Global Coccidioidomycosis Drugs Market

Market Size in USD Million

USD

393.60 Million

USD

604.05 Million

2024

2032

USD

393.60 Million

USD

604.05 Million

2024

2032

| 2025 - 2032 | |

| USD 393.60 Million | |

| USD 604.05 Million | |

| % | |

|

Coccidioidomycosis Drugs Market Size

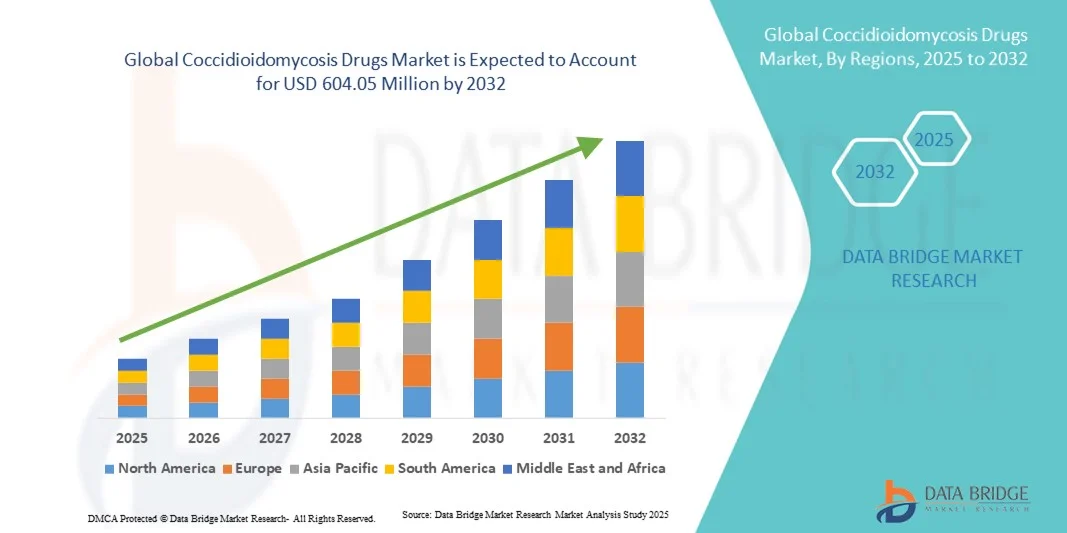

- The global coccidioidomycosis drugs market size was valued at USD 393.6 Million in 2024 and is expected to reach USD 604.05 Million by 2032, at a CAGR of 5.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of fungal infections and the growing awareness about coccidioidomycosis (Valley Fever) in endemic regions, leading to higher demand for effective antifungal medications

- Furthermore, advancements in antifungal drug formulations and diagnostic technologies are improving early detection and treatment outcomes. These converging factors are accelerating the uptake of Coccidioidomycosis Drugs solutions, thereby significantly boosting the industry's growth

Coccidioidomycosis Drugs Market Analysis

- Coccidioidomycosis (Valley Fever) treatments, including antifungal drugs and combination therapies, are becoming increasingly critical in regions with endemic fungal exposure and rising immunocompromised populations

- The growing awareness of fungal lung infections, expansion of healthcare infrastructure in endemic zones, and advances in antifungal formulations are driving demand for effective coccidioidomycosis drugs globally

- North America dominated the coccidioidomycosis drugs market with the largest revenue share of 40.5% in 2024, owing to the high prevalence of the disease in the southwestern U.S., advanced diagnostic capabilities, and strong pharmaceutical infrastructure. The U.S. accounts for a substantial portion of this share, supported by continuous surveillance efforts, increased diagnosis rates, and broad use of azole antifungals such as fluconazole and itraconazole

- Asia-Pacific is expected to be the fastest growing region in the coccidioidomycosis drugs market, as rising healthcare investments, improved diagnostic reach, and greater awareness of fungal diseases in countries like China and India drive higher uptake of treatment option

- The prescription drugs segment dominated the coccidioidomycosis drugs market with a revenue share of 84.6% in 2024, as coccidioidomycosis generally requires medical evaluation, confirmed laboratory diagnosis, and physician-prescribed antifungal therapy

Report Scope and Coccidioidomycosis Drugs Market Segmentation

|

Attributes |

Coccidioidomycosis Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Coccidioidomycosis Drugs Market Trends

Advancements in Antifungal Therapies and Diagnostic Innovations

- A significant and accelerating trend in the global coccidioidomycosis drugs market is the continuous advancement in antifungal drug development and diagnostic technologies, which is improving disease detection, patient outcomes, and overall treatment efficiency

- For instance, in March 2024, Gilead Sciences announced progress in its antifungal research pipeline, focusing on the development of new azole-based compounds designed to enhance efficacy against resistant strains of Coccidioides species. These innovations are intended to address the limitations of existing treatments, such as fluconazole and itraconazole, which face growing resistance concerns

- Moreover, diagnostic advancements such as rapid molecular testing and serological assays are allowing for early and accurate detection of coccidioidomycosis, leading to faster initiation of therapy. Companies like Thermo Fisher Scientific and Bio-Rad Laboratories are expanding their molecular diagnostic portfolios to include specific fungal infection panels, enhancing clinical response capabilities

- The introduction of novel formulations, such as liposomal antifungals and targeted delivery systems, is also improving drug tolerability and bioavailability, reducing side effects, and enhancing patient compliance. Furthermore, ongoing collaborations between pharmaceutical companies and research institutions are fostering innovation in antifungal drug design and personalized treatment approaches

- This growing focus on next-generation antifungal therapies and rapid diagnostics is expected to reshape the treatment landscape for coccidioidomycosis, addressing both unmet clinical needs and emerging resistance trends globally

Coccidioidomycosis Drugs Market Dynamics

Driver

Rising Incidence of Fungal Infections and Increased Awareness in Endemic Regions

- The increasing prevalence of coccidioidomycosis, commonly known as Valley Fever, particularly in endemic regions such as the southwestern United States, Mexico, and parts of Central and South America, is a major driver of market growth. The growing incidence of fungal infections due to climate change, dust exposure, and increased travel to endemic areas is boosting the demand for effective therapeutic options

- For instance, in February 2023, the U.S. Centers for Disease Control and Prevention (CDC) reported a notable rise in coccidioidomycosis cases across Arizona and California, prompting renewed efforts to improve public awareness and enhance diagnostic infrastructure

- Government and healthcare organizations are also increasing initiatives for early detection and prevention, including educational campaigns and improved reporting systems. These efforts, combined with rising healthcare expenditure and improved access to antifungal medications, are driving steady growth in the market

- Furthermore, the development of novel treatment strategies such as combination antifungal therapy, alongside ongoing clinical trials for vaccine candidates, is anticipated to strengthen the therapeutic pipeline. Growing investment in public health preparedness and disease surveillance programs is also supporting the long-term expansion of the coccidioidomycosis drugs market

Restraint/Challenge

Drug Resistance, Side Effects, and Limited Treatment Accessibility

- One of the major challenges restraining the coccidioidomycosis drugs market is the increasing concern over antifungal resistance, which can limit the effectiveness of existing therapies such as fluconazole and amphotericin B. Resistance development complicates treatment outcomes, leading to prolonged recovery periods and higher healthcare costs

- For instance, recent studies published in 2024 indicated a growing number of Coccidioides isolates showing reduced susceptibility to azole-based antifungals, highlighting the urgent need for new drug classes

- In addition, the potential for adverse effects, including nephrotoxicity and hepatotoxicity associated with some antifungal drugs, can discourage long-term use or complicate treatment in patients with comorbidities

- Limited access to advanced antifungal drugs in developing regions, due to high costs and inadequate healthcare infrastructure, further constrains market penetration. The availability of only a few approved antifungal options also underscores the need for accelerated drug development and improved global supply chains

- To overcome these challenges, key players are focusing on developing safer, broad-spectrum agents and investing in awareness programs that emphasize early diagnosis and appropriate treatment adherence. The integration of government-supported healthcare initiatives and cost-effective drug production strategies will be crucial to ensuring equitable access and sustained market growth

Coccidioidomycosis Drugs Market Scope

The market is segmented on the basis of disease type, drugs type, product category, end-users, and distribution channel.

- By Disease Type

On the basis of disease type, the coccidioidomycosis drugs market is segmented into acute coccidioidomycosis, chronic coccidioidomycosis, and disseminated coccidioidomycosis. The acute coccidioidomycosis segment dominated the largest market revenue share of 47.3% in 2024, driven by the high prevalence of mild and self-limiting infections in endemic regions such as the southwestern U.S., Mexico, and parts of Latin America. Early and widespread diagnosis using serology and molecular testing, combined with public health awareness campaigns about Valley Fever, has significantly increased treatment adoption. Azole antifungals, particularly fluconazole, are widely prescribed for mild to moderate acute cases. Government programs promoting fungal disease management and the presence of strong healthcare infrastructure reinforce its dominance. Increased access to outpatient clinics and hospitals, alongside physician adherence to clinical guidelines, further sustains market leadership. Rising insurance coverage, timely intervention, and public education on early symptom detection support broad usage of acute treatment regimens. The segment also benefits from ongoing research into improved antifungal formulations and the availability of generic drugs, ensuring consistent global demand. Strategic initiatives by pharmaceutical companies to maintain supply and increase accessibility in endemic areas have strengthened acute coccidioidomycosis’s leading position.

The disseminated coccidioidomycosis segment is projected to witness the fastest CAGR of 8.6% from 2025 to 2032, driven by the rising number of immunocompromised populations including HIV/AIDS patients, organ transplant recipients, and chemotherapy patients. Severe systemic infections require long-term antifungal therapy, often with intravenous amphotericin B or liposomal formulations. Expansion of advanced diagnostic facilities capable of detecting extrapulmonary dissemination, government funding for rare fungal diseases, and clinical trials for newer azoles with improved safety profiles are enhancing early identification and treatment rates. Growing awareness among healthcare professionals, better hospital access, and availability of combination antifungal therapy contribute to market growth. Increased prevalence of chronic comorbidities, integration of fungal disease management into national health programs, and rising adoption of tertiary care facilities strengthen the segment’s rapid growth trajectory. Moreover, innovations in therapeutic delivery and targeted treatment options further accelerate the expansion of the disseminated coccidioidomycosis treatment market, making it the fastest-growing disease type segment globally.

- By Drugs Type

On the basis of drugs type, the coccidioidomycosis drugs market is segmented into clotrimazole, econazole, miconazole, terbinafine, fluconazole, ketoconazole, and amphotericin. The fluconazole segment held the largest market revenue share of 41.8% in 2024, owing to its status as the most widely prescribed antifungal for coccidioidomycosis management. Fluconazole is preferred for its oral availability, affordability, broad safety profile, and inclusion in CDC-recommended treatment protocols. Its generic availability ensures widespread access across both hospital and outpatient settings. Major pharmaceutical players continue to maintain consistent supply and quality, supporting global adoption. Awareness among physicians and integration into public health antifungal programs, particularly in endemic regions, further reinforce the dominance of fluconazole. It is often prescribed for mild to moderate infections, while its dosing flexibility allows use across diverse patient populations. The segment also benefits from research into new formulations and combination therapies. Increased accessibility, cost-effectiveness, and continued guideline recommendations position fluconazole as the primary drug choice for coccidioidomycosis worldwide.

The amphotericin B segment is expected to witness the fastest CAGR of 9.2% from 2025 to 2032, driven by its critical role in severe and disseminated infections unresponsive to azoles. Lipid-based formulations, such as liposomal amphotericin B, reduce nephrotoxicity while maintaining strong antifungal efficacy. Rising demand in tertiary care hospitals, immunocompromised populations, and intravenous administration support segment growth. Ongoing innovations in hospital delivery systems, improved safety profiles, and availability of advanced therapeutics enable its expanding use. Moreover, clinical trials exploring combination therapies, government support for antifungal access, and increasing severe infection prevalence fuel market expansion. The segment is further supported by growing recognition of amphotericin B’s role in resistant infections and its inclusion in hospital treatment protocols.

- By Product Category

On the basis of product category, the coccidioidomycosis drugs market is segmented into prescription and over the counter. The prescription drugs segment dominated the market with a revenue share of 84.6% in 2024, as coccidioidomycosis generally requires medical evaluation, confirmed laboratory diagnosis, and physician-prescribed antifungal therapy. Complex dosing regimens, the risk of recurrence, and potential drug interactions necessitate medical supervision. Hospitals and clinics primarily manage dispensing through structured treatment pathways. Regulatory oversight ensures the safety and efficacy of these drugs, and constant updates in clinical guidelines reinforce prescription dominance. The presence of infectious disease specialists, advanced laboratory infrastructure, and patient monitoring programs further strengthen the segment. Patient adherence programs, insurance coverage, and access to tertiary care facilities support the ongoing demand for prescription antifungals globally. The segment also benefits from pharmaceutical initiatives to maintain consistent supply and introduce newer treatment options.

The over-the-counter segment is projected to grow at the fastest CAGR of 7.5% from 2025 to 2032, driven by rising awareness of mild fungal infections and increasing consumer preference for topical antifungal products. Availability of creams, ointments, and gels for early symptom management supports self-treatment, especially in regions with limited healthcare access. Retail and online pharmacy expansions, cost-effective formulations, and e-commerce penetration accelerate adoption. Growing self-medication trends, easy application, and preventive use options further enhance segment growth. Government support for OTC antifungal awareness campaigns, convenience, and digital marketing also contribute to rapid uptake. Increasing consumer confidence in early intervention, combined with broader distribution channels, positions OTC antifungals as the fastest-growing product category globally.

- By End-Users

On the basis of end-users, the coccidioidomycosis drugs market is segmented into Specialty Clinics, Hospitals, Homecare, and Others. The hospitals segment accounted for the largest market revenue share of 52.1% in 2024, driven by hospital-based diagnoses, management of moderate to severe cases, and administration of advanced antifungal therapies including intravenous formulations. Hospitals provide infectious disease specialists, diagnostic imaging, laboratory facilities, and intensive care, ensuring accurate treatment. High patient inflow, insurance coverage, integration of stewardship programs, and long-term patient monitoring reinforce hospital dominance. The segment benefits from government initiatives promoting hospital-based care and expanding tertiary care facilities. Established patient referral systems, centralized treatment protocols, and structured care pathways further strengthen hospitals’ leadership in the market.

The specialty clinics segment is expected to record the fastest CAGR of 8.9% from 2025 to 2032, as outpatient care expands through targeted infectious disease and pulmonary clinics. Clinics provide follow-up therapy, localized treatment, and chronic care management, improving patient compliance. Decentralization of healthcare services, government initiatives, cost-effective care, and shorter treatment cycles support segment growth. The rise in fungal disease reference centers, specialized physician training, and patient preference for outpatient care accelerate adoption. Expanded coverage, awareness campaigns, and improved access to antifungal therapy in community clinics reinforce the segment’s rapid growth trajectory globally.

- By Distribution Channel

On the basis of distribution channel, the coccidioidomycosis drugs market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The hospital pharmacy segment held the largest market revenue share of 48.5% in 2024, due to centralized dispensing of prescription antifungals, management of complex dosing, and intravenous drug administration. Bulk procurement, regulatory compliance, trained pharmacists, and hospital oversight maintain high fulfillment rates. Centralized pharmacy management, integration with hospital treatment pathways, and quality assurance further support dominance.

The online pharmacy segment is projected to register the fastest CAGR of 9.8% from 2025 to 2032, driven by digital healthcare adoption, e-commerce penetration, door-step delivery, and online prescription refills. Patients in remote or non-endemic regions increasingly rely on digital platforms. Expanding smartphone use, digital payments, government e-pharmacy regulations, and convenience of online access accelerate segment growth. COVID-19-induced digital adoption further strengthened online pharmacy uptake. Easy accessibility, cost-effectiveness, and availability of antifungal drugs through e-pharmacies make this the fastest-growing distribution channel globally.

Coccidioidomycosis Drugs Market Regional Analysis

- North America dominated the coccidioidomycosis drugs market with the largest revenue share of 40.5% in 2024, owing to the high prevalence of the disease in the southwestern U.S., advanced diagnostic capabilities, and strong pharmaceutical infrastructure

- The region’s dominance is further strengthened by robust healthcare expenditure, widespread clinical awareness, and a well-established antifungal drug supply chain. The growing incidence of coccidioidomycosis, commonly known as Valley Fever, in states such as Arizona and California have prompted greater government and institutional focus on early detection and treatment accessibility

- Ongoing research collaborations between healthcare institutions and pharmaceutical companies are facilitating the development of novel azole-based and echinocandin antifungal therapies, further boosting regional growth

U.S. Coccidioidomycosis Drugs Market Insight

The U.S. coccidioidomycosis drugs market captured the largest revenue share in 2024 within North America, primarily driven by the increasing number of reported cases and expanding clinical diagnostic infrastructure. High disease prevalence in endemic regions, along with improved public health reporting systems, is leading to early diagnosis and greater treatment uptake. The presence of leading pharmaceutical companies such as Gilead Sciences, Pfizer, and Astellas Pharma—actively involved in antifungal research—supports innovation and accessibility of advanced therapeutics. Furthermore, growing investments in vaccine development programs and the availability of both oral and parenteral antifungal formulations have positioned the U.S. as the dominant market within the region.

Europe Coccidioidomycosis Drugs Market Insight

The Europe coccidioidomycosis drugs market is projected to grow at a moderate CAGR during the forecast period, driven by rising awareness of imported fungal infections and the growing availability of antifungal drugs through well-structured healthcare systems. The region’s focus on enhancing diagnostic capabilities for fungal pathogens and the expansion of hospital-based infectious disease units are key growth contributors. The European Centre for Disease Prevention and Control (ECDC) has also increased surveillance programs to monitor fungal infections, leading to higher treatment adoption. Moreover, supportive government healthcare policies and advancements in molecular diagnostic tools continue to strengthen the region’s market position.

U.K. Coccidioidomycosis Drugs Market Insight

The U.K. coccidioidomycosis drugs market is anticipated to expand steadily over the forecast period, supported by the country’s growing focus on improving fungal infection diagnostics and the availability of advanced treatment protocols. Although the disease is not endemic to the U.K., rising cases among travelers returning from North America and Latin America have driven demand for improved diagnostic awareness among healthcare professionals. The National Health Service (NHS) is enhancing laboratory infrastructure to ensure early detection of fungal infections, contributing to consistent market growth.

Germany Coccidioidomycosis Drugs Market Insight

The Germany coccidioidomycosis drugs market is expected to grow at a significant CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and focus on infectious disease management. Increased emphasis on clinical research and the development of antifungal resistance monitoring systems are key drivers supporting the market. Germany’s pharmaceutical sector is also investing in the production and distribution of antifungal agents, ensuring steady supply across hospitals and specialty clinics. Additionally, the rise in fungal awareness campaigns and government-led initiatives promoting early treatment have strengthened Germany’s role in the European market.

Asia-Pacific Coccidioidomycosis Drugs Market Insight

The Asia-Pacific coccidioidomycosis drugs market is projected to grow at the fastest CAGR during 2025–2032, driven by rising healthcare investments, improved diagnostic reach, and growing awareness of fungal diseases. Countries such as China, India, and Japan are witnessing increasing recognition of coccidioidomycosis and other fungal infections due to better healthcare infrastructure and expanding clinical research activities. Regional governments are also investing in advanced fungal testing facilities, which is improving early diagnosis rates. Furthermore, as pharmaceutical manufacturers increase local production and distribution of antifungal drugs, treatment accessibility is improving, supporting overall market expansion.

Japan Coccidioidomycosis Drugs Market Insight

The Japan coccidioidomycosis drugs market is gaining traction as awareness about fungal infections grows among clinicians and travelers returning from endemic regions. Japan’s emphasis on high-quality healthcare delivery, coupled with ongoing research in antifungal therapies, is driving steady market progress. The country’s regulatory support for fast-track approvals of essential antifungal medications ensures rapid market entry of new drugs, further promoting accessibility and affordability.

China Coccidioidomycosis Drugs Market Insight

The China coccidioidomycosis drugs market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s increasing healthcare expenditure, rising diagnostic awareness, and expanding hospital network. China’s pharmaceutical industry is also investing heavily in the development of antifungal drug formulations and rapid testing kits to address the rising burden of fungal diseases. The combination of a growing middle-class population, improved healthcare access, and government initiatives to enhance disease surveillance and treatment availability is expected to make China one of the fastest-growing countries in the Coccidioidomycosis Drugs market.

Coccidioidomycosis Drugs Market Share

The Coccidioidomycosis Drugs industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Novartis AG (Switzerland)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Viatris Inc. (U.S.)

- Cipla Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Cadila Pharmaceuticals (India)

- AbbVie Inc. (U.S.)

- Dr. Reddy’s Laboratories Ltd. (India)

Latest Developments in Global Coccidioidomycosis Drugs Market

- In August 2024, the University of Arizona announced that a human Valley fever vaccine candidate would proceed toward Phase 1 clinical trials, thanks to a significant investment from the National Institutes of Health (NIH). This advancement follows the successful testing of a canine vaccine candidate for Valley fever, which is currently under review by the U.S. Department of Agriculture’s Center for Veterinary Biologics

- In August 2024, Anivive Lifesciences Inc. received a contract worth up to USD 33 million from the NIH's National Institute of Allergy and Infectious Diseases (NIAID) to support the development of a vaccine against Coccidioides, the fungus responsible for Valley fever. This funding aims to advance the vaccine candidate toward human clinical trials

- In November 2024, a study published in Antimicrobial Agents and Chemotherapy evaluated the in vitro activity of olorofim against Coccidioides species. The results demonstrated potent activity against all isolates tested, including those with elevated fluconazole minimum inhibitory concentrations, suggesting its potential as a treatment option for resistant strains

- In March 2025, NIAID published an updated strategic plan for research to develop a Valley fever vaccine. The plan outlines three major research areas: addressing gaps in Coccidioides basic research to support vaccine development, developing tools and resources to support vaccine development, and advancing vaccines to prevent coccidioidomycosis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.