Global Ceramic Additives Market

Market Size in USD Million

USD

801.17 Million

USD

1,621.04 Million

2024

2032

USD

801.17 Million

USD

1,621.04 Million

2024

2032

| 2025 - 2032 | |

| USD 801.17 Million | |

| USD 1,621.04 Million | |

| % | |

|

Ceramic Additives Market Size

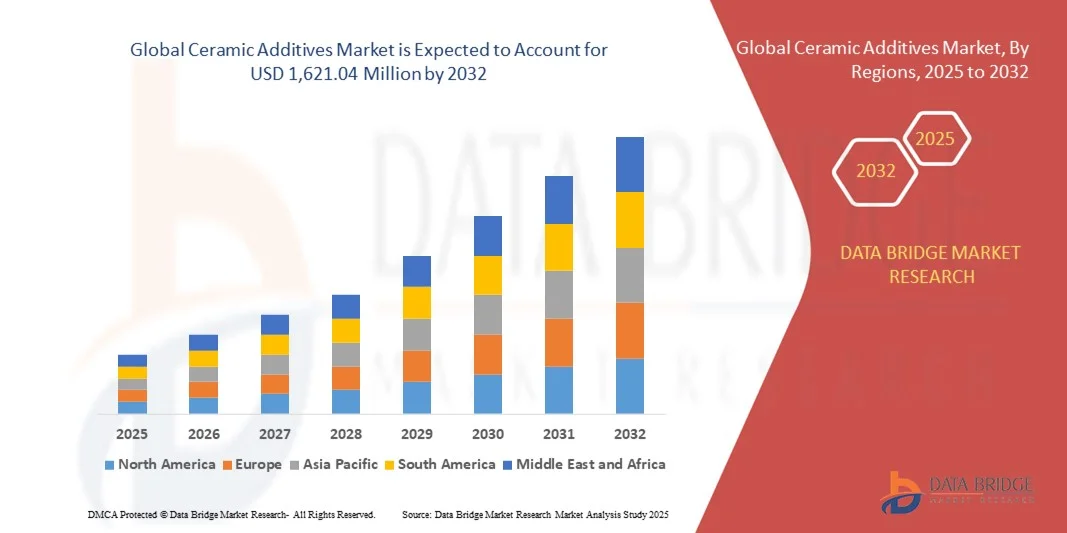

- The global ceramic additives market size was valued at USD 801.17 million in 2024 and is expected to reach USD 1,621.04 million by 2032, at a CAGR of 9.20% during the forecast period

- The market growth is largely fuelled by the rising demand for high-performance ceramics across industries such as electronics, automotive, and construction, driven by their superior mechanical strength, thermal stability, and corrosion resistance

- The growing adoption of ceramic additives in advanced manufacturing applications such as 3D printing and aerospace components is further enhancing product innovation and market expansion

Ceramic Additives Market Analysis

- The global ceramic additives market is witnessing robust growth due to increasing applications of ceramics in high-temperature environments and precision engineering processes. Additives such as binders, dispersants, and sintering aids play a crucial role in improving ceramic quality, strength, and processability

- The electronics industry remains a key consumer, particularly for components such as capacitors, insulators, and substrates, where ceramic performance is critical. Furthermore, the trend toward lightweight materials and sustainable manufacturing is driving innovation in eco-friendly ceramic formulations

- North America dominated the ceramic additives market with the largest revenue share of 39.82% in 2024, driven by the strong presence of advanced manufacturing industries such as aerospace, automotive, and electronics

- Asia-Pacific region is expected to witness the highest growth rate in the global ceramic additives market, driven by growing urbanization, rising investments in infrastructure development, and expanding electronics and automotive manufacturing bases in countries such as China, Japan, and South Korea

- The dispersant segment held the largest market revenue share in 2024, driven by its essential role in improving particle dispersion, reducing viscosity, and enhancing homogeneity during ceramic processing. Dispersants help minimize agglomeration and improve the mechanical strength and density of finished products, making them indispensable across high-performance ceramic formulations

Report Scope and Ceramic Additives Market Segmentation

|

Attributes |

Ceramic Additives Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ceramic Additives Market Trends

Rising Utilization Of Ceramic Additives In Advanced Manufacturing

- The growing adoption of ceramic additives in advanced manufacturing industries is transforming product performance and process efficiency. These additives improve strength, thermal stability, and corrosion resistance, making them essential in the production of high-performance ceramics used in electronics, automotive, and aerospace applications. The trend aligns with the global shift toward lightweight, durable, and energy-efficient materials. Furthermore, as manufacturers seek to optimize production cycles, ceramic additives play a pivotal role in minimizing waste, improving yield, and ensuring consistent quality in mass production environments

- Manufacturers are increasingly investing in additive-enhanced formulations to meet the rising demand for components capable of withstanding extreme environments. Ceramic additives enable superior sintering, reduced porosity, and improved mechanical integrity, which are critical for the next generation of functional materials used in semiconductors, sensors, and energy devices. In addition, the continuous evolution of nanotechnology and surface modification techniques is allowing for more controlled particle dispersion and enhanced bonding at the microstructural level, significantly improving material durability and precision

- The increasing use of ceramic-based 3D printing and additive manufacturing technologies is also boosting demand for ceramic additives. These additives enhance printability, improve surface finish, and ensure structural uniformity, thereby expanding their use across industries focusing on high-precision fabrication. As industries transition toward automation and digital manufacturing, ceramic additives are enabling the development of complex geometries with enhanced performance characteristics, reducing material consumption and post-processing requirements

- For instance, in 2024, several material technology firms across the U.S. and Europe incorporated zirconia and alumina additives in advanced 3D printing applications, leading to improved product consistency and extended lifespan of printed components. Such advancements are contributing to the development of customized, high-strength ceramic materials for industrial and biomedical uses. These innovations are also creating opportunities for hybrid manufacturing models, where traditional ceramics and additive manufacturing processes are seamlessly integrated to deliver superior outcomes across niche markets

- While advanced ceramics are witnessing strong demand, the cost and processing complexity of ceramic additives pose challenges. Continuous R&D, innovation in additive dispersion technologies, and scalability improvements are necessary to maximize market adoption and cost-efficiency. Strategic collaborations among material scientists, research institutions, and manufacturers are becoming increasingly important to overcome technical barriers and accelerate commercialization of advanced ceramic additive solutions

Ceramic Additives Market Dynamics

Driver

Increasing Demand For High-Performance Ceramics In Electronics And Automotive Industries

- The growing demand for high-performance ceramics in industries such as electronics and automotive is one of the major drivers for ceramic additives. Additives play a critical role in enhancing material strength, dielectric properties, and thermal resistance, enabling ceramics to meet stringent performance standards. These attributes are vital for applications in sensors, capacitors, and catalytic converters. Moreover, the ongoing shift toward miniaturized and energy-efficient devices continues to propel the need for advanced material engineering solutions enabled by ceramic additives

- The shift toward electric vehicles (EVs) and renewable energy solutions is accelerating the use of ceramic materials due to their efficiency in heat management and insulation. Ceramic additives help optimize the manufacturing process, ensuring consistent quality and mechanical performance under high stress and temperature conditions. Their application in battery components, electronic control systems, and heat shields underscores their growing importance in sustainable mobility and clean energy systems worldwide

- The miniaturization of electronic devices and the demand for advanced packaging materials are further driving the adoption of ceramic additives. Their ability to fine-tune microstructure and improve process stability makes them indispensable in modern electronic manufacturing. As demand for high-frequency communication and faster semiconductor chips grows, ceramic additives enable enhanced signal integrity and greater material reliability, ensuring long-term performance across critical applications

- For instance, in 2023, several automotive component manufacturers in Japan and Germany reported improved engine efficiency and emission control after integrating ceramic additives into catalytic systems and thermal barriers, reflecting their growing industrial importance. These developments highlight how ceramic additives contribute to energy savings, emission reduction, and environmental compliance across production chains

- While technological progress continues to drive this trend, manufacturers must focus on balancing cost, sustainability, and performance to maintain competitiveness and ensure long-term growth in the ceramic additives market. Investments in eco-friendly manufacturing techniques and recycled raw materials are gaining momentum as the industry aligns with global decarbonization goals

Restraint/Challenge

High Production Cost And Limited Availability Of Raw Materials

- The high production cost of ceramic additives, driven by complex synthesis processes and expensive raw materials such as alumina, zirconia, and silica, remains a major restraint for the market. These costs often lead to higher end-product prices, limiting adoption among small and mid-sized manufacturers. Moreover, the energy-intensive nature of ceramic processing further contributes to elevated operational expenses. To mitigate this, manufacturers are exploring low-temperature sintering technologies and alternative raw material sources to enhance affordability

- The limited availability of high-purity raw materials and supply chain disruptions have caused fluctuations in material pricing and hindered consistent production. Dependence on specific mining sources and the environmental impact of extraction activities continue to challenge sustainability efforts within the industry. Furthermore, geopolitical tensions and trade restrictions have exacerbated raw material shortages, prompting companies to diversify sourcing and adopt circular material recovery models

- In several developing economies, a lack of advanced manufacturing infrastructure and skilled personnel further restricts large-scale production and integration of ceramic additives into high-value applications. This slows market penetration and innovation, particularly in cost-sensitive regions. Government incentives and skill development programs are essential to strengthen industrial capacity and promote the widespread use of ceramic technologies in emerging markets

- For instance, in 2023, European manufacturers reported production slowdowns due to supply shortages of zirconium compounds and rising energy costs, resulting in extended lead times and increased product pricing. These disruptions have encouraged companies to invest in regional supply networks and renewable energy-based ceramic production to stabilize operations

- To overcome these challenges, market participants are focusing on the development of cost-effective additive formulations, sustainable sourcing strategies, and recycling initiatives aimed at improving resource efficiency and supply chain stability. Collaborative research programs and industry alliances are playing a vital role in addressing cost pressures while ensuring consistent supply and innovation across the ceramic additives landscape

Ceramic Additives Market Scope

The market is segmented on the basis of additive type, application, and end use.

- By Additive Type

On the basis of additive type, the ceramic additives market is segmented into dispersant, binder, lubricant, enhancer, grinding aid, water reducing agent, and others. The dispersant segment held the largest market revenue share in 2024, driven by its essential role in improving particle dispersion, reducing viscosity, and enhancing homogeneity during ceramic processing. Dispersants help minimize agglomeration and improve the mechanical strength and density of finished products, making them indispensable across high-performance ceramic formulations.

The enhancer segment is expected to witness the fastest growth rate from 2025 to 2032, fuelled by its ability to improve the physical and thermal properties of advanced ceramics used in electronics and automotive components. Enhancers contribute to optimizing sintering behavior, increasing thermal conductivity, and enhancing corrosion resistance, making them highly valuable for next-generation industrial ceramics.

- By Application

On the basis of application, the ceramic additives market is segmented into architecture, automotive, and industrial. The industrial segment held the largest market share in 2024, owing to the extensive use of ceramic additives in manufacturing advanced materials for electronics, energy, and aerospace applications. Additives play a crucial role in achieving precision, performance consistency, and durability in industrial ceramics that operate under extreme conditions.

The automotive segment is expected to witness the fastest growth rate from 2025 to 2032, supported by the increasing use of ceramic components in engines, exhaust systems, and EV batteries. Ceramic additives enhance the performance and longevity of these components by improving wear resistance, heat tolerance, and structural integrity, aligning with the industry's shift toward high-efficiency and low-emission vehicles.

- By End Use

On the basis of end use, the ceramic additives market is segmented into tiles, sanitary ware, tableware, and technical ceramics. The tiles segment accounted for the largest market share in 2024, attributed to the widespread demand for ceramic tiles in residential and commercial construction. Additives are extensively used to improve glaze quality, reduce cracking, and enhance surface finish, leading to higher aesthetic and functional value.

The technical ceramics segment is projected to witness the fastest growth from 2025 to 2032, driven by their expanding application in semiconductors, medical devices, and aerospace components. Ceramic additives improve mechanical strength, purity, and temperature stability in technical ceramics, supporting their growing use in high-precision and high-performance environments.

Ceramic Additives Market Regional Analysis

- North America dominated the ceramic additives market with the largest revenue share of 39.82% in 2024, driven by the strong presence of advanced manufacturing industries such as aerospace, automotive, and electronics

- The region’s focus on innovation, energy efficiency, and sustainable production methods is accelerating the adoption of ceramic additives to enhance material performance and process reliability

- In addition, continuous R&D investments and collaboration between research institutions and manufacturers are promoting technological advancements across end-use sectors

U.S. Ceramic Additives Market Insight

The U.S. ceramic additives market captured the largest revenue share in 2024 within North America, supported by the country’s leadership in high-performance materials and precision manufacturing. Growing demand from aerospace and defense sectors for lightweight, heat-resistant ceramics is a key factor driving market growth. Moreover, the increasing integration of ceramic materials in electronic devices and electric vehicles (EVs) is fuelling the need for additives that enhance strength, thermal stability, and processing efficiency.

Europe Ceramic Additives Market Insight

The Europe ceramic additives market is projected to experience significant growth from 2025 to 2032, driven by stringent environmental standards and a rising preference for eco-friendly materials. The region’s strong industrial base in countries such as Germany, France, and the U.K. supports the development and adoption of high-performance ceramics. Furthermore, the push toward energy-efficient manufacturing processes and sustainable construction materials continues to strengthen market potential across Europe.

Germany Ceramic Additives Market Insight

The Germany ceramic additives market is anticipated to record notable growth from 2025 to 2032, supported by the country’s technological leadership in engineering and advanced manufacturing. The growing use of ceramic materials in electronics, automotive components, and renewable energy systems is driving the adoption of performance-enhancing additives. Moreover, Germany’s commitment to sustainable production and innovation in ceramic processing technologies further bolsters its market position.

Asia-Pacific Ceramic Additives Market Insight

The Asia-Pacific ceramic additives market is expected to witness the fastest growth rate from 2025 to 2032, fuelled by rapid industrialization, expanding construction activities, and rising demand for consumer goods. Countries such as China, Japan, and India are emerging as major production hubs due to cost-effective manufacturing and easy availability of raw materials. In addition, government programs promoting digitalization and infrastructure development are further driving market demand.

China Ceramic Additives Market Insight

The China ceramic additives market accounted for the largest revenue share in the Asia-Pacific region in 2024, owing to strong domestic manufacturing capabilities and a rapidly expanding construction and electronics sector. The country’s large-scale production of raw materials, coupled with its growing focus on high-performance and energy-efficient materials, continues to drive market growth. In addition, China’s position as a leading exporter of ceramic products supports sustained demand for additives.

Japan Ceramic Additives Market Insight

The Japan ceramic additives market is expected to experience robust growth from 2025 to 2032, driven by the increasing adoption of advanced ceramics in electronics, semiconductors, and precision manufacturing. Japanese industries are focusing on innovation, product miniaturization, and high durability, which require high-quality ceramic additives. Furthermore, Japan’s emphasis on environmentally friendly materials and cutting-edge production technologies strengthens its global competitiveness.

Ceramic Additives Market Share

The Ceramic Additives industry is primarily led by well-established companies, including:

• 3DCeram (France)

• AGC Inc. (Japan)

• BioCote Limited (U.K.)

• BASF SE (Germany)

• CARBO Ceramics Inc. (U.S.)

• ENVISIONTEC INC (U.S.)

• EOS (Germany)

• ExOne (U.S.)

• Lamberti S.p.A (Italy)

• MakerBot Industries, LLC (U.S.)

• Materialise (Belgium)

• Novabeans Prototyping Labs LLP (India)

• Optomec, Inc. (U.S.)

• SANYO CHEMICAL INDUSTRIES, LTD. (Japan)

• Johnson Matthey (U.K.)

• Wöllner GmbH (Germany)

• Bentonite Performance Minerals, LLC (U.S.)

• Ferro Corporation (U.S.)

• Stratasys Ltd (U.S.)

• XJet (Israel)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Ceramic Additives Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Ceramic Additives Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Ceramic Additives Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.