthcare systems, rising cancer awareness, and increasing investment in laboratory automation technologies are further enhancing market adoption across the region.

U.K. Carcinoembryonic Antigen (CEA) Market Insight

The U.K. Carcinoembryonic Antigen (CEA) market is experiencing steady growth, supported by increasing cancer screening initiatives, strong NHS-driven diagnostic programs, and rising adoption of tumor marker testing in clinical practice. Growing focus on early detection of colorectal cancer and increasing use of CEA in patient monitoring and recurrence assessment are contributing to market expansion. Furthermore, advancements in laboratory automation and improved access to diagnostic services are enhancing testing efficiency.

Germany Carcinoembryonic Antigen (CEA) Market Insight

The Germany Carcinoembryonic Antigen (CEA) market is expanding steadily due to strong oncology research infrastructure, high adoption of advanced diagnostic technologies, and increasing prevalence of gastrointestinal cancers. Hospitals and diagnostic laboratories are increasingly integrating CEA testing into routine cancer management workflows. Continuous advancements in immunoassay technologies and strong healthcare spending are further driving market growth in the country.

Asia-Pacific Carcinoembryonic Antigen (CEA) Market Insight

The Asia-Pacific Carcinoembryonic Antigen (CEA) market is expected to witness rapid growth, driven by rising cancer burden, expanding diagnostic laboratory infrastructure, and increasing healthcare expenditure across countries such as China, India, and Japan. Growing awareness of early cancer detection, improving access to diagnostic testing, and increasing adoption of tumor marker-based screening programs are supporting regional expansion. In addition, rising investments in healthcare infrastructure are accelerating market growth.

Japan Carcinoembryonic Antigen (CEA) Market Insight

The Japan Carcinoembryonic Antigen (CEA) market is witnessing consistent growth due to increasing cancer screening rates, advanced diagnostic capabilities, and strong focus on early disease detection. High adoption of tumor marker testing in colorectal cancer monitoring and growing use of automated laboratory systems are supporting market development. In addition, Japan’s aging population is further contributing to increased demand for oncology diagnostics.

China Carcinoembryonic Antigen (CEA) Market Insight

The China Carcinoembryonic Antigen (CEA) market is growing rapidly, driven by increasing cancer incidence, expanding hospital and diagnostic laboratory infrastructure, and rising government focus on early disease screening programs. Growing adoption of tumor biomarker testing, improving access to healthcare services, and rapid expansion of oncology diagnostics capabilities are positioning China as one of the fastest-growing markets globally.

Carcinoembryonic Antigen (CEA) Market Share

The Carcinoembryonic Antigen (CEA) industry is primarily led by well-established companies, including:

- Roche Diagnostics (Switzerland)

- Abbott Laboratories (U.S.)

- Siemens Healthineers AG (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- bioMérieux SA (France)

- Becton, Dickinson and Company (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Merck KGaA (Germany)

- Beckman Coulter (U.S.)

- Qiagen N.V. (Netherlands)

- Bio-Rad Laboratories, Inc. (U.S.)

- Sysmex Corporation (Japan)

- Ortho Clinical Diagnostics (U.S.)

- Danaher Corporation (U.S.)

- PerkinElmer Inc. (U.S.)

- Fujirebio (Japan)

- Randox Laboratories Ltd (UK)

- DiaSorin S.p.A. (Italy)

- Tosoh Corporation (Japan)

- Shenzhen Mindray Bio-Medical Electronics (China)

- Abcam plc (UK)

- Agilent Technologies Inc. (U.S.)

- Illumina Inc. (U.S.)

- QuidelOrtho Corporation (U.S.)

- Epitope Diagnostics Inc. (U.S.)

Latest Developments in Carcinoembryonic Antigen (CEA) Market

- In March 2025, Abbott Laboratories announced the launch of a high-sensitivity Carcinoembryonic Antigen (CEA) immunoassay, designed to improve early detection and monitoring of colorectal and other cancers. The assay enhances analytical sensitivity and precision, enabling more accurate tracking of tumor recurrence and treatment response in oncology patients. This development reflects Abbott’s continued focus on expanding its immunoassay diagnostics portfolio and strengthening its position in cancer biomarker testing

- In May 2024, Roche Diagnostics expanded its Elecsys tumor marker portfolio, including CEA-related oncology testing solutions, to improve automated cancer monitoring across large hospital laboratories. The expansion focused on increasing throughput, standardization, and integration with Roche’s Cobas laboratory systems, supporting improved clinical decision-making in gastrointestinal and lung cancer management

- In September 2023, Siemens Healthineers enhanced its ADVIA Centaur immunoassay system menu, strengthening its tumor marker testing capabilities, including CEA-based oncology diagnostics. The update improved workflow efficiency and enabled higher throughput for cancer screening laboratories, particularly in colorectal cancer monitoring programs across Europe and North America

- In June 2022, Sysmex Corporation expanded its global oncology diagnostics collaboration with healthcare laboratories to strengthen automated immunoassay and tumor marker testing solutions, including CEA testing integration in high-volume clinical laboratories. The initiative focused on improving diagnostic accuracy and standardizing cancer biomarker testing workflows in routine clinical practice

- In November 2021, Thermo Fisher Scientific introduced enhancements to its oncology immunoassay and laboratory analytics platforms, supporting improved detection and quantification of tumor markers such as CEA. The development aimed to support cancer research laboratories and clinical diagnostics centers with more reliable biomarker analysis tools and improved reproducibility in cancer monitoring workflows

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.