Global Cardiometabolic Diseases Market

Market Size in USD Billion

USD

192.90 Billion

USD

305.14 Billion

2024

2032

USD

192.90 Billion

USD

305.14 Billion

2024

2032

| 2025 - 2032 | |

| USD 192.90 Billion | |

| USD 305.14 Billion | |

| % | |

|

Cardiometabolic Diseases Market Size

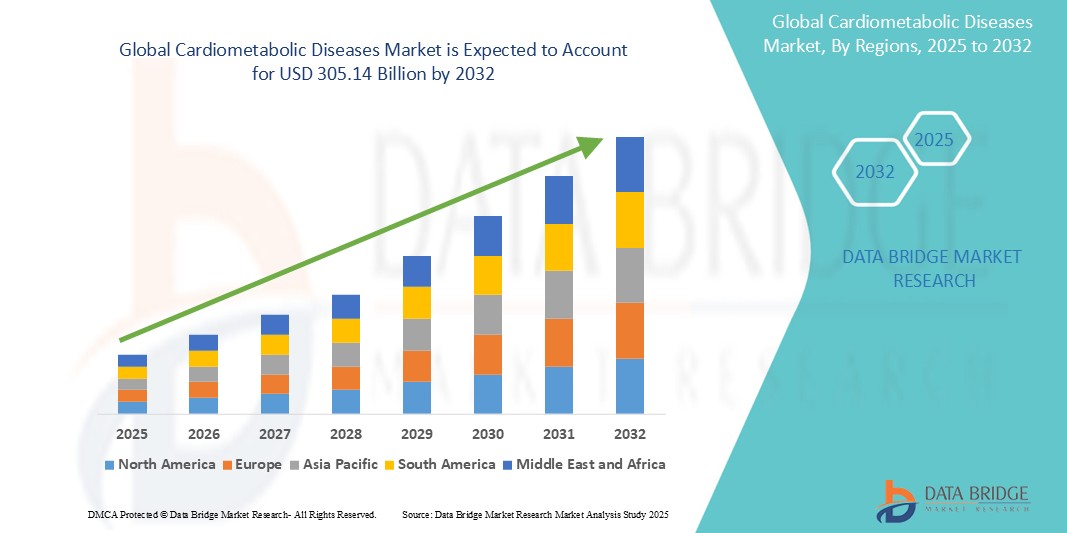

- The global cardiometabolic diseases market size was valued at USD 192.9 billion in 2024 and is expected to reach USD 305.14 billion by 2032, at a CAGR of 5.90% during the forecast period

- The market growth is primarily driven by the rising prevalence of cardiometabolic conditions such as diabetes, hypertension, dyslipidemia, and obesity, which often occur in comorbidity. The growing burden of sedentary lifestyles, poor dietary habits, and genetic predispositions are also significant contributors

- In addition, increasing awareness of early risk detection and preventive care, alongside the introduction of advanced therapeutics such as GLP-1 receptor agonists and SGLT2 inhibitors, is expected to further boost market expansion

Cardiometabolic Diseases Market Analysis

- Cardiometabolic-disease therapy addresses the four modifiable risk pillars — hyper-glycaemia, dyslipidaemia, hypertension and obesity — through drugs such as GLP-1/GIP receptor agonists, SGLT-2 inhibitors, statins/PCSK9 inhibitors and renin–angiotensin–aldosterone–system (RAAS) blockers. By normalising these parameters, the regimens cut major adverse cardiovascular events (MACE) and all-cause mortality, making them the cornerstone of long-term chronic-disease management for diabetes, heart failure and atherosclerotic CVD

- Escalating demand is fuelled by the twin pandemics of type-2 diabetes and obesity, population ageing, and the emergence of multi-benefit drugs (for instance, semaglutide, tirzepatide and coming triple-agonists) that tackle weight, glucose and cardiovascular risk in one shot

- North America dominates the cardiometabolic diseases market with a market share of 46% due to the early adoption of GLP-1s/PCSK9s, robust payer coverage and a deep clinical-trial pipeline led by U.S.-based majors

- Asia–Pacific is expected to be the fastest growing region in the cardiometabolic diseases market, due to large scale diabetes-hypertension screening, upgrade reimbursement and rapid urban-lifestyle shift

- ACE-inhibitor segment dominates the cardiometabolic diseases market with market share of 43.5% in 2024, reflecting its entrenched first-line status for blood-pressure and reno-cardio protection

Report Scope and Cardiometabolic Diseases Market Segmentation

|

Attributes |

Cardiometabolic Diseases Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cardiometabolic Diseases Market Trends

“Increasing Focus on Integrated, Multi-Target Cardiometabolic Therapies”

- A significant and accelerating trend in the global cardiometabolic diseases market is the shift toward integrated therapeutic approaches that address multiple conditions such as diabetes, hypertension, dyslipidemia, and obesity simultaneously, improving overall cardiovascular outcomes and quality of life

- For instance, dual and triple agonist therapies (for instance, GLP-1/GIP/Glucagon receptor agonists) are being developed to manage both glucose levels and weight, while also reducing cardiovascular risk, offering a comprehensive treatment solution for complex patients

- Technological innovations such as oral formulations of previously injectable drugs, extended-release profiles, and targeted biologics are enhancing treatment efficacy and patient adherence, particularly in chronic disease management

- The integration of digital health platforms, including connected glucose monitors, wearables, and AI-driven decision support tools, is facilitating personalized treatment adjustments and proactive disease management across care settings

- This convergence of pharmacological innovation and digital health is transforming cardiometabolic care into a patient-centered, value-driven model, prompting pharmaceutical companies to invest heavily in R&D pipelines focused on combination and long-acting therapies

- As healthcare systems globally move toward preventive and holistic management of chronic diseases, cardiometabolic therapies that offer multi-faceted benefits are experiencing strong adoption and are expected to be a major growth driver in the coming years

Cardiometabolic Diseases Market Dynamics

Driver

“Rising global burden of chronic lifestyle diseases and associated comorbidities”

- The increasing global incidence of chronic lifestyle-related conditions such as type 2 diabetes, obesity, hypertension, and dyslipidemia, along with their frequent coexistence, is a key driver for the cardiometabolic diseases market

- For instance, more than 1 billion adults worldwide are overweight, with a significant portion developing insulin resistance, cardiovascular complications, and metabolic syndrome, creating continuous demand for integrated treatment regimens

- Cardiometabolic therapies—especially GLP-1 receptor agonists, SGLT-2 inhibitors, ACE inhibitors, and statins—are central to managing these interlinked conditions, helping reduce the risk of major adverse cardiovascular events (MACE) and improve long-term health outcomes

- As sedentary lifestyles, unhealthy diets, and urban stress contribute to rising disease prevalence across age groups, particularly in urbanized and emerging markets, there is a growing need for long-term, multi-benefit therapeutic options

- Furthermore, the increasing awareness of early screening and preventive care, along with government initiatives and reimbursement support in both developed and developing nations, is accelerating diagnosis and treatment uptake

- The convergence of clinical urgency, economic burden, and therapeutic innovation is driving pharmaceutical companies and healthcare systems to prioritize cardiometabolic disease management, positioning it as a critical growth sector in global healthcare

Restraint/Challenge

“High Cost of Advanced Therapies and Limited Affordability in Low- And Middle-Income Countries”

- One of the key challenges facing the cardiometabolic diseases market is the high cost associated with innovative treatments, such as GLP-1 receptor agonists, SGLT-2 inhibitors, PCSK9 inhibitors, and combination biologics, which can limit accessibility, especially in cost-sensitive regions

- For instance, novel drugs such as semaglutide and tirzepatide, while clinically effective, are priced significantly higher than traditional medications, creating affordability barriers for patients and healthcare systems in low- and middle-income countries (LMICs)

- In many emerging economies, limited reimbursement coverage, out-of-pocket payment models, and inadequate insurance penetration further restrict patient access to these life-saving therapies

- In addition, the high cost of long-term disease management, including regular diagnostics, follow-up consultations, and monitoring tools (for instance, CGMs, lipid panels), adds to the financial burden on both patients and healthcare providers

- These economic constraints may lead to delayed diagnosis, poor treatment adherence, and under-treatment, especially among rural and underserved populations, hampering overall market penetration

- Addressing this restraint will require policy reforms, generic competition, tiered pricing models, and increased collaboration between public and private stakeholders to improve affordability and access to essential cardiometabolic treatments worldwide

Cardiometabolic Diseases Market Scope

The market is segmented on the basis of type, treatment, dosage, route of administration, distribution channel, and end user.

By Type

On the basis of type, the cardiometabolic diseases market is segmented into chronic/ congestive heart failure, hypertension, type 2 diabetes, and obesity. The type 2 diabetes segment dominated the market with an revenue share of 37% in 2024, driven by the high global prevalence of diabetes, increasing sedentary lifestyles, and rising adoption of antidiabetic therapies.

The Hypertension segment is anticipated to witness the fastest growth rate of 29% from 2025 to 2032, supported by growing awareness, improved diagnosis, and long-term therapy needs.

• By Treatment

On the basis of treatment, the cardiometabolic diseases Market is segmented into ACE Inhibitors, Diuretics, Glucophage, Liposuction, and Others. The ACE Inhibitors segment held the largest market revenue share of 43.5% in 2024, attributed to their proven efficacy in managing hypertension and heart failure, both critical components of cardiometabolic disorders. ACE inhibitors are widely prescribed due to their role in preventing cardiovascular complications by relaxing blood vessels and reducing blood pressure. Their longstanding clinical acceptance and inclusion in standard treatment guidelines continue to drive their market dominance.

The glucophage segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the rising global prevalence of type 2 diabetes and its central role in cardiometabolic syndrome. As a first-line oral antihyperglycemic agent, Glucophage (metformin) offers effective blood glucose control with a favorable safety profile. Its growing use in prediabetes, polycystic ovary syndrome (PCOS), and adjunct therapies enhances its market expansion across diverse patient populations

• By Dosage

On the basis of dosage form, the market is segmented into Tablet, Injection, and Others. The Tablet segment held the largest market share in 2024, driven by patient convenience, ease of storage and administration, and cost-effectiveness. Tablets are the preferred form for chronic management of cardiometabolic conditions, especially for daily maintenance medications such as antihypertensives and antidiabetics.

The injection segment is expected to witness the fastest CAGR from 2025 to 2032 due to the increasing adoption of injectable therapies such as GLP-1 receptor agonists and insulin analogs for more effective glycemic control. Advances in delivery technologies and patient-centric designs such as pre-filled pens are further accelerating the demand for injectable options.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Intravenous, and Others. The Oral route dominated the market in 2024 due to its non-invasive nature and high patient adherence. Oral medications are typically the first choice in managing long-term cardiometabolic conditions, contributing to their widespread use.

The intravenous route is expected to witness the fastest CAGR from 2025 to 2032 particularly for acute interventions in hospital settings, such as for severe hypertensive crises or cardiovascular complications requiring immediate drug action.

• By End User

Based on end user, the cardiometabolic diseases market is segmented into hospitals, clinics, and others. The hospitals segment held the largest market revenue share in 2024, owing to the high volume of inpatient cardiovascular and metabolic care services.

The clinics segment is expected to witness the fastest CAGR from 2025 to 2032 due to the increasing trend of outpatient management and early diagnosis initiatives in primary care and specialty clinics.

•By Distribution Channel

On the basis of distribution channel, the cardiometabolic diseases market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. Retail Pharmacies held the largest share of 44.8% in 2024, supported by widespread drug availability and convenience for chronic refills.

The online pharmacies segment is expected to witness the fastest CAGR from 2025 to 2032 propelled by rising digital adoption, home delivery convenience, and growing consumer trust in e-commerce platforms for chronic disease medication management

Cardiometabolic Diseases Market Regional Analysis

- North America dominates the global cardiometabolic diseases market with the largest revenue share of 46% in 2024, driven by stringent regulatory frameworks, high healthcare expenditure, and a strong presence of leading pharmaceutical and medical device companies

- The region’s well‑established healthcare infrastructure, emphasis on quality care, and early adoption of advanced cardiometabolic disease management technologies contribute to its market leadership

- The market’s growth is further fueled by technological advancements, such as remote monitoring tools, wearables for continuous glucose tracking, and AI-powered health management apps, which help individuals with cardiometabolic risk manage their conditions more effectively

U.S. Cardiometabolic Diseases Market Insight

The U.S. cardiometabolic diseases market captured 76.2% of North America’s revenue in 2024. This dominance is fueled by a high prevalence of obesity, diabetes, and cardiovascular disorders, rising geriatric population, and increasing adoption of precision medicine. A strong network of healthcare providers, significant investment in clinical research, and FDA-approved therapies accelerate market growth. The push for value-based care and digital health integration further propels innovation and market expansion.

Europe Cardiometabolic Diseases Market Insight

The Europe cardiometabolic diseases market held 28% of the global market share in 2024, ranking as the second-largest regional market. Market growth is driven by robust public healthcare systems, rising incidence of lifestyle-related disorders, and broad access to advanced diagnostics and therapeutics. The European Medicines Agency (EMA)’s strict regulatory standards ensure treatment efficacy and safety, supporting wider adoption of innovative cardiometabolic interventions.

U.K. Cardiometabolic Diseases Market Insight

The U.K. cardiometabolic diseases market is poised for steady growth, supported by increased investments in preventive healthcare and chronic disease management. Government-backed health campaigns targeting obesity, diabetes, and heart health are improving early diagnosis and treatment. Growth is also reinforced by the National Health Service (NHS)’s emphasis on clinical excellence and technology integration in patient care pathways.

Germany Cardiometabolic Diseases Market Insight

The Germany cardiometabolic diseases market contributes significantly to the European market, with strong demand for advanced therapeutics, a flourishing pharmaceutical industry, and high awareness around cardiometabolic risk factors. A well-regulated healthcare system and investments in digital health and AI-based diagnostic tools enhance the early detection and personalized treatment of cardiometabolic conditions. Germany’s leadership in medical innovation strengthens its regional foothold.

Asia-Pacific Cardiometabolic Diseases Market Insight

The Asia-Pacific cardiometabolic diseases market is projected to witness the fastest CAGR of 21.21% from 2025 to 2032 driven by surging healthcare demand, rising prevalence of diabetes and cardiovascular diseases, and improved access to quality care in emerging economies. The region accounted for about 18% of the global market share in 2024, expected to increase due to rapid urbanization, higher health awareness, and expanding insurance coverage. Governments in countries such as China, India, and Japan are investing heavily in healthcare infrastructure and local pharmaceutical production, stimulating market growth.

Japan Cardiometabolic Diseases Market Insight

Japan cardiometabolic diseases market is expanding steadily, supported by a rapidly aging population and government efforts to manage rising chronic disease burdens. High public health awareness, universal healthcare access, and technological advancements in drug delivery and diagnostics drive adoption of novel treatments. Japan accounts for a notable portion of the regional market, particularly in diabetes and heart failure management.

China Cardiometabolic Diseases Market Insight

China cardiometabolic diseases market represents one of the most dynamic growth opportunities, capturing a rising share of the Asia-Pacific market. The expansion is fueled by increasing urban lifestyle-related diseases, robust government healthcare reforms, and growing demand for affordable yet advanced treatments. China’s emergence as a biopharma innovation hub, coupled with its high patient volume and improving healthcare access, makes it a focal point for both local and multinational players.

Cardiometabolic Diseases Market Share

The cardiometabolic diseases industry is primarily led by well-established companies, including:

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Arrowhead Pharmaceuticals, Inc. (U.S.)

- Cardax, Inc. (U.S.)

- Novartis AG (Switzerland)

- Boehringer Ingelheim International GmbH (Germany)

- Kowa Company, Ltd. (Japan)

- AstraZeneca (U.K.)

- Takeda Pharmaceutical Company Limited (Japan

- Sarepta Therapeutics, Inc. (U.S.)

- Rocket Pharmaceuticals, Inc. (U.S.)

- AskBio Inc. (U.S.)

- BridgeBio Pharma, Inc. (U.S.)

- Neurocrine Biosciences, Inc. (U.S.)

- PTC Therapeutics, Inc. (U.S.)

- Chiesi Farmaceutici S.p.A. (Italy)

- Astellas Pharma Inc. (U.S.)

- Ionis Pharmaceuticals, Inc. (U.S.)

- Amicus Therapeutics, Inc. (U.S.)

Latest Developments in Global Cardiometabolic Diseases Market

- In January 2024, Novo Nordisk entered into strategic collaborations with Omega Therapeutics and Cellarity to develop innovative therapies targeting cardiometabolic disorders. These partnerships aim to leverage cutting-edge technologies to accelerate the discovery of transformative treatments

- In January 2024, Eli Lilly and Company launched LillyDirect, a digital healthcare platform designed to streamline access to care for U.S. patients managing obesity, migraine, and diabetes. This initiative enhances patient support through online services and personalized treatment pathways

- In June 2023, the U.S. FDA approved VASCEPA capsules, the first prescription therapy comprised entirely of icosapent ethyl, a purified form of eicosapentaenoic acid. The approval represents a milestone in lipid management and cardiovascular risk reduction

- In October 2022, Eli Lilly and Company and Boehringer Ingelheim launched CRMSynced, an initiative aimed at encouraging healthcare professionals to adopt an integrated approach to managing cardio-renal-metabolic (C-R-M) conditions, recognizing the interconnection and shared disease pathways among the cardiovascular, renal, and metabolic systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.