Global Cardiorenal Disease Market

Market Size in USD Billion

USD

6.28 Billion

USD

13.85 Billion

2025

2033

USD

6.28 Billion

USD

13.85 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.28 Billion | |

| USD 13.85 Billion | |

| % | |

|

Cardiorenal Disease Market Overview

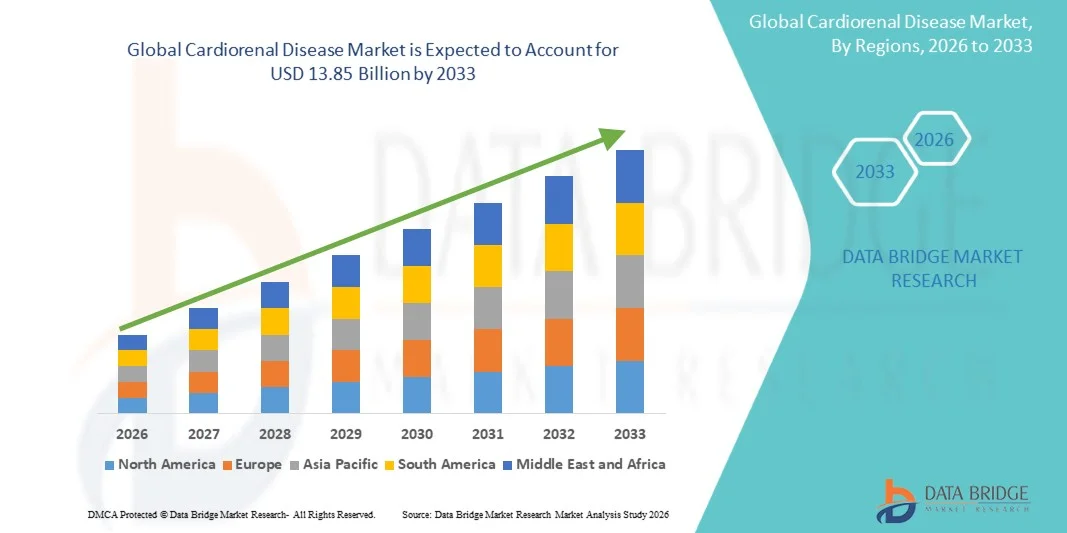

The Cardiorenal Disease Market was valued at USD 6.28 billion in 2025 and is projected to reach USD 13.85 billion by 2033, growing at a CAGR of 10.40% from 2026 to 2033. The market is experiencing steady growth driven by the rising prevalence of chronic kidney disease (CKD), heart failure, and diabetes, increasing awareness of the interconnected nature of cardiovascular and renal disorders, and continuous advancements in targeted therapeutics and diagnostic technologies.

The growing burden of aging populations, sedentary lifestyles, and metabolic disorders worldwide, coupled with increasing healthcare expenditure and improved disease screening programs, is encouraging healthcare providers to adopt integrated cardiorenal management approaches. Innovative therapies such as SGLT2 inhibitors, mineralocorticoid receptor antagonists, and novel cardiovascular-renal protective treatments are transforming patient outcomes, while expanding clinical research and precision medicine initiatives continue to support market growth across hospitals, specialty clinics, and dialysis centers.

Key Market Trends & Insights

- North America dominated the Cardiorenal Disease Market with the largest revenue share of 39.12% in 2025, supported by a high prevalence of cardiovascular and kidney disorders, advanced healthcare infrastructure, and strong adoption of innovative cardiorenal therapies.

- The Cardiorenal Syndrome Type II segment led the market with a 34.82% share in 2025, driven by the increasing prevalence of chronic heart failure leading to progressive kidney dysfunction

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by the rising burden of diabetes and chronic kidney disease, improving healthcare access, and increasing investments in specialty care services across China, India, and Southeast Asia.

- Cardiorenal Syndrome Type IV are the fastest-growing disease type, projected to register a CAGR of 8.4%, reflecting the surge in global burden of chronic kidney disease and its cardiovascular complications

- The Pharmacological Therapy segment dominated the treatment type category with a 47.38% revenue share in 2025, led by the widespread use of evidence-based medications for managing both cardiac and renal complications.

- Oral accounted for 61.24% of the market, preferred by the high patient preference, ease of administration, and extensive availability of oral medications for long-term disease management.

- The Injectable segment is the fastest-growing route of administration category, with a CAGR of 8.2%, driven by the introduction of novel biologics and advanced therapeutic agents targeting complex cardiorenal pathways.

Market Size & Forecast

- Global Market Value (2025): USD 6.28 Billion

- Expected Market Value (2033): USD 13.85 Billion

- Forecast CAGR (2026–2033): 10.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Cardiorenal Disease Market Segmentation

|

Attributes |

Cardiorenal Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· AstraZeneca (U.K.) · Bayer AG (Germany) · Boehringer Ingelheim International GmbH (Germany) · Novartis AG (Switzerland) · Novo Nordisk A/S (Denmark) · F. Hoffmann-La Roche Ltd (Switzerland) · Pfizer Inc. (U.S.) · Eli Lilly and Company (U.S.) · Merck & Co., Inc. (U.S.) · AbbVie Inc. (U.S.) · Amgen Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Bristol Myers Squibb (U.S.) · Sanofi (France) · Otsuka Holdings Co., Ltd. (Japan) · Mitsubishi Tanabe Pharma Corporation (Japan) · Baxter (U.S.) · Fresenius Medical Care AG (Germany) · Vifor Pharma Management Ltd. (Switzerland) · CSL Limited (Australia) |

|

Market Opportunities |

· Expansion of SGLT2 inhibitor and next-generation cardiorenal therapies · Growing adoption of integrated cardiorenal care clinics and multidisciplinary treatment models · Increasing use of biomarker-based diagnostics and predictive analytics tools |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Cardiorenal Disease Market Trends

Trend: Rising Adoption of Integrated Cardiorenal Care Models

Healthcare systems are increasingly adopting integrated cardiorenal care models to improve outcomes for patients with coexisting cardiovascular and kidney disorders. These multidisciplinary approaches enable coordinated disease management, earlier diagnosis, and optimized treatment pathways across cardiology and nephrology specialties. Hospitals and specialty centers are similarly leveraging digital health platforms and remote monitoring solutions to support continuous patient assessment, while advances in biomarker-guided care facilitate personalized interventions that closely align with individual disease progression patterns. For instance, in November 2024, several leading healthcare networks across North America expanded multidisciplinary cardiorenal clinics focused on coordinated management of heart failure and chronic kidney disease patients, highlighting the growing emphasis on integrated care delivery.

Cardiorenal Disease Market Dynamics

Key Market Driver: Expanding Clinical Adoption of Cardiorenal Protective Therapies

The growing clinical adoption of cardiorenal protective therapies has created substantial demand for advanced treatment solutions that address both cardiovascular and renal disease progression. Pharmaceutical companies, healthcare providers, and research organizations are increasingly incorporating therapies with proven dual-organ benefits into treatment guidelines, reducing hospitalization risks, improving patient outcomes, and supporting long-term disease management. The continued expansion of evidence-based treatment protocols is further accelerating utilization across diverse patient populations worldwide. For instance, in January 2025, updated clinical recommendations in several major healthcare markets further reinforced the use of SGLT2 inhibitors for patients with chronic kidney disease and heart failure, supporting broader therapeutic adoption.

Key Restraint/Challenge: High Cost of Long-Term Cardiorenal Disease Management

A significant restraint in the Cardiorenal Disease Market is the high cost associated with long-term disease management and specialized treatment regimens. Modern care pathways often require advanced diagnostics, multiple medications, regular monitoring, and multidisciplinary clinical support, resulting in considerable financial burdens for healthcare systems and patients. The overall treatment expense extends to hospitalization costs, follow-up evaluations, and ongoing disease surveillance, making access challenging for underserved populations and resource-constrained healthcare environments.

For instance, throughout 2024, multiple healthcare systems reported increasing expenditures related to chronic kidney disease and heart failure management programs, reflecting the broader challenge of maintaining affordable long-term care.

Key Market Opportunity: Expansion of Precision Medicine and Biomarker-Based Diagnostics

The expansion of precision medicine in cardiorenal disease management presents a significant market opportunity. Biomarker-enabled diagnostic platforms can support earlier disease detection, provide individualized risk assessment, and facilitate targeted therapeutic decision-making. The development of advanced molecular diagnostics and digital health monitoring technologies is further improving personalized patient management, opening growth opportunities across both developed and emerging healthcare markets seeking to reduce disease burden and improve clinical outcomes. For instance, in September 2024, researchers reported positive advancements in biomarker-guided risk stratification approaches for cardiorenal patients, demonstrating the potential of precision medicine to enhance treatment effectiveness and patient outcomes.

Cardiorenal Disease Market Scope

The cardiorenal disease market is segmented on the basis of disease type, treatment type, route of administration, and end user.

- By Disease Type

On the basis of disease type, the Cardiorenal Disease Market is segmented into Cardiorenal Syndrome Type I, Cardiorenal Syndrome Type II, Cardiorenal Syndrome Type III, Cardiorenal Syndrome Type IV, and Cardiorenal Syndrome Type V. The Cardiorenal Syndrome Type II segment dominated the market with an estimated 34.82% share in 2025, owing to the increasing prevalence of chronic heart failure leading to progressive kidney dysfunction. This condition represents a significant proportion of long-term cardiorenal cases managed across healthcare systems worldwide. Rising geriatric populations and increasing incidence of hypertension and diabetes are contributing to a larger patient pool. Continuous monitoring and prolonged treatment requirements generate substantial healthcare expenditure within this segment. Improved awareness and diagnosis rates are also supporting market expansion. The chronic nature of the disease continues to make this the largest revenue-generating segment globally.

The Cardiorenal Syndrome Type IV segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by the growing global burden of chronic kidney disease and its cardiovascular complications. Patients with long-standing renal impairment face elevated risks of cardiovascular morbidity and mortality, increasing demand for integrated treatment approaches. Advances in nephrology care and early disease detection are improving identification rates. Expanding access to specialty renal services in emerging economies is further supporting growth. Pharmaceutical innovation targeting both renal and cardiovascular outcomes is accelerating adoption. Growing healthcare focus on preventing disease progression is expected to strengthen segment expansion over the forecast period.

- By Treatment Type

On the basis of treatment type, the Cardiorenal Disease Market is segmented into pharmacological therapy, renal replacement therapy, and device-based therapy. The Pharmacological Therapy segment dominated the market with an estimated 47.38% share in 2025, driven by the widespread use of evidence-based medications for managing both cardiac and renal complications. Drug classes such as SGLT2 inhibitors, ACE inhibitors, ARBs, beta blockers, and mineralocorticoid receptor antagonists form the foundation of treatment protocols. Increasing clinical guideline recommendations are encouraging broader adoption of these therapies. Pharmaceutical advancements continue to improve efficacy and patient outcomes. The availability of multiple treatment options across disease stages further supports utilization. Strong physician preference for non-invasive therapeutic approaches reinforces segment leadership.

The Device-Based Therapy segment is expected to witness the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing adoption of advanced cardiovascular support technologies and innovative monitoring solutions. Rising prevalence of severe heart failure and complex cardiorenal conditions is creating demand for specialized intervention devices. Technological advancements are improving treatment precision and patient management capabilities. Expanding use of implantable monitoring systems is enhancing disease surveillance and early intervention. Growing investments in cardiovascular innovation are supporting product development. The segment is also benefiting from increasing acceptance of technology-driven treatment strategies.

- By Route of Administration

On the basis of route of administration, the Cardiorenal Disease Market is segmented into oral, injectable, and intravenous. The Oral segment led the market with an estimated 61.24% share in 2025, owing to high patient preference, ease of administration, and extensive availability of oral medications for long-term disease management. Most first-line cardiorenal therapies are administered orally, enabling convenient treatment adherence. Oral formulations reduce the need for frequent clinical visits and lower overall healthcare costs. Continuous innovation in oral drug development is expanding treatment choices. Favorable reimbursement support in major healthcare markets is also driving adoption. The convenience and accessibility of oral therapies continue to support segment dominance.

The Injectable segment is projected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by the introduction of novel biologics and advanced therapeutic agents targeting complex cardiorenal pathways. Injectable therapies offer enhanced bioavailability and targeted treatment effects for selected patient populations. Growing research activities are expanding the pipeline of innovative injectable products. Increasing hospital-based treatment programs are supporting utilization. Healthcare providers are adopting injectable options for patients requiring intensive disease management. Rising demand for advanced therapies is expected to accelerate segment growth throughout the forecast period.

- By End User

On the basis of end user, the Cardiorenal Disease Market is segmented into hospitals, specialty cardiology clinics, nephrology clinics, dialysis centers, and home healthcare settings. The Hospitals segment dominated the market with an estimated 56.23% share in 2025, driven by the availability of multidisciplinary care teams, advanced diagnostic capabilities, and comprehensive treatment infrastructure. Hospitals serve as primary centers for managing complex cardiorenal patients requiring coordinated cardiac and renal care. High patient admission rates for heart failure and kidney disease contribute significantly to demand. Access to specialized physicians and emergency services strengthens treatment outcomes. Continuous investments in healthcare infrastructure further support segment growth. Their ability to provide integrated care makes hospitals the leading end-user segment.

The Home Healthcare Settings segment is expected to witness the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by increasing emphasis on remote patient management and cost-effective long-term care solutions. Advances in telehealth technologies and home monitoring devices are enabling continuous disease surveillance outside traditional clinical settings. Patients increasingly prefer home-based care due to convenience and reduced hospitalization requirements. Healthcare systems are encouraging decentralized care models to improve efficiency and lower treatment costs. Growing adoption of digital health platforms is further supporting market expansion. The shift toward patient-centric care is expected to drive substantial growth in this segment.

Cardiorenal Disease Market Regional Analysis

North America dominated the Cardiorenal Disease Market with the largest revenue share of 39.12% in 2025, supported by a high prevalence of cardiovascular and kidney disorders, advanced healthcare infrastructure, and strong adoption of innovative cardiorenal therapies. The region also benefits from favorable reimbursement frameworks, extensive clinical research activities, and the presence of leading pharmaceutical and biotechnology companies. Growing utilization of SGLT2 inhibitors and other disease-modifying treatments, coupled with increasing awareness of integrated cardiorenal care, continues to drive market expansion. Rising investments in precision medicine, biomarker-based diagnostics, and multidisciplinary disease management programs continue to strengthen North America's leadership position in the global market.

U.S. Cardiorenal Disease Market Insight

The U.S. cardiorenal disease market is witnessing strong growth due to the rising prevalence of chronic kidney disease, heart failure, and diabetes, along with increasing adoption of advanced therapeutic interventions. The country’s well-established healthcare infrastructure, extensive clinical research ecosystem, and strong presence of leading pharmaceutical companies are driving demand for innovative cardiorenal treatments across hospitals and specialty clinics. In addition, growing emphasis on early diagnosis, integrated disease management, and reducing hospitalization rates is accelerating the adoption of novel therapies and biomarker-based diagnostic solutions.

Europe Cardiorenal Disease Market Insight

The Europe cardiorenal disease market remains a major contributor to global revenue, driven by strong healthcare systems, increasing awareness of cardiorenal disorders, and high adoption of evidence-based treatment approaches. The widespread use of advanced pharmaceuticals, multidisciplinary care models, and specialized cardiovascular and nephrology services is supporting market expansion across the region. Increasing investments in precision medicine technologies, coupled with favorable reimbursement policies and a highly skilled healthcare workforce, continue to enhance the adoption of cardiorenal disease management solutions throughout Europe.

U.K. Cardiorenal Disease Market Insight

The U.K. cardiorenal disease market is experiencing steady growth, supported by rising prevalence of cardiovascular and renal disorders, expanding access to specialty care, and increasing focus on preventive healthcare strategies. Growing investments in advanced diagnostic technologies and innovative therapeutic solutions are contributing to market growth. Furthermore, integration of digital health platforms, remote patient monitoring systems, and data-driven disease management approaches is improving treatment outcomes and healthcare efficiency, positioning the U.K. as a key innovation hub in the cardiorenal disease industry.

Germany Cardiorenal Disease Market Insight

The Germany cardiorenal disease market is expanding steadily due to the country’s advanced healthcare infrastructure, strong clinical research capabilities, and increasing adoption of next-generation treatment solutions. Healthcare providers, research institutions, and pharmaceutical companies are increasingly focusing on integrated management strategies for patients with coexisting cardiovascular and kidney disorders. Continuous advancements in diagnostic technologies, biomarker development, and personalized medicine approaches, along with strong government support for healthcare innovation, are further driving market growth in Germany.

Asia-Pacific Cardiorenal Disease Market Insight

The Asia-Pacific cardiorenal disease market is expected to witness rapid growth, driven by increasing prevalence of diabetes, hypertension, and chronic kidney disease across countries such as China, India, and Japan. Growing awareness regarding early disease detection, rising healthcare expenditure, and increasing adoption of advanced treatment options are supporting regional market expansion. In addition, the growing presence of specialty care centers, expanding pharmaceutical investments, and improving healthcare accessibility are accelerating adoption of cardiorenal disease management solutions across both urban and rural populations.

Japan Cardiorenal Disease Market Insight

The Japan cardiorenal disease market is witnessing consistent growth due to rising investments in advanced healthcare technologies, chronic disease management programs, and cardiovascular research initiatives. Healthcare providers, pharmaceutical companies, and research institutions are increasingly adopting innovative treatment approaches for improving outcomes in patients with combined cardiac and renal disorders. Moreover, increasing utilization of precision medicine tools and the country’s focus on improving quality of care for aging populations are further contributing to market growth.

China Cardiorenal Disease Market Insight

The China cardiorenal disease market is growing rapidly, driven by increasing prevalence of chronic kidney disease, cardiovascular disorders, and diabetes, along with rising government focus on improving public health outcomes. Growing adoption of advanced therapeutic agents and modern diagnostic technologies across hospitals and specialty care centers is significantly boosting market demand. In addition, rising investments in pharmaceutical research, increasing awareness regarding early disease management, and rapid healthcare infrastructure development are positioning China as one of the fastest-growing markets for cardiorenal disease treatment globally.

Cardiorenal Disease Market Share

The cardiorenal disease industry is primarily led by well-established companies, including:

- AstraZeneca (U.K.)

- Bayer AG (Germany)

- Boehringer Ingelheim International GmbH (Germany)

- Novartis AG (Switzerland)

- Novo Nordisk A/S (Denmark)

- Hoffmann-La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Merck & Co., Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

- Sanofi (France)

- Otsuka Holdings Co., Ltd. (Japan)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Baxter (U.S.)

- Fresenius Medical Care AG (Germany)

- Vifor Pharma Management Ltd. (Switzerland)

- CSL Limited (Australia)

Latest Developments in Cardiorenal Disease Market

- In January 2025, Novo Nordisk announced that the U.S. FDA approved Ozempic (semaglutide) to reduce the risk of kidney disease progression, kidney failure, and cardiovascular death in adults with type 2 diabetes and chronic kidney disease. The approval was supported by data from the FLOW trial, which demonstrated significant cardiorenal benefits. This milestone expanded the therapeutic scope of GLP-1 receptor agonists and reinforced the growing focus on integrated cardiovascular and renal disease management

- In January 2025, SeaStar Medical announced that the U.S. FDA approved an Investigational Device Exemption (IDE) application for a feasibility study evaluating its Selective Cytopheretic Device (SCD-ADULT) in patients with acute heart failure and worsening renal function due to cardiorenal syndrome. The study aims to assess the device’s ability to reduce inflammation and improve outcomes in severely ill patients. The development highlights increasing innovation in device-based therapies targeting cardiorenal conditions

- In June 2024, Novo Nordisk announced the discontinuation of its Phase III CLARION-CKD trial evaluating ocedurenone for patients with uncontrolled hypertension and advanced chronic kidney disease after the study failed to meet its primary endpoint. The company subsequently recorded a significant impairment charge related to the asset. The event underscored the scientific and clinical challenges associated with developing novel cardiorenal therapies

- In September 2023, Eli Lilly and Company and Boehringer Ingelheim announced that the U.S. FDA approved Jardiance (empagliflozin) for the treatment of adults with chronic kidney disease at risk of progression. The approval was based on results from the EMPA-KIDNEY Phase III trial, which demonstrated substantial reductions in kidney disease progression and cardiovascular complications. The approval further strengthened the role of SGLT2 inhibitors in cardiorenal disease management

- In July 2023, Boehringer Ingelheim and Eli Lilly and Company announced that the European Commission approved Jardiance (empagliflozin) for the treatment of adults with chronic kidney disease. The approval expanded access to a therapy shown to reduce the risk of kidney disease progression and cardiovascular events. The decision represented a significant advancement in the management of interconnected cardiovascular, renal, and metabolic disorders across Europe

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.