Global Cataract Treatment Market

Market Size in USD Billion

USD

9.35 Billion

USD

13.81 Billion

2025

2033

USD

9.35 Billion

USD

13.81 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.35 Billion | |

| USD 13.81 Billion | |

| % | |

|

Cataract Treatment Market Size

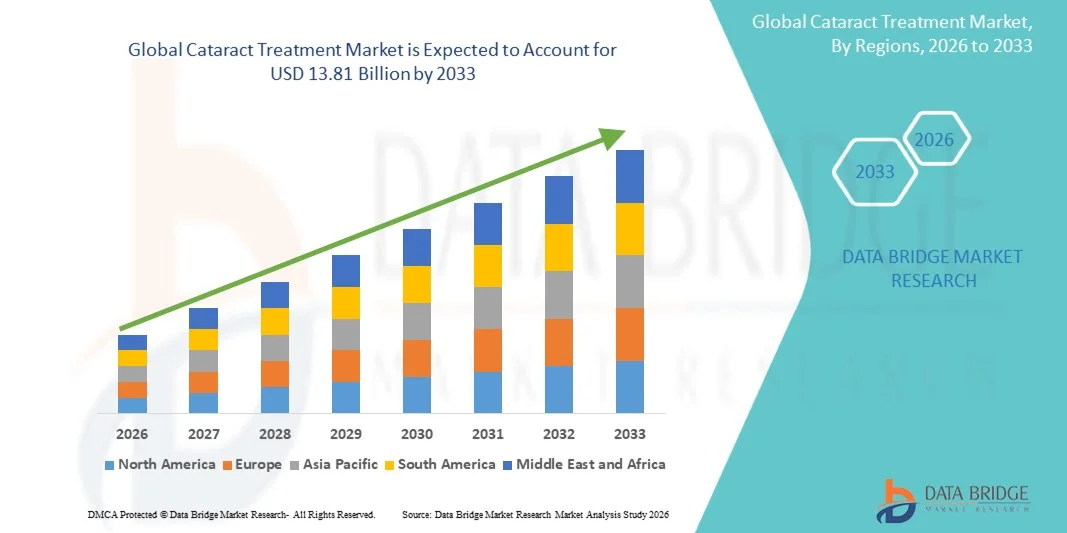

- The global cataract treatment market size was valued at USD 9.35 billion in 2025 and is expected to reach USD 13.81 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cataracts, particularly among the aging population, along with rising awareness regarding vision care and the availability of advanced treatment options, leading to higher adoption of cataract treatment solutions across healthcare settings

- Furthermore, continuous advancements in surgical techniques such as minimally invasive procedures and the development of premium intraocular lenses (IOLs) are enhancing patient outcomes and satisfaction. Growing demand for effective, safe, and quick vision restoration solutions is establishing cataract treatment as a critical component of ophthalmic care. These converging factors are accelerating the uptake of cataract treatment solutions, thereby significantly boosting the market growth

Cataract Treatment Market Analysis

- Cataract treatment, involving surgical procedures and advanced intraocular lens (IOL) implantation to restore vision impaired by lens clouding, is an essential component of modern ophthalmic care across hospitals, specialty clinics, and ambulatory surgical centers due to its high success rate and ability to significantly improve quality of life

- The escalating demand for cataract treatment is primarily driven by the rapidly aging global population, increasing prevalence of vision disorders, and growing awareness regarding timely eye care, along with rising preference for minimally invasive and quick recovery surgical procedures

- North America dominated the cataract treatment market with the largest revenue share of 36.8% in 2025, supported by advanced healthcare infrastructure, high healthcare spending, and early adoption of premium intraocular lenses and laser-assisted surgical technologies, with the U.S. witnessing strong procedural volumes and continuous technological innovations

- Asia-Pacific is expected to be the fastest-growing region in the cataract treatment market during the forecast period due to rising geriatric population, increasing healthcare investments, improving access to eye care services, and growing awareness in countries such as India and China

- The surgery segment held the largest market revenue share of around 72.5% in 2025, driven by the fact that surgery remains the only definitive treatment for cataracts

Report Scope and Cataract Treatment Market Segmentation

|

Attributes |

Cataract Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Cataract Treatment Market Trends

“Advancements in Surgical Technologies and Intraocular Lens (IOL) Innovations”

- A significant and accelerating trend in the global cataract treatment market is the continuous advancement in surgical technologies and the development of innovative intraocular lenses (IOLs), which are enhancing visual outcomes and patient satisfaction

- For instance, the adoption of femtosecond laser-assisted cataract surgery (FLACS) and phacoemulsification techniques has improved surgical precision, reduced recovery time, and minimized complications compared to traditional procedures

- The introduction of advanced IOLs, including multifocal, toric, and extended depth-of-focus lenses, allows patients to achieve improved vision at multiple distances, reducing dependency on corrective eyewear

- Furthermore, the growing preference for premium IOLs is enabling personalized vision correction tailored to individual patient needs, thereby enhancing overall quality of life

- The integration of advanced imaging and diagnostic tools in preoperative planning is also contributing to more accurate lens selection and better surgical outcomes

- This trend towards technologically advanced and patient-centric treatment solutions is reshaping the cataract treatment landscape, with healthcare providers increasingly adopting innovative surgical approaches and premium lens options

Cataract Treatment Market Dynamics

Driver

“Rising Geriatric Population and Increasing Prevalence of Cataract Cases”

- The increasing global geriatric population is a major driver for the cataract treatment market, as aging is the primary risk factor associated with cataract development

- For instance, the growing life expectancy across both developed and developing regions has resulted in a higher number of individuals susceptible to vision impairment caused by cataracts

- In addition, the rising prevalence of lifestyle-related conditions such as diabetes further contributes to the increasing incidence of cataracts, thereby driving the demand for effective treatment solutions

- Government initiatives and awareness programs aimed at reducing preventable blindness are also encouraging early diagnosis and timely surgical intervention

- The expanding healthcare infrastructure and improved access to ophthalmic care services are supporting the growing number of cataract procedures globally

- The availability of advanced surgical techniques and improved reimbursement policies in several regions are further accelerating market growth

Restraint/Challenge

“High Treatment Costs and Limited Access in Developing Regions”

- High costs associated with advanced cataract surgeries and premium intraocular lenses pose a significant challenge to the widespread adoption of cataract treatment, particularly in low- and middle-income regions

- Many patients in developing areas face financial constraints and limited access to specialized ophthalmic care, which delays diagnosis and treatment

- For instance, in several rural regions, patients often need to travel long distances to access cataract surgery services in urban hospitals, leading to delays or complete avoidance of treatment due to travel and accommodation costs

- In addition, inadequate healthcare infrastructure and a shortage of skilled ophthalmologists in rural and underserved regions further restrict market growth

- Concerns regarding postoperative complications and lack of awareness about available treatment options also impact patient willingness to undergo surgery

- Addressing these challenges requires increased investment in healthcare infrastructure, expansion of affordable treatment programs, and training of skilled professionals

- While efforts are being made to improve accessibility and reduce costs, these barriers continue to limit the full potential of the cataract treatment market

- Overcoming these issues through public health initiatives, technological advancements, and cost-effective treatment solutions will be essential for sustained market expansion

Cataract Treatment Market Scope

The market is segmented on the basis of types, treatment, drug class, route of administration, distribution channel, and end-users.

• By Types

On the basis of types, the Cataract Treatment market is segmented into nuclear cataracts, cortical cataracts, posterior subcapsular cataracts, and congenital cataracts. The nuclear cataracts segment dominated the largest market revenue share of approximately 41.8% in 2025, driven by its high prevalence among the aging population. Nuclear cataracts are the most common type associated with age-related vision impairment, making them a primary focus in ophthalmic care. The increasing global geriatric population significantly contributes to the dominance of this segment. In addition, lifestyle factors such as prolonged UV exposure and smoking further increase incidence rates. Early diagnosis and widespread awareness programs have led to increased treatment rates. The availability of advanced surgical techniques such as phacoemulsification supports effective management. Hospitals and eye care centers prioritize nuclear cataract cases due to their volume. Government initiatives promoting eye health screenings also play a crucial role. Continuous advancements in intraocular lens (IOL) technology further strengthen treatment outcomes. Moreover, increased healthcare spending and improved access to ophthalmic care drive sustained growth.

The posterior subcapsular cataracts segment is expected to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by its rising incidence among younger individuals and patients with diabetes or prolonged steroid use. This type progresses faster than other cataracts, increasing the urgency for treatment. Growing awareness regarding early symptoms such as glare and vision disturbances is boosting diagnosis rates. Technological advancements in surgical procedures are improving outcomes for these patients. Increasing prevalence of diabetes globally is a key contributing factor. In addition, improved accessibility to eye care services in emerging economies supports growth. Ophthalmologists are increasingly focusing on early intervention strategies for this segment. Rising adoption of minimally invasive cataract surgeries further accelerates demand. Research and innovation in lens implants are also contributing to better visual outcomes. The segment is expected to expand significantly due to changing disease patterns and improved healthcare infrastructure.

• By Treatment

On the basis of treatment, the market is segmented into medication and surgery. The surgery segment held the largest market revenue share of around 72.5% in 2025, driven by the fact that surgery remains the only definitive treatment for cataracts. Procedures such as phacoemulsification and laser-assisted cataract surgery are widely adopted due to their high success rates. Increasing patient awareness regarding surgical outcomes significantly boosts demand. Technological advancements have reduced surgical risks and recovery time, encouraging more patients to opt for surgery. The growing aging population further drives the need for surgical interventions. In addition, improved healthcare infrastructure and availability of skilled ophthalmologists support segment growth. Government initiatives and insurance coverage for cataract surgeries also contribute to increased adoption. The rising number of eye care centers globally enhances accessibility. Continuous innovation in intraocular lenses improves patient satisfaction and visual outcomes.

The medication segment is projected to grow at the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing research into non-surgical treatment options. Although medications cannot completely cure cataracts, they play a role in managing symptoms and delaying progression. Growing interest in early-stage intervention is supporting this segment. Pharmaceutical companies are investing in developing eye drops and antioxidant therapies. Increasing awareness about preventive eye care also boosts demand. In addition, patients hesitant to undergo surgery often rely on medication initially. Expanding access to ophthalmic drugs in emerging markets further supports growth. Technological advancements in drug delivery systems improve effectiveness. The segment is expected to grow steadily with ongoing clinical research and innovation.

• By Drug Class

On the basis of drug class, the market is segmented into mydriatics, antibiotics, ophthalmic NSAIDs, corticosteroids, and others. The corticosteroids segment dominated the market with a share of approximately 33.9% in 2025, driven by their widespread use in reducing inflammation post cataract surgery. These drugs are essential in preventing complications and ensuring successful recovery. The increasing number of cataract surgeries globally significantly boosts demand for corticosteroids. In addition, their effectiveness in managing ocular inflammation makes them a preferred choice among ophthalmologists. The availability of various formulations further enhances accessibility. Growing awareness about post-operative care supports segment growth. Pharmaceutical companies continue to develop improved formulations with fewer side effects. The segment benefits from strong clinical adoption and established treatment protocols. Increasing healthcare expenditure also contributes to its dominance.

The ophthalmic NSAIDs segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by their effectiveness in pain management and inflammation control. These drugs are increasingly used as alternatives or complements to corticosteroids. Rising awareness about minimizing steroid-related side effects boosts adoption. Increasing surgical volumes further drive demand for post-operative medications. Advancements in drug formulations improve patient comfort and compliance. In addition, growing preference for combination therapies supports segment growth. Expansion of ophthalmic care services in developing regions enhances accessibility. Continuous research and development efforts are expected to further accelerate growth.

• By Route of Administration

On the basis of route of administration, the market is segmented into oral and topical. The topical segment held the largest market share of 68.2% in 2025, driven by its direct application to the eye and higher effectiveness in delivering targeted treatment. Eye drops are widely used both before and after cataract surgery, making them a primary mode of administration. Patients prefer topical treatments due to their ease of use and minimal systemic side effects. The availability of a wide range of ophthalmic formulations further supports segment growth. Increasing awareness regarding eye care and hygiene also boosts demand. Pharmaceutical advancements in eye drop formulations improve drug absorption and effectiveness. In addition, topical administration is cost-effective and easily accessible.

The oral segment is expected to grow at the fastest CAGR of 6.9% from 2026 to 2033, driven by its role in supporting overall eye health and managing underlying conditions. Oral medications are often used as adjunct therapy in cataract management. Increasing awareness about nutritional supplements for eye health contributes to growth. In addition, patients prefer oral medications for convenience in certain cases. Expanding healthcare access in emerging markets further supports demand. Ongoing research into oral antioxidant therapies is expected to drive future growth.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with a share of 49.5% in 2025, driven by the high number of cataract surgeries performed in hospitals. Patients typically receive medications directly from hospital pharmacies during treatment. The presence of trained healthcare professionals ensures proper drug dispensing. In addition, hospitals maintain a consistent supply of essential ophthalmic drugs. Increasing hospital admissions for eye surgeries further support segment growth. Government investments in healthcare infrastructure also contribute to dominance.

The online pharmacy segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, driven by the growing adoption of digital healthcare platforms. Patients increasingly prefer online channels for convenience and home delivery. Rising internet penetration and smartphone usage support this trend. Competitive pricing and discounts further attract consumers. The COVID-19 pandemic accelerated the shift toward online medicine purchases. Improved regulatory frameworks enhance consumer trust. The segment is expected to grow significantly with continued digital transformation in healthcare.

• By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment held the largest market share of 54.1% in 2025, driven by the availability of advanced surgical facilities and skilled ophthalmologists. Hospitals are the primary centers for cataract diagnosis and treatment. The increasing number of surgical procedures significantly boosts demand. In addition, hospitals offer comprehensive care, including pre- and post-operative management. Government support and funding further strengthen this segment.

The homecare segment is projected to grow at the fastest CAGR of 8.7% from 2026 to 2033, driven by the increasing preference for post-operative care at home. Patients prefer homecare for convenience and reduced hospital visits. Advancements in telemedicine and remote monitoring support this trend. The growing elderly population further drives demand for home-based care. Increasing awareness about self-care and recovery management also boosts growth. The segment is expected to expand rapidly with the shift toward patient-centric healthcare models.

Cataract Treatment Market Regional Analysis

- North America dominated the cataract treatment market with the largest revenue share of 36.8% in 2025, supported by advanced healthcare infrastructure, high healthcare spending, and early adoption of premium intraocular lenses (IOLs) and laser-assisted surgical technologies

- The region benefits from a high volume of cataract procedures and strong presence of leading ophthalmic device manufacturers

- Patients and healthcare providers in the region increasingly prefer advanced surgical solutions such as femtosecond laser-assisted cataract surgery and premium IOLs, which enhance visual outcomes and reduce dependence on glasses. In addition, favorable reimbursement policies, well-established clinical practices, and continuous technological advancements are further driving market growth across North America

U.S. Cataract Treatment Market Insight

The U.S. cataract treatment market captured the largest revenue share within North America in 2025, driven by strong procedural volumes and continuous technological innovations. The country witnesses high adoption of premium intraocular lenses, including multifocal and toric lenses, along with increasing utilization of minimally invasive and laser-assisted surgical techniques. Moreover, the growing aging population, rising awareness regarding vision care, and the presence of leading industry players are significantly contributing to market expansion in the United States.

Europe Cataract Treatment Market Insight

The Europe cataract treatment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the increasing prevalence of age-related eye disorders and well-established public healthcare systems. Government-supported healthcare programs and rising adoption of advanced surgical technologies are supporting market growth. In addition, growing geriatric population and increasing demand for improved visual outcomes are encouraging the use of premium IOLs and modern cataract treatment procedures across the region.

U.K. Cataract Treatment Market Insight

The U.K. cataract treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by rising awareness about eye health and increasing demand for timely surgical interventions. The presence of structured healthcare services and initiatives to reduce surgical waiting times are contributing to higher procedure volumes. Furthermore, growing adoption of advanced surgical techniques and intraocular lenses is enhancing treatment outcomes in the U.K.

Germany Cataract Treatment Market Insight

The Germany cataract treatment market is expected to expand at a considerable CAGR during the forecast period, driven by the country’s strong healthcare infrastructure and emphasis on medical innovation. Increasing adoption of advanced ophthalmic technologies, including laser-assisted surgery and premium IOLs, is supporting market growth. In addition, high healthcare expenditure and a growing elderly population are further contributing to the increasing demand for cataract treatment in Germany.

Asia-Pacific Cataract Treatment Market Insight

The Asia-Pacific cataract treatment market is expected to grow at the fastest CAGR during the forecast period, driven by the rising geriatric population, increasing healthcare investments, and improving access to eye care services. Growing awareness regarding cataract-related blindness and expanding healthcare infrastructure in countries such as India and China are significantly boosting demand. In addition, government initiatives and outreach programs aimed at reducing preventable blindness are accelerating the adoption of cataract surgeries across the region.

Japan Cataract Treatment Market Insight

The Japan cataract treatment market is gaining momentum due to its rapidly aging population and high standard of healthcare services. The country has a strong focus on early diagnosis and advanced treatment options, leading to widespread adoption of modern cataract surgical techniques and premium intraocular lenses. Continuous technological advancements and high patient awareness are key factors supporting market growth in Japan.

China Cataract Treatment Market Insight

The China cataract treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to its large aging population and improving healthcare infrastructure. Increasing government initiatives to address preventable blindness, along with rising awareness about eye health, are driving the demand for cataract surgeries. Furthermore, the expansion of healthcare facilities and availability of cost-effective treatment options are key factors propelling market growth in China.

Cataract Treatment Market Share

The Cataract Treatment industry is primarily led by well-established companies, including:

- Alcon Inc. (Switzerland)

- Johnson & Johnson Vision (U.S.)

- Bausch + Lomb (Canada)

- Carl Zeiss Meditec AG (Germany)

- Hoya Corporation (Japan)

- EssilorLuxottica (France)

- Nidek Co., Ltd. (Japan)

- Topcon Corporation (Japan)

- STAAR Surgical Company (U.S.)

- Rayner Intraocular Lenses Ltd. (U.K.)

- Oculentis GmbH (Germany)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Allergan (AbbVie Inc.) (Ireland)

- Aurolab (India)

- Appasamy Associates (India)

- Eyekon Medical Inc. (U.S.)

- Lenstec, Inc. (U.S.)

- HumanOptics AG (Germany)

Latest Developments in Global Cataract Treatment Market

- In October 2025, BVI Medical, a leading global ophthalmic device company, announced that the U.S. Food and Drug Administration (FDA) approved its FINEVISION® HP trifocal intraocular lens (IOL) for cataract surgery. This next-generation lens, already widely used internationally, provides vision correction at near, intermediate, and far distances through advanced diffractive optics and improved light distribution. The approval significantly expands premium cataract surgery options in the U.S., reinforcing BVI’s leadership in advanced intraocular lens innovation

- In January 2025, Alcon, a global leader in eye care, expanded the commercial rollout of its PanOptix Pro trifocal intraocular lens, which had received FDA approval in late 2023. The lens offers enhanced contrast sensitivity, reduced visual disturbances such as halos, and improved low-light performance, enabling greater independence from glasses for cataract patients. This launch reflects continuous innovation in premium IOL technologies aimed at improving post-surgical visual outcomes

- In March 2025, Bausch + Lomb, a major ophthalmology company, highlighted advancements in its enVista Envy intraocular lens, designed to deliver a continuous range of vision while minimizing glare and halos. Incorporating ActivSync Optic and ClearPath technologies, the lens improves contrast sensitivity and visual clarity, representing a significant development in cataract treatment focused on patient-centric visual performance

- In February 2025, the American Refractive Surgery Council, an industry organization focused on vision correction awareness, reported growing adoption of the Light Adjustable Lens (LAL) technology in cataract surgery. This FDA-approved innovation allows post-operative customization of vision using UV light adjustments, with clinical outcomes showing a high percentage of patients achieving 20/20 vision without glasses, marking a major advancement in personalized cataract treatment

- In May 2025, global ophthalmology researchers and clinicians highlighted the ongoing development of accommodative intraocular lenses designed to restore the eye’s natural focusing ability after cataract surgery. These next-generation lenses, currently under investigation, aim to provide a full range of vision and represent a key innovation area expected to transform cataract treatment outcomes in the coming years

- In June 2023, BVI Medical introduced its FineVision HP trifocal intraocular lens in international markets, particularly in Japan, prior to its U.S. approval. The lens demonstrated strong clinical performance with accurate refractive outcomes and improved vision across multiple distances, supporting its later regulatory success and global adoption in cataract procedures

- In January 2024, the ophthalmology industry witnessed multiple product approvals and launches across cataract and presbyopia treatment segments, reflecting rapid technological advancements in intraocular lenses and surgical techniques. These developments underscore the growing focus on improving visual outcomes, reducing complications, and enhancing patient quality of life following cataract surgery

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.