Global Clinical Trial Supply And Logistics Market

Market Size in USD Billion

USD

5.96 Billion

USD

5.96 Billion

2025

2033

USD

5.96 Billion

USD

5.96 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.96 Billion | |

| USD 5.96 Billion | |

| % | |

|

What is the Clinical Trial Supply & Logistics Market Size and Overview?

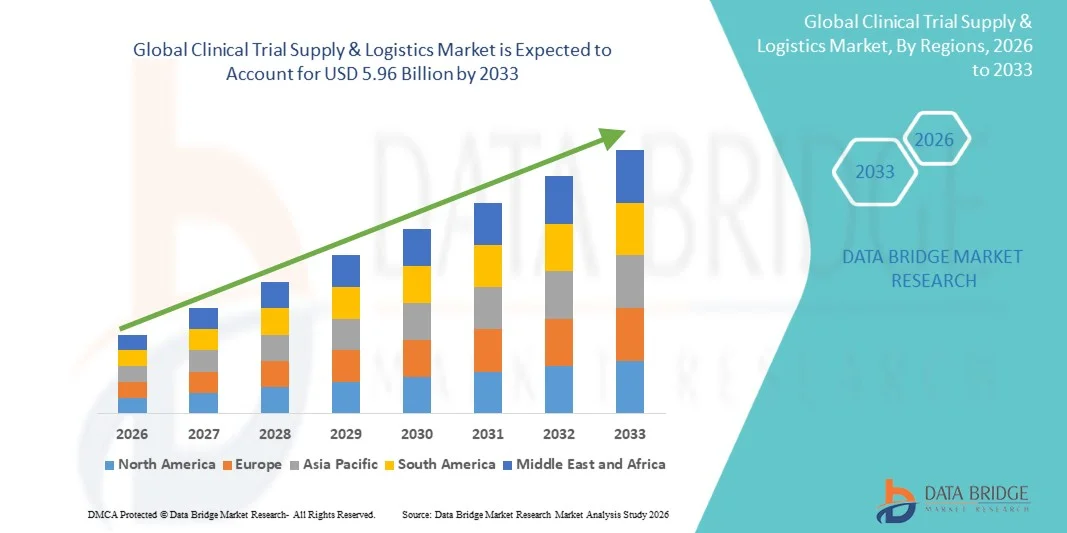

As per Data Bridge Market Research Analysis The global clinical trial supply and logistics market was valued at USD 5.96 billion in 2025 and is projected to reach USD 10.8 billion by 2033, growing at a CAGR of 7.80% during the forecast period.

The current market scenario is characterized by increasing clinical trial complexity, globalization of research, and rising adoption of biologics and cell and gene therapies. Key growth drivers include the increasing number of global clinical trials, rising pharmaceutical R&D expenditure, expansion of decentralized clinical trials (DCTs), growing demand for cell and gene therapy logistics, AI-driven supply forecasting, direct-to-patient delivery models, and increasing outsourcing of logistics operations to specialized third-party providers.

Market Size & Forecast

- Global Market Value (2025): USD 5.96 Billion

- Expected Market Value (2033): USD 10.8 Billion

- Forecast CAGR (2026–2033): 7.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America accounted for the largest revenue share in 2024, holding 38.3% of the global market, driven by strong pharmaceutical R&D infrastructure and a high volume of clinical trial activity.

- Asia-Pacific is expected to witness the fastest growth during the forecast period due to increasing clinical trial activities, improving healthcare infrastructure, and favorable government policies. The region accounted for 21.0% of the global market in 2024.

- Logistics & Distribution dominated the service segment in 2024, accounting for revenue of USD 1.2 billion, driven by the critical need for timely delivery of clinical trial materials and temperature-controlled logistics.

- Phase III dominated the market in 2025, as large-scale trials require extensive logistics support for distribution across multiple sites.

- Pharmaceutical & Biopharmaceutical Companies represented the largest end-use segment, as these organizations conduct the majority of clinical trials.

- Increasing adoption of decentralized clinical trials is supporting demand for direct-to-patient logistics and last-mile delivery solutions.

- AI, IoT, and digital supply chain technologies are improving logistics efficiency, visibility, and compliance across the clinical trial ecosystem.

- Sustainability in clinical trial logistics is emerging as a significant trend, with companies investing in reusable temperature-controlled shippers, recyclable packaging, carbon-neutral transportation, and route optimization.

Report Scope and Clinical Trial Supply & Logistics Market Segmentation

|

Attributes |

Clinical Trial Supply & Logistics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the Clinical Trial Supply & Logistics Market?

Trend: Decentralized Clinical Trials and Direct-to-Patient Logistics

The emergence of decentralized clinical trials (DCTs) is fundamentally transforming clinical trial supply chains. Logistics providers are adapting their service models to prioritize last-mile delivery, home-based treatment workflows, and direct-to-patient shipping with temperature-controlled direct-to-patient delivery and robust chain-of-custody documentation. The shift toward hybrid trial models is driving demand for flexible, scalable logistics solutions.

For instance, the Trials@Home RADIAL trial, conducted across six European countries, implemented a direct-to-participant delivery model and achieved a 94% successful delivery rate. Additionally, in November 2025, Cenmed and Curavit partnered to streamline clinical trial kitting and logistics for decentralized and hybrid clinical trials.

Clinical Trial Supply & Logistics Market Dynamics

Key Market Driver: Growing Complexity of Clinical Trials

The rise of biologics, personalized medicine, gene therapies, and decentralized trial designs has created increasingly complex supply chain requirements. Advanced therapies require stringent temperature controls, customized packaging, real-time tracking, and specialized handling protocols. Cell and gene therapies that require cryogenic storage below -150°C further amplify logistical requirements, driving demand for specialized logistics providers with robust quality management systems.

For instance, a global biotechnology company conducting an LN2-based cell and gene therapy study in Israel required cryogenic storage, rapid access to specialized ancillary equipment, and locally sourced products. Oximio coordinated the procurement of cryogenic water baths, ultra-low-temperature freezers, and lymphodepletion medications from multiple suppliers while maintaining strict patient treatment timelines.

Key Restraint/Challenge: High Costs of Temperature-Controlled Logistics

A significant restraint in ensuring consistent temperature control from manufacturing to clinical site delivery presents significant operational and financial challenges. Temperature excursions can lead to product degradation, trial delays, and regulatory non-compliance, resulting in substantial financial losses. Costs associated with specialized cold chain packaging, continuous monitoring, and contingency planning significantly increase clinical trial budgets.

According to Grand View Research, the global cold chain logistics market is projected to grow at a CAGR of 15.2% from 2025 to 2030, reflecting the significant investment required for temperature-controlled logistics. For example, packaging two investigational biologic vials in a single cold-chain carton reduced overall study costs by nearly 20%, resulting in savings of approximately USD 200,000 while maintaining patient enrollment momentum.

Key Market Opportunity: Expansion in Emerging Markets

Emerging markets, particularly in Asia Pacific and Latin America, offer significant growth opportunities. The growing presence of pharmaceutical and biopharmaceutical companies in China, India, Brazil, and South Korea, coupled with increasing clinical trial activity, is driving demand for specialized logistics services. Clinical trial activity in Asia Pacific is rising significantly faster than in Europe, creating opportunities for logistics providers to establish regional distribution hubs.

For instance, in March 2026, Zuellig Pharma relocated its clinical depot to Misato, Japan, strengthening its clinical supply capability across Asia Pacific. In December 2025, Zuellig Pharma opened a 3,800-square-meter Clinical Trial Support Innovation Center in South Korea. In April 2025, Akesa partnered with Rock8 Science to strengthen pharmaceutical supply chains across the Asia Pacific region.

Clinical Trial Supply & Logistics Market Scope

The clinical trial supply & logistics market is segmented on the basis of service, phase, therapeutic area, and end use.

- By Service

On the basis of service, the market is segmented into logistics & distribution, storage & retention, packaging, labeling & blinding, manufacturing, comparator sourcing, and other services. Logistics & distribution dominated the market in 2024, accounting for revenue of USD 1,200.3 million, driven by the critical need for timely delivery of clinical trial materials to sites worldwide and the increasing complexity of temperature-controlled logistics. The segment encompasses transportation, inventory management, customs clearance, and last-mile delivery services essential for clinical trial operations. Increasing outsourcing of logistics operations to specialized third-party providers is expected to support segment growth throughout the forecast period. The adoption of digital tracking platforms, inventory optimization tools, and real-time monitoring solutions is enhancing efficiency and compliance in logistics and distribution operations.

- By Phase

On the basis of phase, the market is segmented into Phase I, Phase II, Phase III, and Phase IV. Phase III held the largest market share in 2025, as these trials involve large-scale testing with extensive patient enrollment, complex protocols, and strict regulatory requirements, necessitating robust supply chain solutions to manage distribution across multiple sites. Phase III trials generate significant volumes of biological samples and require long-term storage and retrieval systems, driving the highest demand for biorepository and logistics services. The Phase II segment is projected to grow at a steady rate during the forecast period, driven by an increase in the number of mid-sized clinical trials.

- By Therapeutic Area

On the basis of therapeutic area, the market is segmented into oncology, cardiovascular diseases, respiratory diseases, CNS and mental disorders, and others. Cardiovascular diseases held the largest therapeutic area share in 2024, driven by the high prevalence of cardiovascular conditions and the large number of clinical trials conducted in this therapeutic area. Oncology is also a significant segment, driven by the increasing number of oncology clinical trials and the complexity of cancer therapies requiring specialized logistics solutions. The rising prevalence of chronic diseases, including cancer, diabetes, and cardiovascular disorders, is a significant driver of the global clinical trial supplies market.

- By End Use

On the basis of end use, the market is segmented into pharmaceutical & biopharmaceutical companies, contract research organizations, and others. Pharmaceutical & biopharmaceutical companies are the largest end users, as these organizations conduct the majority of clinical trials and require comprehensive supply chain and logistics services to support their research activities. Contract research organizations (CROs) are also significant end users, as they manage clinical trials on behalf of pharmaceutical sponsors and require specialized logistics capabilities. The increasing trend toward outsourcing supply chain management to specialized providers is expected to drive growth across both end-user segments.

Clinical Trial Supply & Logistics Market Regional Analysis

North America Clinical Trial Supply & Logistics Market Insight

North America held the largest revenue share of the global clinical trial supply and logistics market in 2024, accounting for 38.3% of the global market. The region's dominance is supported by a high concentration of pharmaceutical research organizations, advanced healthcare infrastructure, robust regulatory frameworks, and significant R&D investments. The U.S. is projected to lead the global market in terms of revenue through 2030. In 2023, the U.S. Food and Drug Administration issued the "Good Distribution Practice Guidance for Industry," mandating that logistics providers comply with Good Distribution Practices for storage, transportation, documentation, and risk management.

Europe Clinical Trial Supply & Logistics Market Insight

Europe represents a significant market for clinical trial supply and logistics, supported by a strong pharmaceutical research base, advanced healthcare infrastructure, and stringent regulatory frameworks. Countries such as Germany, the United Kingdom, France, and Switzerland are major contributors to the European market. The region's focus on regulatory compliance and quality standards drives demand for specialized logistics services. The European Medicines Agency's rigorous oversight of clinical trial supply chains further supports adoption of specialized logistics providers capable of meeting strict regulatory requirements.

Asia-Pacific Clinical Trial Supply & Logistics Market Insight

Asia-Pacific is expected to witness the fastest growth during the forecast period, driven by increasing pharmaceutical research activities, improving healthcare infrastructure, rising investments, and favorable government policies. Clinical trial activity in the Asia-Pacific region is rising significantly faster than in Europe, a trend expected to accelerate over the next decade. Countries such as China, India, South Korea, and Australia are emerging as key destinations for clinical trials due to lower costs, diverse patient populations, and supportive government initiatives. South Korea is expected to register the highest CAGR from 2025 to 2030, projected to reach USD 170.0 million by 2030.

Middle East & Africa Clinical Trial Supply & Logistics Market Insight

The Middle East and Africa region represents an emerging market for clinical trial supply and logistics, with demand primarily concentrated in the Gulf Cooperation Council countries and South Africa. The MEA market is expected to reach projected revenue of USD 121.9 million by 2030, growing at a CAGR of 6.4% from 2024 to 2030. Governments across the region are increasing investments in healthcare infrastructure and research capabilities to diversify their economies. The region offers advantages such as a diverse patient population and ease in patient recruitment, making it an attractive destination for clinical trials.

South America Clinical Trial Supply & Logistics Market Insight

South America represents an emerging market for clinical trial supply and logistics, with growing demand influenced by increasing clinical trial activity, rising healthcare investments, and expanding pharmaceutical research capabilities. Brazil dominates the South American market, driven by the country's large economy, growing healthcare sector, and increasing government focus on research and development. However, market growth is currently constrained by limited infrastructure, budget constraints, and economic volatility compared to more developed regions.

Which are the Top Companies in Clinical Trial Supply & Logistics Market?

The clinical trial supply & logistics industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- UPS Healthcare (U.S.)

- DHL Supply Chain (Germany)

- FedEx Corporation (U.S.)

- Almac Group (U.K.)

- Catalent Pharma Solutions (U.S.)

- Parexel International Corporation (U.S.)

- Labcorp Drug Development (U.S.)

- Marken (U.S.)

- World Courier (U.S.)

- Kuehne + Nagel (Switzerland)

- PPD (part of Thermo Fisher Scientific) (U.S.)

- ICON plc (Ireland)

- Syneos Health (U.S.)

- Clinigen Group (U.K.)

- Movianto (U.S.)

- UDG Healthcare (Ireland)

- Celerion (U.S.)

- Ancillare (U.S.)

- CRYOPDP (France)

Latest Developments in Clinical Trial Supply & Logistics Market

- In November 2025, UPS Healthcare completed the acquisition of Andlauer Healthcare Group for approximately CAD 2.2 billion (USD 1.6 billion). Under the terms of the agreement, AHG shareholders received CAD 55.00 per share in cash. The acquisition expanded UPS Healthcare's cold chain logistics capabilities and strengthened its position in the clinical trial supply and logistics market across North America.

- In November 2025, Oximio completed the acquisition of Bay Area Research Logistics (now Oximio BARL Canada), expanding its clinical trial supply chain capabilities across North America. This strategic acquisition strengthens Oximio's presence in the Canadian market and enhances its ability to provide end-to-end clinical trial supply chain services.

- In November 2025, Cenmed and Curavit Clinical Research announced a strategic collaboration to streamline clinical trial kitting and logistics. The partnership integrates customized kitting, just-in-time operations, and nationwide distribution to accelerate decentralized and hybrid trials.

- In November 2025, IQVIA and Veeva launched a global clinical and commercial partnership to simplify and accelerate clinical trials by integrating software, data, and services from both organizations. IQVIA joined Veeva's partner programs as an AI partner to enhance Veeva products, including AI-driven applications.

- In October 2025, Oximio announced the opening of a new state-of-the-art depot in Saudi Arabia, expanding its global network in the Middle East. The new depot enhances Oximio's ability to serve pharmaceutical and biotechnology clients conducting clinical trials in the region.

- In September 2025, Science 37 and Catalent announced a strategic partnership to refine the investigational medicinal product supply chain for at-home trial participation. The partnership has enrolled nearly 1,700 patients across 17 studies and delivered over 6,400 shipments.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.