Global Cardiomyopathy Market

Market Size in USD Million

USD

512.95 Million

USD

684.38 Million

2024

2032

USD

512.95 Million

USD

684.38 Million

2024

2032

| 2025 - 2032 | |

| USD 512.95 Million | |

| USD 684.38 Million | |

| % | |

|

Cardiomyopathy Market Size

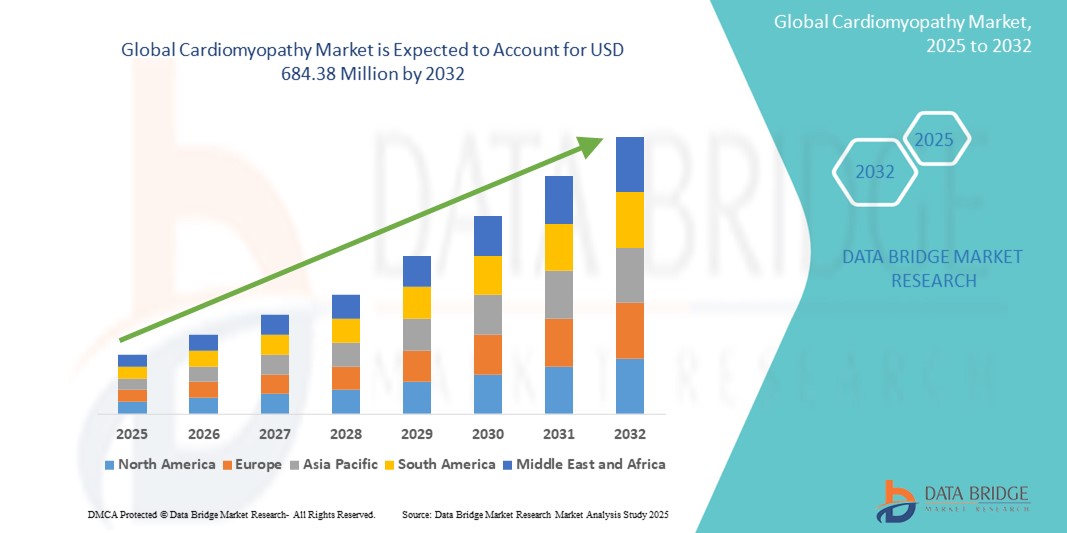

- The Global Cardiomyopathy Market size was valued at USD 512.95 Million in 2024 and is expected to reach USD 684.38 Million by 2032, at a CAGR of 3.67% during the forecast period

- Market growth is primarily driven by the rising prevalence of cardiovascular diseases, increasing awareness about early diagnosis, and advancements in imaging technologies such as echocardiograms, MRIs, and CT scans

- Additionally, the demand for innovative treatment options, including implantable devices, cardioverter-defibrillators, and targeted medication, is contributing to the expansion of the market. The increased focus on specialized care in clinics and hospitals, along with better access to healthcare infrastructure and online pharmacy channels, is further fueling market growth by making diagnosis and treatment more accessible and efficient

Cardiomyopathy Market Analysis

- Cardiomyopathy, a group of disorders impairing the heart muscle's ability to pump blood efficiently, is becoming an increasingly important focus in global cardiac care due to its rising prevalence, impact on quality of life, and potential for heart failure if untreated. Key diagnostic tools such as echocardiograms, MRIs, CT scans, and blood tests are central to early detection and disease management in both hospital and outpatient settings.

- The escalating demand for cardiomyopathy treatment is primarily fueled by the growing geriatric population, increasing incidence of hypertension, diabetes, and genetic conditions, and rising awareness about cardiovascular health and routine screening practices.

- North America dominates the cardiomyopathy market with the largest revenue share of 41.8% in 2025, attributed to advanced healthcare infrastructure, high diagnosis and treatment rates, and the strong presence of medical device manufacturers and research institutions. The U.S., in particular, is experiencing steady growth in the adoption of implantable cardioverter-defibrillators (ICDs) and ventricular assist devices (VADs) supported by favorable reimbursement policies and clinical innovations.

- Asia-Pacific is expected to be the fastest-growing region in the cardiomyopathy market during the forecast period, driven by urbanization, increasing healthcare investments, and a rising prevalence of heart-related conditions, especially in India, China, and Southeast Asia.

- The dilated cardiomyopathy segment is expected to dominate the cardiomyopathy market with a market share of 46.3% in 2025, owing to its high global prevalence, progressive nature requiring long-term treatment, and increasing uptake of oral medications and device implants for disease management.

Report Scope and Cardiomyopathy Market Segmentation

|

Attributes |

Cardiomyopathy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Cardiomyopathy Market Trends

“Rising Focus on Precision Medicine and Genetic Profiling”

- A significant and accelerating trend in the global cardiomyopathy market is the increasing adoption of precision medicine approaches, particularly driven by genetic profiling and advancements in molecular diagnostics. These innovations are enabling more personalized treatment strategies for subtypes of cardiomyopathy, such as hypertrophic and dilated forms, which often have hereditary components.

- For instance, companies like MyoKardia (now part of Bristol Myers Squibb) are developing targeted therapies like mavacamten, which specifically addresses the underlying cause of hypertrophic cardiomyopathy at the molecular level. This signals a shift away from symptomatic treatment toward disease-modifying interventions.

- Genetic testing tools are being increasingly used to identify at-risk family members, especially in hypertrophic cardiomyopathy, facilitating early diagnosis and preventive care. With rising affordability and awareness of such testing, healthcare systems in North America and parts of Europe are incorporating genetic screening into cardiomyopathy diagnostic protocols.

- Furthermore, wearable cardiac monitoring devices and AI-enabled diagnostic platforms are being integrated into routine cardiology care. These technologies support continuous heart monitoring, real-time alerts, and data-driven clinical decisions, enhancing disease management and patient compliance.

- This trend towards personalized, proactive, and tech-driven cardiomyopathy care is reshaping treatment pathways and opening avenues for novel therapeutics, digital health platforms, and remote cardiac care, especially for chronic management in outpatient settings.

Cardiomyopathy Market Dynamics

Driver

“Growing Prevalence of Cardiovascular Diseases and Increased Diagnostic Awareness”

- The rising global burden of cardiovascular conditions, especially among aging populations, is a primary driver of growth in the cardiomyopathy market. Increasing exposure to risk factors such as hypertension, diabetes, obesity, and sedentary lifestyles is contributing to higher incidence rates of both dilated and hypertrophic cardiomyopathy.

- For instance, global estimates suggest that dilated cardiomyopathy affects over 1 in 2,500 people, with a large percentage remaining undiagnosed until advanced stages. The growing awareness of heart failure symptoms and routine cardiac assessments is improving early detection rates, leading to timely intervention and better outcomes.

- Governments and healthcare organizations are launching awareness campaigns and screening initiatives. In countries like the U.S., U.K., and Japan, cardiomyopathy is increasingly being addressed as a public health concern, with policies promoting the use of non-invasive imaging tools and genetic counseling services.

- Moreover, the expanding availability of oral medications, device-based interventions (like ICDs and heart pumps), and outpatient cardiac rehabilitation programs is improving treatment access, especially in urban centers of developing economies. These factors are collectively driving market demand across both the medication and device segments.

Restraint/Challenge

“Delayed Diagnosis and Limited Treatment Access in Low-Income Regions”

- One of the most pressing challenges in the global cardiomyopathy market is the delayed diagnosis due to non-specific symptoms and lack of routine screening in many regions. Cardiomyopathy often remains undiagnosed until advanced stages, limiting treatment efficacy and increasing the risk of sudden cardiac death or heart failure.

- In low- and middle-income countries, access to echocardiograms, MRIs, or genetic testing remains limited due to cost constraints and insufficient infrastructure. The shortage of trained cardiologists and lack of awareness among primary care providers further contributes to underreporting and mismanagement of the disease.

- Additionally, advanced treatment options such as implantable cardioverter-defibrillators (ICDs), heart transplants, or targeted therapies are often unaffordable or unavailable in many healthcare systems, particularly in rural or underserved areas.

- Another constraint is the lack of standardized treatment guidelines across regions, leading to inconsistent care protocols and variable patient outcomes. Regulatory delays and high R&D costs for novel cardiomyopathy drugs also pose barriers for market entry and innovation.

- Addressing these challenges will require multi-stakeholder collaboration involving governments, healthcare providers, and private players to improve diagnostic outreach, subsidize high-cost treatments, and build local manufacturing and distribution channels for greater global access.

Cardiomyopathy Market Scope

The market is segmented on the basis of type, diagnosis, treatment, route of administration, end-user, and distribution channel.

• By Type

On the basis of type, the cardiomyopathy market is segmented into hypertrophic, dilated, and restrictive cardiomyopathy. The dilated cardiomyopathy segment is expected to dominate the global market with the largest revenue share of 46.3% in 2025, due to its high global prevalence, particularly among aging populations and patients with a history of cardiovascular risk factors such as hypertension and diabetes. It typically requires long-term pharmacological treatment and often progresses to heart failure, driving demand for consistent medical management and device-based interventions.

The hypertrophic cardiomyopathy segment is anticipated to witness the fastest CAGR of 4.9% from 2025 to 2032, supported by rising awareness, improved genetic screening, and the emergence of targeted therapies like mavacamten, which address the root cause at a molecular level. Growing recognition of familial inheritance patterns and routine screening of asymptomatic family members are also fueling early detection and intervention.

• By Diagnosis

On the basis of diagnosis, the market is segmented into X-ray, echocardiogram, electrocardiogram (ECG), MRI, CT scan, blood tests, and others. Echocardiogram held the largest market revenue share in 2025, owing to its non-invasive nature, cost-effectiveness, and reliability in assessing ventricular function, chamber size, and wall thickness — critical in diagnosing all three types of cardiomyopathy.

Cardiac MRI is projected to witness the fastest growth rate from 2025 to 2032, due to its high-resolution imaging capabilities that enable accurate tissue characterization, detection of fibrosis, and assessment of myocardial viability. Technological advances and the increasing use of MRI in comprehensive cardiomyopathy workups are expanding its adoption across developed and emerging markets.

• By Treatment

On the basis of treatment, the market is segmented into medication, implantable devices, heart pumps, cardioverter-defibrillators, and others. The medication segment held the largest market share in 2025, driven by the widespread use of beta-blockers, ACE inhibitors, ARBs, and diuretics for symptom management and slowing disease progression, particularly in dilated cardiomyopathy.

The implantable devices segment is expected to grow at the fastest CAGR from 2025 to 2032, fueled by rising adoption of ICDs and CRT devices for arrhythmia prevention and heart failure management. Increasing availability of reimbursement, technological improvements, and physician preference for early device implantation in high-risk patients are contributing to segment growth.

• By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The oral segment dominates with the highest market share in 2025 due to the chronic nature of cardiomyopathy and the widespread availability of oral drug formulations, which offer ease of administration, high patient compliance, and cost-effectiveness.

The parenteral route is expected to witness the fastest CAGR, supported by the need for acute care interventions and hospital-administered treatments, particularly during heart failure decompensation or in emergency settings.

• By End-User

On the basis of end-user, the market is segmented into clinics, hospitals, and others. The hospital segment accounted for the largest revenue share in 2025, owing to the presence of specialized cardiac units, higher volumes of advanced diagnostic imaging, and immediate access to surgical and device-based treatments.

The clinic segment is projected to grow at the fastest rate from 2025 to 2032, due to the rising role of outpatient cardiology services, follow-up monitoring, and community-based heart failure management programs, particularly in developed countries and urban centers of emerging economies.

• By Distribution Channel

On the basis of distribution channel, the cardiomyopathy market is segmented into direct tenders, retail sales, hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the market in 2025 due to the centralized dispensing of prescribed medications, particularly during inpatient care and after cardiac interventions.

The online pharmacy segment is expected to exhibit the fastest CAGR from 2025 to 2032, supported by rising digital adoption, convenience of home delivery, competitive pricing, and increasing usage of chronic disease medication auto-refill programs in both developed and developing regions.

Cardiomyopathy Market Regional Analysis

- North America dominates the cardiomyopathy market with the largest revenue share of 41.8% in 2024, driven by a high prevalence of cardiovascular diseases, advanced healthcare infrastructure, and strong adoption of diagnostic technologies such as echocardiography, cardiac MRI, and genetic testing

- Consumers in the region benefit from widespread access to specialized cardiology services, early screening programs, and innovative treatment options including implantable cardioverter-defibrillators (ICDs) and targeted medications for heart failure and hypertrophic cardiomyopathy

- This dominance is further supported by favorable reimbursement policies, high healthcare spending, and growing awareness about hereditary and lifestyle-related cardiac conditions. The increasing availability of outpatient cardiac care, along with clinical research in precision medicine and gene therapy, continues to enhance the region’s market leadership across both medication and device segments

U.S. Cardiomyopathy Market Insight

The U.S. cardiomyopathy market captured the largest revenue share of 79% within North America in 2025, driven by the country’s advanced cardiac care infrastructure and high awareness of cardiovascular diseases. Early adoption of genetic testing, echocardiography, and implantable cardiac devices supports timely diagnosis and intervention. Furthermore, the presence of key pharmaceutical and med-tech companies, along with robust research into targeted therapies and regenerative treatments, continues to expand treatment options. The growing emphasis on remote monitoring and outpatient care models is also supporting the market’s long-term growth.

Europe Cardiomyopathy Market Insight

The European cardiomyopathy market is projected to grow at a steady CAGR throughout the forecast period, supported by government-funded healthcare systems, an aging population, and increasing incidence of hypertension and diabetes. Advancements in diagnostic imaging and the integration of AI in cardiac risk assessment are fueling early diagnosis and efficient management. Widespread adoption of implantable cardioverter-defibrillators (ICDs) and cardiac rehabilitation programs across Germany, France, and the Nordic countries is also contributing to market growth.

U.K. Cardiomyopathy Market Insight

The U.K. cardiomyopathy market is anticipated to grow at a notable CAGR over the forecast period, driven by NHS-supported screening initiatives, increased adoption of non-invasive cardiac imaging, and improved accessibility to genetic counseling for inherited cardiomyopathies. Heightened public awareness of sudden cardiac arrest (SCA) among young athletes and the implementation of national heart health strategies are further propelling diagnosis rates. The expansion of digital health solutions, including telecardiology, is expected to enhance long-term disease monitoring and treatment adherence.

Germany Cardiomyopathy Market Insight

The German cardiomyopathy market is expected to expand steadily, bolstered by the country’s advanced diagnostic capabilities and emphasis on evidence-based cardiac care. Germany’s strong medical device ecosystem fosters early adoption of ICDs, CRTs, and MRI-compatible implants, particularly in tertiary care settings. Increasing integration of AI and machine learning in diagnostic imaging, coupled with a high prevalence of lifestyle-related cardiovascular conditions, is driving demand for both early-stage detection and long-term therapy solutions.

Asia-Pacific Cardiomyopathy Market Insight

The Asia-Pacific cardiomyopathy market is poised to grow at the fastest CAGR of over 6.1% in 2025, fueled by increasing cardiovascular disease prevalence, growing healthcare expenditure, and rapid urbanization in countries such as China, India, and Japan. Government-led screening programs, public health awareness campaigns, and the proliferation of cardiac care centers in urban regions are improving access to timely diagnosis. Local manufacturing of generic cardiac drugs and the expansion of affordable device options are also contributing to rising treatment adoption across the region.

Japan Cardiomyopathy Market Insight

The Japan cardiomyopathy market is gaining momentum due to the country’s aging population, high standards in medical imaging, and a strong focus on precision medicine. The widespread availability of echocardiography and advanced genetic testing protocols is aiding early detection of hypertrophic and restrictive cardiomyopathy. Integration of digital health tools, especially for elderly care and remote cardiac monitoring, is expanding access to personalized treatment plans. Additionally, collaborations between academic institutions and biopharma companies are advancing research into novel therapeutics for cardiomyopathy.

China Cardiomyopathy Market Insight

The China cardiomyopathy market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by the country’s large population base, rapid urbanization, and rising incidence of cardiovascular disease. Significant improvements in hospital infrastructure, widespread adoption of diagnostic imaging, and the increasing availability of oral medications and implantable devices are fueling market growth. Supportive government initiatives to address non-communicable diseases and expansion of insurance coverage are further accelerating diagnosis and treatment accessibility across both urban and rural areas.

Cardiomyopathy Market Share

The Cardiomyopathy industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- GlaxoSmithKline plc (U.K.)

- Cipla Inc (India)

- Teva Pharmaceutical Industries Ltd (Israel)

- Sun Pharmaceutical Industries Ltd (India)

- Zensun (China)

- Hikma Pharmaceuticals PLC (U.K.)

- Endo International Inc (U.S.)

- Zydus Cadila (India)

- Capricor Therapeutics (U.S.)

- MyoKardia (U.S.)

- Aastrom Biosciences (U.S.)

- t2cure GmbH (Germany)

- Boston Scientific Corporation (U.S.)

- Covance (U.S.)

- Mylan N.V. (U.S.)

- Pfizer, Inc. (U.S.)

- BG Medicine Inc. (U.S.)

- Biomerieux (France)

- Bio-Rad Laboratories (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.