Global Cold Agglutinin Disease Market

Market Size in USD Billion

CAGR :

%

USD

145.35 Billion

USD

592.41 Billion

2025

2033

USD

145.35 Billion

USD

592.41 Billion

2025

2033

| 2026 –2033 | |

| USD 145.35 Billion | |

| USD 592.41 Billion | |

| % | |

|

Cold Agglutinin Disease Market Size

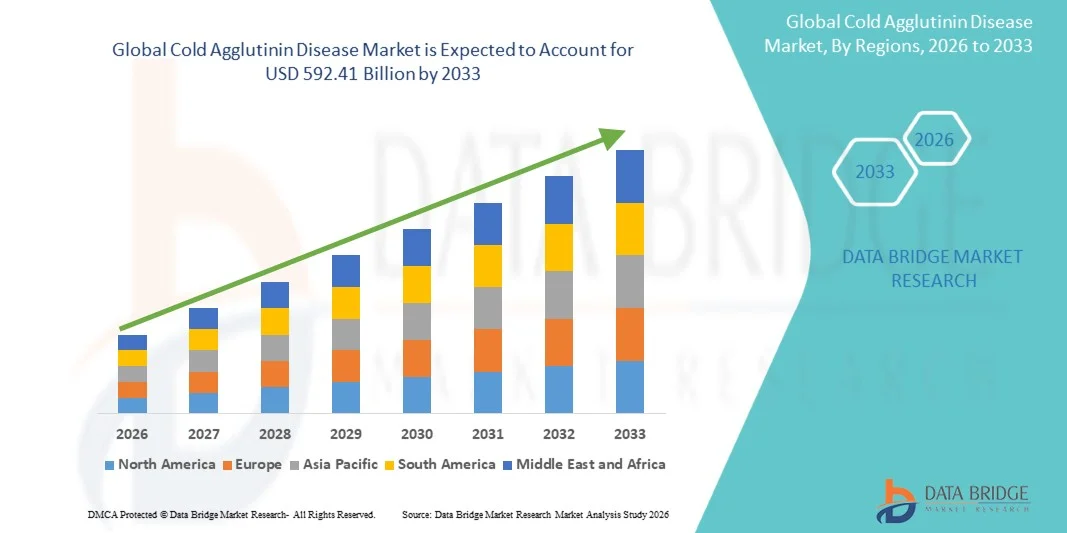

- The global cold agglutinin disease market size was valued at USD 145.35 billion in 2025 and is expected to reach USD 592.41 billion by 2033, at a CAGR of 19.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cold agglutinin disease along with improved awareness, advancements in diagnostic techniques, and the rising adoption of targeted therapies and biologics within hematology and rare disease treatment landscapes

- Furthermore, growing demand for effective and patient-centric treatment options, coupled with ongoing clinical research, regulatory approvals, and the expansion of healthcare infrastructure, is establishing advanced therapeutic solutions as a preferred approach for managing cold agglutinin disease. These converging factors are accelerating the uptake of novel treatments, thereby significantly boosting the industry's growth

Cold Agglutinin Disease Market Analysis

- Cold agglutinin disease (CAD), a rare autoimmune hemolytic anemia characterized by cold-reactive antibodies that lead to red blood cell destruction, is increasingly being recognized as a distinct clinical condition, driving demand for effective pharmacological management across multiple therapeutic classes in hematology and rare disease care

- The growing burden of cold agglutinin disease is primarily driven by improved diagnostic awareness, advancements in hematological testing, and the increasing use of targeted and supportive therapies, including corticosteroids, alkylating agents, purine nucleoside analogs, biologics, and other treatment options that help manage hemolysis and disease symptoms

- North America dominated the cold agglutinin disease market with the largest revenue share of 40.01% in 2025, supported by advanced healthcare infrastructure, early adoption of novel therapies, strong clinical research activity, and a high concentration of specialized treatment centers, with the U.S. leading in diagnosis rates and treatment accessibility

- Asia-Pacific is expected to be the fastest growing region in the cold agglutinin disease market during the forecast period, accounting for a growing share of the market, due to increasing healthcare awareness, improving diagnostic capabilities, expanding access to advanced therapies, and rising investments in healthcare infrastructure across emerging economies

- Biologics segment dominated the cold agglutinin disease market with a significant market share of 52.6% in 2025, driven by their targeted mechanism of action, improved clinical efficacy in reducing hemolysis, and growing preference among healthcare providers compared to traditional therapies such as corticosteroids and alkylating agents

Report Scope and Cold Agglutinin Disease Market Segmentation

|

Attributes |

Cold Agglutinin Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Cold Agglutinin Disease Market Trends

“Rising Adoption of Targeted Biologics and Complement Inhibitors”

- A significant and accelerating trend in the global cold agglutinin disease market is the increasing adoption of targeted biologics and complement pathway inhibitors that directly address the underlying disease mechanism

- For instance, drugs such as sutimlimab are being used to inhibit the classical complement pathway, offering improved control of hemolysis and reducing the need for frequent transfusions

- The shift toward precision medicine in CAD is enabling more effective and individualized treatment approaches, with therapies designed to minimize immune-mediated red blood cell destruction. Furthermore, ongoing clinical trials are expanding the pipeline of novel biologics aimed at complement components

- The integration of advanced diagnostics with targeted therapies is facilitating earlier and more accurate identification of patients who can benefit from these treatments, improving clinical outcomes and disease management

- This trend toward mechanism-based therapies is fundamentally reshaping treatment expectations in rare hematologic disorders, as companies such as Sanofi are advancing complement inhibitor portfolios for CAD and related conditions

- The demand for biologics and complement-targeted therapies is growing steadily across both developed and emerging regions, as healthcare systems increasingly prioritize effective, long-term disease control options

- Additionally, the expansion of rare disease registries and real-world evidence studies is supporting better understanding of treatment outcomes, further guiding clinical decision-making and therapy optimization

Cold Agglutinin Disease Market Dynamics

Driver

“Rising Diagnosis Rates and Increasing Awareness of Rare Hematologic Disorders”

- The increasing awareness among healthcare professionals and patients regarding rare hematologic disorders such as cold agglutinin disease is a significant driver for market growth

- For instance, improved screening programs and advancements in immunohematology testing have enabled earlier detection and diagnosis of CAD in clinical settings

- As clinicians become more familiar with disease symptoms and laboratory markers, the rate of accurate diagnosis is increasing, leading to higher treatment adoption

- Furthermore, the growing emphasis on rare disease research and the expansion of hematology specialty centers are supporting better disease management and patient referral networks. The availability of specialized care pathways is also improving treatment access

- The combination of improved diagnostic capabilities and heightened disease awareness is driving demand for effective therapies and encouraging pharmaceutical innovation in this niche segment

- Increasing government initiatives and support programs for rare diseases are also contributing to improved access to diagnostics and treatments, further supporting market expansion

- Growing collaboration between academic institutions and biopharmaceutical companies is accelerating research activities and clinical trials, enhancing the availability of advanced therapeutic options

Restraint/Challenge

“Limited Treatment Accessibility and High Cost of Advanced Therapies”

- Limited access to specialized healthcare facilities and advanced therapies poses a significant challenge to the broader adoption of cold agglutinin disease treatments

- For instance, complement inhibitor therapies and biologics often require specialized administration and monitoring, which may not be readily available in low-resource settings

- The high cost associated with advanced biologic treatments can restrict patient access, particularly in developing regions or among underinsured populations. Furthermore, reimbursement limitations in certain healthcare systems can delay or restrict therapy uptake

- Variability in diagnostic capabilities across regions also contributes to delayed diagnosis and underdiagnosis of the disease, impacting timely treatment initiation

- Overcoming these challenges through improved healthcare infrastructure, expanded reimbursement policies, and increased availability of cost-effective treatment options will be critical for sustained market growth

- Additionally, stringent regulatory requirements for approval of rare disease therapies can prolong development timelines and increase overall commercialization costs for manufacturers

- Limited patient population size also poses challenges for large-scale clinical trials, making it difficult to generate extensive real-world evidence and slowing down the pace of innovation

Cold Agglutinin Disease Market Scope

The market is segmented on the basis of drugs, route of administration, dosage form, end-users, and distribution channel.

- By Drugs

On the basis of drugs, the cold agglutinin disease market is segmented into corticosteroids, alkylating agents, purine nucleoside analogs, biologics, and others. The biologics segment dominated the market with the largest market revenue share of 52.6% in 2025, driven by their targeted mechanism of action that addresses the underlying complement-mediated hemolysis in CAD. Biologics such as complement inhibitors are increasingly preferred due to their improved clinical efficacy in reducing transfusion dependence and disease relapse rates. The growing focus on precision medicine and targeted therapies has further accelerated the adoption of biologics over conventional treatments. Additionally, strong clinical pipelines and regulatory approvals are supporting market expansion. Healthcare providers increasingly favor biologics for their ability to deliver sustained disease control with fewer systemic side effects compared to traditional drug classes. The segment continues to benefit from ongoing research and innovation by pharmaceutical companies focused on rare hematologic disorders.

The purine nucleoside analogs segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by their immunosuppressive properties and increasing use in managing refractory cases of cold agglutinin disease. These agents help in reducing abnormal immune responses responsible for red blood cell destruction. Growing clinical evidence supporting their effectiveness in combination therapies is boosting their adoption. Furthermore, their role as adjunct therapies in patients who are not eligible for biologics is expanding their clinical relevance. Increasing physician familiarity and inclusion in treatment guidelines are also contributing to segment growth.

- By Route of Administration

On the basis of route of administration, the cold agglutinin disease market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with the largest revenue share of 64.3% in 2025, primarily due to the widespread use of injectable biologics and complement inhibitors that require intravenous or subcutaneous administration. Parenteral administration ensures higher bioavailability and rapid therapeutic action, which is critical in managing hemolytic episodes in CAD patients. Many advanced therapies in this market are biologics that cannot be administered orally due to their molecular structure. Hospitals and specialty clinics also prefer parenteral routes for better monitoring and controlled dosing. The increasing availability of infusion centers and trained healthcare professionals further supports the dominance of this segment. Additionally, clinical protocols for CAD management often recommend parenteral therapies for effective disease control.

The oral segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing development and adoption of oral purine nucleoside analogs and other supportive therapies. Oral administration offers greater convenience, improved patient compliance, and suitability for long-term outpatient treatment. The growing preference for home-based care and reduced hospital visits is further accelerating demand for oral therapies. Advances in drug formulation and improved bioavailability of oral medications are also contributing to segment expansion.

- By Dosage Form

On the basis of dosage form, the cold agglutinin disease market is segmented into tablets, injections, and others. The injections segment dominated the market with the largest revenue share of 61.8% in 2025, driven by the high adoption of biologics and complement inhibitors that are primarily available in injectable formulations. Injections allow for precise dosing and rapid onset of action, which is essential for managing acute hemolysis in CAD patients. The clinical requirement for controlled administration of advanced therapies supports the dominance of this segment. Hospitals and specialty clinics are the primary settings for injectable treatments, ensuring proper monitoring of patients during administration. Additionally, many newly approved CAD therapies are biologics formulated as injections, reinforcing segment growth. The need for intravenous or subcutaneous delivery of large-molecule drugs further strengthens the preference for injectable dosage forms.

The tablets segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing use of oral medications such as purine nucleoside analogs and supportive therapies. Tablets offer ease of administration, improved patient adherence, and suitability for long-term outpatient management. The growing trend toward homecare treatment and self-administration is also supporting adoption. Pharmaceutical advancements in oral drug delivery systems are enhancing the effectiveness and stability of tablet formulations.

- By End-Users

On the basis of end-users, the cold agglutinin disease market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment dominated the market with the largest revenue share of 48.5% in 2025, due to the availability of advanced diagnostic infrastructure, access to biologics and infusion therapies, and the presence of specialized hematology departments. Hospitals are the primary centers for initiating treatment in CAD patients, particularly for administering injectable biologics and managing acute complications. The need for continuous monitoring and multidisciplinary care further supports hospital dominance. Additionally, most clinical trials and advanced treatment protocols are conducted in hospital settings. The availability of skilled healthcare professionals and emergency care facilities also contributes to higher patient preference for hospitals.

The homecare segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing shift toward outpatient care and self-administration of oral therapies. Homecare settings provide convenience, reduced hospitalization costs, and improved quality of life for patients with chronic conditions such as CAD. The rising availability of portable medical devices, telemedicine support, and oral treatment options is facilitating this transition. Increasing patient awareness and preference for at-home treatment management are further supporting segment growth.

- By Distribution Channel

On the basis of distribution channel, the cold agglutinin disease market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the market with the largest revenue share of 46.9% in 2025, as most biologics and injectable therapies are dispensed directly through hospitals where treatment is administered. Hospital pharmacies ensure proper storage, handling, and controlled distribution of specialized drugs required for CAD treatment. The close integration with inpatient and outpatient services makes hospital pharmacies the primary channel for advanced therapies. Additionally, hospital-based dispensing allows for better patient monitoring and adherence to treatment protocols. The presence of complex therapies that require physician supervision further reinforces the dominance of this segment.

The online pharmacy segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing adoption of digital healthcare platforms and e-commerce in pharmaceutical distribution. Online pharmacies offer convenience, home delivery, and easy access to medications, particularly for oral therapies used in CAD management. The growing penetration of internet services and digital health awareness is supporting this trend. Additionally, the expansion of telemedicine and prescription digitization is facilitating the use of online channels for drug procurement.

Cold Agglutinin Disease Market Regional Analysis

- North America dominated the cold agglutinin disease market with the largest revenue share of 40.01% in 2025, supported by advanced healthcare infrastructure, early adoption of novel therapies, strong clinical research activity, and a high concentration of specialized treatment centers

- Patients and healthcare providers in the region benefit from widespread availability of specialized hematology centers, advanced laboratory testing, and access to innovative therapies such as biologics and complement inhibitors

- This widespread adoption is further supported by high healthcare expenditure, active clinical research, favorable reimbursement policies, and the presence of key pharmaceutical companies, establishing North America as a leading market for cold agglutinin disease management

U.S. Cold Agglutinin Disease Market Insight

The U.S. dominated the North America cold agglutinin disease market with a significant share in 2025, driven by advanced healthcare infrastructure, high awareness of rare hematologic disorders, and early adoption of innovative therapies. The presence of leading pharmaceutical and biotechnology companies supports strong clinical research and rapid commercialization of novel treatments. Patients in the U.S. benefit from access to specialized hematology centers, advanced diagnostic tools, and well-established treatment protocols. Favorable reimbursement policies and high healthcare spending further enable adoption of biologics and complement inhibitors. Additionally, ongoing clinical trials and regulatory approvals are accelerating the availability of targeted therapies, strengthening the overall market growth.

Europe Cold Agglutinin Disease Market Insight

Europe cold agglutinin disease market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing disease awareness, supportive healthcare systems, and rising investments in rare disease management. The region has a well-established regulatory framework that encourages orphan drug development and approvals. Growing participation in clinical trials and rare disease registries is improving patient identification and treatment outcomes. Additionally, expanding access to advanced therapies across major countries is supporting market penetration. Increasing collaboration between academic institutions and pharmaceutical companies is further contributing to research and innovation in CAD treatments.

U.K. Cold Agglutinin Disease Market Insight

U.K. cold agglutinin disease market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong public healthcare infrastructure, rising awareness of rare diseases, and increasing adoption of advanced therapeutic options. The National Health Service (NHS) plays a key role in facilitating diagnosis and treatment access for patients. Growing emphasis on early diagnosis and specialized care pathways is improving patient outcomes. Additionally, the presence of clinical research initiatives and participation in global trials is supporting innovation in treatment approaches. The availability of specialized hematology services further strengthens the market in the country.

Germany Cold Agglutinin Disease Market Insight

Germany cold agglutinin disease market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, strong emphasis on medical research, and high adoption of innovative therapies. The country’s focus on precision medicine and rare disease treatment supports the uptake of biologics and complement inhibitors. Germany’s well-developed hospital network and specialized treatment centers enable efficient disease management. Additionally, increasing awareness among healthcare professionals is leading to improved diagnosis rates. The integration of advanced diagnostic technologies with treatment protocols is further enhancing patient care and market growth.

Asia-Pacific Cold Agglutinin Disease Market Insight

Asia-Pacific cold agglutinin disease market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by improving healthcare infrastructure, rising awareness of rare diseases, and increasing access to advanced diagnostic tools. Countries such as China, Japan, and India are witnessing growing investments in healthcare and expanding adoption of modern treatment options. The region’s large patient pool and improving diagnosis rates are contributing to market expansion. Government initiatives promoting healthcare modernization and rare disease management are further supporting growth. Additionally, the increasing presence of global pharmaceutical companies in the region is enhancing availability of therapies.

Japan Cold Agglutinin Disease Market Insight

Japan cold agglutinin disease market is gaining momentum due to its advanced healthcare system, aging population, and strong focus on precision medicine and early diagnosis. The country’s well-established medical infrastructure supports efficient disease detection and management. High awareness of rare diseases among healthcare professionals is contributing to better treatment outcomes. The integration of biologics and complement inhibitors into clinical practice is increasing steadily. Additionally, Japan’s emphasis on research and innovation is driving the development and adoption of novel therapies for CAD.

India Cold Agglutinin Disease Market Insight

India cold agglutinin disease market accounted for a significant share in Asia Pacific in 2025, attributed to improving healthcare access, rising awareness of rare diseases, and increasing availability of diagnostic facilities. The country’s expanding middle-class population and growing healthcare expenditure are supporting adoption of advanced therapies. Government initiatives aimed at strengthening healthcare infrastructure and promoting rare disease awareness are contributing to market growth. Increasing presence of specialty clinics and tertiary care hospitals is improving diagnosis and treatment access. Additionally, the availability of cost-effective treatment options is encouraging wider adoption across both urban and semi-urban regions.

Cold Agglutinin Disease Market Share

The Cold Agglutinin Disease industry is primarily led by well-established companies, including:

- Sanofi (France)

- Novartis AG (Switzerland)

- AstraZeneca (U.K.)

- Alexion Pharmaceuticals (U.S.)

- Apellis Pharmaceuticals (U.S.)

- BioCryst Pharmaceuticals (U.S.)

- UCB Pharma (Belgium)

- Pfizer Inc. (U.S.)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Sun Pharmaceutical Industries Ltd. (India)

- Amgen Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Merck KGaA (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Zydus Lifesciences Ltd. (India)

- Incyte Corporation (U.S.)

What are the Recent Developments in Global Cold Agglutinin Disease Market?

- In November 2025, Recordati Rare Diseases announced that it will share new data on cold agglutinin disease at the American Society of Hematology (ASH) Annual Meeting, highlighting advances in research and understanding of CAD and related hematologic conditions, further supporting clinical knowledge and treatment strategies in the disease space

- In January 2025, research published in Blood showed that pegcetacoplan demonstrated safety and potential effectiveness for treating cold agglutinin disease, suggesting it may serve as a treatment option in CAD

- In March 2024, developers Apellis and Sobi halted the clinical development of pegcetacoplan for CAD, discontinuing its Phase 3 trial due to strategic reprioritization in light of recent therapeutic advances in the space

- In January 2023, the U.S. Food and Drug Administration approved an expanded label for Enjaymo® (sutimlimab-jome) to include long-term safety and efficacy data for people with cold agglutinin disease, enabling its use in patients with or without a history of blood transfusions

- In February 2022, the U.S. FDA granted full approval for Enjaymo (sutimlimab-jome) infusion as the first and only approved treatment to decrease the need for red blood cell transfusion due to hemolysis in adults with cold agglutinin disease

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.