Global Cardiovascular Risk Reduction Market

Market Size in USD Billion

USD

83.46 Billion

USD

112.47 Billion

2025

2033

USD

83.46 Billion

USD

112.47 Billion

2025

2033

| 2026 - 2033 | |

| USD 83.46 Billion | |

| USD 112.47 Billion | |

| % | |

|

Cardiovascular Risk Reduction Market Size

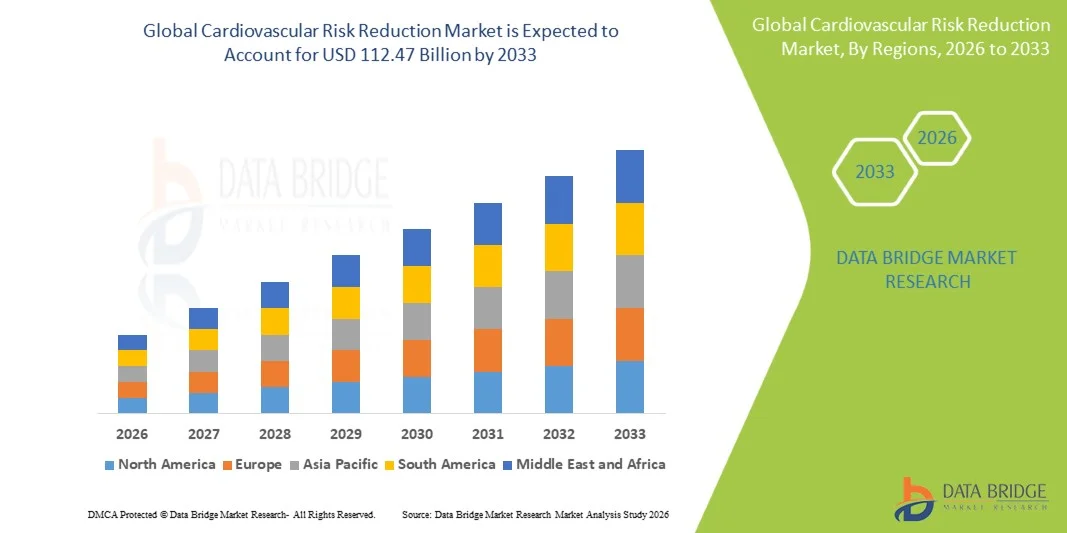

- The global cardiovascular risk reduction market size was valued at USD 83.46 billion in 2025 and is expected to reach USD 112.47 billion by 2033, at a CAGR of 3.80% during the forecast period

- The market growth is largely driven by the rising global burden of cardiovascular diseases, increasing prevalence of hypertension, hyperlipidemia, diabetes, and obesity, along with expanding use of preventive therapies and lipid-lowering and antihypertensive drug classes across high-risk populations

- Furthermore, growing emphasis on early risk assessment, wider adoption of personalized preventive care, and increasing integration of digital health tools and clinical decision-support systems in chronic disease management are accelerating the uptake of cardiovascular risk reduction strategies, thereby significantly boosting market growth

Cardiovascular Risk Reduction Market Analysis

- Cardiovascular risk reduction therapies, including pharmacological and preventive interventions aimed at managing hypertension, dyslipidemia, diabetes, and other metabolic risk factors, play a critical role in reducing the overall incidence of cardiovascular events such as myocardial infarction and stroke across high-risk populations

- The escalating demand for cardiovascular risk reduction solutions is primarily driven by the rising global prevalence of chronic diseases such as hypertension, diabetes, and dyslipidemia, along with increasing awareness of early diagnosis, preventive screening, and long-term risk management strategies

- North America dominated the cardiovascular risk reduction market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare systems, strong adherence to clinical guidelines, high screening rates, and widespread adoption of preventive therapies, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the cardiovascular risk reduction market during the forecast period due to rapidly increasing burden of lifestyle-related diseases, improving healthcare infrastructure, and growing focus on preventive care and early intervention strategies

- The hypertension segment dominated the cardiovascular risk reduction market in 2025, accounting for a market share of 41.8%, attributed to its high global prevalence, strong association with cardiovascular complications, and widespread implementation of long-term blood pressure management programs across both developed and emerging healthcare systems

Report Scope and Cardiovascular Risk Reduction Market Segmentation

|

Attributes |

Cardiovascular Risk Reduction Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cardiovascular Risk Reduction Market Trends

“Expansion of AI-Enabled Predictive Risk Stratification in Preventive Cardiology”

- A significant and accelerating trend in the global cardiovascular risk reduction market is the increasing integration of artificial intelligence (AI) and predictive analytics into clinical decision-making systems to identify high-risk patients earlier and improve preventive treatment outcomes across healthcare settings

- For instance, platforms such as IBM Watson Health and EHR-integrated risk engines are increasingly being used to analyze patient history and biomarkers to support early cardiovascular risk prediction and intervention planning

- AI integration in cardiovascular care enables advanced functions such as predicting the likelihood of myocardial infarction or stroke, stratifying patients based on multi-factor risk profiles, and supporting clinicians in optimizing lipid and blood pressure management strategies over time

- The seamless integration of cardiovascular risk tools with electronic health records (EHRs) and hospital information systems allows centralized monitoring of patient risk factors such as hypertension, diabetes, and dyslipidemia, improving continuity of preventive care

- This trend towards data-driven, personalized, and technology-enabled risk assessment is fundamentally reshaping preventive cardiology, with companies and healthcare providers increasingly adopting AI-supported platforms to improve long-term cardiovascular outcomes

- The demand for AI-enabled cardiovascular risk reduction solutions is growing rapidly across both developed and emerging healthcare systems, as payers and providers increasingly prioritize early intervention and cost-effective chronic disease management

Cardiovascular Risk Reduction Market Dynamics

Driver

“Rising Burden of Lifestyle Diseases and Expanding Preventive Healthcare Adoption”

- The increasing prevalence of lifestyle-related disorders such as hypertension, diabetes, and obesity, coupled with growing awareness of preventive healthcare, is a significant driver for the heightened demand for cardiovascular risk reduction therapies worldwide

- For instance, in April 2025, the American Heart Association reported continued rising incidence of cardiometabolic risk factors globally, reinforcing the need for early intervention and long-term cardiovascular risk management strategies

- As patients become more aware of long-term cardiovascular complications, preventive therapies such as antihypertensives, statins, and antiplatelet agents are increasingly being prescribed to reduce the likelihood of heart attack and stroke

- Furthermore, the growing adoption of clinical guidelines emphasizing early screening and risk-based treatment approaches is making cardiovascular risk reduction an essential part of routine healthcare practice in both primary and specialty care

- The expansion of government-led cardiovascular health awareness programs and workplace wellness initiatives is further accelerating early screening and preventive therapy adoption across large population groups

- The convenience of long-term pharmacological management, combined with increasing access to diagnostic screening and routine health check-ups, is further accelerating the adoption of cardiovascular risk reduction strategies across global populations

Restraint/Challenge

“Low Long-Term Patient Adherence and High Economic Burden of Chronic Therapy”

- Concerns surrounding poor long-term patient adherence to cardiovascular risk reduction therapies, including antihypertensives and lipid-lowering drugs, pose a significant challenge to achieving optimal treatment outcomes and sustained market growth

- For instance, real-world studies have shown that a large proportion of patients discontinue or inconsistently use prescribed cardiovascular preventive medications within the first year of therapy due to lack of symptoms or perceived necessity

- Addressing adherence challenges requires improved patient education, simplified dosing regimens, and enhanced follow-up systems, along with digital health tools that support medication reminders and continuous monitoring of cardiovascular risk factors

- In addition, the long-term economic burden of lifelong preventive therapy, especially in low- and middle-income regions, can limit access to optimal treatment and reduce overall market penetration despite high disease prevalence

- While generic drug availability has improved affordability in many regions, the cumulative cost of combination therapies for multiple risk factors still remains a barrier for sustained patient compliance and healthcare system adoption

Cardiovascular Risk Reduction Market Scope

The market is segmented on the basis of diseases, treatment, route of administration, end-users, and distribution channel.

- By Diseases

On the basis of diseases, the cardiovascular risk reduction market is segmented into hypertension, dyslipidemia, diabetes, and others. The hypertension segment dominated the market with the largest revenue share of 41.8% in 2025, driven by its extremely high global prevalence and strong association with major cardiovascular events such as stroke, heart failure, and myocardial infarction. Hypertension is widely recognized as a primary modifiable risk factor, leading to extensive adoption of long-term antihypertensive therapies across both developed and emerging healthcare systems. Strong guideline-based treatment recommendations and routine screening programs further reinforce its dominance. In addition, the availability of multiple drug classes and combination therapies improves treatment accessibility and adherence in large patient populations.

The diabetes segment is expected to witness the fastest growth rate of 9.6% from 2026 to 2033, fueled by the rapidly increasing global incidence of type 2 diabetes linked to sedentary lifestyles and obesity. Diabetes significantly elevates cardiovascular risk, leading to higher demand for preventive therapies targeting multiple risk factors simultaneously. Growing adoption of integrated care approaches combining glycemic control with cardiovascular protection is further accelerating segment expansion. Pharmaceutical innovations such as SGLT2 inhibitors and GLP-1 receptor agonists with cardioprotective benefits are also driving growth. Rising awareness of early intervention and routine screening in high-risk populations continues to support strong future demand.

- By Treatment

On the basis of treatment, the market is segmented into antiplatelet agents, beta-blockers, angiotensin-converting enzyme (ACE) inhibitors, and others. The antiplatelet agents segment dominated the market with the largest revenue share of 36.4% in 2025, due to their critical role in preventing thrombotic cardiovascular events such as heart attacks and strokes. These drugs are widely used in both primary and secondary prevention, particularly among patients with established cardiovascular disease. Strong clinical evidence supporting long-term efficacy and guideline-based recommendations contributes to their broad adoption. Their affordability and availability in generic formulations further enhance accessibility across global healthcare systems. Increasing use in post-operative and high-risk patient management continues to reinforce segment dominance.

The ACE inhibitors segment is expected to witness the fastest growth rate of 8.7% from 2026 to 2033, driven by their expanding use in managing hypertension, heart failure, and diabetic nephropathy. These drugs are increasingly prescribed as first-line therapy due to their proven ability to reduce cardiovascular morbidity and mortality. Rising prevalence of comorbid conditions such as diabetes and kidney disease is further boosting demand. Combination therapies incorporating ACE inhibitors for multi-risk management are gaining traction in clinical practice. Continued guideline support and expanding adoption in emerging markets are expected to sustain strong growth momentum.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The oral segment dominated the market with the largest revenue share of 88.2% in 2025, primarily due to the widespread use of oral medications for long-term management of cardiovascular risk factors such as hypertension, dyslipidemia, and diabetes. Oral therapies are preferred for their convenience, cost-effectiveness, and ease of administration in outpatient and homecare settings. Most first-line cardiovascular drugs, including statins, beta-blockers, and ACE inhibitors, are available in oral formulations. High patient compliance and strong prescription volumes further support dominance. The chronic nature of treatment also makes oral administration the standard approach in preventive cardiology.

The parenteral segment is expected to witness the fastest growth rate of 10.2% from 2026 to 2033, driven by increasing use in acute cardiovascular care and hospital-based emergency interventions. Injectable therapies are gaining importance in high-risk and critical care settings where rapid drug action is required. Development of biologics and advanced injectable lipid-lowering therapies is further supporting segment expansion. Rising hospital admissions for acute cardiovascular events is increasing demand for parenteral treatment options. Technological advancements in drug delivery systems are also improving safety and efficacy in this segment.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment dominated the market with the largest revenue share of 52.6% in 2025, driven by high patient inflow for diagnosis, emergency care, and management of complex cardiovascular conditions. Hospitals serve as the primary setting for initiating cardiovascular risk reduction therapies, particularly in high-risk and comorbid patients. Availability of advanced diagnostic infrastructure and specialist care supports strong treatment adoption. Government and insurance coverage for hospital-based care further strengthens dominance. In addition, acute cardiovascular events such as heart attacks and strokes are predominantly managed in hospital settings.

The homecare segment is expected to witness the fastest growth rate of 11.4% from 2026 to 2033, fueled by the increasing shift toward remote patient monitoring and long-term chronic disease management outside clinical settings. Growing adoption of digital health tools, wearable devices, and telemedicine is enabling effective cardiovascular risk tracking at home. Patients prefer homecare due to convenience, cost savings, and reduced hospital visits. Expansion of elderly populations with long-term cardiovascular conditions further supports growth. Integration of mobile health applications with medication adherence systems is also accelerating segment expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the market with the largest revenue share of 47.3% in 2025, driven by high prescription volumes for inpatient and post-acute cardiovascular care. Hospital pharmacies play a critical role in dispensing acute and chronic cardiovascular medications immediately after diagnosis or hospitalization. Strong integration with hospital treatment protocols ensures consistent drug availability. Preference for institutional dispensing in high-risk cases further supports dominance. In addition, insurance-linked hospital procurement systems contribute to high utilization of this channel.

The online pharmacy segment is expected to witness the fastest growth rate of 13.8% from 2026 to 2033, fueled by increasing digitalization of healthcare and rising consumer preference for home delivery of chronic medications. Online platforms offer convenience, discounted pricing, and subscription-based medication refills, improving long-term adherence. Growth in e-prescriptions and telemedicine consultations is further accelerating adoption. Expanding internet penetration and smartphone usage, especially in emerging markets, is supporting rapid growth. The COVID-19 pandemic has also permanently shifted consumer behavior toward digital pharmaceutical services.

Cardiovascular Risk Reduction Market Regional Analysis

- North America dominated the cardiovascular risk reduction market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare systems, strong adherence to clinical guidelines, high screening rates, and widespread adoption of preventive therapies, particularly in the U.S.

- Consumers and healthcare providers in the region highly prioritize early diagnosis, guideline-based treatment, and long-term management of risk factors such as hypertension, diabetes, and dyslipidemia through advanced pharmacological interventions

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare expenditure, strong insurance coverage, and the increasing integration of digital health tools for continuous cardiovascular risk monitoring and personalized preventive care

U.S. Cardiovascular Risk Reduction Market Insight

The United States cardiovascular risk reduction market captured the largest revenue share of 81% in North America in 2025, driven by the high prevalence of cardiovascular diseases and strong adoption of preventive healthcare therapies. Patients are increasingly prioritizing early intervention and long-term management of risk factors such as hypertension, diabetes, and dyslipidemia through guideline-based pharmacological treatments. The growing use of combination therapies, routine screening programs, and strong insurance coverage further supports market expansion. Moreover, advanced healthcare infrastructure and increasing integration of digital health tools for continuous monitoring are significantly contributing to market growth.

Europe Cardiovascular Risk Reduction Market Insight

The Europe cardiovascular risk reduction market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent clinical guidelines and a strong emphasis on preventive cardiology across healthcare systems. The rising aging population and increasing prevalence of chronic conditions such as hypertension and dyslipidemia are fostering greater demand for long-term cardiovascular risk management therapies. European healthcare providers are increasingly focusing on cost-effective preventive strategies, including early screening and structured treatment pathways. In addition, strong public healthcare systems and growing awareness of lifestyle-related risk factors are supporting steady market adoption.

United Kingdom Cardiovascular Risk Reduction Market Insight

The United Kingdom cardiovascular risk reduction market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of cardiovascular disease prevention and strong national screening initiatives. Rising cases of obesity, diabetes, and hypertension are encouraging both healthcare providers and patients to adopt preventive pharmacological interventions and lifestyle modification programs. The country’s well-established public healthcare system supports widespread access to essential cardiovascular therapies. Furthermore, growing adoption of digital health tools for remote monitoring and medication adherence is enhancing long-term treatment outcomes.

Germany Cardiovascular Risk Reduction Market Insight

The Germany cardiovascular risk reduction market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure and high emphasis on early diagnosis and chronic disease management. The rising prevalence of cardiovascular risk factors is driving demand for advanced preventive therapies across hospital and outpatient settings. Germany’s focus on precision medicine and structured treatment protocols is further improving patient-specific cardiovascular risk management. In addition, increasing integration of digital health solutions and strong reimbursement support are contributing to sustained market growth.

Asia-Pacific Cardiovascular Risk Reduction Market Insight

The Asia-Pacific cardiovascular risk reduction market is poised to grow at the fastest CAGR of 10.8% during the forecast period of 2026 to 2033, driven by the rapidly increasing burden of cardiovascular diseases and improving access to healthcare services. Rising urbanization, lifestyle changes, and increasing prevalence of risk factors such as diabetes and hypertension are significantly boosting demand for preventive therapies. Government initiatives promoting healthcare modernization and expanding awareness of early diagnosis are further supporting market expansion. Moreover, the availability of affordable generic drugs is accelerating adoption across emerging economies.

Japan Cardiovascular Risk Reduction Market Insight

The Japan cardiovascular risk reduction market is gaining momentum due to its rapidly aging population and strong focus on preventive healthcare and chronic disease management. The country places high importance on early screening and long-term control of hypertension, dyslipidemia, and other cardiovascular risk factors through structured healthcare programs. Advanced healthcare infrastructure and regular health check-ups support consistent adoption of preventive therapies. In addition, integration of digital health monitoring systems and personalized treatment approaches is improving patient adherence and outcomes.

India Cardiovascular Risk Reduction Market Insight

The India cardiovascular risk reduction market accounted for the largest revenue share in Asia Pacific in 2025, attributed to its large population base, rising middle-class income, and increasing burden of lifestyle-related diseases. Growing awareness of conditions such as diabetes, hypertension, and obesity is driving higher adoption of preventive cardiovascular therapies in both urban and semi-urban regions. Government-led health screening initiatives and expanding access to affordable generic medicines are further strengthening market penetration. In addition, rapid healthcare infrastructure development and increasing focus on preventive care are supporting strong market growth.

Cardiovascular Risk Reduction Market Share

The Cardiovascular Risk Reduction industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Amgen Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- Boehringer Ingelheim International GmbH (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Abbott (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Esperion Therapeutics, Inc. (U.S.)

- Ionis Pharmaceuticals, Inc. (U.S.)

- Novo Nordisk A/S (Denmark)

- Servier (France)

- Amarin Corporation plc (Ireland)

What are the Recent Developments in Global Cardiovascular Risk Reduction Market?

- In March 2026, Amgen announced new VESALIUS-CV subgroup results showing that Repatha (evolocumab) reduced the risk of first major cardiovascular events by 31% in high-risk patients without prior cardiovascular disease. The study further confirmed strong LDL-C lowering and reinforced earlier intervention in primary prevention settings

- In November 2025, new large-scale clinical evidence presented at the American Heart Association meeting showed that Amgen’s PCSK9 inhibitor Repatha (evolocumab) reduced the risk of first major cardiovascular events by 25% in high-risk patients without prior heart attacks or strokes. The study also reported a 36% reduction in heart attack risk

- In November 2025, results from the VESALIUS-CV trial demonstrated that evolocumab reduced major cardiovascular events by 25% and heart attack risk by 36% in patients without prior heart attack or stroke. This was the first large-scale evidence confirming that PCSK9 inhibitors can significantly reduce first-time cardiovascular events, expanding their use in preventive cardiology

- In July 2025, the U.S. FDA approved an expanded indication for Novartis’ Leqvio (inclisiran), allowing its use earlier in patients with high LDL cholesterol and increased cardiovascular risk, even before established cardiovascular events. This update supports earlier intervention in lipid management and strengthens preventive cardiovascular risk reduction strategies

- In April 2025, the U.S. FDA approved an updated label for Novartis’ Leqvio (inclisiran) allowing its use as a standalone first-line therapy for lowering LDL cholesterol in adults with hypercholesterolemia. This marked a major shift from its prior role as an add-on therapy to statins. The decision was supported by clinical evidence showing strong LDL-C reduction with twice-yearly dosing and improved patient adherence potential

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.