Global Central Line Associated Bloodstream Infection Treatment Market

Market Size in USD Billion

USD

1.71 Billion

USD

2.32 Billion

2025

2033

USD

1.71 Billion

USD

2.32 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.71 Billion | |

| USD 2.32 Billion | |

| % | |

|

Central Line Associated Bloodstream Infection Treatment Market Size

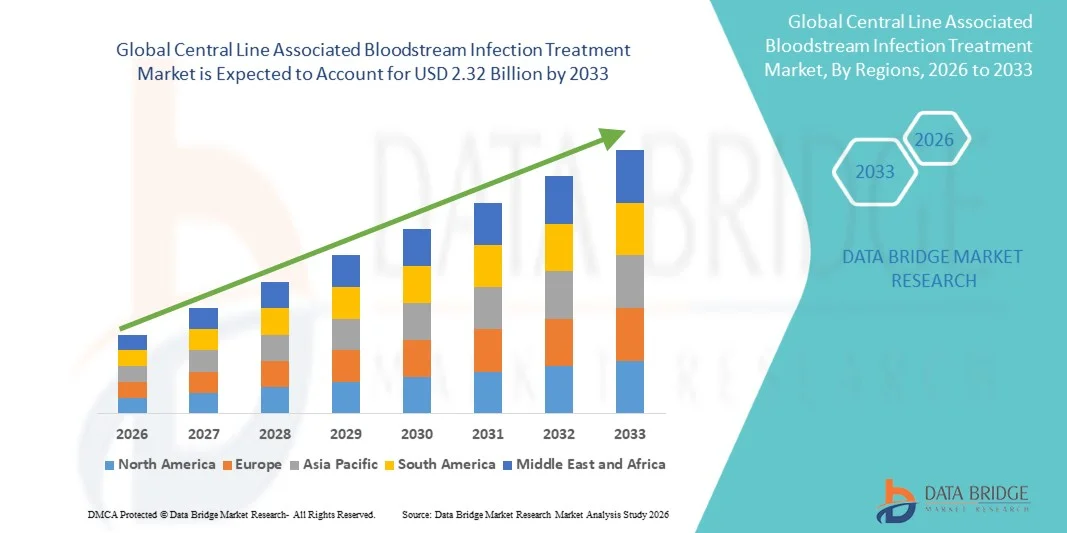

- The global central line associated bloodstream infection treatment market size was valued at USD 1.71 billion in 2025 and is expected to reach USD 2.32 billion by 2033, at a CAGR of 3.90% during the forecast period

- The market growth is largely fueled by the rising incidence of hospital-acquired infections, increasing use of central venous catheters, and continuous advancements in infection prevention technologies across healthcare settings. Growing adoption of evidence-based clinical practices, improved diagnostic methods, and greater hospital focus on reducing CLABSI rates are driving the demand for effective CLABSI treatment solutions, including antimicrobial therapies, catheter lock solutions, and rapid diagnostic tools

- Furthermore, increasing awareness among healthcare providers regarding standardized infection-control protocols and the need for timely, accurate CLABSI management is strengthening the demand for safe, efficient, and integrated treatment practices. These converging factors are accelerating the uptake of Central Line Associated Bloodstream Infection Treatment solutions, thereby significantly boosting the industry's growth

Central Line Associated Bloodstream Infection Treatment Market Analysis

- Central Line Associated Bloodstream Infection (CLABSI) treatments, including antimicrobial therapies, catheter lock solutions, infection-control devices, and rapid diagnostic tools, are becoming increasingly vital components of modern healthcare systems due to rising hospital-acquired infection rates, growing use of central venous catheters, and the need for timely, effective infection management across intensive care units and acute care settings

- The escalating demand for CLABSI treatment solutions is primarily fueled by heightened awareness of infection prevention protocols, increasing emphasis on patient safety, and the adoption of advanced diagnostic technologies that enable faster detection and targeted treatment of bloodstream infections. In addition, global initiatives to reduce CLABSI rates in hospitals are strengthening market growth

- North America dominated the central line associated bloodstream infection treatment market with the largest revenue share of 40.60% in 2025, supported by advanced healthcare infrastructure, high catheter utilization, strong adoption of evidence-based infection prevention protocols, and widespread availability of specialized infectious disease management solutions. The U.S. experienced substantial growth due to early adoption of antimicrobial lock therapies, increased CLABSI surveillance programs, and strong investment in hospital infection-control systems

- Asia-Pacific is expected to be the fastest growing region in the central line associated bloodstream infection treatment market during the forecast period, driven by increasing healthcare expenditure, rising rates of central line catheterization, improved access to diagnostic technologies, and growing awareness among clinicians regarding early detection and treatment of bloodstream infections across India, China, and Japan

- The Intravenous segment dominated the largest market revenue share of 57.4% in 2025, owing to its critical role in delivering high-concentration antibiotics directly into the bloodstream for immediate therapeutic effect

Report Scope and Central Line Associated Bloodstream Infection Treatment Market Segmentation

|

Attributes |

Central Line Associated Bloodstream Infection Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Central Line Associated Bloodstream Infection Treatment Market Trends

“Enhanced Focus on Antimicrobial Stewardship and Evidence-Based Infection Prevention Protocols”

- A significant and accelerating trend in the global Central Line–Associated Bloodstream Infection (CLABSI) Treatment market is the increasing emphasis on antimicrobial stewardship, improved infection-prevention bundles, and data-driven clinical decision support systems (CDSS) adopted by hospitals worldwide. These developments aim to reduce CLABSI incidence while optimizing therapeutic decisions for affected patients

- For instance, many healthcare systems have begun implementing AI-supported infection surveillance tools that analyze patient data, catheter-use practices, and microbiological profiles to help clinicians promptly detect potential bloodstream infections and initiate appropriate treatment. Such technologies enable hospitals to standardize central-line maintenance, reduce contamination risks, and support earlier therapeutic interventions for CLABSI cases

- Furthermore, updated clinical bundles—such as enhanced catheter insertion checklists, use of chlorhexidine-impregnated dressings, and antimicrobial lock solutions—are being increasingly integrated into hospital protocols to minimize infection risk. These prevention-focused strategies indirectly shape treatment-demand patterns by reducing unnecessary antibiotic use and improving patient outcomes

- The broader adoption of real-time monitoring platforms, which provide alerts for early bloodstream infection indicators (e.g., rising inflammatory markers, catheter complications), supports more accurate and timely CLABSI management. Through centralized data dashboards, clinicians can track infection rates, identify high-risk units, and ensure adherence to CDC/NHSN guidelines

- This trend toward evidence-based, technology-enabled, and prevention-oriented care pathways is reshaping hospital expectations for managing CLABSIs and improving antimicrobial selection. Consequently, major pharmaceutical and medical device companies are developing advanced antimicrobial catheter lock solutions, improved antiseptic agents, diagnostic assays, and treatment guidelines aligned with global stewardship initiatives

- The demand for CLABSI-specific treatment interventions continues to grow across hospitals and intensive-care units as medical organizations increasingly prioritize infection control, optimized antibiotic usage, and standardized central-line management frameworks

Central Line Associated Bloodstream Infection Treatment Market Dynamics

Driver

“Growing Need for Effective Treatment Due to Increasing Incidence of Hospital-Acquired Bloodstream Infections”

- The rising global burden of hospital-acquired bloodstream infections—particularly those associated with central venous catheters—is a major driver for growth in the Central Line–Associated Bloodstream Infection Treatment market. High-risk populations such as ICU patients, oncology patients, dialysis recipients, and neonates require intensive catheter-based care, increasing vulnerability to CLABSI

- For instance, in April 2025, several healthcare safety organizations emphasized updated CLABSI prevention and management guidelines, encouraging hospitals to adopt improved antimicrobial treatment strategies and surveillance systems. Such initiatives by leading clinical bodies are expected to drive the CLABSI treatment industry growth during the forecast period

- As healthcare providers worldwide become increasingly aware of CLABSI-related mortality, extended hospital stays, and rising antimicrobial resistance, there is heightened demand for more effective therapeutic options, including broad-spectrum antibiotics, antifungal therapies, and catheter-directed antimicrobial lock solutions

- Furthermore, the increasing implementation of central-line insertion in critical care, long-term intravenous therapy, parenteral nutrition, and hemodynamic monitoring has made CLABSI an unavoidable challenge for many healthcare systems. This drives the need for standardized treatment protocols, rapid diagnostics, and advanced antimicrobial therapies

- The availability of guidelines supporting timely catheter removal, targeted antibiotic therapy, and use of adjunct antiseptic/antimicrobial agents adds to the market momentum. With the rising adoption of hospital-based infection-control programs, demand for innovative CLABSI treatment products, technologies, and pharmacological options is expected to continue its upward trajectory

Restraint/Challenge

“Rising Antimicrobial Resistance and High Economic Burden of CLABSI Management”

- A major challenge hindering broader market penetration is the growing antimicrobial resistance (AMR) observed in pathogens commonly associated with CLABSI—particularly Gram-positive bacteria (e.g., MRSA), Gram-negative organisms (e.g., Pseudomonas, Klebsiella), and certain fungal species. As resistance rates rise, commonly used antibiotics may become less effective, making treatment more complex and costly

- For instance, in March 2024, the CDC reported an outbreak of multi-drug resistant Klebsiella bloodstream infections in a U.S. hospital ICU, highlighting how resistant pathogens complicate CLABSI treatment protocols and increase hospital mortality risk. In addition, high-profile scientific reports highlighting multidrug-resistant bloodstream infections have led to increased clinician caution and the need for more customized treatment regimens. These concerns make it difficult for hospitals to rely solely on standard antibiotic therapies, requiring more advanced—and often more expensive—treatment options

- Addressing AMR challenges requires the use of novel antimicrobial agents, strict adherence to stewardship practices, and regular monitoring of resistance patterns—all of which add operational burdens to healthcare providers

- Another significant barrier is the high economic cost of CLABSI management. Treating a single case can require lengthy hospital stays, additional diagnostic tests, catheter removal procedures, and combination antimicrobial therapies. These costs can be prohibitive for underfunded healthcare systems, particularly in low- and middle-income regions

- While some hospitals are adopting cost-effective approaches such as antimicrobial lock therapy and rapid diagnostic testing, the overall financial burden remains substantial

- Overcoming these challenges through the development of new antimicrobials, improved diagnostic tools, increased awareness of infection-prevention strategies, and broader healthcare investment will be essential for supporting sustainable market growth

Central Line Associated Bloodstream Infection Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, symptoms, route of administration, end-users, and distribution channel.

• By Treatment

On the basis of treatment, the Central Line Associated Bloodstream Infection market is segmented into Antibiotic, Antifungal Drugs, Supportive Therapy, and Others. The Antibiotic segment dominated the largest market revenue share of 48.5% in 2025, driven by the urgent need to treat bacterial bloodstream infections promptly and prevent sepsis complications. Broad-spectrum antibiotics are frequently administered empirically in hospitals while culture results are awaited. Hospitals rely on evidence-based antibiotic protocols to ensure optimal patient outcomes. Pediatric and adult patients with central lines benefit from standardized antibiotic regimens. Rising prevalence of multi-drug-resistant pathogens in healthcare settings increases demand for advanced antibiotic therapies. Increasing hospital admissions and ICU utilization for patients with central lines boost segment growth. Guidelines from infectious disease societies emphasize early antibiotic initiation. Adoption of combination therapy in complex cases strengthens market share. Hospitals integrate antibiotic stewardship programs to optimize therapy. High patient adherence and proven clinical efficacy further reinforce dominance. Research and development in novel antibiotics enhance pipeline availability. Overall, antibiotic therapy remains the backbone of CLABSI management.

The Supportive Therapy segment is expected to witness the fastest CAGR of 20.8% from 2026 to 2033, driven by rising adoption of interventions such as fluid resuscitation, electrolyte management, and nutritional support to stabilize critically ill patients. Supportive care improves recovery outcomes alongside primary antimicrobial therapy. Hospitals increasingly emphasize comprehensive treatment plans combining supportive and drug therapy. ICU and specialized care units are major contributors to segment growth. Pediatric and adult populations benefit from early supportive intervention. Technological advances, such as automated infusion systems, enhance precision and safety. Awareness among clinicians of sepsis management guidelines fuels adoption. Growing government and insurance coverage for supportive care contributes to revenue growth. Expanding demand in emerging economies strengthens market potential. NGOs and health programs highlight supportive therapy in infection control. Evidence-based studies validate improved survival rates with integrated supportive care. Increasing hospital investments in critical care infrastructure support rapid segment expansion.

• By Diagnosis

On the basis of diagnosis, the market is segmented into Blood Tests and Culture, Urine Tests, Sputum Tests, and Others. The Blood Tests and Culture segment dominated the largest market revenue share of 52.3% in 2025, as it is the gold standard for confirming bloodstream infections and identifying causative organisms. Routine blood cultures are essential for guiding targeted therapy. Hospitals, especially ICUs, rely on rapid microbiology labs for timely results. Pediatric and adult patients with central lines undergo repeated testing for early detection. Clinical protocols prioritize blood cultures to prevent systemic infection. Automated blood culture systems reduce time to diagnosis and improve accuracy. Integration with hospital EMR systems enhances monitoring and reporting. High adoption in tertiary and teaching hospitals supports segment leadership. Continuous medical education reinforces laboratory best practices. Global increase in catheterized patient population boosts testing frequency. Early detection reduces hospital stays and treatment costs. Laboratories increasingly adopt advanced microbial identification techniques.

The Urine Tests segment is expected to witness the fastest CAGR of 19.7% from 2026 to 2033, as concurrent urinary tract infections often accompany CLABSI cases and must be detected for comprehensive management. Rapid urinalysis and culture help prevent misdiagnosis. Hospitals increasingly integrate urine testing into routine infection surveillance protocols. Growth in hospital-acquired infection awareness programs boosts adoption. Pediatric and geriatric patients benefit from timely diagnosis. Expansion of point-of-care urine testing technology facilitates faster results. Training of nurses and clinicians enhances utilization. Development of cost-effective urine test kits in emerging economies supports growth. Standardized guidelines recommend urine tests for catheterized patients. Homecare monitoring programs also contribute to uptake. Insurance coverage for diagnostic tests ensures affordability. Overall, urine testing complements primary blood diagnostics to improve clinical outcomes.

• By Symptoms

On the basis of symptoms, the market is segmented into Chills, Fever, Rapid Heart Rate, Swelling, Redness, Drainage from Catheter Site, and Others. The Fever segment dominated the largest market revenue share of 55.1% in 2025, due to its status as the most common and early clinical indicator of CLABSI. Hospitals monitor temperature trends closely for timely intervention. Fever triggers initiation of empirical antimicrobial therapy. Pediatric and adult patients are routinely evaluated for febrile episodes. Standardized sepsis bundles incorporate fever as a critical diagnostic criterion. Integration of temperature monitoring in ICU and ward protocols supports early detection. Rapid recognition of fever reduces morbidity and hospital stay. Clinical training emphasizes fever assessment in catheterized patients. High prevalence of febrile episodes across central line patients strengthens segment dominance. Research indicates fever as a primary predictor of bloodstream infections. Hospital EMRs flag fever alerts for immediate action. Overall, fever management drives the clinical and therapeutic response.

The Drainage from Catheter Site segment is expected to witness the fastest CAGR of 21.4% from 2026 to 2033, driven by increasing emphasis on early recognition of localized infection to prevent systemic spread. Drainage is a key sign monitored by nursing staff and infection control teams. Early catheter site intervention reduces the need for systemic therapy. Training programs for healthcare providers improve detection rates. Expansion of infection prevention protocols in hospitals enhances adoption. Use of sterile dressings and observation checklists boosts segment relevance. Pediatric and adult catheterized patients benefit from early drainage management. Digital wound monitoring tools accelerate response times. Awareness campaigns for caregivers and staff improve detection. Rapid catheter site assessment reduces ICU complications. Increasing global focus on hospital-acquired infection prevention supports high growth.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral and Intravenous. The Intravenous segment dominated the largest market revenue share of 57.4% in 2025, owing to its critical role in delivering high-concentration antibiotics directly into the bloodstream for immediate therapeutic effect. IV therapy is essential for hospitalized patients, particularly those in ICUs. Pediatric and adult patients with central lines benefit from precise dosing via IV administration. Hospitals prioritize IV therapy for rapid response to bloodstream infections. Advanced infusion systems enhance safety and monitoring. Guidelines for sepsis and CLABSI management emphasize IV over oral therapy. Emergency departments and inpatient care heavily contribute to segment revenue. Continuous monitoring during IV administration improves patient outcomes. Adoption of IV-compatible antifungal agents complements antibiotic therapy. Increased hospital infrastructure investments support segment leadership. Overall, IV administration ensures effective and timely treatment of CLABSI.

The Oral segment is expected to witness the fastest CAGR of 18.9% from 2026 to 2033, driven by growing outpatient management of mild or recovering CLABSI cases. Oral antibiotics provide convenient continuation therapy post-hospitalization. Telemedicine programs support home-based oral treatment. Pediatric and adult patients increasingly receive oral therapy during convalescence. Development of long-acting oral formulations enhances adherence. Guidelines recommend oral switch therapy after stabilization on IV treatment. Awareness campaigns promote proper oral antibiotic use. Pharmaceutical companies expand oral drug availability in emerging regions. Homecare nurse support programs facilitate adherence. Reduced hospital stay and healthcare costs encourage oral therapy adoption. Overall, oral administration supports continuity of care in CLABSI management.

• By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment dominated the largest market revenue share of 61.2% in 2025, owing to the high prevalence of central line placement in inpatient settings, particularly ICUs and oncology units. Hospitals provide comprehensive diagnostic, therapeutic, and monitoring services for CLABSI patients. Pediatric and adult patients with severe infections rely heavily on hospital-based care. Multidisciplinary teams ensure coordinated management of infection, catheter care, and supportive therapies. Infection control protocols in hospitals further drive segment dominance. Hospital pharmacies ensure timely availability of IV antibiotics. Training of nursing and medical staff supports efficient CLABSI management. Expansion of tertiary and specialty hospitals enhances service coverage. Government and insurance support programs reinforce hospital-based treatment. Research initiatives for hospital-acquired infections strengthen segment relevance. High patient volume contributes to sustained revenue.

The Clinic segment is expected to witness the fastest CAGR of 19.6% from 2026 to 2033, due to rising outpatient monitoring, follow-up care, and mild infection management. Clinics provide convenient access to diagnostic testing and oral therapy. Increasing awareness among caregivers and patients promotes early consultation. Telehealth integration facilitates remote monitoring. Pediatric and adult patients with mild infections prefer clinic visits. Expansion of private clinics in emerging economies boosts growth. Training programs for outpatient infection management enhance adoption. Outpatient care reduces hospital burden. Supportive therapy and oral antibiotics are frequently managed in clinic settings. Overall, clinics play a growing role in early-stage CLABSI management.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 58.7% in 2025, due to its direct link with inpatient treatment, IV therapy administration, and immediate availability of antibiotics and supportive care drugs. Hospital pharmacies provide a controlled environment for handling high-risk medications. Pediatric and adult patients with CLABSI rely on hospital pharmacy access. Standardized stocking policies ensure uninterrupted supply. Integration with inpatient electronic records supports efficient dispensing. High prescription volumes maintain strong revenue contribution. Hospitals maintain rigorous quality control protocols. Government initiatives supporting hospital pharmacies boost market dominance. ICU and specialty unit reliance on hospital pharmacies reinforces growth. Clinical guidelines ensure prompt availability of required drugs. Research programs in hospitals further strengthen distribution networks.

The Online Pharmacy segment is expected to witness the fastest CAGR of 22.5% from 2026 to 2033, driven by increased digital adoption and growing preference for home delivery of oral antibiotics and supportive medications. Online pharmacies provide convenience for post-discharge patients. Telemedicine prescriptions facilitate online fulfillment. Pediatric and adult patients benefit from subscription-based delivery models. Expansion of e-commerce infrastructure in developing regions accelerates growth. Regulatory improvements ensure secure online drug dispensing. Cost comparison and discounts encourage patient adoption. Homecare programs integrate online pharmacy services. Rising awareness among caregivers supports utilization. Online pharmacies contribute to continuity of care for recovering CLABSI patients. Improved logistics and supply chain management enhance reliability. Digital awareness campaigns increase patient trust and usage.

Central Line Associated Bloodstream Infection Treatment Market Regional Analysis

- North America dominated the central line associated bloodstream infection treatment market with the largest revenue share of 40.60% in 2025

- Supported by advanced healthcare infrastructure, high catheter utilization, strong adoption of evidence-based infection prevention protocols, and widespread availability of specialized infectious disease management solutions

- The market experienced substantial growth due to early adoption of antimicrobial lock therapies, increased CLABSI surveillance programs, and strong investment in hospital infection-control systems

U.S. Central Line Associated Bloodstream Infection Treatment Market Insight

The U.S. central line associated bloodstream infection treatment market captured the largest revenue share within North America in 2025, driven by the increasing number of central venous catheter procedures and the implementation of hospital-wide infection prevention measures. Hospitals and specialized clinics are increasingly adopting novel antibiotic and antifungal therapies, coupled with rapid diagnostic solutions, to manage bloodstream infections effectively. Growing awareness among clinicians and hospital administrators about the clinical and economic burden of CLABSI further propels market growth.

Europe Central Line Associated Bloodstream Infection Treatment Market Insight

The Europe central line associated bloodstream infection treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent healthcare regulations, mandatory hospital infection control guidelines, and increasing investments in advanced therapeutic options. Rising awareness among healthcare providers and the growing prevalence of catheter-associated bloodstream infections in intensive care units are also fueling the adoption of targeted treatments across the region.

U.K. Central Line Associated Bloodstream Infection Treatment Market Insight

The U.K. central line associated bloodstream infection treatment market is anticipated to grow steadily during the forecast period, supported by enhanced infection surveillance systems and widespread hospital adherence to international catheter care protocols. Healthcare providers are prioritizing early detection and preventive strategies, including the use of evidence-based antibiotic regimens and specialized infection-control products, which further contribute to market expansion.

Germany Central Line Associated Bloodstream Infection Treatment Market Insight

The Germany central line associated bloodstream infection treatment market is expected to expand at a considerable CAGR, fueled by well-established healthcare infrastructure, high awareness of hospital-acquired infections, and a focus on patient safety and quality of care. Hospitals are increasingly investing in antimicrobial therapies, rapid diagnostics, and staff training programs to reduce bloodstream infection incidences, thereby driving market demand.

Asia-Pacific Central Line Associated Bloodstream Infection Treatment Market Insight

The Asia-Pacific central line associated bloodstream infection treatment market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare expenditure, rising rates of central line catheterization, and improved access to diagnostic technologies. Growing awareness among clinicians regarding early detection and effective management of bloodstream infections, alongside government initiatives to improve hospital infection-control systems, is further accelerating market growth in countries such as India, China, and Japan.

Japan Central Line Associated Bloodstream Infection Treatment Market Insight

The Japan central line associated bloodstream infection treatment market is gaining momentum due to the country’s focus on patient safety, advanced hospital infrastructure, and high procedural volumes for catheterization. Adoption of antimicrobial lock therapies, coupled with continuous monitoring and early intervention strategies, is driving the market. In addition, government-led programs emphasizing infection prevention are expected to sustain long-term growth.

China Central Line Associated Bloodstream Infection Treatment Market Insight

The China central line associated bloodstream infection treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly expanding healthcare sector, increasing prevalence of catheterization procedures, and high rates of hospital-acquired infections. The implementation of national infection-control initiatives, coupled with rising availability of specialized treatment options and improved clinical awareness, is contributing significantly to market growth.

Central Line Associated Bloodstream Infection Treatment Market Share

The Central Line Associated Bloodstream Infection Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Merck & Co., Inc. (U.S.)

- GlaxoSmithKline (U.K.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche AG (Switzerland)

- Sanofi S.A. (France)

- AbbVie Inc. (U.S.)

- Bayer AG (Germany)

- Bristol-Myers Squibb (U.S.)

- Takeda Pharmaceutical Company (Japan)

- Gilead Sciences, Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Boehringer Ingelheim GmbH (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

Latest Developments in Global Central Line Associated Bloodstream Infection Treatment Market

- In May 2024, World Health Organization (WHO) published its first global guidelines aimed at reducing bloodstream infections from catheter use. The guidelines include recommendations on aseptic insertion, maintenance, removal of catheters, hand hygiene and catheter‑selection practices — measures directly relevant to CLABSI prevention

- In April 2024, researchers published a new fully automated algorithm for surveillance of catheter‑associated bloodstream infections. The algorithm improves detection and monitoring of CLABSI, which can help healthcare institutions track infection rates faster and more reliably

- In November 2024, a systematic review and meta-analysis comparing ultrasound‑guided central venous catheter (CVC) insertion vs. landmark‑technique insertion was published. The study assessed whether ultrasound guidance lowers the risk of catheter‑related infections — offering updated evidence for safer CVC insertion method

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.