Global Cheek Depression Injectable Fillers Market

Market Size in USD Million

USD

461.97 Million

USD

949.58 Million

2025

2033

USD

461.97 Million

USD

949.58 Million

2025

2033

| 2026 - 2033 | |

| USD 461.97 Million | |

| USD 949.58 Million | |

| % | |

|

Cheek Depression Injectable Fillers Market Size

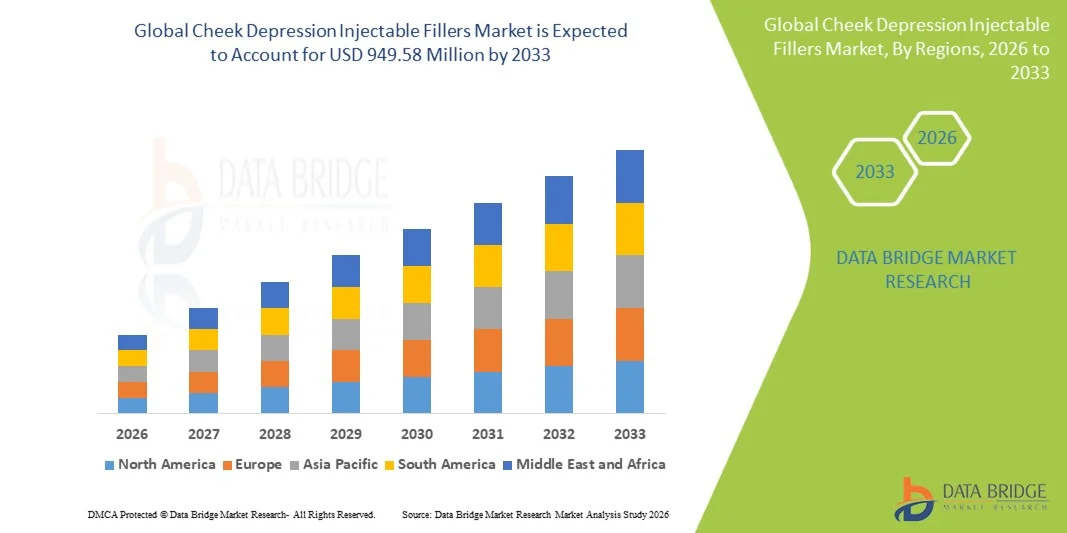

- The global cheek depression injectable fillers market size was valued at USD 461.97 Million in 2025 and is expected to reach USD 949.58 Million by 2033, at a CAGR of 9.42% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced cosmetic procedures and technological innovations in injectable filler formulations, leading to greater availability and effectiveness in both clinical and aesthetic settings

- Furthermore, rising consumer demand for minimally invasive, safe, and effective facial enhancement solutions is establishing Cheek Depression Injectable Fillers as the preferred treatment option. These converging factors are accelerating the uptake of Cheek Depression Injectable Fillers solutions, thereby significantly boosting the industry's growth

Cheek Depression Injectable Fillers Market Analysis

- Cheek Depression Injectable Fillers, offering minimally invasive or non-surgical correction of facial volume loss, are increasingly vital in aesthetic and reconstructive procedures due to their ability to restore facial contours, enhance symmetry, and provide natural-looking results

- The escalating demand for cheek depression injectable Fillers is primarily fueled by growing awareness of cosmetic procedures, increasing consumer focus on facial aesthetics, and rising preference for non-surgical facial enhancement solutions

- North America dominated the cheek depression injectable Fillers market with the largest revenue share of 41% in 2025, characterized by high disposable incomes, well-established aesthetic clinics, and the presence of key industry players, with the U.S. experiencing substantial growth driven by innovations in filler formulations, safety enhancements, and increasing adoption of non-surgical cosmetic procedures

- Asia-Pacific is expected to be the fastest-growing region in the cheek depression injectable fillers market during the forecast period due to rising awareness of aesthetic treatments, growing middle-class population, and increasing availability of injectable filler products in countries such as China, Japan, and India

- The non-surgical segment accounted for the largest revenue share of 49.3% in 2025, driven by the rising popularity of injectable fillers for cheek depression due to minimal downtime and low risk. Patients prefer quick aesthetic improvements without hospitalization

Report Scope and Cheek Depression Injectable Fillers Market Segmentation

|

Attributes |

Cheek Depression Injectable Fillers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Cheek Depression Injectable Fillers Market Trends

“Enhanced Focus on Minimally Invasive Aesthetic Treatments”

- A significant and accelerating trend in the global cheek depression injectable fillers market is the growing adoption of minimally invasive procedures for facial contouring and volume restoration. This trend is driven by patient preference for treatments with minimal downtime and reduced risk compared to surgical options

- For instance, clinics and dermatology centers are increasingly offering advanced hyaluronic acid-based fillers that provide natural mid-face volume enhancement and long-lasting results, catering to the rising demand for non-surgical aesthetic solutions

- The introduction of precision injection techniques and cannula-based delivery systems is improving procedural safety, minimizing bruising, and ensuring consistent and predictable outcomes for patients

- Patients are seeking customizable treatment plans, allowing tailored volume restoration and cheek contouring according to individual facial anatomy and aesthetic goals

- The use of combination treatments, including dermal fillers with skin boosters or biostimulatory agents, is becoming more common to achieve holistic facial rejuvenation

- Awareness campaigns by aesthetic practitioners, influencers, and social media platforms are driving patient interest in cheek depression correction, making injectable fillers a preferred choice for facial enhancement

- Technological advances in filler formulations, such as longer-lasting, cross-linked hyaluronic acids, are attracting both clinicians and patients to invest in high-quality, minimally invasive treatments

Cheek Depression Injectable Fillers Market Dynamics

Driver

“Increasing Demand for Minimally Invasive Cosmetic Procedures”

- The rising awareness about facial aesthetics and anti-aging solutions is a major driver for the Cheek Depression Injectable Fillers market

- For instance, in June 2024, Allergan Aesthetics launched a new line of cheek volumizing fillers designed specifically to correct cheek depressions and enhance mid-face contour, offering longer-lasting and natural results

- Patients are preferring injectable fillers over surgical options due to lower risks, quicker recovery, and immediate visual improvement, boosting adoption in aesthetic clinics and dermatology centers

- Rising disposable incomes and greater accessibility of cosmetic procedures in emerging markets are further contributing to market growth

- Training programs for dermatologists and cosmetic practitioners on advanced filler techniques are improving procedural safety and patient confidence

- The increasing number of aesthetic clinics and medical chains offering minimally invasive facial treatments is expanding the reach of cheek depression injectable fillers globally

Restraint/Challenge

“Concerns Regarding Safety, Side Effects, and Cost”

- Potential side effects, such as bruising, swelling, asymmetry, and rare allergic reactions, can limit adoption in certain patient groups

- For instance, in October 2023, several European clinics reported temporary patient hesitancy due to mild post-injection swelling and erythema, highlighting the importance of skilled practitioners for optimal outcomes

- The relatively high cost of premium fillers, particularly those with advanced formulations offering long-lasting and natural results, can be a barrier for price-sensitive consumers

- Regulatory approvals and compliance with regional medical standards can delay the introduction of new injectable fillers, affecting market expansion

- Integration of advanced filler products into clinical practice requires staff training and patient education, which can slow adoption rates

- Overcoming these challenges requires safe, effective formulations, trained practitioners, and awareness campaigns to educate patients about benefits, side effects, and expected outcomes

Cheek Depression Injectable Fillers Market Scope

The market is segmented on the basis of type, application area, end-user, and procedure type.

• By Type

On the basis of type, the Cheek Depression Injectable Fillers market is segmented into hyaluronic acid, calcium hydroxylapatite, poly-L-lactic acid, polymethylmethacrylate (PMMA), autologous fat, and others. The hyaluronic acid segment dominated the market with a revenue share of 41.5% in 2025, driven by its high biocompatibility, minimal invasiveness, and reversibility. It is widely used for mid-face volumization, facial contouring, and malar enhancement, making it highly preferred by aesthetic practitioners globally. The growing number of dermatology and aesthetic clinics offering hyaluronic acid-based treatments, along with increased patient awareness and demand for non-surgical procedures, further strengthens its market position. In addition, its versatility across multiple facial areas, including malar, tear trough, and nasolabial folds, contributes to its dominance. Technological advancements in hyaluronic acid formulations, such as cross-linking for longer-lasting results, also fuel its widespread adoption. Marketing campaigns highlighting safety and efficacy enhance patient confidence, encouraging repeat procedures. The segment benefits from strong support by leading filler manufacturers and increasing reimbursement options in some regions.

The poly-L-lactic acid segment is expected to witness the fastest CAGR of 18.3% from 2026 to 2033. Its growth is driven by its unique ability to stimulate collagen production gradually, offering natural-looking, long-term facial volumization. Rising popularity among younger demographics seeking subtle and preventive rejuvenation is contributing to adoption. Increasing use in aesthetic clinics and dermatology centers, along with expanding training for physicians in poly-L-lactic acid injection techniques, supports market growth. The product’s extended duration and patient satisfaction enhance repeat treatment rates. Marketing efforts emphasizing longevity and natural results are further boosting demand. Technological innovations in injection devices and formulations improve safety and comfort. Poly-L-lactic acid’s versatility across malar, jawline, and nasolabial areas increases applicability. The expanding number of minimally invasive procedures globally supports rapid adoption. Growing awareness through social media and online campaigns fuels patient demand. Its compatibility with other fillers enhances combinational treatment approaches. Increasing clinical studies validating efficacy further strengthen confidence among practitioners and patients.

• By Application Area

On the basis of application area, the market is segmented into malar region, nasolabial fold, tear trough, jawline, and others. The malar region segment held the largest revenue share of 36.7% in 2025, driven by high patient demand for mid-face volumization and youthful facial contouring. Aging populations seeking correction of cheek sagging and hollowing support market dominance. Non-surgical enhancement is preferred over surgical alternatives due to lower risk, faster recovery, and cost-effectiveness. Dermatology and aesthetic clinics promote malar treatments extensively, driving patient adoption. The widespread use of hyaluronic acid and calcium hydroxylapatite fillers in this area strengthens its position. Social media influence and cosmetic trends promoting high cheekbones further contribute to growth. Increasing disposable incomes and urbanization, especially in North America and Europe, boost market uptake. Clinical innovations enabling natural results with minimal downtime increase patient preference. The availability of advanced injection techniques improves safety and outcome predictability. Marketing campaigns and celebrity endorsements enhance consumer awareness. Rising medical tourism in countries offering cost-effective procedures fuels adoption. The segment benefits from strong physician recommendation networks.

The tear trough segment is projected to grow at the fastest CAGR of 17.5% from 2026 to 2033. Demand is driven by increasing awareness of non-surgical treatments for under-eye hollows, dark circles, and facial fatigue. Younger demographics and millennials increasingly seek aesthetic rejuvenation in subtle areas. Adoption of hyaluronic acid fillers, combined with improved techniques for minimal bruising, supports growth. Increasing availability of treatment in dermatology and aesthetic clinics globally accelerates uptake. Social media trends emphasizing refreshed eyes boost patient interest. Repeat treatments due to predictable and satisfactory outcomes drive sustained revenue. Clinics focus marketing on tear trough correction as a high-demand procedure. Technological advances in microcannulas and filler formulations enhance safety and precision. Patient preference for minimally invasive, outpatient procedures fuels rapid adoption. Expansion in emerging markets with rising disposable income supports CAGR. Growing physician training and awareness of tear trough procedures improve treatment outcomes. Positive patient reviews and word-of-mouth referrals further increase adoption.

• By End-User

On the basis of end-user, the market is segmented into hospitals, aesthetic clinics, dermatology clinics, and ambulatory surgical centers. Aesthetic clinics dominated the market with a revenue share of 44.2% in 2025, owing to their specialization in cosmetic procedures and availability of trained professionals. Clinics provide personalized consultation and treatment plans, which enhance patient confidence and repeat procedures. High patient traffic, marketing initiatives, and brand recognition strengthen their market dominance. The concentration of advanced injectable technologies in aesthetic clinics increases procedure efficiency and results. Their ability to offer combined aesthetic services such as botulinum toxin, fillers, and skincare treatments enhances appeal. Urban centers with higher disposable incomes favor clinic-based procedures. Patient preference for non-hospital settings for privacy and convenience further contributes. Aesthetic clinics often leverage digital marketing and social media to attract younger clients. Training programs for practitioners and clinical research partnerships enhance procedural credibility. The segment benefits from rapid adoption in North America, Europe, and parts of Asia-Pacific. Collaboration with cosmetic product manufacturers supports high service quality.

Ambulatory surgical centers are expected to witness the fastest CAGR of 16.8% from 2026 to 2033. Their growth is fueled by the cost-effectiveness, shorter waiting times, and convenience offered to patients. Centers specialize in minimally invasive treatments and provide flexible scheduling, appealing to working professionals. Increasing number of outpatient centers equipped with advanced filler technologies supports rapid adoption. Patient preference for privacy and individualized care enhances demand. Expansion in tier-2 and tier-3 cities increases accessibility. Collaboration with dermatologists and aesthetic professionals promotes adoption. Centers capitalize on preventive and early aesthetic interventions. Marketing campaigns highlighting comfort and efficiency attract patients. Technological advancements in equipment and filler delivery improve patient satisfaction. Regulatory support and accreditation of ambulatory centers build trust among clients. The increasing number of procedures performed per center enhances revenue generation.

• By Procedure Type

On the basis of procedure type, the market is segmented into non-surgical, minimally invasive, and surgical. The non-surgical segment accounted for the largest revenue share of 49.3% in 2025, driven by the rising popularity of injectable fillers for cheek depression due to minimal downtime and low risk. Patients prefer quick aesthetic improvements without hospitalization. The dominance is supported by the wide availability of hyaluronic acid fillers and trained practitioners. Marketing efforts promoting non-surgical options increase awareness. Non-surgical procedures are offered at aesthetic clinics and dermatology centers extensively. The segment benefits from social media influence and cosmetic trends advocating non-invasive enhancements. Repeat procedures to maintain results drive recurring revenue. Lower treatment costs compared to surgical alternatives boost accessibility. Safety profiles and minimal side effects further strengthen adoption. Patient preference for outpatient treatments fuels growth. Clinics emphasize personalized, quick, and reliable procedures. Increasing urban patient population seeking aesthetic improvements contributes.

Minimally invasive procedures are expected to record the fastest CAGR of 15.9% during 2026–2033. Growth is driven by advancements in filler delivery techniques, precision instruments, and hybrid approaches combining multiple products. Rising awareness of procedures that are effective yet less invasive than traditional surgery attracts patients. Clinics are adopting techniques ensuring safety, comfort, and predictable outcomes. Technological innovation in cannulas and micro-injections improves procedural accuracy. Marketing campaigns highlight reduced downtime and natural-looking results. Patient preference for gradual correction and early intervention boosts adoption. Training programs for practitioners ensure proper technique and enhance trust. Expanding availability across urban and semi-urban centers increases reach. Repeat sessions for maintenance of aesthetic results contribute to revenue. Positive patient experiences and word-of-mouth referrals strengthen market traction. Regulatory approvals for newer minimally invasive devices further support growth.

Cheek Depression Injectable Fillers Market Regional Analysis

- North America dominated the cheek depression injectable fillers market with the largest revenue share of 41% in 2025

- Characterized by high disposable incomes, well-established aesthetic clinics, and the presence of key industry players

- The market is witnessing substantial growth driven by innovations in filler formulations, improved safety profiles, and increasing adoption of non-surgical cosmetic procedures for cheek volume enhancement and facial contouring

U.S. Cheek Depression Injectable Fillers Market Insight

The U.S. cheek depression injectable fillers market captured the largest revenue share within North America in 2025, fueled by growing consumer preference for minimally invasive cosmetic treatments. Rising awareness of aesthetic procedures, coupled with the availability of advanced injectable fillers and professional training among clinicians, is supporting market expansion.

Europe Cheek Depression Injectable Fillers Market Insight

The Europe cheek depression injectable fillers market is projected to expand at a healthy CAGR during the forecast period, driven by rising demand for facial rejuvenation procedures, a strong presence of aesthetic clinics, and increasing acceptance of injectable fillers across the region. Countries such as Germany, France, and Italy are witnessing significant adoption due to technological advancements in filler formulations and growing consumer awareness.

U.K. Cheek Depression Injectable Fillers Market Insight

The U.K. cheek depression injectable fillers market is expected to grow steadily during the forecast period, propelled by increasing consumer interest in non-surgical facial enhancement. Enhanced safety standards, availability of premium fillers, and the expansion of cosmetic clinics across urban centers are contributing to market growth.

Germany Cheek Depression Injectable Fillers Market Insight

The Germany cheek depression injectable fillers market is anticipated to expand at a notable CAGR, supported by well-established healthcare and aesthetic infrastructure, heightened consumer awareness of facial aesthetics, and the increasing availability of technologically advanced filler products. The market is also benefiting from training programs for aesthetic practitioners.

Asia-Pacific Cheek Depression Injectable Fillers Market Insight

The Asia-Pacific cheek depression injectable fillers market is expected to register the fastest CAGR during the forecast period, driven by rising awareness of aesthetic treatments, growing middle-class population, and increased availability of injectable filler products. Markets in China, Japan, and India are witnessing strong adoption due to expanding aesthetic clinics, urbanization, and rising disposable incomes.

Japan Cheek Depression Injectable Fillers Market Insight

The Japan cheek depression injectable fillers market is gaining traction due to increasing consumer interest in facial rejuvenation and minimally invasive procedures. High safety standards, advanced filler formulations, and a growing number of cosmetic clinics are supporting steady market growth.

China Cheek Depression Injectable Fillers Market Insight

The China cheek depression injectable fillers market accounted for the largest revenue share in Asia-Pacific in 2025. Growth is driven by the expanding middle-class population, rising aesthetic awareness, and strong adoption of advanced injectable fillers in both urban clinics and emerging cities, supported by increasing investments in cosmetic and dermatology infrastructure.

Cheek Depression Injectable Fillers Market Share

The Cheek Depression Injectable Fillers industry is primarily led by well-established companies, including:

- Revance Therapeutics (U.S.)

- Hugel, Inc. (South Korea)

- MediTox (South Korea)

- Ipsen (France)

- Croma-Pharma (Austria)

- Sinclair Pharma (U.K.)

- Daewoong Pharmaceutical (South Korea)

- Luminera (Israel)

- Mentor (U.S.)

- Galderma (Switzerland)

- Teoxane (Switzerland)

- Kythera Biopharmaceuticals (U.S.)

- Evolus (U.S.)

- Dermal Korea (South Korea)

Latest Developments in Global Cheek Depression Injectable Fillers Market

- In June 2021, Restylane Contour, developed by Galderma, received U.S. FDA approval for cheek augmentation and correction of mid‑face contour deficiencies, marking its first indication for the cheeks in the U.S., using the proprietary XpresHAn technology

- In January 2023, Galderma announced at IMCAS its long‑term data from the Sculptra cheek wrinkle study, demonstrating high aesthetic improvement, strong patient satisfaction, and effective cheek contour correction over 24 months

- In August 2023, SEDY FILL was launched by Maypharm as a hyaluronic acid dermal filler specifically developed for non‑surgical body shape correction, including facial volumization and contouring—highlighting the broader innovation around cheek and mid‑face fillers

- In May 2024, Skinvive (a hyaluronic acid‑based intradermal micro‑droplet injection) was launched in the U.S., indicated to improve skin smoothness of the cheeks across all Fitzpatrick skin types—an aesthetic innovation focusing on texture rather than volume

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.