Global Chylomicronemia Market

Market Size in USD Billion

USD

500.50 Billion

USD

739.46 Billion

2024

2032

USD

500.50 Billion

USD

739.46 Billion

2024

2032

| 2025 - 2032 | |

| USD 500.50 Billion | |

| USD 739.46 Billion | |

| % | |

|

Chylomicronemia Market Size

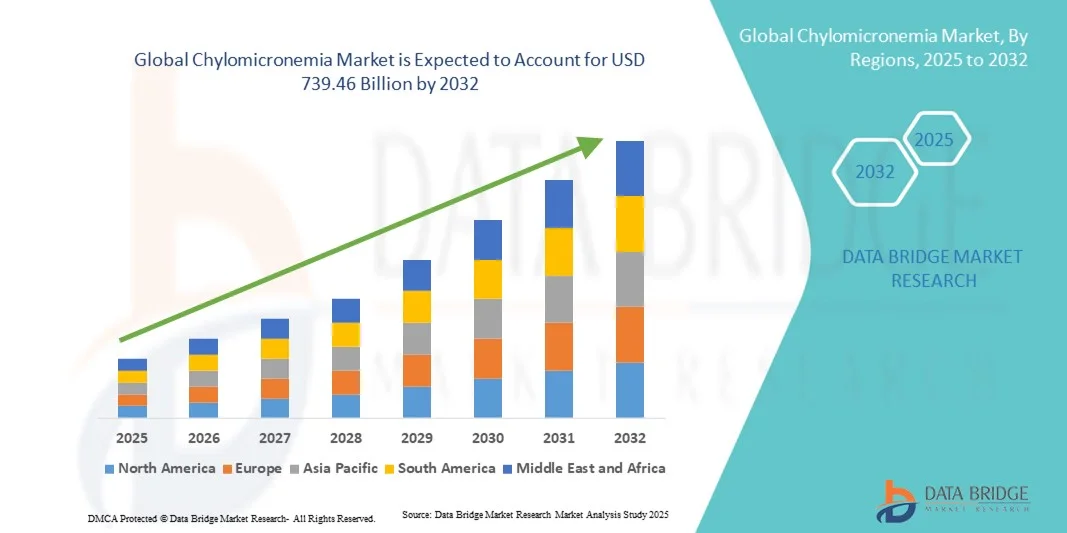

- The global chylomicronemia market size was valued at USD 500.5 billion in 2024 and is expected to reach USD 739.46 billion by 2032, at a CAGR of 5.00% during the forecast period

- The market growth is largely fueled by the rising prevalence of severe hypertriglyceridemia and chylomicronemia syndrome, along with increasing awareness of rare lipid disorders. Advances in genetic testing, lipid profiling, and early diagnosis are driving the identification of patients, which in turn is increasing the demand for effective therapeutic and management solutions for chylomicronemia

- Furthermore, the development of novel therapies, including antisense oligonucleotides, gene therapy, and lipid-lowering agents, is accelerating the uptake of chylomicronemia treatment solutions. Growing collaborations between pharmaceutical companies, research institutions, and rare disease advocacy groups are facilitating innovation and improving patient access, thereby significantly boosting the growth of the chylomicronemia market

Chylomicronemia Market Analysis

- The Chylomicronemia market is witnessing significant growth due to the increasing prevalence of severe hypertriglyceridemia and familial chylomicronemia syndrome, rising awareness of rare lipid disorders, and advancements in diagnostics such as genetic testing and lipid profiling. Improved patient identification and early intervention are driving the adoption of therapies and management solutions across global healthcare systems.

- Furthermore, the market is fueled by the development of innovative therapies, including antisense oligonucleotides, gene therapy, fibrates, and novel lipid-lowering agents. Strategic collaborations between pharmaceutical companies, research institutions, and patient advocacy groups are accelerating treatment innovation and accessibility, thereby significantly boosting the overall market growth

- North America dominated the chylomicronemia market with the largest revenue share of 42.3% in 2024, driven by high healthcare expenditure, strong presence of key pharmaceutical players, widespread adoption of advanced diagnostics, and robust clinical research infrastructure. The U.S. remains the leading country in the region, supported by early adoption of novel therapies and reimbursement policies for rare disease treatments

- Asia-Pacific is expected to be the fastest-growing region in the chylomicronemia market during the forecast period (2025–2032), with a CAGR of 9.1%, owing to growing awareness of rare lipid disorders, increasing healthcare spending, improving diagnostic facilities, and expanding patient access to innovative therapies, particularly in Japan, China, and India

- The Blood Test segment dominated the largest market revenue share of 53.1% in 2024, as fasting lipid panels and triglyceride measurements remain the first-line diagnostic tools for detecting chylomicronemia

Report Scope and Chylomicronemia Market Segmentation

|

Attributes |

Chylomicronemia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Chylomicronemia Market Trends

Rising Awareness and Focus on Early Diagnosis

- A significant and accelerating trend in the global chylomicronemia market is the increasing awareness among patients, healthcare providers, and policymakers regarding early detection and management of lipid metabolism disorders. This trend is driving improvements in screening programs and access to specialized treatment

- For instance, several leading hospitals and research centers are introducing comprehensive lipid profile screening protocols to identify high-risk patients at an earlier stage. Such initiatives facilitate timely intervention and improved patient outcomes

- The emphasis on early diagnosis enables healthcare providers to adopt personalized treatment strategies, monitor triglyceride levels more effectively, and reduce the risk of acute pancreatitis associated with chylomicronemia

- Governments and non-profit organizations are also launching awareness campaigns and educational programs to highlight the importance of lifestyle management, dietary regulation, and adherence to treatment, further supporting market growth

- This trend towards proactive disease management is fostering innovation in therapeutic approaches, diagnostic testing, and patient monitoring, shaping the expectations of healthcare providers and patients alike

- The growing availability of advanced diagnostics and improved clinical guidance is expected to accelerate the adoption of effective chylomicronemia treatment strategies across regions

Chylomicronemia Market Dynamics

Driver

Increasing Prevalence of Genetic Lipid Disorders and Growing Therapeutic Advancements

- The rising prevalence of rare lipid disorders such as familial chylomicronemia syndrome (FCS) is a primary driver of the Chylomicronemia market. Enhanced awareness among physicians and patients is facilitating early diagnosis and treatment initiation

- For instance, in 2024, key pharmaceutical companies advanced novel therapies targeting lipoprotein lipase deficiencies and associated triglyceride metabolism abnormalities, providing better patient outcomes and improved management options. Such developments are expected to accelerate market growth over the forecast period

- Healthcare providers are increasingly adopting a combination of pharmacological interventions, dietary modifications, and lifestyle counseling to manage triglyceride levels effectively

- Growing investments in R&D for rare lipid disorders are leading to the development of targeted therapies, gene therapies, and supportive care solutions, expanding the market scope

- The increasing availability of clinical trial programs, patient support initiatives, and reimbursement policies is also propelling adoption across hospitals, specialty clinics, and diagnostic centers

Restraint/Challenge

High Treatment Costs and Limited Access to Specialized Care

- High costs associated with novel pharmacological therapies, gene therapies, and advanced diagnostic testing pose a significant challenge for broader market penetration. Many patients in developing regions may not have access to specialized care or expensive treatment options

- For instance, in 2023, a study published in the Journal of Clinical Lipidology highlighted that patients with familial chylomicronemia syndrome (FCS) in Southeast Asia had limited access to enzyme replacement therapies due to prohibitive costs and lack of reimbursement

- The limited availability of lipid metabolism specialists and tertiary care centers in certain geographies further restricts access to optimal disease management

- Ensuring equitable patient access requires policy support, improved insurance coverage, and broader healthcare infrastructure investments. Companies and healthcare providers are increasingly focusing on patient assistance programs and partnerships with government initiatives to overcome these barriers

- While technological advancements in diagnostics and therapeutics are reducing disease complications, the perceived high cost and limited availability of certain therapies may continue to hinder adoption in some regions

- Addressing these challenges through improved healthcare infrastructure, awareness campaigns, and cost-effective treatment solutions will be crucial to sustain long-term market growth

Chylomicronemia Market Scope

The market is segmented on the basis of treatment, diagnosis, symptoms, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Chylomicronemia market is segmented into dietary counseling, gene therapy, triglyceride-lowering agents, Waylivra, and others. The Triglyceride-lowering agents segment dominated the largest market revenue share of 46.3% in 2024, driven by their well-established efficacy in reducing plasma triglyceride levels and preventing acute pancreatitis. These agents, including fibrates and omega-3 fatty acids, are widely prescribed and reimbursed across major markets. Frequent monitoring and dose adjustments lead to repeated prescriptions, adding sustained revenue streams. The broad clinical familiarity among endocrinologists and lipid specialists ensures high adoption rates. The availability of combination therapies enhances patient adherence and outcomes. Pharmaceutical innovation continues to improve efficacy and safety profiles, supporting market dominance. Insurance coverage and guideline recommendations further reinforce their widespread use. Triglyceride-lowering agents remain a cornerstone in chronic management strategies for familial chylomicronemia syndrome. They also facilitate integration with other supportive care measures like dietary counseling. The segment benefits from mature distribution channels and long-standing clinical protocols. Clinical trials focusing on novel agents expand treatment options within this category. These factors collectively secure the highest revenue share for triglyceride-lowering agents in 2024.

The Gene Therapy segment is anticipated to witness the fastest CAGR of 21.4% from 2025 to 2032, propelled by the development of targeted therapies that address the underlying genetic causes of chylomicronemia. Clinical trials for novel gene-editing platforms are showing promising early results in normalizing lipid metabolism. The potential for a one-time curative intervention makes gene therapy highly attractive for patients and investors. Expansion of compassionate use programs and orphan drug incentives is accelerating adoption. Regulatory agencies in North America and Europe are providing expedited pathways for these therapies, further driving growth. Collaborations between biotech firms and academic centers are increasing pipeline robustness. Manufacturing scale-up and improved vector delivery technologies are improving accessibility. Patient advocacy groups are raising awareness, encouraging earlier diagnosis and treatment uptake. Gene therapy’s potential to reduce lifelong treatment costs supports reimbursement discussions. The high unmet need in severe cases ensures sustained market interest. Ongoing R&D and positive trial outcomes continue to drive investor confidence and projected CAGR.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests and molecular genetic testing. The Blood Test segment dominated the largest market revenue share of 53.1% in 2024, as fasting lipid panels and triglyceride measurements remain the first-line diagnostic tools for detecting chylomicronemia. Routine blood tests are easily accessible, cost-effective, and widely adopted by clinics and hospitals globally. High prevalence of repeated monitoring in chronic management ensures consistent demand. Integration of blood testing in preventive and family-screening programs reinforces its clinical relevance. Standardized protocols and laboratory infrastructure support reliability and scalability. Blood tests are often used as baseline metrics to guide treatment efficacy and adjustments. Regular monitoring is crucial for patients on triglyceride-lowering agents or dietary interventions. The convenience and non-invasiveness of blood tests drive patient compliance. Blood testing also facilitates early identification of high-risk individuals and secondary prevention strategies. The combination of cost-effectiveness, clinical reliability, and repeated usage solidifies its dominant market position.

The Molecular Genetic Testing segment is expected to witness the fastest CAGR of 22.0% from 2025 to 2032, driven by increasing awareness of familial chylomicronemia syndrome and the growing need for precise diagnosis. Advances in next-generation sequencing allow rapid identification of pathogenic variants in the LPL and related genes. Early genetic diagnosis enables tailored therapeutic strategies, including eligibility for gene therapy trials. Expansion of genetic counseling and population-screening programs is increasing adoption. Rising investment in molecular diagnostics and decreasing costs are improving accessibility. Personalized medicine initiatives and regulatory support for rare disease testing are further accelerating growth. Genetic testing is increasingly integrated into specialized lipid clinics and tertiary care centers. Patient advocacy and educational programs enhance awareness of testing benefits. Molecular testing’s precision, coupled with its role in disease stratification, makes it the fastest-growing diagnostic segment.

- By Symptoms

On the basis of symptoms, the market is segmented into xanthomas, hepatosplenomegaly, lipemia retinalis, depression, memory loss, and others. The Xanthomas segment dominated the largest market revenue share of 38.7% in 2024, due to their visible presentation and role as a clinical trigger for early diagnosis. Xanthomas often prompt specialist referral and lipid panel testing, generating diagnostic and treatment demand. Their presence serves as a biomarker for disease severity and therapeutic monitoring. Recurrent manifestations can require dermatological management and procedural interventions. Clinical recognition of xanthomas contributes to prompt therapeutic initiation and reduces complications such as pancreatitis. Patient and caregiver awareness also enhance early medical consultation. The frequency of xanthomas in familial chylomicronemia syndrome makes it a consistent clinical feature. Integration with guideline-based management ensures standardized care pathways. Longitudinal patient follow-ups contribute to healthcare resource utilization and market activity.

The Depression segment is expected to witness the fastest CAGR of 19.3% from 2025 to 2032, driven by increased recognition of neuropsychiatric impacts associated with chronic metabolic disorders. Growing awareness of mental health in rare disease populations is driving screening and management efforts. Psychiatric intervention, counseling, and pharmacotherapy are increasingly incorporated into holistic patient care. Telepsychiatry and integrated clinic models improve access to mental health services. Clinical studies highlighting quality-of-life improvements with psychiatric care encourage wider adoption. The burden of chronic disease and frequent hospital visits makes mental health support essential. Insurance coverage expansion for mental health treatments is further fueling growth. Awareness campaigns and patient advocacy are promoting early recognition and management. Integration with multidisciplinary care strengthens the adoption of psychiatric interventions.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, diagnostic centres, and others. The Hospitals segment dominated the largest market revenue share of 47.5% in 2024, owing to their role as primary centers for diagnosis, treatment, and ongoing management of chylomicronemia. Hospitals provide access to triglyceride-lowering therapies, gene therapy programs, and multidisciplinary care. Tertiary hospitals facilitate rare disease clinics and clinical trial participation, concentrating high-value services. Complex interventions, such as lipid apheresis or advanced therapies, are largely hospital-based. Reimbursement frameworks often favor hospital-administered care. Hospitals serve as hubs for integrated care, including dietary counseling, genetic testing, and psychiatric support. High patient volumes and referral networks reinforce their market dominance. Centers of excellence and specialized lipid units further centralize treatment, sustaining revenue streams.

The Diagnostic Centres segment is expected to witness the fastest CAGR of 20.2% from 2025 to 2032, due to expanded capacity for biochemical and genetic testing. Standalone diagnostic facilities are increasingly partnering with hospitals to provide accessible screening and monitoring. Investments in high-throughput molecular platforms and automated testing improve turnaround times. Outpatient monitoring, family screening, and early detection programs enhance patient engagement. Tele-diagnostics and remote reporting models are further accelerating adoption. Cost efficiency, scalability, and specialization make diagnostic centers the fastest-growing end-user segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 52.4% in 2024, as most specialized therapies, including triglyceride-lowering agents and investigational gene therapies, are administered under hospital supervision. High-value medications, inpatient monitoring, and integrated care pathways concentrate procurement in hospital pharmacies. Contracts, bulk purchasing, and specialized compounding further reinforce dominance. The critical nature of therapy initiation and follow-up ensures continued market concentration in hospitals.

The Online Pharmacy segment is expected to witness the fastest CAGR of 23.5% from 2025 to 2032, fueled by digital healthcare adoption and increasing patient preference for home delivery of chronic medications. E-pharmacy platforms provide wider access to triglyceride-lowering drugs and supportive care products, including specialty medications. Integration with telemedicine and e-prescription systems streamlines repeat dispensing. Regulatory support for online sales of rare disease medications and improved logistics, including cold-chain management, enhance accessibility. Partnerships between pharmaceutical companies and e-pharmacy providers further accelerate market growth. Convenience, geographic reach, and cost efficiency drive the rapid expansion of online pharmacy channels through 2032.

Chylomicronemia Market Regional Analysis

- North America dominated the chylomicronemia market with the largest revenue share of 42.3% in 2024, driven by high healthcare expenditure, strong presence of key pharmaceutical players, widespread adoption of advanced diagnostics, and robust clinical research infrastructure

- The market remains the leading country in the region, supported by early adoption of novel therapies and favorable reimbursement policies for rare disease treatments

- This widespread adoption is further reinforced by the availability of specialized treatment centers, advanced laboratories, and a strong network of clinical research institutions focusing on rare lipid disorders

U.S. Chylomicronemia Market Insight

The U.S. chylomicronemia market captured the largest revenue share in North America in 2024, fueled by advanced healthcare infrastructure, widespread availability of specialized treatment centers, and ongoing development of innovative therapies targeting familial chylomicronemia syndrome (FCS) and other rare lipid disorders.

Europe Chylomicronemia Market Insight

The Europe chylomicronemia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of rare lipid disorders and the adoption of advanced treatment protocols. The region benefits from stringent healthcare regulations, established clinical networks, and improved access to tertiary care centers. Significant growth is observed across hospitals, specialty clinics, and diagnostic centers in countries such as Germany, France, and the U.K.

U.K. Chylomicronemia Market Insight

The U.K. chylomicronemia market is expected to grow at a noteworthy CAGR during the forecast period, supported by national rare disease initiatives, access to cutting-edge therapies, and a strong emphasis on early diagnosis and treatment. Increased healthcare funding and patient support programs are further stimulating market growth.

Germany Chylomicronemia Market Insight

The Germany chylomicronemia market is anticipated to expand at a considerable CAGR during the forecast period, driven by increasing awareness among healthcare professionals, well-developed medical infrastructure, and the availability of advanced therapeutic options. Germany’s focus on innovation and sustainability in healthcare promotes the adoption of novel treatment regimens for rare lipid disorders.

Asia-Pacific Chylomicronemia Market Insight

The Asia-Pacific chylomicronemia market is projected to grow at the fastest CAGR of 9.1% during the forecast period (2025–2032), driven by rising awareness of rare lipid disorders, increasing healthcare spending, improving diagnostic facilities, and expanding patient access to innovative therapies. Rapid urbanization, government healthcare initiatives, and growing adoption of novel treatment options in countries such as China, Japan, and India are key factors propelling market growth.

Japan Chylomicronemia Market Insight

The Japan chylomicronemia market is gaining momentum due to increasing disease awareness, advanced healthcare infrastructure, and government support for rare disease treatment programs. The availability of specialized lipid clinics and expansion of clinical research is further driving growth.

China Chylomicronemia Market Insight

The China chylomicronemia market accounted for the largest revenue share within Asia-Pacific in 2024, attributed to government-backed rare disease programs, rapid expansion of tertiary hospitals, and technological upgrades in diagnostic and laboratory facilities. The increasing availability of innovative therapies and strong domestic pharmaceutical manufacturing capabilities are significantly contributing to the market’s expansion.

Chylomicronemia Market Share

The Chylomicronemia industry is primarily led by well-established companies, including:

- Ionis Pharmaceuticals, Inc. (U.S.)

- Arrowhead Pharmaceuticals, Inc. (U.S.)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Sanofi (France)

- Boehringer Ingelheim International GmbH (Germany)

- Akcea Therapeutics, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Roche Holding AG (Switzerland)

- Novartis AG (Switzerland)

- Amgen Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- MedDay Pharmaceuticals (France)

Latest Developments in Global Chylomicronemia Market

- In February 2024, Olezarsen (brand name Tryngolza) received Orphan Drug designation from the U.S. Food and Drug Administration (FDA) for the treatment of adults with familial chylomicronemia syndrome (FCS). This designation highlighted the high unmet need in this rare metabolic disorder and provided incentives for accelerated development and regulatory support

- In September 2024, Arrowhead Pharmaceuticals announced that its investigational therapy Plozasiran had successfully met primary and key secondary endpoints in a Phase 3 clinical trial for FCS. The positive trial results demonstrated significant reduction in plasma triglyceride levels and marked improvement in patient-reported outcomes, positioning the therapy as a promising new option for this rare disease population

- In December 2024, the FDA approved Olezarsen (Tryngolza) as the first-ever therapy in the United States specifically for adults with FCS, to be used in conjunction with a low-fat diet. This approval represented a historic milestone, offering patients a targeted treatment option that addresses the underlying lipid abnormalities and reduces the risk of acute pancreatitis

- In November 2024, Arrowhead Pharmaceuticals announced that the FDA had accepted its New Drug Application (NDA) for Plozasiran in FCS, with a PDUFA action date set for November 18, 2025. This acceptance marked a significant regulatory milestone, reflecting the agency’s acknowledgment of the therapy’s potential to meet critical unmet medical needs in patients suffering from severe hypertriglyceridemia associated with FCS

- In July 2025, the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency (EMA) issued a positive opinion recommending Olezarsen for EU approval. This step indicated a likely expansion of the therapy’s availability to European patients and underscored global recognition of its clinical benefits in managing FCS

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.