Global Cardiac Ai Monitoring And Diagnostics Market

Market Size in USD Billion

USD

1.49 Billion

USD

7.70 Billion

2024

2032

USD

1.49 Billion

USD

7.70 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.49 Billion | |

| USD 7.70 Billion | |

| % | |

|

Cardiac AI Monitoring and Diagnostics Market Size

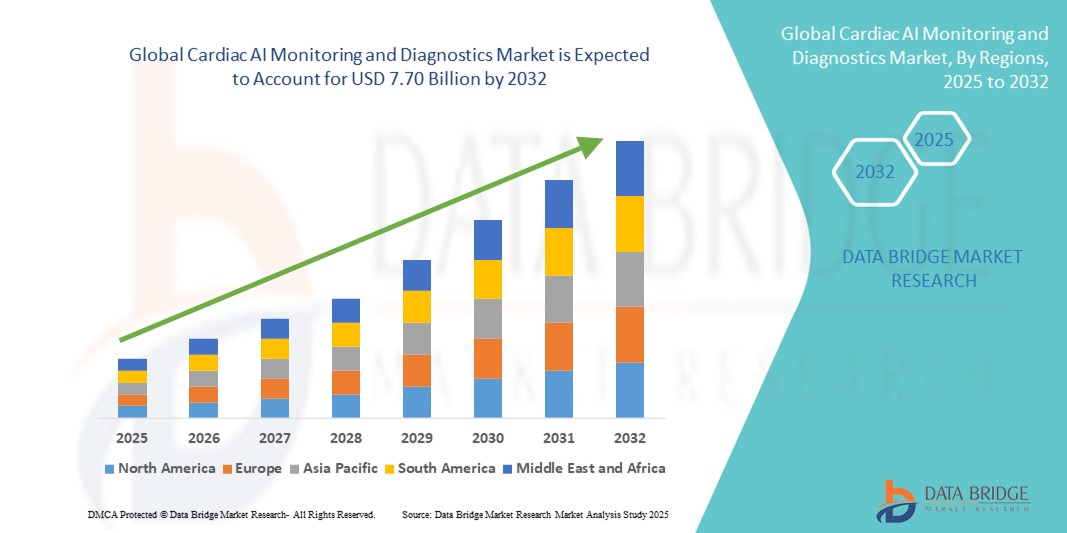

- The global cardiac AI monitoring and diagnostics market size was valued at USD 1.49 billion in 2024 and is expected to reach USD 7.70 billion by 2032, at a CAGR of 22.8% during the forecast period

- The market growth is largely fueled by the rising burden of cardiovascular diseases (CVDs) globally, which is prompting the integration of artificial intelligence (AI) in cardiac diagnostics to enable earlier detection and improve patient outcomes

- Furthermore, the growing adoption of AI-driven ECG interpretation, wearable cardiac monitors, and remote diagnostic platforms is revolutionizing cardiology workflows by enhancing diagnostic precision, minimizing manual errors, and reducing clinician workload

Cardiac AI Monitoring and Diagnostics Market Analysis

- Cardiac AI Monitoring and Diagnostics systems, leveraging artificial intelligence to interpret cardiovascular data, are becoming increasingly essential in both hospital and outpatient settings. These systems enhance diagnostic accuracy, enable early detection of heart conditions, and optimize treatment pathways through real-time analytics and predictive modeling

- The rising prevalence of cardiovascular diseases (CVDs), the demand for remote monitoring, and the integration of AI into wearable and clinical ECG platforms are major factors driving market growth

- North America dominated the cardiac AI monitoring and diagnostics market with the largest revenue share of 41.7% in 2024, attributed to the region's advanced healthcare infrastructure, early adoption of AI technologies in diagnostics, and strong presence of leading digital health companies

- Asia-Pacific is projected to be the fastest growing region in the cardiac AI monitoring and diagnostics market, with a CAGR of 25.6% from 2025 to 2032, fueled by growing urbanization, increasing awareness of heart health, and the proliferation of smart wearable technologies

- The ECG Monitor segment dominated the cardiac AI monitoring and diagnostics with a market revenue share of 31.5% in 2024, driven by the widespread adoption of AI-integrated ECG tools in both clinical and home-based settings. These monitors facilitate early diagnosis of arrhythmias and ischemic conditions, offering continuous and accurate cardiac data that enhances clinical decision-making

Report Scope and Cardiac AI Monitoring and Diagnostics Market Segmentation

|

Attributes |

Cardiac AI Monitoring and Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cardiac AI Monitoring and Diagnostics Market Trends

Rising Integration of Intelligent Automation in Cardiac Monitoring Solutions

- A significant and accelerating trend in the global cardiac AI monitoring and diagnostics market is the integration of intelligent automation tools, including machine learning algorithms and real-time data systems, into cardiac care platforms. This evolution is transforming traditional diagnostic workflows and enabling more proactive, personalized care

- For instance, leading companies have introduced AI-powered ECG interpretation systems that assist clinicians by flagging arrhythmias, ischemic changes, and other cardiac anomalies instantly, helping improve diagnostic accuracy and reduce clinician burden

- Advanced cardiac monitoring devices are now equipped with smart features such as predictive alerts for heart failure decompensation, real-time telemetry dashboards, and adaptive learning models that improve over time. Some systems can suggest optimized treatment pathways based on historical patient data and evolving symptoms

- The integration with cloud platforms and voice-activated medical record access (e.g., via Amazon Alexa or Google Assistant-enabled hospital systems) allows for hands-free documentation and real-time data retrieval, streamlining workflow efficiency for healthcare providers

- Furthermore, wearable cardiac monitoring solutions integrated with home automation tools enable patients to receive alerts, medication reminders, and emergency connectivity without requiring manual operation. Such innovations are especially valuable for elderly or high-risk patients living alone

- This trend toward intelligent, adaptive, and connected cardiac monitoring ecosystems is reshaping both inpatient and outpatient cardiology services. Key players like AliveCor, iRhythm Technologies, and Eko are pushing the boundaries by combining real-time biometrics with AI-enabled analytics to deliver faster and more actionable cardiac insights

- With the growing emphasis on remote care, chronic disease management, and real-time intervention, the demand for such intelligent and user-friendly cardiac AI monitoring and diagnostics solutions is expected to rise sharply across hospitals, ambulatory settings, and even home care environments

Cardiac AI Monitoring and Diagnostics Market Dynamics

Driver

Growing Demand Driven by Rising Cardiovascular Disease Burden and Remote Monitoring Adoption

- The rising global burden of cardiovascular diseases, including arrhythmias, heart failure, and coronary artery disease, coupled with the increasing focus on preventive healthcare, is a major factor driving the demand for cardiac AI monitoring and diagnostics solutions

- For instance, in April 2024, AliveCor, a leader in AI-based ECG technologies, launched an advanced algorithm capable of detecting multiple arrhythmias through mobile devices, helping reduce reliance on traditional clinical setups. Such strategic advancements are expected to accelerate market expansion

- As healthcare systems pivot towards value-based care, hospitals and providers are investing in AI-powered cardiac monitoring platforms that offer continuous data collection, real-time alerts, and predictive analytics—enabling early intervention and reducing hospital readmissions

- Furthermore, the growing adoption of telehealth and home-based diagnostics is making cardiac monitoring devices more user-friendly and connected. Patients can now benefit from wearable ECG patches, smartphone-enabled stethoscopes, and cloud-based monitoring dashboards that link directly with care teams

- The convenience of remote diagnostics, along with increased reimbursement support for AI-enabled cardiac tools in countries like the U.S., is encouraging both providers and patients to adopt these technologies at scale. In addition, self-installable and app-integrated cardiac monitoring systems are gaining popularity, especially in outpatient and post-surgical care settings

Restraint/Challenge

Concerns Regarding Data Privacy, Regulatory Compliance, and High Implementation Costs

- A significant challenge for the cardiac AI monitoring and diagnostics market is the concern surrounding patient data privacy and cybersecurity. Since these platforms collect sensitive health information and often operate via cloud infrastructure, they are susceptible to cyber threats and breaches

- High-profile data leak incidents and increasing regulatory scrutiny under frameworks like HIPAA (U.S.) and GDPR (Europe) have made healthcare providers cautious about adopting AI-driven diagnostic systems without robust encryption and compliance mechanisms

- Another restraint is the high initial cost associated with implementing advanced AI diagnostic platforms. Hospitals in developing regions may struggle with budget constraints, lacking the infrastructure to support cloud-based platforms, edge devices, or wearable integration

- While the cost of wearable cardiac monitors and AI software is gradually decreasing, many institutions still perceive these technologies as premium investments. Educating stakeholders on long-term cost savings from reduced hospitalizations and earlier diagnosis is crucial for improving adoption

- Overcoming these barriers will require collaborative efforts between med-tech companies, regulators, and payers. Enhanced cybersecurity protocols, data governance frameworks, and affordable pricing models (including pay-per-use AI services) will be critical to scaling adoption and trust in the market

Cardiac AI Monitoring and Diagnostics Market Scope

The market is segmented on the basis of device type and end-user.

- By Device Type

On the basis of device type, the cardiac AI monitoring and diagnostics market is segmented into ECG monitor, event recorder, implantable cardiac loop recorder, pacemaker, defibrillator, cardiac resynchronization therapy (CRT) devices, smart wearable, and others. The ECG monitor segment dominated the largest market revenue share of 31.5% in 2024, driven by the widespread adoption of AI-integrated ECG tools in both clinical and home-based settings. These monitors facilitate early diagnosis of arrhythmias and ischemic conditions, offering continuous and accurate cardiac data that enhances clinical decision-making.

The Smart Wearable segment is anticipated to witness the fastest CAGR of 22.8% from 2025 to 2032, owing to the increasing consumer demand for real-time heart health monitoring, coupled with growing integration of AI in wearable health technologies. Innovations from companies like Apple and Fitbit are contributing to this trend, making cardiac monitoring more accessible and preventive in nature.

- By End-User

On the basis of end-user, the cardiac AI monitoring and diagnostics is segmented into hospitals and clinics, home care settings, and others. The hospitals and clinics segment accounted for the largest market share of 44.6% in 2024, due to high patient inflow, availability of advanced diagnostic infrastructure, and the need for rapid, AI-enabled clinical decision support tools to manage cardiac conditions.

The home care settings segment is projected to register the fastest growth rate of 20.3% from 2025 to 2032, driven by the rising demand for remote monitoring solutions, aging population, and cost-saving healthcare delivery models. AI-powered portable and wearable cardiac devices are making at-home diagnostics more reliable and increasingly favored by patients and providers alike.

Cardiac AI Monitoring and Diagnostics Market Regional Analysis

- North America dominated the cardiac AI monitoring and diagnostics market with the largest revenue share of 41.7% in 2024, driven by the rapid adoption of artificial intelligence in clinical workflows, growing incidence of cardiovascular diseases (CVDs), and strong presence of leading digital health innovators

- Consumers and healthcare providers in the region value AI-integrated solutions that offer early detection, personalized risk assessments, and real-time cardiac monitoring, enabling timely interventions and improved patient outcomes

- Furthermore, the market is supported by favorable reimbursement structures, robust healthcare IT infrastructure, and regulatory initiatives that encourage the adoption of AI in clinical diagnostics

U.S. Cardiac AI Monitoring and Diagnostics Market Insight

The U.S. cardiac AI monitoring and diagnostics market captured the largest revenue share of 77% in 2024 within North America, driven by the increasing demand for remote patient monitoring (RPM), precision diagnostics, and value-based care delivery. The presence of a mature digital health ecosystem, high healthcare expenditure, and strong investments in AI-enabled medical devices has significantly boosted market adoption. The rise in wearable ECG patches, AI-based arrhythmia detection tools, and mobile-enabled diagnostic apps is reshaping cardiac care in both clinical and at-home settings.

Europe Cardiac AI Monitoring and Diagnostics Market Insight

The Europe cardiac AI monitoring and diagnostics market is projected to expand at a strong CAGR during the forecast period, owing to the region’s commitment to healthcare innovation, data-driven care models, and rising awareness of cardiovascular health. Stringent healthcare standards, cross-border AI policy alignment (like the EU AI Act), and initiatives promoting telecardiology are fostering adoption. Countries such as Germany, France, and the U.K. are leading in deploying AI-powered cardiac tools across hospitals and research institutes, particularly for risk stratification and post-operative cardiac monitoring.

U.K. Cardiac AI Monitoring and Diagnostics Market Insight

The U.K. cardiac AI monitoring and diagnostics market is expected to grow notably, backed by NHS-driven digitization efforts, AI-specific funding, and increased CVD awareness. Key initiatives like the NHS AI Lab and the push for early detection of heart disease are supporting AI integration into diagnostic workflows. Additionally, rising use of AI-assisted echocardiograms, cloud-based ECG monitoring, and real-time analytics platforms is transforming cardiology departments across the U.K.

Germany Cardiac AI Monitoring and Diagnostics Market Insight

The Germany cardiac AI monitoring and diagnostics market is set for significant growth, propelled by advancements in AI-powered imaging analysis, electronic health records (EHRs), and strong government support for digital transformation in healthcare. Germany’s commitment to data privacy and secure interoperability has spurred innovations in AI-based cardiac diagnostics, particularly in academic medical centers and specialized cardiology clinics.

Asia-Pacific Cardiac AI Monitoring and Diagnostics Market Insight

The Asia-Pacific cardiac AI monitoring and diagnostics market is projected to grow at the fastest CAGR of 25.6% from 2025 to 2032, driven by rising CVD prevalence, increasing mobile health (mHealth) adoption, and supportive government investments in digital health. Emerging economies like China and India are witnessing rapid integration of AI into primary care and cardiology practices due to affordability, smartphone penetration, and growing telemedicine platforms. Countries such as Japan and South Korea are leveraging advanced infrastructure for real-time diagnostics and AI-based cardiac imaging analysis.

Japan Cardiac AI Monitoring and Diagnostics Market Insight

The Japan cardiac AI monitoring and diagnostics market is expanding steadily due to its aging population, high CVD incidence, and strong governmental push for AI-driven medical innovation. Hospitals are increasingly adopting AI-assisted tools for arrhythmia detection, smart stethoscopes, and predictive analytics for heart failure management. Moreover, Japan's high digital literacy and preference for non-invasive technologies support strong market growth.

China Cardiac AI Monitoring and Diagnostics Market Insight

The China cardiac AI monitoring and diagnostics market accounted for the largest revenue share in the Asia-Pacific region in 2024, supported by massive investments in AI, smart healthcare infrastructure, and growing burden of heart diseases. China’s focus on smart hospitals, integration of AI in electronic medical records, and partnerships between tech giants and medical institutions have accelerated product development and deployment. Additionally, government-backed initiatives for AI in healthcare are helping scale cardiac diagnostics to rural and underserved populations.

Cardiac AI Monitoring and Diagnostics Market Share

The cardiac AI monitoring and diagnostics industry is primarily led by well-established companies, including:

- Koninklijke Philips N.V. (Netherlands)

- HeartVista Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- RSIP Vision (Israel)

- Ultromics Limited (U.S.)

- Tempus Labs Inc. (U.S.)

- Cardiologs Technologies (U.S.)

- Cleerly, Inc. (U.S.)

- AliveCor, Inc. (U.S.)

- Aidoc Medical Ltd. (Israel)

- Boston Scientific Corporation (U.S.)

Latest Developments in Global Cardiac AI Monitoring and Diagnostics Market

- In August 2023, Koninklijke Philips N.V. integrates Al in cardiac ultrasound and across cardiac care at ESC 2023. Philips is a global leader in health technology, it integrates Al in cardiac ultrasound across cardiac care to help improve clinical confidence and increase efficiency

- In March 2023, Aidoc, the prominent provider of healthcare Al solutions, made a significant breakthrough with the introduction of their groundbreaking cardiovascular Al solutions package

- In July 2025, Philips launched its ECG AI Marketplace, a centralized platform allowing clinicians to integrate FDA-cleared AI tools like Anumana’s Low Ejection Fraction (LEF) algorithm directly into Philips ECG systems. This initiative is designed to streamline clinical workflows and accelerate early detection of heart failure

- In July 2025, a groundbreaking AI screening tool called EchoNext, developed by Columbia University and NewYork-Presbyterian, demonstrated 77% accuracy in detecting structural heart disease from ECGs, outperforming cardiologists (64%) and flagging thousands of previously undetected high-risk patients

- In July 2025, Eko Health’s SENSORA AI-enabled cardiac analysis solution received a Category III CPT code from the AMA, with CMS approving a reimbursement rate of USD 128.90 per use—marking a pivotal step toward broader clinical adoption of AI-based diagnostics in outpatient settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.