Global Catheters Market

Market Size in USD Billion

USD

6.84 Billion

USD

11.23 Billion

2025

2033

USD

6.84 Billion

USD

11.23 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 6.84 Billion |

Market Size (Forecast Year) |

USD 11.23 Billion |

CAGR |

% |

Major Markets Players |

|

Catheters Market Overview

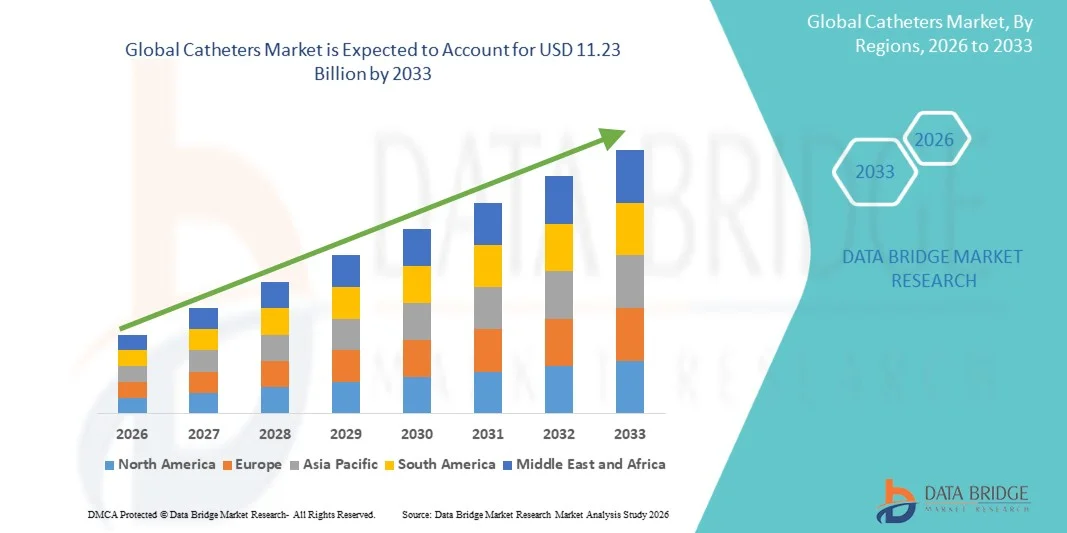

The Catheters Market was valued at USD 6.84 billion in 2025 and is projected to reach USD 11.23 billion by 2033, growing at a CAGR of 6.40% from 2026 to 2033. The market is witnessing steady growth driven by the rising prevalence of cardiovascular, urological, and renal disorders, increasing volumes of minimally invasive procedures, and continuous advancements in catheter design and biomaterials.

The growing burden of chronic diseases such as heart disease, kidney failure, and urinary incontinence, coupled with an aging global population, is significantly boosting demand for catheter-based interventions across hospitals and specialty care centers. In addition, the shift toward minimally invasive and image-guided procedures is further accelerating adoption, as catheters play a critical role in diagnosis and treatment across multiple therapeutic areas.

Key Market Trends & Insights

- North America dominated the Catheters Market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong presence of leading medical device manufacturers.

- The Urology Catheters segment led the market with a 34.2% share in 2025, driven by the growing prevalence of urinary incontinence, benign prostatic hyperplasia (BPH), urinary retention, and other urological disorders.

- Asia-Pacific is expected to be the fastest-growing region from 2026 to 2033, with a projected CAGR of 7.4%, fueled by expanding healthcare access, rising surgical volumes, and increasing investment in hospital infrastructure across China, India, and Southeast Asia.

- Neurovascular Catheters are the fastest-growing product type, projected to register a CAGR of 8.1%, reflecting the surge in increasing incidence of ischemic stroke, cerebral aneurysms, and other neurovascular disorders.

- Foley Catheters segment dominated the design category with a 37.8% revenue share in 2025, led by their extensive use in hospitals, surgical procedures, intensive care units, and long-term urinary management.

- Urology & Urinary Care accounted for 31.9% of the market, preferred by the high prevalence of urinary tract disorders, incontinence, and bladder dysfunction worldwide.

- The Neurology segment is the fastest-growing application category, with a CAGR of 8.3%, driven by the rising incidence rates of stroke, aneurysms, and neurovascular diseases.

Market Size & Forecast

- Global Market Value (2025): USD 6.84 Billion

- Expected Market Value (2033): USD 11.23 Billion

- Forecast CAGR (2026–2033): 6.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Catheters Market Segmentation

|

Attributes |

Catheters Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Medtronic (Ireland) · BD (U.S.) · Boston Scientific Corporation (U.S.) · Abbott (U.S.) · Teleflex Incorporated (U.S.) · B. Braun SE (Germany) · Terumo Corporation (Japan) · Coloplast A/S (Denmark) · Convatec Group PLC (U.K.) · Hollister Incorporated (U.S.) · Cook (U.S.) · Cardinal Health (U.S.) · Edwards Lifesciences Corporation (U.S.) · Merit Medical Systems, Inc. (U.S.) · AngioDynamics, Inc. (U.S.) · NIPRO CORPORATION (Japan) · Penumbra, Inc. (U.S.) · BIOTRONIK SE & Co. KG (Germany) · Amsino International, Inc. (U.S.) · Well Lead Medical Co., Ltd. (China) |

|

Market Opportunities |

· Expansion of home healthcare and self-catheterization programs · Growing adoption of antimicrobial and infection-prevention catheter technologies · Increasing utilization of catheter-based minimally invasive procedures in cardiovascular and neurovascular interventions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Catheters Market Trends

Trend: Rising Adoption of Antimicrobial and Advanced Coated Catheters

Healthcare providers are increasingly adopting antimicrobial-coated and hydrophilic-coated catheters to reduce infection risks, improve patient comfort, and enhance clinical outcomes across long-term and acute care settings. These advanced catheter technologies help minimize catheter-associated urinary tract infections and bloodstream infections while supporting smoother insertion and extended usage durations. Hospitals, ambulatory care centers, and home healthcare providers are similarly utilizing coated catheter solutions to meet evolving patient safety standards, while material innovations continue improving biocompatibility and overall device performance.

For instance, in January 2024, Becton, Dickinson and Company (BD) expanded its portfolio of infection-prevention vascular access technologies, highlighting the industry's focus on reducing catheter-related complications.

Catheters Market Dynamics

Key Market Driver: Growing Demand for Minimally Invasive Diagnostic and Therapeutic Procedures

The increasing preference for minimally invasive procedures has created substantial demand for advanced catheter systems that support diagnosis, treatment, and monitoring across cardiovascular, urological, neurovascular, and electrophysiology applications. Healthcare providers and medical device manufacturers are deploying catheter-based technologies as a core component of modern treatment pathways, reducing recovery times, lowering procedural risks, and improving patient outcomes. Rising prevalence of chronic diseases and expanding access to specialized healthcare services are further accelerating catheter utilization across global markets. For instance, in September 2024, Medtronic announced continued advancements in catheter-based cardiovascular therapies, reinforcing the growing role of minimally invasive interventions.

Key Restraint/Challenge: Risk of Catheter-Associated Infections and Procedural Complications

A significant restraint in the Catheters Market is the persistent risk of catheter-associated infections and procedure-related complications. Long-term catheterization can increase the likelihood of urinary tract infections, bloodstream infections, thrombosis, and tissue damage, requiring strict monitoring and adherence to clinical protocols. The overall burden extends to additional treatment costs, prolonged hospital stays, and regulatory compliance requirements, making healthcare providers increasingly cautious regarding catheter selection, placement, and maintenance practices.

For instance, ongoing initiatives by the Centers for Disease Control and Prevention (CDC) continue to emphasize prevention strategies for catheter-associated infections, reflecting the broader challenge faced by healthcare systems worldwide.

Key Market Opportunity: Expansion of Home Healthcare and Self-Catheterization Solutions

The expansion of home healthcare services presents a significant market opportunity. User-friendly intermittent and specialty catheter solutions can support long-term disease management, improve patient independence, and reduce hospital utilization for chronic conditions. The development of compact, discreet, and technologically enhanced catheter systems is further increasing accessibility across aging populations and patients requiring ongoing care. Growing reimbursement support and healthcare decentralization trends are also creating growth opportunities across emerging and developed healthcare markets. For instance, in April 2024, Convatec Group PLC continued expanding its continence care and intermittent catheter offerings, supporting the shift toward home-based patient management.

Catheters Market Scope

The catheters market is segmented on the basis of product type, design, application, and end user.

- By Product Type

On the basis of product type, the Catheters Market is segmented into cardiovascular catheters, urology catheters, intravenous catheters, neurovascular catheters, dialysis catheters, and specialty catheters. The Urology Catheters segment dominated the market with a 34.2% share in 2025, owing to the growing prevalence of urinary incontinence, benign prostatic hyperplasia (BPH), urinary retention, and other urological disorders. These catheters are extensively used across hospitals, long-term care facilities, and home healthcare settings for both short-term and chronic patient management. The rising geriatric population, which is more susceptible to bladder dysfunction and urinary complications, continues to support demand. Increasing awareness regarding intermittent catheterization and improvements in catheter materials are further enhancing patient comfort and adoption. The segment also benefits from recurring demand due to regular replacement requirements. Strong clinical necessity and broad applicability continue to reinforce its leadership position globally.

The Neurovascular Catheters segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by the increasing incidence of ischemic stroke, cerebral aneurysms, and other neurovascular disorders. These catheters play a critical role in minimally invasive neurological interventions, including thrombectomy and embolization procedures. Growing investments in advanced neurointerventional technologies and expanding access to stroke care centers are accelerating adoption. Technological advancements in microcatheters and navigation systems are improving procedural precision and patient outcomes. Rising awareness regarding early stroke intervention is further contributing to market expansion. Increasing demand for minimally invasive neurosurgical procedures is expected to sustain strong growth throughout the forecast period.

- By Design

On the basis of design, the Catheters Market is segmented into 2-way catheters, 3-way catheters, 4-way catheters, intermittent catheters, Foley catheters, and external catheters. The Foley Catheters segment dominated the market with a 37.8% share in 2025, driven by their extensive use in hospitals, surgical procedures, intensive care units, and long-term urinary management. These indwelling catheters provide continuous bladder drainage and remain the standard solution for patients requiring prolonged catheterization. Their widespread adoption is supported by increasing surgical volumes and the growing prevalence of chronic urinary conditions. Continuous improvements in catheter coatings and infection-control features are enhancing safety and performance. Healthcare providers continue to rely on Foley catheters due to their clinical effectiveness and ease of use. Their established role in patient care maintains strong market demand worldwide.

The Intermittent Catheters segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, fueled by increasing preference for self-catheterization and infection prevention strategies. These catheters are associated with lower risks of catheter-associated urinary tract infections compared to long-term indwelling alternatives. Growing patient awareness and healthcare initiatives promoting independent bladder management are supporting adoption. Advancements in hydrophilic coatings and user-friendly catheter designs are improving convenience and patient compliance. Home healthcare expansion and favorable reimbursement policies in several countries are further driving market penetration. The segment is also benefiting from increasing focus on quality-of-life improvements for patients with chronic urological disorders.

- By Application

On the basis of application, the Catheters Market is segmented into cardiovascular procedures, urology & urinary care, neurology, gastroenterology, renal care, and respiratory & anesthesia use. The Urology & Urinary Care segment accounted for the largest market share of 31.9% in 2025, owing to the high prevalence of urinary tract disorders, incontinence, and bladder dysfunction worldwide. Catheters remain essential for both acute and chronic urinary management across diverse patient populations. Rising demand from aging populations and long-term care facilities continues to support utilization. Increased diagnosis rates and greater awareness of urinary health conditions are further expanding treatment volumes. Technological advancements aimed at improving patient comfort and reducing infection rates are strengthening product adoption. The broad clinical use of urinary catheters ensures continued segment dominance.

The Neurology segment is anticipated to be the fastest-growing application area, expanding at a CAGR of 8.3% from 2026 to 2033, driven by rising incidence rates of stroke, aneurysms, and neurovascular diseases. Catheter-based neurointerventional procedures are increasingly preferred due to their minimally invasive nature and favorable patient outcomes. Growing investments in stroke management infrastructure and specialized neurovascular treatment centers are accelerating procedure volumes. Advances in catheter navigation technologies are enabling more precise and effective interventions. Increasing healthcare expenditure and improved access to neurological care are supporting market growth. Expanding clinical adoption of neurovascular therapies is expected to drive strong demand over the coming years.

- By End User

On the basis of end user, the Catheters Market is segmented into hospitals, ambulatory surgical centers, specialty clinics, home healthcare, dialysis centers, and long-term care facilities. The Hospitals segment dominated the market with a 52.8% revenue share in 2025, driven by high patient volumes and extensive use of catheter-based procedures across multiple medical specialties. Hospitals serve as primary centers for cardiovascular interventions, urinary care, critical care management, and dialysis-related treatments. Availability of advanced infrastructure and skilled healthcare professionals supports widespread catheter utilization. Increasing numbers of surgical procedures and hospital admissions continue to strengthen demand. Hospitals also remain key purchasers of technologically advanced catheter systems. Their central role in healthcare delivery sustains the segment’s market leadership.

The Home Healthcare segment is projected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, supported by the increasing shift toward decentralized and patient-centric care models. Growing numbers of patients requiring long-term urinary management, dialysis support, and chronic disease care are driving demand for home-use catheter solutions. Technological advancements have improved ease of use, safety, and patient comfort, enabling broader adoption outside clinical settings. Rising healthcare costs are encouraging providers and payers to promote home-based treatment alternatives. Expanding elderly populations and increasing preference for independent care are further contributing to growth. Continued development of user-friendly catheter products is expected to accelerate adoption throughout the forecast period.

Catheters Market Regional Analysis

North America dominated the Catheters Market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong presence of leading medical device manufacturers. The region also benefits from a high prevalence of cardiovascular, urological, and renal disorders, strong reimbursement frameworks, and widespread adoption of minimally invasive treatment approaches. Increasing utilization of antimicrobial-coated and specialty catheters across hospitals, ambulatory care centers, and home healthcare settings continues to support market growth. Growing investments in healthcare innovation and rising demand for patient-centric care solutions further strengthen North America’s leadership position in the global market.

U.S. Catheters Market Insight

The U.S. catheters market is witnessing strong growth due to rising prevalence of cardiovascular diseases, urinary disorders, and chronic kidney conditions requiring long-term catheterization and minimally invasive interventions. The country’s advanced healthcare infrastructure, favorable reimbursement policies, and strong presence of leading medical device manufacturers are driving demand across hospitals, ambulatory care centers, and home healthcare settings. In addition, growing adoption of antimicrobial-coated, hydrophilic-coated, and specialty catheter technologies is accelerating market expansion while improving patient safety and clinical outcomes.

Europe Catheters Market Insight

The Europe catheters market remains a major contributor to global revenue, driven by strong healthcare systems, technological innovation, and high demand for minimally invasive treatment solutions. The widespread use of catheters in cardiovascular procedures, urinary care, dialysis, and neurovascular interventions is supporting market expansion across the region. Increasing investments in advanced catheter technologies, coupled with strict infection-control standards and a growing elderly population, continue to enhance catheter adoption throughout Europe.

U.K. Catheters Market Insight

The U.K. catheters market is experiencing steady growth, supported by rising demand for chronic disease management, increasing surgical volumes, and expanding utilization of minimally invasive procedures. Growing investments in advanced catheter technologies and increasing focus on reducing catheter-associated complications are contributing to market growth. Furthermore, integration of infection-prevention coatings, patient-centric catheter designs, and improved clinical care pathways is enhancing treatment efficiency and positioning the U.K. as a key market for catheter innovation.

Germany Catheters Market Insight

The Germany catheters market is expanding steadily due to the country’s advanced healthcare infrastructure, strong medical device industry, and increasing adoption of innovative catheter technologies. Hospitals, specialty clinics, and research institutions are increasingly utilizing catheters for cardiovascular interventions, urinary management, dialysis procedures, and neurovascular treatments. Continuous advancements in catheter materials, infection-control technologies, and minimally invasive treatment approaches, along with strong government focus on healthcare quality, are further driving market growth in Germany.

Asia-Pacific Catheters Market Insight

The Asia-Pacific catheters market is expected to witness rapid growth, driven by increasing healthcare expenditure, expanding hospital infrastructure, and rising prevalence of chronic diseases across countries such as China, India, and Japan. Growing awareness regarding early diagnosis and minimally invasive treatments, rising adoption of advanced catheter technologies, and increasing demand for cost-effective healthcare solutions are supporting regional market expansion. Additionally, improving access to healthcare services and a rapidly aging population are accelerating catheter adoption across hospitals and home healthcare settings.

Japan Catheters Market Insight

The Japan catheters market is witnessing consistent growth due to rising demand for cardiovascular care, urinary management solutions, and advanced minimally invasive procedures. Healthcare providers, hospitals, and specialty centers are increasingly adopting high-performance catheters for diagnosis, treatment, and long-term patient care. Moreover, increasing integration of advanced biomaterials, infection-prevention technologies, and the country’s focus on high-quality healthcare delivery are further contributing to market growth.

China Catheters Market Insight

The China catheters market is growing rapidly, driven by increasing healthcare investments, expanding medical infrastructure, and rising government focus on improving patient care standards. Growing adoption of advanced catheter technologies across cardiovascular, urology, dialysis, and neurovascular applications is significantly boosting market demand. In addition, rising prevalence of chronic diseases, increasing awareness regarding minimally invasive treatments, and rapid healthcare modernization are positioning China as one of the fastest-growing markets for catheters globally.

Catheters Market Share

The catheters industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- BD (U.S.)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Teleflex Incorporated (U.S.)

- Braun SE (Germany)

- Terumo Corporation (Japan)

- Coloplast A/S (Denmark)

- Convatec Group PLC (U.K.)

- Hollister Incorporated (U.S.)

- Cook (U.S.)

- Cardinal Health (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- AngioDynamics, Inc. (U.S.)

- NIPRO CORPORATION (Japan)

- Penumbra, Inc. (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- Amsino International, Inc. (U.S.)

- Well Lead Medical Co., Ltd. (China)

Latest Developments in Catheters Market

- In July 2025, Terumo Neuro unveiled new real-world physician preference data for its SOFIA™ 88 Neurovascular Support Catheter at the Society of NeuroInterventional Surgery (SNIS) Annual Meeting. The data demonstrated strong performance in trackability, atraumatic design, and overall physician experience during stroke intervention procedures. The development highlights growing innovation in neurovascular catheter technologies aimed at improving procedural efficiency and patient outcomes in acute ischemic stroke treatment

- In April 2025, Medtronic announced positive one-year clinical outcomes for its Affera™ pulsed field ablation (PFA) catheter technologies, including the investigational Sphere-360™ and Sphere-9™ catheters for atrial fibrillation treatment. The results demonstrated strong safety, efficiency, and procedural performance, reinforcing the growing adoption of advanced electrophysiology catheters in cardiac rhythm management. This development reflects the industry's focus on minimally invasive cardiac interventions

- In March 2024, Boston Scientific Corporation received U.S. FDA approval for its AGENT™ Drug-Coated Balloon Catheter, the first drug-coated coronary balloon approved in the United States for the treatment of coronary in-stent restenosis. The catheter is designed to reopen narrowed coronary arteries while reducing the likelihood of repeat blockage. The approval expanded treatment options for interventional cardiologists and marked a significant advancement in catheter-based cardiovascular therapy

- In August 2023, Boston Scientific Corporation received FDA approval for the POLARx™ Cryoablation System, featuring the POLARx FIT Cryoablation Balloon Catheter for the treatment of paroxysmal atrial fibrillation. The catheter introduced dual balloon-size capability within a single device, improving procedural flexibility and physician control during cardiac ablation procedures. The launch strengthened Boston Scientific’s electrophysiology catheter portfolio and expanded treatment options for heart rhythm disorders

- In October 2023, Boston Scientific Corporation reported positive 12-month results from the pivotal ADVENT clinical trial evaluating its FARAPULSE™ Pulsed Field Ablation System and associated catheter technologies. The study met primary safety and efficacy endpoints and demonstrated noninferiority compared with conventional ablation approaches for atrial fibrillation treatment. The results supported broader adoption of pulsed field ablation catheters and underscored the industry's shift toward next-generation cardiac electrophysiology solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.