Global Clostridial Diseases Market

Market Size in USD Billion

CAGR :

%

USD

3.49 Billion

USD

8.64 Billion

2025

2033

USD

3.49 Billion

USD

8.64 Billion

2025

2033

| 2026 –2033 | |

| USD 3.49 Billion | |

| USD 8.64 Billion | |

| % | |

|

Clostridial Diseases Market Size

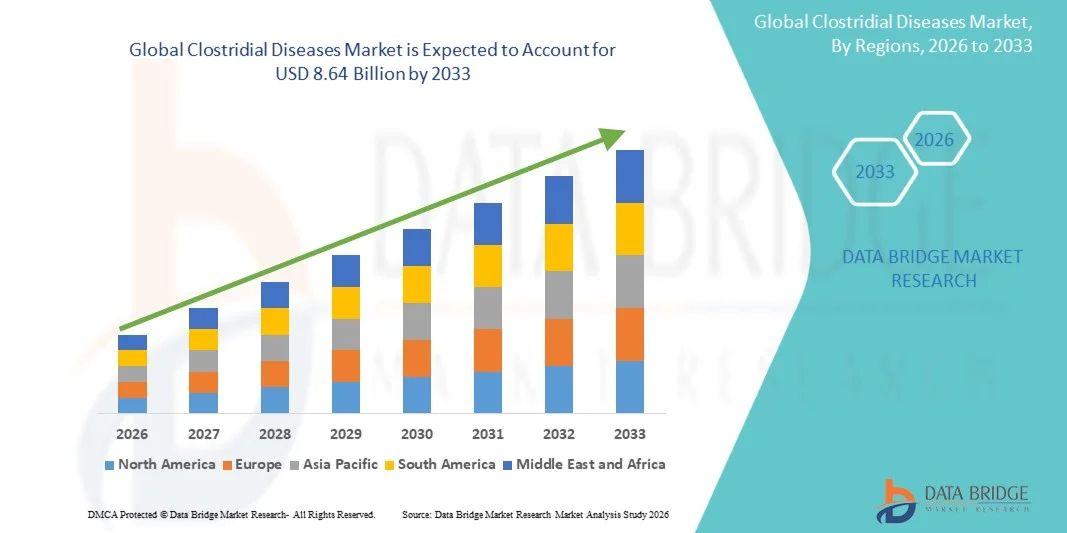

- The global Clostridial Diseases market size was valued at USD 3.49 billion in 2025 and is expected to reach USD 8.64 billion by 2033, at a CAGR of 12.00% during the forecast period

- The market growth is largely driven by the rising incidence of Clostridium-associated infections such as tetanus, botulism, gas gangrene, and Clostridioides difficile infections, along with increasing awareness regarding early diagnosis and preventive vaccination strategies across both human and veterinary healthcare sectors

- Furthermore, growing hospital-acquired infection rates, expanding use of antibiotics, and improving healthcare infrastructure in emerging economies are contributing to increased demand for advanced diagnostic tools, vaccines, and treatment options, thereby significantly accelerating market expansion

Clostridial Diseases Market Analysis

- Clostridial diseases, caused by toxin-producing bacteria such as Clostridium tetani, Clostridium botulinum, and related species, are increasingly important in both veterinary and human healthcare due to their severe, often life-threatening infections, leading to rising demand for vaccines, antibiotics, and preventive disease management solutions

- The escalating demand for Clostridial Disease control is primarily driven by increasing livestock disease burden, rising awareness of zoonotic and toxin-mediated infections, and expanding adoption of preventive vaccination programs such as tetanus toxoid and multivalent vaccines across animal healthcare systems

- North America dominated the Clostridial Diseases market with the largest revenue share of 38.6% in 2025, supported by advanced veterinary infrastructure, high vaccination penetration, strong disease surveillance systems, and established pharmaceutical and biologics manufacturers, with cattle farming contributing significantly to market demand

- Asia-Pacific is expected to be the fastest growing region in the Clostridial Diseases market during the forecast period due to expanding livestock production, rising meat and dairy consumption, increasing veterinary healthcare investments, and government-led immunization and disease prevention initiatives

- The Tetanus segment dominated the Clostridial Diseases market with a market share of 32.8% in 2025, driven by high incidence rates in livestock and humans, strong global immunization coverage through tetanus toxoid vaccination, and continued need for emergency antitoxin and supportive care treatments

Report Scope and Clostridial Diseases Market Segmentation

|

Attributes |

Clostridial Diseases Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Clostridial Diseases Market Trends

“Rising Adoption of Advanced Vaccination and Molecular Diagnostics in Livestock and Clinical Settings”

- A significant and accelerating trend in the global Clostridial Diseases market is the increasing adoption of advanced vaccination strategies such as multivalent clostridial vaccines alongside rapid molecular diagnostic tools for early detection and control of toxin-mediated infections across veterinary and human healthcare systems

- For instance, multivalent vaccines targeting diseases such as blackleg, tetanus, and malignant oedema are being widely used in cattle and sheep populations to provide broader protection and reduce overall disease burden in livestock farming operations

- The integration of molecular diagnostic techniques such as PCR-based testing is improving early identification of infections such as Clostridioides difficile, enabling faster treatment decisions and reducing severe complications in hospital and veterinary environments

- The shift toward preventive healthcare is driving centralized disease management programs where vaccination schedules, surveillance systems, and diagnostic reporting are integrated for improved outbreak control and herd health monitoring

- The growing use of digital livestock health monitoring systems and farm management software is enabling real-time tracking of vaccination status and disease outbreaks, improving efficiency in large-scale animal husbandry operations

- This trend toward more preventive, data-driven, and broad-spectrum disease management approaches is reshaping expectations in infection control, with companies and veterinary institutions increasingly prioritizing combined vaccine-diagnostic solutions

- The demand for effective clostridial disease prevention and rapid diagnostic solutions is growing rapidly across both developed and emerging markets, as livestock producers and healthcare providers focus on reducing mortality, treatment costs, and economic losses

Clostridial Diseases Market Dynamics

Driver

“Growing Livestock Disease Burden and Rising Demand for Preventive Vaccination Programs”

- The increasing prevalence of clostridial infections in livestock and human populations, coupled with rising awareness of zoonotic and toxin-related diseases, is a major driver for the growing demand for vaccines, antibiotics, and preventive healthcare solutions

- For instance, government-led vaccination initiatives in cattle and sheep populations are being expanded in multiple regions to control outbreaks of diseases such as blackleg and tetanus, significantly supporting market growth

- As livestock production intensifies to meet rising global meat and dairy demand, farmers are increasingly adopting preventive healthcare practices to reduce mortality and improve productivity through routine immunization programs

- Furthermore, expanding veterinary healthcare infrastructure and improved access to biologics are enabling wider distribution of tetanus toxoid and multivalent vaccines, strengthening disease prevention efforts across rural and commercial farming systems

- Rising investments in veterinary R&D are leading to the development of more effective and combination-based vaccines that improve protection against multiple clostridial strains simultaneously

- Increasing government support programs for animal disease surveillance and eradication campaigns are further strengthening vaccination coverage in high-risk agricultural regions

- The increasing reliance on preventive vaccination, along with rising investments in animal health management, is significantly propelling adoption of clostridial disease control solutions in both developed and emerging economies

Restraint/Challenge

“Limited Awareness in Rural Regions and High Cost of Advanced Vaccination and Diagnostics”

- Limited awareness regarding clostridial disease prevention in rural and low-income livestock farming communities, along with inadequate veterinary infrastructure, poses a significant challenge to widespread adoption of advanced vaccines and diagnostic solutions

- For instance, delayed diagnosis and underreporting of diseases such as malignant oedema and botulism are still observed in several developing regions due to lack of access to veterinary services and laboratory facilities

- The relatively high cost of multivalent vaccines and molecular diagnostic tests compared to conventional treatment methods can restrict adoption among small-scale farmers and price-sensitive end users

- Furthermore, logistical challenges in cold-chain storage and distribution of biologics in remote areas further limit the effective penetration of vaccination programs in emerging markets

- Limited availability of trained veterinary professionals in rural areas often delays timely diagnosis and treatment, increasing mortality rates and economic losses in livestock populations

- Weak disease reporting and surveillance systems in several developing countries reduce the effectiveness of outbreak monitoring and early intervention strategies

- Overcoming these challenges through awareness programs, government subsidies, and expansion of rural veterinary infrastructure will be critical for improving disease control and supporting long-term market growth

Clostridial Diseases Market Scope

The market is segmented on the basis of disease type, animal species, exotoxins, treatment, end-users, and distribution channel.

- By Disease Type

On the basis of disease type, the Clostridial Diseases market is segmented into black disease, blackleg, malignant oedema, tetanus, botulism, and others. The Tetanus segment dominated the market with the largest revenue share of 32.8% in 2025, driven by its high incidence in both humans and livestock, strong dependence on tetanus toxoid vaccination programs, and the critical need for rapid antitoxin-based emergency treatment. It remains a major public health concern in rural and agricultural regions where wound-related infections are common, sustaining consistent demand. The disease also requires immediate medical intervention, increasing reliance on hospital-based care and emergency therapeutics. Rising awareness of preventive immunization programs further strengthens its dominance across both developed and emerging markets.

The Botulism segment is expected to witness the fastest growth rate of 9.6% from 2026 to 2033, fueled by increasing food and feed contamination cases, rising awareness of toxin-mediated foodborne illnesses, and expanding diagnostic capabilities for early toxin detection. Growing investments in surveillance systems and improved veterinary reporting are further accelerating this segment’s expansion across developed and emerging markets. In addition, increased focus on biosecurity in livestock production is supporting early detection and prevention strategies.

- By Animal Species

On the basis of animal species, the Clostridial Diseases market is segmented into cattle, sheep, poultry, horses, and others. The Cattle segment dominated the market with the largest revenue share of 41.5% in 2025, driven by high susceptibility to clostridial infections such as blackleg and malignant oedema, large-scale dairy and beef production systems, and widespread adoption of routine vaccination programs in commercial livestock farming. Economic losses from cattle mortality strongly encourage preventive healthcare measures, further strengthening market dominance. Cattle also represent a high-value livestock category, increasing investment in disease prevention programs.

The Sheep segment is expected to witness the fastest growth rate of 8.9% from 2026 to 2033, supported by rising small ruminant farming, increasing global demand for meat and wool products, and improved veterinary outreach in rural agricultural regions. Government-supported vaccination initiatives and herd health management programs are also contributing significantly to segment growth. Expansion of organized livestock farming in developing regions is further boosting preventive treatment adoption. Increasing commercialization of sheep farming is also accelerating vaccine penetration.

- By Exotoxins

On the basis of exotoxins, the Clostridial Diseases market is segmented into enterotoxins, neurotoxins, and others. The Neurotoxins segment dominated the market with the largest revenue share of 46.2% in 2025, primarily due to its strong association with severe and life-threatening conditions such as tetanus and botulism, which require immediate medical intervention and long-term preventive immunization strategies. These diseases have high clinical priority, ensuring continuous demand for antitoxins and supportive therapies. Neurotoxin-related infections often lead to high mortality rates, increasing urgency for treatment.

The Enterotoxins segment is expected to witness the fastest growth rate of 10.1% from 2026 to 2033, driven by rising cases of gastrointestinal infections, increasing hospital-acquired Clostridioides difficile infections, and improved adoption of molecular diagnostic tools for toxin identification. Expanding awareness of gut health disorders and infection control practices is further boosting this segment’s growth. Advancements in laboratory diagnostics and rapid testing technologies are also supporting early disease detection. Increasing focus on hospital hygiene is further accelerating demand for enterotoxin management solutions.

- By Treatment

On the basis of treatment, the Clostridial Diseases market is segmented into tetanus toxoid, multivalent vaccine, antibiotics, and others. The Antibiotics segment dominated the market with the largest revenue share of 44.1% in 2025, driven by their widespread use as first-line therapy for active clostridial infections in both human and veterinary medicine, along with rapid symptom control and easy availability across healthcare systems. Antibiotics remain essential in acute infection management, ensuring stable demand globally. They are widely accessible in hospital and veterinary pharmacy settings, supporting their dominant position.

The Multivalent Vaccine segment is expected to witness the fastest growth rate of 11.3% from 2026 to 2033, fueled by increasing preference for broad-spectrum protection against multiple clostridial pathogens, rising adoption in large-scale livestock farming, and cost-effective preventive healthcare strategies. Growing awareness of vaccination benefits over curative treatment is further accelerating segment expansion. Integration of preventive veterinary programs is also enhancing vaccine penetration. Increasing government support for livestock immunization is further strengthening growth momentum.

- By End-Users

On the basis of end-users, the Clostridial Diseases market is segmented into veterinary hospitals, specialty clinics, and others. The Veterinary Hospitals segment dominated the market with the largest revenue share of 39.4% in 2025, supported by high patient inflow for livestock disease management, availability of advanced diagnostic infrastructure, and strong implementation of vaccination and treatment programs. These facilities serve as primary centers for animal infection control and emergency care services. Veterinary hospitals also handle large-scale vaccination campaigns, increasing their dominance.

The Specialty Clinics segment is expected to witness the fastest growth rate of 9.4% from 2026 to 2033, driven by increasing demand for specialized infectious disease treatment, rising awareness among livestock owners, and expanding availability of advanced veterinary services in urban and semi-urban regions. Growth in professional veterinary consultation services is also supporting this segment. Rising focus on targeted and advanced animal healthcare is further accelerating adoption.

- By Distribution Channel

On the basis of distribution channel, the Clostridial Diseases market is segmented into hospital pharmacy, retail pharmacy, and others. The Hospital Pharmacy segment dominated the market with the largest revenue share of 37.1% in 2025, driven by strong in-hospital availability of vaccines, antibiotics, and emergency antitoxins ensuring immediate treatment access in critical cases. Centralized procurement systems and government-supported veterinary programs further reinforce this dominance. Hospital pharmacies ensure rapid drug administration in emergency infections, strengthening their role in disease control.

The Retail Pharmacy segment is expected to witness the fastest growth rate of 8.7% from 2026 to 2033, supported by increasing accessibility of veterinary medicines, expanding rural pharmacy networks, and growing demand for convenient drug availability outside hospital settings. Improved supply chain infrastructure and rising awareness of disease management are also contributing to segment growth. Expanding penetration of veterinary drugs in semi-urban and rural areas is further boosting adoption.

Clostridial Diseases Market Regional Analysis

- North America dominated the Clostridial Diseases market with the largest revenue share of 38.6% in 2025, supported by advanced veterinary infrastructure, high vaccination penetration, strong disease surveillance systems, and established pharmaceutical and biologics manufacturers, with cattle farming contributing significantly to market demand

- The region benefits from well-established cattle and dairy farming industries, where preventive immunization against diseases such as blackleg and tetanus is widely practiced to reduce economic losses

- Strong presence of pharmaceutical and veterinary biologics manufacturers further supports early availability of vaccines, antitoxins, and antibiotics for effective disease management. Government-backed animal health monitoring programs and strict biosecurity regulations are further strengthening early detection and outbreak control capabilities across farms and clinical settings

U.S. Clostridial Diseases Market Insight

The U.S. Clostridial Diseases market captured the largest revenue share within North America in 2025, driven by advanced veterinary healthcare infrastructure, high livestock productivity, and strong implementation of preventive vaccination programs across cattle, sheep, and equine populations. The country’s well-established dairy and beef industries are major contributors to consistent demand for clostridial disease prevention and treatment solutions. Increasing awareness among livestock producers regarding economic losses from diseases such as blackleg, tetanus, and botulism is further accelerating vaccine adoption. The presence of leading pharmaceutical and animal health companies ensures strong availability of antibiotics, antitoxins, and multivalent vaccines. In addition, advanced diagnostic technologies and robust disease surveillance systems enable early detection and effective outbreak management.

Europe Clostridial Diseases Market Insight

The Europe Clostridial Diseases market is projected to expand at a substantial CAGR during the forecast period, driven by stringent animal health regulations, increasing focus on food safety, and rising demand for high-quality livestock production. Countries across the region are emphasizing preventive vaccination programs to control clostridial outbreaks in cattle, sheep, and horses. Growing adoption of advanced veterinary diagnostics and improved disease reporting systems is further supporting market expansion. The region is also witnessing increasing investment in sustainable livestock farming practices, which prioritize disease prevention over treatment. Strong veterinary healthcare infrastructure and awareness among farmers continue to enhance market penetration across both Western and Eastern Europe.

U.K. Clostridial Diseases Market Insight

The U.K. Clostridial Diseases market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising concerns over livestock infections and strong emphasis on preventive animal healthcare practices. Increasing adoption of vaccination programs for cattle and sheep is supporting disease control efforts across rural and commercial farms. The country’s well-established veterinary healthcare system and strong regulatory framework for animal disease prevention are key growth drivers. In addition, rising awareness among farmers regarding economic losses caused by clostridial infections is encouraging proactive immunization. The presence of advanced veterinary service providers further strengthens market development in the region.

Germany Clostridial Diseases Market Insight

The Germany Clostridial Diseases market is expected to expand at a considerable CAGR during the forecast period, supported by strong focus on livestock health, advanced veterinary infrastructure, and high adoption of preventive vaccination programs. Germany’s emphasis on food safety and quality livestock production encourages routine immunization against diseases such as blackleg and tetanus. Increasing integration of veterinary diagnostics and disease monitoring systems is improving early detection and treatment outcomes. The country’s strong research ecosystem in veterinary sciences further supports development of advanced vaccines and biologics. Rising awareness of antimicrobial resistance is also driving a shift toward preventive healthcare strategies.

Asia-Pacific Clostridial Diseases Market Insight

The Asia-Pacific Clostridial Diseases market is poised to grow at the fastest CAGR of 10.2% during the forecast period of 2026 to 2033, driven by expanding livestock populations, increasing meat and dairy consumption, and rising awareness of animal health management. Government initiatives promoting vaccination and disease control programs are significantly boosting market adoption across emerging economies. Rapid urbanization and growth in commercial farming practices are further supporting demand for preventive veterinary solutions. The region is also benefiting from improving access to veterinary healthcare services and expanding distribution of vaccines and antibiotics. In addition, increasing investments in animal health infrastructure are enhancing disease surveillance and outbreak control capabilities.

Japan Clostridial Diseases Market Insight

The Japan Clostridial Diseases market is gaining momentum due to advanced veterinary healthcare systems, high awareness of animal disease prevention, and strong focus on food safety standards. The country’s livestock industry is increasingly adopting preventive vaccination programs to control clostridial infections in cattle and horses. Integration of advanced diagnostic technologies is improving early disease detection and treatment outcomes. Japan’s emphasis on biosecurity and strict animal health regulations further supports market growth. In addition, increasing modernization of livestock farming practices is driving demand for efficient disease management solutions.

India Clostridial Diseases Market Insight

The India Clostridial Diseases market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid expansion of livestock farming, rising rural veterinary awareness, and increasing government initiatives for animal disease prevention. The country has a large cattle and sheep population, which is highly susceptible to clostridial infections such as blackleg and tetanus. Expanding vaccination campaigns and improving access to veterinary healthcare services are significantly supporting market growth. The growth of dairy and meat industries is further driving demand for preventive and therapeutic solutions. In addition, increasing affordability and availability of veterinary biologics are strengthening adoption across rural and semi-urban regions.

Clostridial Diseases Market Share

The Clostridial Diseases industry is primarily led by well-established companies, including:

- Zoetis Inc., (U.S.)

- Merck & Co., Inc., (U.S.)

- Boehringer Ingelheim International GmbH, (Germany)

- Elanco Animal Health Incorporated, (U.S.)

- Ceva Santé Animale, (France)

- Virbac S.A., (France)

- Bimeda, Inc., (Ireland)

- Vetoquinol S.A., (France)

- Phibro Animal Health Corporation, (U.S.)

- HIPRA S.A., (Spain)

- Dechra Pharmaceuticals PLC, (U.K.)

- Neogen Corporation, (U.S.)

- Huvepharma EOOD, (Bulgaria)

- Zoetis Services LLC, (U.S.)

- Merck Animal Health, (U.S.)

- Indian Immunologicals Limited, (India)

- Zydus Animal Health (India)

- Bayer AG, (Germany)

- Valneva SE, (France)

- Virbac Australia Pty Ltd, (Australia)

What are the Recent Developments in Global Clostridial Diseases Market?

- In February 2026, Vanderbilt Health researchers reported a breakthrough experimental mucosal vaccine approach against Clostridioides difficile, demonstrating strong protection in animal models, including elimination of infection, reduced tissue damage, and prevention of recurrence. This development represents a major advancement in next-generation vaccine strategies targeting gut-based immunity rather than systemic response

- In June 2025, Idorsia announced early clinical progress of its first synthetic glycan-based vaccine candidate for Clostridioides difficile infection, reporting that Phase I data showed good tolerability and promising immunogenicity results, marking an important step in vaccine pipeline diversification

- In February 2025, Mikrobiomik received approval of its Paediatric Investigation Plan (PIP) from the European Medicines Agency (EMA) for development of microbiome-based therapy targeting Clostridioides difficile infection in pediatric patients, strengthening focus on microbiota restoration therapies

- In January 2025, Merck discontinued ZINPLAVA (bezlotoxumab), a monoclonal antibody used to prevent recurrent Clostridioides difficile infection, reflecting shifting treatment strategies and evolving competitive dynamics in CDI prevention therapies

- In March 2022, Pfizer reported results from its Phase III CLOVER clinical trial evaluating a vaccine candidate (PF-06425090) for prevention of Clostridioides difficile infection, marking one of the most advanced late-stage vaccine efforts in the field

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.