Global Cellulite Treatment Market

Market Size in USD Billion

USD

1.85 Billion

USD

4.08 Billion

2025

2033

USD

1.85 Billion

USD

4.08 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.85 Billion | |

| USD 4.08 Billion | |

| % | |

|

Cellulite Treatment Market Overview

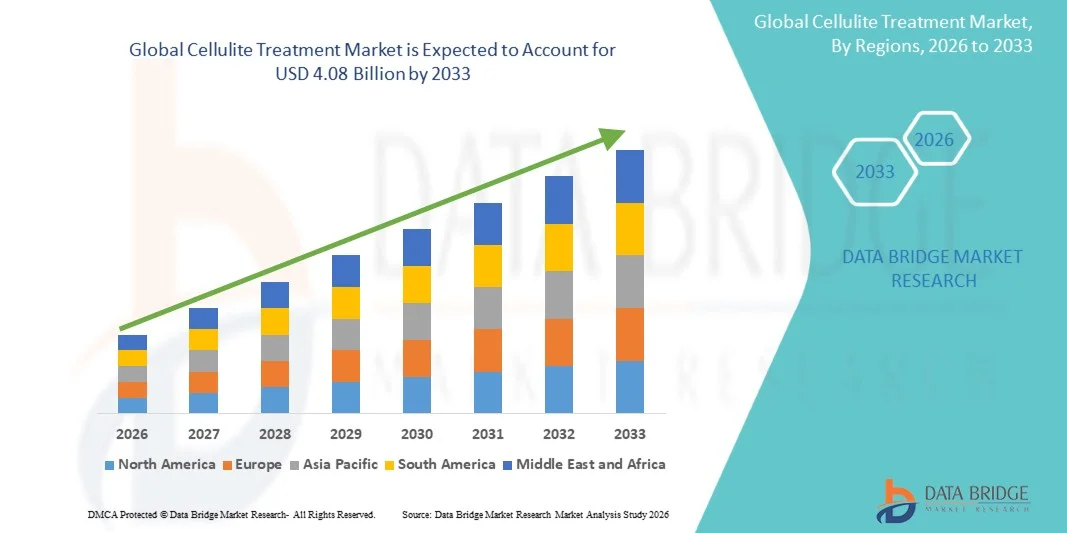

The Cellulite Treatment Market was valued at USD 1.85 billion in 2025 and is projected to reach USD 4.08 billion by 2033, growing at a CAGR of 10.40% from 2026 to 2033. The Cellulite Treatment Market is experiencing steady growth driven by rising aesthetic consciousness, increasing demand for non-invasive body contouring procedures, and continuous advancements in cosmetic dermatology technologies.

The growing prevalence of lifestyle-related factors such as obesity, sedentary behavior, hormonal changes, and aging skin is significantly contributing to the demand for cellulite reduction treatments worldwide. In addition, increasing awareness about personal grooming and physical appearance, supported by social media influence and rising disposable incomes, is encouraging more consumers to opt for professional aesthetic procedures. Clinics and dermatology centers are increasingly adopting advanced technologies such as laser therapy, radiofrequency devices, ultrasound-based treatments, and mechanical massage systems, which offer safer, faster, and more effective results compared to traditional methods. These minimally invasive and non-invasive solutions are becoming the preferred choice among consumers due to reduced downtime, improved safety profiles, and visible outcomes.

Key Market Trends & Insights

- North America dominated the Cellulite Treatment Market with the largest revenue share of 38.42% in 2025, supported by high aesthetic awareness, strong presence of advanced dermatology clinics, and widespread adoption of non-invasive cosmetic procedures.

- The Energy-Based Treatment segment dominated the market with a 48.62% share in 2025, driven by strong adoption of radiofrequency, laser, and ultrasound technologies for skin tightening and cellulite reduction

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rising disposable incomes, expanding beauty and wellness industry, and increasing adoption of aesthetic procedures in China, India, and South Korea.

- Energy-Based Treatment is the fastest-growing treatment segment, projected to register a CAGR of 7.3%, reflecting strong demand for laser, ultrasound, and radiofrequency-based cellulite reduction technologies.

- The Hard Cellulite segment dominates the type category with a 39.28% revenue share in 2025, as it is more commonly treated in clinical settings due to its deeper fibrous structure and higher visibility.

- Specialized Dermatology Clinics account for 46.87% of the market share in 2025, preferred for their advanced equipment, skilled dermatologists, and high success rates in aesthetic procedures.

- The Topical Treatment segment is the fastest-growing segment, with a CAGR of 6.9%, driven by increasing demand for at-home skincare solutions and adjunct therapies supporting clinical cellulite reduction procedures.

Market Size & Forecast

- Global Market Value (2025): USD 1.85 Billion

- Expected Market Value (2033): USD 4.08 Billion

- Forecast CAGR (2026–2033): 10.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Cellulite Treatment Market Segmentation

|

Attributes |

Cellulite Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• AbbVie Inc. (U.S.) |

|

Market Opportunities |

· Rising demand for non-invasive and minimally invasive aesthetic procedures · Expansion of advanced energy-based technologies such as radiofrequency · Increasing penetration of dermatology clinics and medical spas in developing |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Cellulite Treatment Market Trends

Trend: Rising Demand for Aesthetic Body Contouring & Non-Invasive Cosmetic Procedures

The Cellulite Treatment Market is witnessing strong growth due to increasing demand for non-invasive aesthetic procedures such as radiofrequency, laser therapy, and acoustic wave therapy. Consumers are increasingly opting for treatments that offer visible skin tightening and fat reduction without surgery or long recovery periods. Clinics and medspa chains are rapidly adopting advanced devices such as BTL Vanquish ME (BTL Industries) and Endermologie systems by LPG Systems, which are widely used for cellulite reduction. According to clinical adoption trends in aesthetic medicine, non-invasive body contouring procedures have grown significantly, accounting for a major share of dermatology clinic revenues globally, particularly in North America and Europe.

Cellulite Treatment Market Dynamics

Key Market Driver: Rising Aesthetic Awareness and Expansion of Energy-Based Devices

The increasing focus on physical appearance, fueled by social media influence and rising disposable income, is driving strong demand for cellulite treatment procedures globally. Advanced energy-based devices such as radiofrequency (RF), laser-based systems, and high-intensity focused ultrasound (HIFU) are being widely adopted across dermatology clinics. Companies like Cynosure (U.S.), Candela Medical (U.S.), and InMode Ltd. (Israel) are continuously innovating minimally invasive platforms that improve skin tightening and fat reduction outcomes. Clinically, RF-based cellulite reduction treatments have shown visible improvement in skin texture in 60–80% of patients after multiple sessions, making them highly preferred in medical aesthetics clinics. The growing number of accredited dermatology centers in the U.S., South Korea, and Germany further supports market expansion.

Key Restraint/Challenge: High Treatment Cost and Limited Insurance Coverage

A major restraint in the cellulite treatment market is the high cost of advanced aesthetic procedures, combined with the lack of insurance reimbursement since cellulite treatment is considered cosmetic rather than medically necessary. A single session of professional cellulite reduction therapy can range from USD 150 to USD 500 per session in developed markets, with multiple sessions required for optimal results. This cost barrier limits adoption among middle-income consumers, particularly in price-sensitive regions such as parts of Asia-Pacific, Latin America, and Africa. Additionally, advanced devices from manufacturers like BTL Aesthetics, Lumenis Ltd., and Venus Concept require significant capital investment for clinics, further restricting penetration in small dermatology practices.

Key Market Opportunity: Technological Advancements and Growth of At-Home Cellulite Treatment Devices

The integration of advanced technologies such as AI-driven skin analysis, smart RF devices, and wearable body contouring systems is creating strong growth opportunities in the cellulite treatment market. Companies are increasingly developing at-home solutions, such as handheld RF devices and massage-based systems, to target the growing self-care segment. For instance, devices like NuFACE body contouring tools and Zemits aesthetic equipment are gaining traction among consumers seeking affordable alternatives to clinic-based treatments. Furthermore, the global medical aesthetics market has been expanding at a steady pace, with body contouring representing one of the fastest-growing segments. Increasing medical tourism in countries such as South Korea, Thailand, and Turkey, where cosmetic procedures are offered at 30–60% lower cost compared to the U.S. or Western Europe, is further accelerating market opportunity. The combination of AI-enabled treatment planning, personalized dermatology solutions, and expanding clinic networks is expected to significantly enhance accessibility and adoption of cellulite treatment technologies worldwide.

Cellulite Treatment Market Scope

The Cellulite Treatment market is segmented on the basis of type, procedure, treatment, and end use.

- By Type

On the basis of type, the Cellulite Treatment Market is segmented into soft cellulite, hard cellulite, and edematous cellulite. The Hard Cellulite segment dominated the market with a 39.28% share in 2025, owing to its deeper fibrous structure, higher visibility, and greater resistance to topical and lifestyle-based management. This makes it the most commonly treated form in clinical dermatology and aesthetic medicine. Hard cellulite is strongly associated with aging, hormonal changes, and reduced skin elasticity, driving strong demand for professional aesthetic interventions. Energy-based devices such as radiofrequency, laser therapy, and acoustic wave systems are widely used for effective reduction. Leading companies including BTL Industries, Cynosure, and InMode actively target this segment with advanced technologies. Dermatology clinics prefer combination therapies to achieve better clinical outcomes. Rising awareness of body contouring procedures continues to support market growth. High demand for visible and long-lasting results further strengthens adoption across developed regions. Increasing penetration of aesthetic clinics in North America and Europe is also contributing to dominance. Clinical evidence supporting device-based treatments continues to reinforce segment leadership.

The Edematous Cellulite segment is expected to register the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing awareness of lymphatic drainage disorders and fluid retention-related skin concerns. This type is more commonly observed among younger women influenced by hormonal fluctuations and lifestyle-related metabolic conditions. Rising demand for holistic wellness and body detoxification treatments is supporting segment expansion. Clinics are increasingly using lymphatic drainage massage, ultrasound therapy, and combination aesthetic procedures for improved outcomes. Growing preference for preventive aesthetic care is also accelerating demand. Social media influence and increasing body image awareness are encouraging early treatment adoption. Edematous cellulite responds well to combination therapies, improving clinical success rates. Expansion of medspa and wellness centers globally is further driving growth. Increasing disposable income in emerging economies is supporting accessibility. Non-invasive treatment preference continues to strengthen market expansion.

- By Procedure

On the basis of procedure, the Cellulite Treatment Market is segmented into minimally invasive procedures, non-invasive procedures, and topical procedures. The Non-invasive Procedures segment dominated the market with a 44.15% share in 2025, driven by strong consumer preference for painless, safe, and downtime-free aesthetic treatments. Technologies such as radiofrequency, laser therapy, ultrasound, and cryolipolysis are widely used across dermatology clinics and medspas. High patient acceptance, repeat treatment cycles, and strong safety profiles further support dominance. Increasing aesthetic awareness and social media influence are boosting demand globally. Leading companies such as Candela Medical, Cynosure, and Lumenis are expanding non-invasive portfolios. Rising medical tourism in countries such as South Korea and Thailand is also contributing to demand. Insurance exclusion of cosmetic procedures increases out-of-pocket spending on non-invasive solutions. Continuous technological advancements are improving treatment precision and outcomes. Clinics prefer non-invasive procedures due to high profitability and low risk. Growing global demand for body contouring continues to strengthen segment leadership.

The Minimally Invasive Procedures segment is projected to register the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing demand for long-lasting and more intensive cellulite reduction results. Techniques such as subcision, mesotherapy, and injectable collagen stimulators are gaining strong clinical adoption. These procedures are preferred for moderate to severe cellulite cases where non-invasive treatments are less effective. Rising availability of trained aesthetic professionals is supporting segment growth. Patients seeking faster and more visible outcomes are shifting toward minimally invasive options. Technological improvements in injectable and device-assisted therapies are enhancing safety and precision. Growth of premium dermatology clinics in urban regions is accelerating adoption. Combination therapies with energy-based devices are improving effectiveness. Increasing disposable incomes are making advanced treatments more accessible. Expanding cosmetic dermatology infrastructure globally continues to drive growth.

- By Treatment

On the basis of treatment, the Cellulite Treatment Market is segmented into energy-based treatment, non-energy-based treatment, and others. The Energy-Based Treatment segment dominated the market with a 48.62% share in 2025, driven by strong adoption of radiofrequency, laser, and ultrasound technologies for skin tightening and cellulite reduction. These technologies stimulate collagen production and improve skin texture, making them highly preferred in clinical dermatology settings. Leading companies such as BTL Industries, InMode, Cynosure, and Candela Medical are continuously innovating advanced energy-based platforms. Strong clinical outcomes and visible aesthetic improvements are increasing patient preference. The non-invasive nature of these treatments further supports global adoption. Rising number of aesthetic procedures performed annually is boosting market growth. High repeat treatment cycles contribute significantly to revenue generation. Increasing awareness of body contouring solutions is strengthening demand. Continuous R&D in energy-based devices is improving efficiency and safety. Expanding dermatology clinic networks worldwide are reinforcing segment dominance.

The Others segment, including regenerative and emerging therapies, is expected to register the fastest CAGR of 7.2% from 2026 to 2033, driven by growing adoption of collagen-stimulating injectables, stem-cell-based therapies, and advanced biostimulation techniques. Increasing focus on long-term skin regeneration and natural aesthetic outcomes is accelerating demand. Clinics are integrating multi-modal treatment approaches for improved effectiveness. Rising investment in regenerative dermatology research is supporting innovation. Patients are increasingly preferring non-surgical and long-lasting solutions. Technological advancements in bio-aesthetic products are improving treatment performance. Expansion of premium aesthetic clinics is supporting adoption. Regulatory approvals for advanced regenerative therapies are increasing commercialization. Rising demand for anti-aging treatments is further boosting growth. Growing global wellness and aesthetic awareness is supporting long-term expansion.

- By End Use

On the basis of end use, the Cellulite Treatment Market is segmented into hospitals, ambulatory surgical centers, and specialized dermatology clinics. The Specialized Dermatology Clinics segment dominated the market with a 46.87% share in 2025, driven by high patient preference for expert-led aesthetic procedures and access to advanced cellulite treatment technologies. These clinics provide customized treatment plans combining multiple modalities for improved outcomes. Availability of skilled dermatologists enhances success rates and patient satisfaction. High patient footfall and repeat visits contribute to strong revenue generation. Clinics are equipped with advanced devices from companies such as InMode, BTL, and Cynosure. Increasing demand for personalized aesthetic care is supporting growth. Strong presence of dermatology clinics in North America and Europe reinforces dominance. Growing medical tourism in Asia-Pacific is further expanding demand. Continuous technological upgrades improve treatment efficiency and safety. Expanding medspa and cosmetic dermatology networks globally are strengthening market position.

The Ambulatory Surgical Centers segment is projected to register the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing demand for cost-effective outpatient aesthetic procedures. ASCs offer shorter waiting times and lower costs compared to hospitals and specialized clinics. Rising preference for minimally invasive cellulite treatments is supporting adoption. Expansion of outpatient cosmetic surgery infrastructure is accelerating growth. Increasing availability of advanced aesthetic devices in ASCs is improving treatment quality. Patients prefer ASCs for convenience, affordability, and quick recovery. Growth of elective cosmetic procedures without insurance coverage is boosting demand. Increasing number of certified cosmetic surgeons in ASCs is expanding accessibility. Rising urbanization and disposable income are supporting patient inflow. Strong expansion in emerging markets is further driving segment growth.

Cellulite Treatment Market Regional Analysis

North America dominated the Cellulite Treatment Market and accounted for the largest revenue share of 38.42% in 2025, supported by high aesthetic awareness, strong presence of advanced dermatology clinics, and widespread adoption of non-invasive cosmetic procedures. The region benefits from early adoption of advanced energy-based technologies such as radiofrequency, laser therapy, and ultrasound devices. Strong presence of key players including InMode Ltd., Cynosure LLC, BTL Industries, and Candela Medical further strengthens market dominance. Increasing demand for body contouring procedures, driven by rising obesity rates and lifestyle-related cellulite prevalence, is boosting market growth. High disposable income and willingness to spend on aesthetic treatments are also key drivers. The U.S. and Canada continue to lead due to advanced healthcare infrastructure and strong medspa networks. Growing social media influence and beauty standards are further accelerating procedure adoption. Rising number of dermatology clinics and cosmetic centers is expanding service availability. Continuous technological advancements in non-invasive treatments are improving outcomes and patient satisfaction. The region is expected to maintain strong leadership due to innovation and high procedural volume.

U.S. Cellulite Treatment Market Insight

The U.S. Cellulite Treatment market is witnessing strong growth due to rising demand for non-invasive aesthetic procedures, increasing obesity prevalence, and strong consumer focus on body aesthetics. The country has a highly developed dermatology and medspa ecosystem, with widespread availability of advanced cellulite reduction technologies. Leading companies such as AbbVie (Allergan Aesthetics), Cynosure, InMode, and Cutera are actively expanding product portfolios in the U.S. market. High adoption of energy-based devices such as radiofrequency and laser systems is driving treatment effectiveness and popularity. Increasing number of cosmetic procedures performed annually, estimated in millions across body contouring categories, supports market expansion. Strong insurance exclusion for cosmetic treatments increases out-of-pocket spending, boosting clinic revenues. Rising demand from both women and men is expanding the patient base. Growth of medical tourism within premium cosmetic hubs such as California and New York is also contributing. Continuous innovation in minimally invasive procedures is improving clinical outcomes. The U.S. remains the largest revenue-generating country in the global cellulite treatment landscape.

Europe Cellulite Treatment Market Insight

The Europe Cellulite Treatment market remains a major contributor to global revenue, driven by strong aesthetic awareness, advanced dermatology infrastructure, and high adoption of non-invasive cosmetic procedures. Countries such as Germany, France, Italy, and the U.K. are leading adopters of cellulite reduction technologies. Strong presence of companies such as Lumenis Ltd., BTL Industries, and DEKA M.E.L.A. supports technological advancement in the region. High demand for skin tightening and body contouring procedures among aging populations is a key growth driver. Strict regulatory standards ensure high treatment safety and quality outcomes. Increasing popularity of medspas and aesthetic clinics is further supporting market penetration. Growing focus on wellness and personal grooming culture is boosting demand. Rising number of trained dermatologists and aesthetic practitioners enhances service availability. Medical tourism, particularly in countries like Turkey, is also contributing to regional growth. Europe continues to maintain a strong position due to high procedure adoption and innovation in aesthetic technologies.

U.K. Cellulite Treatment Market Insight

The U.K. Cellulite Treatment market is experiencing steady growth, driven by rising demand for aesthetic body contouring procedures and increasing adoption of non-invasive technologies. Growth is supported by expanding medspa networks and dermatology clinics across major cities such as London and Manchester. Strong consumer awareness regarding cosmetic treatments and skin health is boosting demand. The presence of advanced aesthetic device providers such as BTL Industries and Cynosure supports market development. Increasing obesity rates and lifestyle-related skin concerns are contributing to higher treatment uptake. Rising preference for minimally invasive procedures with no downtime is accelerating adoption. Social media influence and celebrity-driven beauty trends are further driving demand. Expansion of private cosmetic healthcare services is improving accessibility. Continuous technological integration such as AI-based skin analysis tools is enhancing treatment precision. The U.K. remains an important innovation hub for aesthetic treatment adoption in Europe.

Germany Cellulite Treatment Market Insight

The Germany Cellulite Treatment market is expanding steadily due to strong healthcare infrastructure, high aesthetic awareness, and increasing demand for advanced dermatology treatments. German consumers show strong preference for clinically validated, non-invasive aesthetic procedures. Leading companies such as BTL Industries, Siemens Healthineers (support technologies), and DEKA M.E.L.A. are active in the market. High adoption of radiofrequency and laser-based cellulite treatments is driving segment growth. Germany’s aging population is increasing demand for skin tightening and body contouring solutions. Strict medical regulations ensure high-quality treatment standards and patient safety. Increasing number of specialized dermatology clinics and aesthetic centers supports accessibility. Rising disposable income levels are encouraging elective cosmetic procedures. Strong focus on technological innovation in medical aesthetics is improving treatment effectiveness. Germany continues to play a key role in Europe’s aesthetic medicine market expansion.

Asia-Pacific Cellulite Treatment Market Insight

The Asia-Pacific Cellulite Treatment market is expected to witness the fastest growth, with a CAGR of 7.6% from 2026 to 2033, driven by rising disposable incomes, expanding beauty and wellness industry, and increasing adoption of aesthetic procedures. Rapid urbanization and changing lifestyle patterns are increasing cellulite prevalence across countries such as China, India, Japan, and South Korea. Growing popularity of body aesthetics influenced by social media and K-beauty trends is boosting demand. Expansion of dermatology clinics and medspa chains is improving accessibility. Increasing medical tourism in countries like Thailand and South Korea is further supporting growth. Rising investments in aesthetic device manufacturing and distribution are strengthening market presence. Growing awareness of non-invasive treatments is accelerating adoption. Strong presence of regional players alongside global companies is increasing competition. Government support for healthcare infrastructure development is also contributing to market expansion. Asia-Pacific is emerging as the most lucrative growth region in the Cellulite Treatment Market.

Japan Cellulite Treatment Market Insight

The Japan Cellulite Treatment market is witnessing consistent growth due to strong focus on advanced cosmetic technologies, aging population, and high aesthetic awareness. Japanese consumers prefer minimally invasive and highly precise dermatology treatments. Increasing adoption of energy-based devices such as radiofrequency and ultrasound systems is driving market expansion. Strong presence of companies such as Lumenis, Cynosure, and local aesthetic device providers supports innovation. High demand for skin tightening and anti-aging procedures is contributing to growth. Integration of AI and VR-based diagnostic tools is improving treatment planning. Rising number of specialized cosmetic clinics in urban regions is increasing accessibility. Cultural emphasis on personal grooming and appearance further supports demand. Medical aesthetics tourism is also gradually increasing. Japan continues to be a technologically advanced and high-value market in Asia-Pacific.

China Cellulite Treatment Market Insight

The China Cellulite Treatment market is growing rapidly, driven by rising disposable income, urbanization, and increasing demand for aesthetic procedures. Expanding middle-class population is significantly boosting demand for non-invasive cosmetic treatments. Strong adoption of advanced technologies such as laser therapy, RF devices, and ultrasound-based systems is accelerating growth. Increasing presence of domestic aesthetic device manufacturers along with global players is enhancing competition. Social media influence and beauty culture trends are strongly driving demand. Rapid expansion of dermatology clinics and medspa chains is improving accessibility. Government focus on healthcare modernization is supporting infrastructure development. Rising popularity of medical tourism within Asia is also contributing to market expansion. Growing awareness of body contouring and cellulite reduction treatments is increasing procedure volumes. China is expected to remain one of the fastest-growing and most dynamic markets globally.

Cellulite Treatment Market Share

The Cellulite Treatment industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Cynosure LLC (U.S.)

- Alma Lasers (Israel)

- Candela Medical (U.S.)

- BTL Industries Inc. (Czech Republic)

- Lumenis Ltd. (Israel)

- Solta Medical (Bausch Health Companies Inc.) (U.S.)

- Merz Pharmaceuticals GmbH (Germany)

- Endymed Medical Ltd. (Israel)

- Cutera Inc. (U.S.)

- Sciton Inc. (U.S.)

- Venus Concept Inc. (Canada)

- InMode Ltd. (Israel)

- Sisram Medical Ltd. (China)

- Hologic Inc. (U.S.)

- Fotona d.o.o. (Slovenia)

- Zimmer MedizinSysteme GmbH (Germany)

- DEKA M.E.L.A. Srl (Italy)

- Syneron Medical Ltd. (Israel)

- ThermiGen LLC (U.S.)

- Galderma S.A. (Switzerland)

- Pierre Fabre Group (France)

- Revance Therapeutics Inc. (U.S.)

- Allergan Aesthetics (AbbVie) (U.S.)

- Sinclair Pharma Ltd. (U.K.)

- Hugel Inc. (South Korea)

- Jeisys Medical Inc. (South Korea)

- Classys Inc. (South Korea)

- Lutronic Corporation (South Korea)

- Cynosure Lutronic Inc. (U.S./South Korea)

- Alma Lasers Ltd. (Israel)

- BTL Aesthetics (Czech Republic)

- Aesthetic Technology Ltd. (U.K.)

Latest Developments in Cellulite Treatment Market

- In January 2022, Cynosure (a division of Hologic) received FDA 510(k) clearance expansion updates for its SculpSure body contouring platform, strengthening its position in non-invasive aesthetic fat and cellulite-related treatments. The system uses laser-based technology for non-surgical body sculpting and is widely adopted in dermatology clinics for cellulite-associated fat reduction procedures

- In December 2022, Sofwave Medical announced FDA clearance for its SUPERB technology for cellulite improvement, marking a significant advancement in non-invasive ultrasound-based cellulite treatment. The clinical study supporting the approval showed visible improvement in cellulite appearance, with high patient satisfaction rates and strong efficacy outcomes in treated subjects

- In May 2022, Revelle Aesthetics introduced Avéli, a minimally invasive FDA-cleared cellulite treatment device, enabling targeted release of fibrous septa responsible for cellulite appearance. The system gained attention for delivering visible results in a single in-office procedure, representing a shift toward precision-based cellulite treatment technologies

- In March 2023, Sentient launched Sentient Sculpt™ in the United States, introducing a non-invasive microwave and electromagnetic wave-based cellulite reduction technology. The system was designed to target cellulite fibers and fat cells through controlled energy delivery, offering a no-incision, no-downtime treatment option across all skin types

- In May 2023, InMode launched its EvolveX body treatment platform, integrating radiofrequency (RF), high-voltage pulse (HVP), and electrical muscle stimulation (EMS) technologies. The system was designed for skin remodeling, body contouring, and cellulite reduction, enabling non-invasive aesthetic treatments with minimal discomfort and no downtime

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.