Global Circular Connectors Market

Market Size in USD Billion

USD

6.52 Billion

USD

9.63 Billion

2025

2033

USD

6.52 Billion

USD

9.63 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.52 Billion | |

| USD 9.63 Billion | |

| % | |

|

Circular Connectors Market Overview

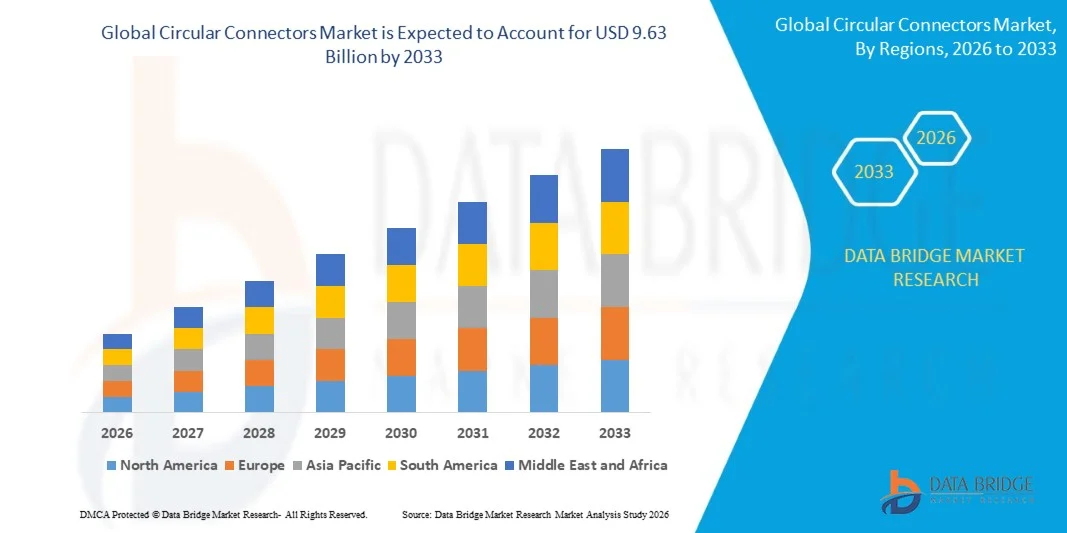

The Circular Connectors Market was valued at USD 6.52 billion in 2025 and is projected to reach USD 9.63 billion by 2033, growing at a CAGR of 5.00% from 2026 to 2033. The market is experiencing steady growth driven by increasing demand for reliable and rugged connectivity solutions, rapid expansion of industrial automation and smart manufacturing systems, and growing adoption across aerospace, defense, transportation, telecommunications, and medical equipment applications.

The increasing need for secure data transmission and uninterrupted power connectivity in harsh operating environments is encouraging manufacturers to deploy advanced circular connector solutions with enhanced durability, environmental sealing, and high-performance capabilities. Circular connectors are increasingly replacing conventional connection systems in mission-critical applications due to their compact design, vibration resistance, ease of installation, and ability to support high-speed data and power transmission. Growing investments in Industry 4.0 infrastructure, electric vehicles, renewable energy systems, and next-generation communication networks are further accelerating market adoption, creating significant opportunities for connector manufacturers worldwide.

Key Market Trends & Insights

- North America dominated the circular connectors market with the largest revenue share of approximately 35.2% in 2025, supported by strong aerospace and defense spending, rapid industrial automation adoption, and widespread integration of advanced electronic systems across critical infrastructure and telecommunications networks.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 6.2% from 2026 to 2033. Growth is driven by rapid industrialization, expanding electronics manufacturing, increasing investments in smart cities and telecom infrastructure, and rising demand for cost-effective and high-performance connectivity solutions across automotive, industrial, and consumer electronics sectors.

- The Circular Metal Shell Connectors (CMSC) segment held the largest market revenue share of approximately 45%–50% in 2025 driven by its extensive use in defense systems, industrial machinery, and aerospace applications. CMSC connectors are widely preferred due to their high durability, superior shielding capability, and strong resistance to harsh environmental conditions, making them suitable for mission-critical connectivity applications.

- The RF Connectors segment is projected to register the fastest growth at a CAGR of 11.2% from 2026 to 2033, driven by rising deployment in 5G infrastructure, satellite communications, and high-frequency signal transmission systems. Increasing demand for high-speed, low-loss connectivity in telecom networks and advanced electronic systems is further accelerating segment expansion.

- The medium pin count segment held the largest market revenue share of approximately 40%–45% in 2025 driven by its balanced performance, cost efficiency, and widespread adoption across industrial automation, railways, and consumer electronics applications. Medium pin connectors are preferred due to their versatility in supporting both power and signal transmission requirements across multiple systems.

- The high pin count segment is projected to register the fastest growth at a CAGR of 10.5% from 2026 to 2033, driven by increasing demand for complex electronic systems in defense platforms, aerospace avionics, and advanced medical equipment where higher data density and multi-function connectivity are required.

- The male connectors segment accounted for the largest market revenue share of approximately 52%–55% in 2025 driven by its extensive use as plug interfaces in industrial and military-grade systems. Male connectors are widely used due to their structural compatibility and ease of integration in modular connection architectures.

- The female connectors segment is projected to grow at the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing demand for secure receptacle-based connectivity solutions in high-vibration environments such as railways, power plants, and aerospace systems.

- The MIL-Spec connectors segment held the largest market revenue share of approximately 48%–52% in 2025 driven by strong adoption in defense, aerospace, and critical communication systems. These connectors are preferred due to their rugged construction, high reliability, and compliance with military-grade performance standards.

- The micro and nano connectors segment is projected to register the fastest growth at a CAGR of 12.0% from 2026 to 2033, driven by miniaturization trends in electronics, increasing adoption in medical devices, and rising demand for compact wearable and portable systems.

- The industrial segment held the largest market revenue share of approximately 38%–42% in 2025 driven by widespread adoption in factory automation, heavy machinery, and industrial control systems. Circular connectors are extensively used in industrial environments due to their robustness, vibration resistance, and long operational life.

- The defense segment is projected to register the fastest growth at a CAGR of 11.5% from 2026 to 2033, driven by increasing modernization of military equipment, rising procurement of advanced communication systems, and growing demand for rugged interconnect solutions in mission-critical operations.

Market Size & Forecast

- Global Market Value (2025): USD 6.52 Billion

- Expected Market Value (2033): USD 9.63 Billion

- Forecast CAGR (2026–2033): 5.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Circular Connectors Market Segmentation

|

Attributes |

Circular Connectors Key Market Insights |

|

Segments Covered |

· By Type: Circular Metal Shell Connectors (CMSC), Circular Plastic Connectors (CPC), Din Connectors, RF Connectors, Power Connectors and Others · By Pins: Number Of Pins In The Connectors · By Gender: Male and Female · By Application: Mil-Spec Connectors, Din Connectors, Micro and Nano Connectors · By End User: Defense, Railways, Audio Equipment, Power Plants, Industrial and Consumer Electronics |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Amphenol Corporation (U.S.) |

|

Market Opportunities |

• Rising Demand In Electric Vehicles And Charging Infrastructure |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Circular Connectors Market Trends

Trend: Growth In High-Reliability Interconnect Systems For Electrification And Harsh-Environment Applications

Increasing demand for rugged, high-performance connectivity solutions across aerospace, defense, industrial automation, and electric mobility sectors is driving the adoption of circular connectors. Rapid electrification of transportation systems, expansion of smart manufacturing, and rising deployment of mission-critical electronic systems are increasing the need for secure, vibration-resistant, and environmentally sealed interconnection solutions capable of ensuring uninterrupted power and signal transmission.

In modern electric vehicles, manufacturers are increasingly integrating circular connectors within battery management systems, charging interfaces, and power distribution units to ensure stable electrical performance under high-load conditions. For instance, several EV platforms launched in China and South Korea in 2025 have incorporated high-density circular connector assemblies to improve thermal stability and reduce energy loss in high-voltage architectures. In industrial automation, these connectors are widely deployed in robotics and CNC machinery to support continuous operation in vibration-heavy environments while minimizing maintenance downtime.

The rapid expansion of 5G infrastructure, data centers, and edge computing systems is also accelerating demand for compact, high-frequency circular connectors capable of supporting high-speed data transmission with minimal signal interference. In addition, aerospace and defense applications continue to rely on advanced circular connector systems, such as those used in avionics and satellite communication modules, due to their reliability under extreme temperature, pressure, and shock conditions. Growing validation through 2024–2025 defense modernization programs in the U.S. and Europe is reinforcing adoption across mission-critical communication and navigation systems, improving operational reliability by reducing connector failure rates in harsh environments.

Circular Connectors Market Dynamics

Key Market Driver: Rising Electrification And Expansion Of High-Performance Industrial And Communication Systems

Industries worldwide are increasingly adopting circular connectors to support electrification trends, automation expansion, and high-speed communication networks. Their robust locking mechanisms, corrosion resistance, and ability to operate under extreme environmental stress make them essential in aerospace, railways, renewable energy systems, and industrial robotics.

For instance, industrial robotics installations across automotive manufacturing hubs in Germany, Japan, and China during 2024–2025 have increasingly deployed circular connectors to ensure continuous production efficiency and reduce unplanned downtime in automated assembly lines. Similarly, defense-grade communication systems are integrating advanced connector architectures to support secure and uninterrupted data transmission in mission-critical operations, further strengthening demand across high-reliability sectors.

Key Restraint/Challenge: High Manufacturing Complexity And Cost Sensitivity In Advanced Connector Designs

The production of high-performance circular connectors requires precision engineering, specialized materials, and compliance with stringent international standards such as MIL-SPEC and aerospace-grade certifications, significantly increasing manufacturing costs. Miniaturized, high-pin-density, and waterproof connector variants further add to design and production complexity, limiting cost competitiveness in price-sensitive applications.

In addition, fluctuations in raw material supply chains, particularly for specialty alloys and high-grade insulating polymers, can impact production stability and pricing. Benchmarking studies indicate that aerospace-certified circular connectors can cost significantly more than standard industrial connectors, creating adoption barriers for small-scale manufacturers and non-critical applications despite their superior performance characteristics.

Key Market Opportunity: Expansion Of Electric Mobility, 5G Networks, And Smart Infrastructure Development

The rapid growth of electric vehicles, autonomous systems, and next-generation communication infrastructure is creating significant opportunities for circular connector adoption. These connectors are increasingly used in EV battery systems, charging infrastructure, and powertrain electronics to ensure high reliability and efficient energy transfer under demanding operating conditions.

For instance, EV development programs in 2025 across China and Europe have integrated advanced circular connectors in high-voltage battery systems to enhance safety performance and thermal stability during fast-charging operations. In addition, the global rollout of 5G base stations and expansion of edge computing networks in Asia-Pacific and North America is driving demand for high-frequency circular connectors capable of supporting ultra-low latency and high-bandwidth data transmission, positioning the market for sustained long-term growth across connected industrial and digital ecosystems.

Circular Connectors Market Scope

The market is segmented on the basis of type, pins, gender, application, and end-use application.

- By Type

On the basis of type, the Circular Connectors Market is segmented into Circular Metal Shell Connectors (CMSC), Circular Plastic Connectors (CPC), DIN Connectors, RF Connectors, Power Connectors, and Others. The Circular Metal Shell Connectors (CMSC) segment held the largest market revenue share of approximately 45%–50% in 2025 driven by its extensive use in defense systems, industrial machinery, and aerospace applications. CMSC connectors are widely preferred due to their high durability, superior shielding capability, and strong resistance to harsh environmental conditions, making them suitable for mission-critical connectivity applications.

The RF Connectors segment is projected to register the fastest growth at a CAGR of 11.2% from 2026 to 2033, driven by rising deployment in 5G infrastructure, satellite communications, and high-frequency signal transmission systems. Increasing demand for high-speed, low-loss connectivity in telecom networks and advanced electronic systems is further accelerating segment expansion.

- By Pins

On the basis of pins, the market is segmented into low pin count, medium pin count, and high pin count connectors. The medium pin count segment held the largest market revenue share of approximately 40%–45% in 2025 driven by its balanced performance, cost efficiency, and widespread adoption across industrial automation, railways, and consumer electronics applications. Medium pin connectors are preferred due to their versatility in supporting both power and signal transmission requirements across multiple systems.

The high pin count segment is projected to register the fastest growth at a CAGR of 10.5% from 2026 to 2033, driven by increasing demand for complex electronic systems in defense platforms, aerospace avionics, and advanced medical equipment where higher data density and multi-function connectivity are required.

- By Gender

On the basis of gender, the market is segmented into male and female connectors. The male connectors segment accounted for the largest market revenue share of approximately 52%–55% in 2025 driven by its extensive use as plug interfaces in industrial and military-grade systems. Male connectors are widely used due to their structural compatibility and ease of integration in modular connection architectures.

The female connectors segment is projected to grow at the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing demand for secure receptacle-based connectivity solutions in high-vibration environments such as railways, power plants, and aerospace systems.

- By Application

On the basis of application, the market is segmented into MIL-Spec connectors, DIN connectors, micro and nano connectors. The MIL-Spec connectors segment held the largest market revenue share of approximately 48%–52% in 2025 driven by strong adoption in defense, aerospace, and critical communication systems. These connectors are preferred due to their rugged construction, high reliability, and compliance with military-grade performance standards.

The micro and nano connectors segment is projected to register the fastest growth at a CAGR of 12.0% from 2026 to 2033, driven by miniaturization trends in electronics, increasing adoption in medical devices, and rising demand for compact wearable and portable systems.

- By End User

On the basis of end user, the market is segmented into defense, railways, audio equipment, power plants, industrial, and consumer electronics. The industrial segment held the largest market revenue share of approximately 38%–42% in 2025 driven by widespread adoption in factory automation, heavy machinery, and industrial control systems. Circular connectors are extensively used in industrial environments due to their robustness, vibration resistance, and long operational life.

The defense segment is projected to register the fastest growth at a CAGR of 11.5% from 2026 to 2033, driven by increasing modernization of military equipment, rising procurement of advanced communication systems, and growing demand for rugged interconnect solutions in mission-critical operations.

Circular Connectors Market Regional Analysis

North America Circular Connectors Market Insight

North America dominated the circular connectors market with the largest revenue share of approximately 35.2% in 2025, supported by strong demand from aerospace, defense, industrial automation, and telecommunications sectors. The region benefits from high adoption of advanced electronic systems, strong investment in military modernization programs, and widespread use of rugged interconnect solutions across critical infrastructure. Increasing deployment of high-speed data transmission systems and growing demand for reliable connectivity in harsh operating environments further strengthen regional market dominance.

U.S. Circular Connectors Market Insight

The U.S. circular connectors market captured the largest revenue share in 2025 within North America, driven by rapid expansion of defense electronics, aerospace manufacturing, and industrial automation systems. Strong demand for MIL-Spec connectors in mission-critical applications, such as avionics, naval systems, and battlefield communication equipment, continues to support market growth. In addition, rising integration of circular connectors in robotics, smart factories, and telecom infrastructure is accelerating adoption across commercial and industrial sectors.

Europe Circular Connectors Market Insight

The Europe circular connectors market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing investments in industrial automation, railway modernization, and renewable energy infrastructure. Strict regulatory standards for safety and reliability in industrial and defense applications are further supporting demand for high-performance connector systems. The growing adoption of smart manufacturing technologies and expansion of electric mobility infrastructure are also contributing to strong regional growth across both OEM and aftermarket channels.

U.K. Circular Connectors Market Insight

The U.K. circular connectors market is expected to witness steady growth from 2026 to 2033, driven by increasing demand from aerospace, defense, and railway sectors. Rising investment in digital infrastructure and smart transportation systems is boosting the use of rugged and high-reliability connectors. In addition, growing adoption of industrial automation and IoT-enabled devices across manufacturing facilities is further supporting market expansion in both commercial and industrial applications.

Germany Circular Connectors Market Insight

The Germany circular connectors market is expected to witness strong growth from 2026 to 2033, fueled by the country’s advanced manufacturing base, strong automotive industry, and leadership in industrial automation. Increasing integration of Industry 4.0 technologies is driving demand for high-density and high-performance connector systems. In addition, Germany’s focus on renewable energy systems, robotics, and precision engineering is significantly accelerating the adoption of circular connectors across multiple end-use sectors.

Asia-Pacific Circular Connectors Market Insight

The Asia-Pacific circular connectors market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding telecommunications infrastructure, and rising demand for consumer electronics. Increasing investments in smart cities, railway networks, and power generation projects are driving large-scale deployment of connector systems. The region also benefits from strong manufacturing capabilities and cost-effective production, making circular connectors more accessible across emerging economies.

Japan Circular Connectors Market Insight

The Japan circular connectors market is expected to witness steady growth from 2026 to 2033, driven by high demand from robotics, automotive electronics, and advanced industrial machinery sectors. Japan’s strong focus on precision engineering and automation is encouraging the adoption of compact and high-reliability connector solutions. In addition, increasing integration of circular connectors in smart manufacturing systems and IoT-enabled devices is further supporting market expansion across industrial and commercial applications.

China Circular Connectors Market Insight

The China circular connectors market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, strong electronics manufacturing base, and large-scale industrial expansion. The country’s leadership in telecommunications infrastructure, electric vehicles, and smart city projects is significantly boosting demand for advanced connector systems. In addition, the presence of strong domestic manufacturers and cost-efficient production capabilities is further accelerating widespread adoption across industrial, commercial, and defense applications.

Circular Connectors Market Share

The Circular Connectors industry is primarily led by well-established companies, including:

• Amphenol Corporation (U.S.)

• TE Connectivity (Switzerland)

• Molex (U.S.)

• BorgWarner Inc. (U.S.)

• Franz Binder GmbH & Co. Elektrische Bauelemente KG (Germany)

• PHOENIX CONTACT (Germany)

• ITT Inc. (U.S.)

• Japan Aviation Electronics Industry, Ltd. (Japan)

• Shenzhen Deren Electronics Co., Ltd. (China)

• Sumitomo Wiring System Ltd. (Japan)

• Belden Inc. (U.S.)

• Souriau (France)

• OMRON Corporation (Japan)

• LEMO (Switzerland)

• HIROSE ELECTRIC CO., LTD. (Japan)

• JONHON (China)

• Binder Group (Germany)

• CUI Inc. (U.S.)

Latest Developments in Circular Connectors Market

- In September 2024, Aptiv partnered with a European automaker to integrate advanced circular connectors into a new generation of hybrid electric vehicles, focusing on high-voltage power applications. The development aimed to enhance charging efficiency by 25% and reduce CO2 emissions by 15% through improved power management systems, strengthening Aptiv’s position in sustainable automotive connectivity and accelerating adoption of efficient EV technologies in the Circular Connectors Market

- In January 2024, Molex entered into a collaboration with a global robotics manufacturer to supply next-generation circular connectors for industrial automation systems, enabling high-speed data and power transmission. The solution improved robotic operational efficiency by around 30% and reduced energy consumption by 20%, supporting the growing demand for smart manufacturing and reinforcing Molex’s role in advanced industrial connectivity solutions

- In March 2023, TE Connectivity expanded its global footprint by establishing a new R&D center in Bangalore, India, focused on developing innovative connectivity solutions for 5G networks, renewable energy, and advanced industrial applications. This strategic expansion strengthened its innovation pipeline, enhanced regional development capabilities, and supported faster commercialization of next-generation circular connector technologies for high-growth markets

- In June 2023, Amphenol enhanced its circular connector portfolio through a strategic acquisition of a company specializing in high-speed interconnect technologies. This move expanded its technological capabilities and product range, enabling improved performance in aerospace, defense, and industrial applications. The acquisition strengthened Amphenol’s competitive position and accelerated its growth in advanced high-reliability connectivity solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Circular Connectors Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Circular Connectors Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Circular Connectors Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.