Global Chronic Disease Management Technology Market

Market Size in USD Billion

USD

7.21 Billion

USD

15.01 Billion

2025

2033

USD

7.21 Billion

USD

15.01 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.21 Billion | |

| USD 15.01 Billion | |

| % | |

|

Chronic Disease Management Technology Market Overview

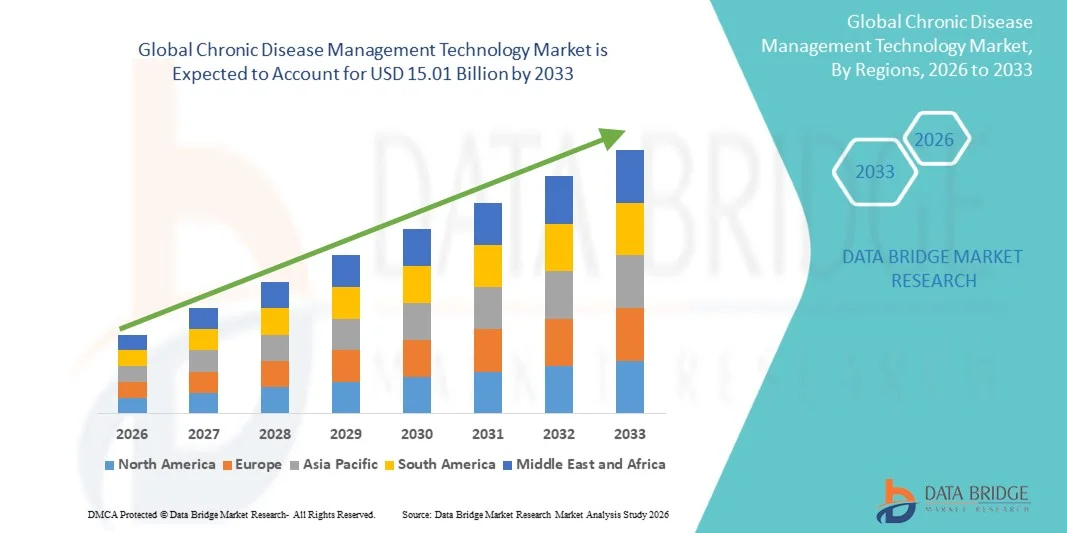

The global chronic disease management technology market was valued at USD 7.21 billion in 2025 and is projected to reach USD 15.01 billion by 2033, growing at a CAGR of 9.6% from 2026 to 2033. The market is experiencing steady growth driven by the rising global burden of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions, along with increasing adoption of digital health platforms, remote patient monitoring systems, and AI-enabled care management solutions.

The growing shift toward value-based healthcare, combined with the need to reduce hospital readmissions and long-term treatment costs, is encouraging healthcare providers, insurers, and government agencies to deploy advanced chronic care management technologies. Integration of wearable devices, mobile health applications, and cloud-based analytics is further enhancing real-time patient monitoring and personalized care delivery, making these solutions a key component of modern healthcare ecosystems.

Key Market Trends & Insights

- North America dominated the global chronic disease management technology market with the largest revenue share of 42.9% in 2025, supported by advanced healthcare infrastructure, high adoption of digital health platforms, and strong reimbursement support for remote patient monitoring services.

- The Cloud-Based segment led the market with a 68.4% share in 2025, driven by rapid digital transformation in healthcare systems and increasing adoption of remote patient monitoring platforms

- Asia-Pacific is expected to be the fastest-growing region, registering a CAGR of 12% from 2026 to 2033, fueled by growing chronic disease burden, rapid healthcare digitalization, and increasing telehealth investments across China, India, and Japan.

- On-Premises are the fastest-growing delivery mode type, projected to register a CAGR of 16.2%, reflecting the surge in large hospitals, government healthcare systems, and organizations with strict data privacy requirements.

- The Implementation Services segment dominated the services category with a 39.8% revenue share in 2025, led by increasing need for deployment, configuration, and integration of chronic disease management platforms within hospital ecosystems.

- Diabetes accounted for 33.1% of the market, preferred by high global prevalence and continuous need for glucose monitoring, medication adherence, and lifestyle management.

- The Consulting Services segment is the fastest-growing services category, with a CAGR of 14.3%, driven by rising complexity in healthcare digitization and increasing focus on value-based care models.

Market Size & Forecast

- Global Market Value (2025): USD 7.21 Billion

- Expected Market Value (2033): USD 15.01 Billion

- Forecast CAGR (2026–2033): 9.6%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Global Chronic Disease Management Technology Market Segmentation

|

Attributes |

Chronic Disease Management Technology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Epic Systems Corporation (U.S.) · Allscripts Healthcare Solutions, Inc. (U.S.) · NextGen Healthcare, Inc. (U.S.) · eClinicalWorks, LLC (U.S.) · athenahealth, Inc. (U.S.) · Greenway Health, LLC (U.S.) · Cerner Corporation (U.S.) · Meditech (U.S.) · McKesson Corporation (U.S.) · Siemens Healthineers AG (Germany) · Koninklijke Philips N.V. (Netherlands) · IBM Corporation (U.S.) · Oracle Corporation (U.S.) · Cognizant Technology Solutions Corporation (U.S.) · Infosys Limited (India) · Optum, Inc. (U.S.) · Health Catalyst, Inc. (U.S.) · Pegasystems Inc. (U.S.) · GE HealthCare (U.S.) · Medtronic (Ireland) |

|

Market Opportunities |

· Expansion of AI-driven predictive care platforms enabling early detection of disease deterioration · Growing integration of wearable-enabled continuous monitoring ecosystems · Rising adoption of value-based healthcare programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Global Chronic Disease Management Technology Market Trends

Trend: Shift Toward Remote and Continuous Patient Monitoring Ecosystems

Healthcare providers are increasingly adopting integrated chronic care platforms that combine remote patient monitoring, mobile health applications, and wearable devices to enable continuous tracking of patient health outside clinical settings. These systems support real-time data collection for conditions such as diabetes, cardiovascular diseases, and respiratory disorders, allowing earlier intervention and improved long-term disease control. The expansion of cloud-based healthcare infrastructure and interoperable digital health records is enabling seamless data exchange between patients, providers, and payers, improving care coordination and treatment adherence. For instance, large-scale RPM deployments in post-discharge cardiac care programs in the U.S. and Europe have significantly reduced readmission rates through continuous glucose and heart rate monitoring integration.

Global Chronic Disease Management Technology Market Dynamics

Key Market Driver: Rising Global Burden of Chronic Diseases and Shift to Value-Based Care

The increasing prevalence of chronic diseases, driven by aging populations, sedentary lifestyles, and lifestyle-related risk factors, is significantly increasing demand for long-term disease management solutions. Healthcare systems are transitioning toward value-based care models that prioritize patient outcomes over service volume, encouraging adoption of digital platforms that reduce hospital readmissions and overall treatment costs. Governments, insurers, and healthcare providers are investing in chronic care management technologies to improve population health outcomes and optimize resource utilization across healthcare networks. For instance, Medicare-led chronic care management reimbursement programs in the U.S. have accelerated adoption of digital care coordination platforms among primary care providers.

Key Restraint/Challenge: Data Privacy, Interoperability, and Regulatory Complexity

A major challenge in the chronic disease management technology market is the complexity of managing sensitive patient data across multiple digital platforms while ensuring compliance with stringent healthcare data privacy regulations. Lack of standardized interoperability between electronic health records, wearable devices, and third-party applications often leads to fragmented care delivery and inefficiencies in data sharing. In addition, varying regulatory frameworks across regions create compliance burdens for solution providers, slowing down large-scale deployment and integration in some healthcare systems.

For instance, differences in HIPAA (U.S.) and GDPR (Europe) compliance requirements often complicate cross-border deployment of unified chronic care platforms by global health-tech vendors.

Key Market Opportunity: Expansion of AI-Driven Predictive and Personalized Chronic Care Platforms

The integration of artificial intelligence and predictive analytics presents a significant market opportunity by enabling early risk detection, personalized treatment planning, and proactive disease intervention. AI-powered platforms can analyze large volumes of patient-generated health data to identify deterioration patterns and recommend timely clinical actions. The growing adoption of cloud-based chronic care ecosystems and digital therapeutics is further expanding opportunities for scalable, data-driven healthcare delivery models across developed and emerging markets. For instance, AI-enabled diabetes management platforms using continuous glucose monitoring data are increasingly being deployed by digital health companies to provide personalized insulin dosing recommendations and lifestyle interventions.

Global Chronic Disease Management Technology Market Scope

The chronic disease management technology market is segmented on the basis of delivery mode, services, disease type, and end user.

- By Delivery Mode

On the basis of delivery mode, the global chronic disease management technology market is segmented into cloud-based and on-premises solutions. The Cloud-Based segment dominated the market with a 68.4% share in 2025, driven by rapid digital transformation in healthcare systems and increasing adoption of remote patient monitoring platforms. Cloud-based systems enable real-time data access, seamless integration with wearable devices, and interoperability with EHR/EMR systems. Healthcare providers prefer these solutions due to lower infrastructure costs and high scalability across multi-location networks. They also support AI-driven predictive analytics for early detection and intervention in chronic conditions. The rise of telehealth and mobile health applications has further strengthened adoption. Their flexibility and accessibility make them the backbone of modern chronic disease management ecosystems.

The On-Premises segment the fastest growing, expanding at a CAGR of 16.2% from 2026–2033, primarily adopted by large hospitals, government healthcare systems, and organizations with strict data privacy requirements. These solutions offer greater control over patient data and internal IT infrastructure, which is critical in highly regulated environments. However, high capital expenditure and limited scalability reduce their competitiveness compared to cloud systems. Upgrading and integrating advanced analytics tools is also more complex in on-premises setups. Despite these limitations, they remain relevant in legacy healthcare IT environments. Their adoption is gradually declining as healthcare providers transition toward cloud-first strategies.

- By Services

On the basis of services, the market is segmented into educational services, implementation services, consulting services, and others. The Implementation Services segment dominated the market with a 39.8% share in 2025, driven by the increasing need for deployment, configuration, and integration of chronic disease management platforms within hospital ecosystems. Healthcare providers depend on implementation services to connect digital health tools with EHR systems, wearable devices, and telehealth platforms. These services ensure smooth workflow integration and reduce operational disruptions during digital transformation. Growing adoption of population health management systems further strengthens demand. Implementation remains essential for ensuring system efficiency and usability across clinical settings. It continues to generate the highest revenue contribution among service segments.

The Consulting Services segment is the fastest growing, expanding at a CAGR of 14.3% from 2026–2033, driven by rising complexity in healthcare digitization and increasing focus on value-based care models. Healthcare organizations require expert advisory support for AI integration, data analytics strategies, and regulatory compliance. Consulting services also help in designing long-term chronic care management strategies and optimizing patient engagement models. The shift toward preventive healthcare and population health management is further accelerating demand. Organizations are increasingly seeking guidance to maximize ROI from digital health investments. This segment is expanding rapidly as healthcare systems transition toward outcome-driven care delivery.

- By Disease Type

On the basis of disease type, the market is segmented into cardiovascular diseases (CVD), diabetes, arthritis, asthma, cancer, and others. The Diabetes segment dominated the market with a 33.1% share in 2025, owing to its high global prevalence and continuous need for glucose monitoring, medication adherence, and lifestyle management. Digital diabetes management platforms are widely integrated with wearable glucose monitors and mobile health applications. Strong patient engagement requirements make diabetes a key application area for chronic care technologies. Government initiatives for diabetes prevention and control further support market dominance. Continuous disease progression necessitates long-term digital monitoring solutions. This ensures sustained demand across global healthcare systems.

The Cancer segment is the fastest growing, projected to expand at a CAGR of 15.6% from 2026–2033, driven by rising oncology cases and increasing adoption of digital cancer care platforms. Cancer management requires highly coordinated, long-term monitoring, making it ideal for chronic disease technologies. AI-enabled analytics and precision medicine tools are increasingly used for personalized treatment planning. Hospitals and oncology centers are adopting remote monitoring systems to enhance survivorship care. Expanding investments in cancer treatment infrastructure are further accelerating growth. Digital integration across chemotherapy, radiology, and post-care pathways is expanding rapidly.

- By End User

On the basis of end user, the market is segmented into healthcare providers, healthcare payers, and others. The Healthcare Providers segment dominated the market with a 54.7% share in 2025, as hospitals, clinics, and ambulatory care centers are the primary users of chronic disease management platforms. Providers rely on these systems for patient monitoring, care coordination, and clinical decision support. Increasing chronic disease burden globally has made efficient digital care delivery essential. Integration with EHR systems, telehealth platforms, and AI-based analytics further strengthens adoption. Healthcare providers remain the central execution point for chronic disease management workflows. Their dominant role in patient care ensures continued market leadership.

The Healthcare Payers segment is the fastest growing, expanding at a CAGR of 13.9% from 2026–2033, driven by the shift toward value-based reimbursement models and cost containment strategies. Insurance companies are increasingly adopting digital health platforms to reduce hospitalization rates and long-term treatment costs. These systems enable predictive risk assessment, preventive care, and population health management. Collaboration between payers and technology providers is expanding rapidly. The growing focus on reducing healthcare expenditure while improving outcomes is boosting adoption. This segment is evolving quickly as payers take a more active role in chronic disease management ecosystems.

Global Chronic Disease Management Technology Market Regional Analysis

North America dominated the global chronic disease management technology market with the largest revenue share of 42.9% in 2025, supported by advanced healthcare infrastructure, high adoption of digital health platforms, and strong reimbursement support for remote patient monitoring services. The region benefits from a high prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer, driving continuous demand for remote patient monitoring and care coordination solutions. Strong presence of leading health-tech companies, favorable reimbursement frameworks, and rapid expansion of telehealth services further accelerate market growth. Increasing investments in AI-driven analytics, wearable devices, and population health management platforms continue to strengthen North America’s leadership position in the global market.

U.S. Chronic Disease Management Technology Market Insight

The United States dominated the chronic disease management technology market and accounted for the largest revenue share in 2025, driven by a highly advanced healthcare IT ecosystem, strong digital health adoption, and widespread integration of EHR/EMR systems across healthcare providers. The country has a high prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer, which continues to fuel demand for remote patient monitoring and digital care management solutions. Strong presence of leading health-tech companies and continuous investment in AI-enabled analytics and wearable health technologies further strengthen market expansion. Favorable reimbursement structures and rapid adoption of telehealth services are also accelerating deployment across hospitals and payer organizations. In addition, increasing focus on value-based care and population health management is enhancing long-term adoption of chronic disease management platforms.

Europe Chronic Disease Management Technology Market Insight

Europe remains a key contributor to the chronic disease management technology market, driven by well-established public healthcare systems, increasing digital health transformation, and rising focus on preventive and value-based care models. The region benefits from strong adoption of interoperable healthcare platforms and expanding integration of chronic care solutions across hospitals and primary care networks. High prevalence of lifestyle-related chronic conditions is further supporting demand for continuous monitoring and care coordination tools. Growing investments in AI-enabled clinical decision support systems and remote patient management platforms are enhancing healthcare efficiency. Continuous government initiatives promoting digital health adoption continue to support steady market expansion across Europe.

Germany Chronic Disease Management Technology Market Insight

The Germany chronic disease management technology market is expanding steadily, supported by a strong healthcare infrastructure, advanced medical research capabilities, and increasing adoption of digital health solutions across hospitals and clinics. The country benefits from a high burden of chronic diseases and a strong emphasis on preventive healthcare strategies. Germany’s healthcare system is increasingly integrating interoperable digital platforms to improve patient monitoring and care coordination. Growing investments in AI-based healthcare analytics and remote monitoring technologies are further supporting market growth. In addition, strong government focus on digital transformation and healthcare innovation is accelerating adoption of chronic disease management technologies across the country.

United Kingdom Chronic Disease Management Technology Market Insight

The United Kingdom chronic disease management technology market is witnessing consistent growth due to strong public healthcare digitization under the NHS framework and increasing adoption of remote care solutions. Rising prevalence of chronic conditions and aging population are key factors driving demand for continuous monitoring systems. The UK is actively promoting digital health transformation through national health data platforms and telehealth expansion. Integration of AI-driven clinical tools and mobile health applications is improving patient engagement and care efficiency. Furthermore, strong focus on reducing hospital burden and improving preventive care outcomes continues to support market expansion.

Asia Pacific Chronic Disease Management Technology Market Insight

The Asia-Pacific chronic disease management technology market is expected to witness the fastest growth, driven by rapid healthcare infrastructure development, increasing chronic disease burden, and strong adoption of mobile health and telemedicine platforms. Countries such as China, India, and Japan are investing heavily in digital healthcare ecosystems and AI-based health monitoring systems. Rising government initiatives focused on expanding healthcare accessibility and improving preventive care are further accelerating adoption. Increasing penetration of smartphones and wearable devices is supporting real-time patient engagement and remote monitoring. Expanding participation of global health-tech companies is also strengthening market penetration across the region.

China Chronic Disease Management Technology Market Insight

The China chronic disease management technology market is growing rapidly, driven by increasing urbanization, rising chronic disease burden, and strong government support for digital healthcare transformation. The country is investing heavily in AI-enabled healthcare systems, mobile health platforms, and large-scale hospital digitization programs. Expanding adoption of wearable devices and remote patient monitoring solutions is significantly improving chronic disease management capabilities. Growing awareness of preventive healthcare and increasing healthcare accessibility are further accelerating demand. In addition, strong participation of domestic health-tech companies is positioning China as one of the fastest-growing markets globally.

Japan Chronic Disease Management Technology Market Insight

The Japan chronic disease management technology market is witnessing steady growth due to a rapidly aging population, high prevalence of chronic illnesses, and strong focus on advanced healthcare technologies. The country is widely adopting digital health platforms, robotics, and AI-based monitoring systems to improve patient care efficiency. Hospitals and research institutes are increasingly using remote monitoring tools for long-term disease management. Strong integration of wearable health technologies and telemedicine platforms is further enhancing adoption. In addition, Japan’s emphasis on precision healthcare and preventive care strategies continues to support market expansion.

Global Chronic Disease Management Technology Market Share

The Chronic Disease Management Technology industry is primarily led by well-established companies, including:

- Epic Systems Corporation (U.S.)

- Allscripts Healthcare Solutions, Inc. (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- eClinicalWorks, LLC (U.S.)

- athenahealth, Inc. (U.S.)

- Greenway Health, LLC (U.S.)

- Cerner Corporation (U.S.)

- Meditech (U.S.)

- McKesson Corporation (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- Cognizant Technology Solutions Corporation (U.S.)

- Infosys Limited (India)

- Optum, Inc. (U.S.)

- Health Catalyst, Inc. (U.S.)

- Pegasystems Inc. (U.S.)

- GE HealthCare (U.S.)

- Medtronic (Ireland)

Latest Developments in Global Chronic Disease Management Technology Market

- In April 2026, El Salvador expanded its AI-driven chronic disease management system powered by Google’s Gemini model, enabling large-scale monitoring of patients with conditions such as diabetes and hypertension. The platform supports real-time symptom tracking, automated clinical assessment, and virtual consultations to improve long-term disease management outcomes. It also provides AI-based recommendations for diagnostics and treatment pathways, strengthening early intervention capabilities. The system has been scaled to serve over a million users, highlighting national-level deployment of AI in healthcare. This initiative demonstrates the growing integration of generative AI into population-scale chronic care delivery systems

- In February 2026, India strengthened its AI-driven healthcare ecosystem by expanding chronic disease detection and management initiatives through advanced research programs at IISc Bengaluru. These initiatives focus on early identification of non-communicable diseases such as diabetes, cancer, and cardiovascular conditions using machine learning models. The system is designed to assist healthcare workers in risk stratification and clinical decision support at scale. Integration with digital health platforms is improving accessibility in rural and underserved regions. This development highlights India’s growing emphasis on AI-enabled preventive healthcare infrastructure

- In September 2025, global healthcare systems accelerated adoption of AI-enabled telemedicine platforms for chronic disease management, particularly for diabetes and cardiovascular conditions. These platforms support continuous remote monitoring, automated patient triage, and personalized treatment recommendations. The integration of AI has improved efficiency in managing long-term patient care outside hospital settings. This shift has been driven by rising chronic disease prevalence and increased demand for home-based care solutions. It reflects a broader global transition toward digital-first chronic care delivery models

- In March 2025, the chronic disease management technology market witnessed increased consolidation, with healthtech companies acquiring digital diabetes and remote care platforms to build integrated care ecosystems. These acquisitions focus on combining AI analytics, wearable integration, and remote monitoring into unified chronic care solutions. The trend is driven by the need to reduce fragmentation in digital health services. It is also improving interoperability between patient monitoring systems and clinical workflows. This consolidation reflects the maturation of the global digital chronic disease management ecosystem

- In December 2024, the UK National Health Service introduced a breakthrough AI-based tool capable of predicting type 2 diabetes risk up to 13 years in advance using ECG data. The system identifies early physiological markers linked to metabolic disorders, enabling preventive intervention before disease onset. It is being tested as part of NHS digital transformation initiatives aimed at reducing chronic disease burden. The tool represents a shift from reactive treatment to predictive chronic disease management. It is expected to significantly improve long-term population health outcomes in the UK healthcare system

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.