Global Combination Antibody Therapy Market

Market Size in USD Billion

USD

241.50 Billion

USD

567.06 Billion

2025

2033

USD

241.50 Billion

USD

567.06 Billion

2025

2033

| 2026 - 2033 | |

| USD 241.50 Billion | |

| USD 567.06 Billion | |

| % | |

|

Combination Antibody Therapy Market Overview

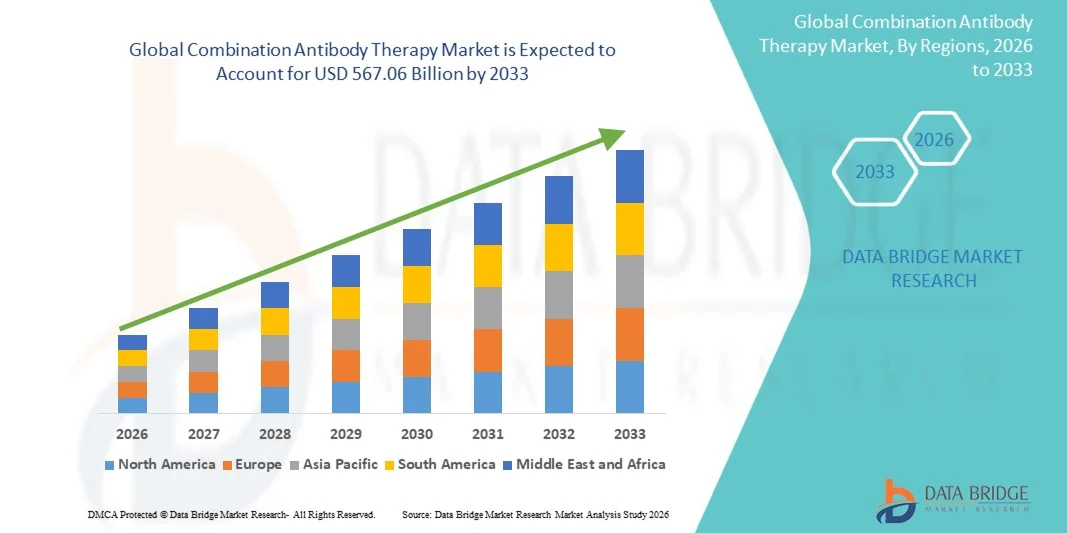

The Combination Antibody Therapy Market was valued at USD 241.50 billion in 2025 and is projected to reach USD 567.06 billion by 2033, growing at a CAGR of 11.26% from 2026 to 2033. The Combination Antibody Therapy market is experiencing strong growth driven by rising prevalence of cancer, autoimmune disorders, and infectious diseases, along with increasing demand for highly targeted and effective biologic treatment approaches. Continuous advancements in monoclonal antibody engineering, bispecific and multispecific antibody platforms, and immune checkpoint inhibition therapies are significantly expanding clinical applications across oncology and immunology. Pharmaceutical companies are increasingly focusing on combination antibody therapies to improve treatment efficacy, overcome drug resistance, and enhance patient survival outcomes across complex disease indications.

The growing burden of cancer worldwide, coupled with the shift toward precision medicine and personalized healthcare, is compelling healthcare providers, research institutions, and pharmaceutical companies to adopt advanced antibody-based combination treatment strategies. Combination therapies that integrate multiple antibodies or antibodies with chemotherapy, targeted therapy, or immunotherapy are increasingly being used to achieve synergistic therapeutic effects and reduce tumor resistance. Rising regulatory approvals for novel biologics, along with expanding clinical trial activity in North America, Europe, and Asia-Pacific, are further accelerating market adoption. In addition, increasing investments in biopharmaceutical R&D and the rapid expansion of oncology pipelines are strengthening the transition from single-agent therapies to advanced combination antibody regimens across global healthcare systems.

Key Market Trends & Insights

- North America dominated the Combination Antibody Therapy Market with the largest revenue share of 38.62% in 2025, supported by advanced biologics manufacturing infrastructure, strong presence of key biopharmaceutical players, and increasing adoption of combination immunotherapy in oncology and infectious disease treatment. The region also benefits from robust clinical research activity, favorable regulatory pathways for monoclonal and bispecific antibody approvals, and strong investment in precision medicine and targeted biologics development across the U.S. and Canada. Rising prevalence of cancer and HIV, along with expanding access to advanced immunotherapy in specialty care settings, continues to strengthen North America’s leadership position in the global market.

- The Bispecific Antibodies segment led the market with a 42.15% share in 2025, driven by increasing clinical success in oncology applications, particularly in hematologic cancers such as leukemia and lymphoma. These therapies enable dual antigen targeting, improving immune response and treatment efficacy compared to conventional monoclonal antibodies. Rapid pipeline expansion, multiple regulatory approvals between 2022–2025, and increasing adoption in combination regimens with checkpoint inhibitors are further supporting segment dominance.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rising healthcare expenditure, expanding biologics manufacturing capabilities, increasing cancer and infectious disease burden, and growing adoption of advanced immunotherapy treatments in China, India, and Japan. The region is also witnessing rapid expansion of clinical research infrastructure, improving access to monoclonal and bispecific antibody therapies, and increasing investments from global pharmaceutical companies in emerging Asian markets.

- The Antibody-Drug Conjugates segment is expected to witness the fastest growth at a CAGR of 9.2% from 2026 to 2033, fueled by rising demand for highly targeted cancer therapies that combine cytotoxic agents with monoclonal antibodies. These therapies are gaining strong traction in solid tumors such as breast, lung, and ovarian cancers due to improved precision and reduced systemic toxicity. Advancements in linker technology, payload engineering, and increasing clinical trial success rates during 2023–2025 are accelerating segment expansion globally.

- The Cancer segment dominated the market with a 61.48% share in 2025, driven by the rising global burden of oncology cases and increasing adoption of combination antibody-based immunotherapies. These therapies are widely used to improve survival outcomes, overcome tumor resistance, and enhance immune system activation. Growing use of bispecific antibodies and checkpoint inhibitor combinations across hospitals and specialty oncology centers is further strengthening segment dominance.

- The HIV segment is expected to witness the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by increasing research into broadly neutralizing antibodies and long-acting combination biologic therapies. These approaches aim to improve viral suppression, enhance treatment adherence, and support functional cure strategies. Rising clinical trials and funding support from global health organizations during 2023–2025 are further accelerating segment growth.

- The Parenteral route of administration dominated the market with a 88.73% share in 2025, due to the biologic nature of antibody therapies requiring intravenous or subcutaneous delivery for optimal therapeutic effectiveness. Hospitals and specialty centers widely prefer parenteral administration for controlled dosing, rapid action, and management of immune-related adverse events. Growing development of subcutaneous formulations is further enhancing patient convenience while maintaining segment dominance.

- The Hospitals segment dominated the market with a 54.26% share in 2025, supported by high patient inflow for oncology and infectious disease treatment, availability of advanced infusion infrastructure, and presence of specialized oncology care units. Hospitals remain the primary setting for administration of combination antibody therapies due to the need for clinical monitoring and complex treatment protocols. Increasing adoption of biomarker-guided therapy selection is further reinforcing segment leadership.

- The Hospital Pharmacy segment dominated the distribution channel with a 57.13% share in 2025, driven by centralized procurement systems, stringent cold-chain requirements, and high-cost biologics handling needs. Hospital pharmacies ensure proper storage, dispensing, and compliance with treatment guidelines for antibody therapies. Growing integration of specialty pharmacy services within hospital networks is further strengthening segment dominance.

- The Parenteral segment dominated the market in 2025 with a 91.26% share, driven by widespread use of intravenous and subcutaneous administration for antibody therapies ensuring high bioavailability and rapid therapeutic response

Market Size & Forecast

- Global Market Value (2025): USD 241.50 Billion

- Expected Market Value (2033): USD 567.06 Billion

- Forecast CAGR (2026–2033): 11.26%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Combination Antibody Therapy Market Segmentation

|

Attributes |

Combination Antibody Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Roche Holding AG (Switzerland) |

|

Market Opportunities |

· Expansion of Bispecific and Next-Generation Antibody Platforms · Growing Adoption of Combination Immunotherapy in Emerging Markets · Integration of Precision Medicine and Biomarker-Guided Therapy Selection |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Combination Antibody Therapy Market Trends

Trend: Growth in Precision Oncology and Combination Immunotherapy Adoption

The Combination Antibody Therapy Market is witnessing strong growth driven by the increasing adoption of multi-mechanism immunotherapy approaches in oncology treatment. Combination antibody therapies, including bispecific antibodies and antibody-drug conjugates, are increasingly being used to enhance tumor targeting, overcome drug resistance, and improve patient survival outcomes across cancers such as breast cancer, lung cancer, and hematologic malignancies. For instance, between 2023 and 2025, several oncology centers across the U.S., Germany, and China expanded use of combination checkpoint inhibitor and monoclonal antibody regimens to improve response rates in advanced-stage cancer patients. In addition, rising clinical trial activity for next-generation bispecific antibodies and ADC-based combination regimens is accelerating innovation in targeted cancer therapy globally.

Combination Antibody Therapy Market Dynamics

Key Market Driver: Rising Demand for Targeted and Personalized Cancer Treatment

The increasing prevalence of cancer globally and the growing shift toward precision medicine are major drivers of the Combination Antibody Therapy Market. Combination antibody therapies are widely adopted due to their ability to target multiple disease pathways simultaneously, improving efficacy in patients who do not respond to single-agent treatments. For example, between 2022 and 2025, multiple FDA and EMA approvals for combination regimens involving bispecific antibodies and checkpoint inhibitors significantly expanded treatment options for hematologic and solid tumors. Pharmaceutical companies are also investing heavily in next-generation immunotherapies to improve survival outcomes and reduce relapse rates, particularly in aggressive cancers such as non-small cell lung cancer and diffuse large B-cell lymphoma.

Key Restraint/Challenge: High Cost of Biologic Therapies and Complex Clinical Development Pathways

A significant challenge in the Combination Antibody Therapy Market is the high cost associated with biologic drug development, manufacturing, and treatment administration. Combination antibody regimens often require complex clinical trials, high R&D investment, and advanced biomanufacturing capabilities, leading to elevated treatment costs for patients and healthcare systems. In addition, regulatory approval processes for combination biologics are highly complex due to safety concerns, immunogenicity risks, and long-term efficacy evaluation requirements. For instance, between 2022 and 2024, several late-stage combination immunotherapy candidates faced delays in approval due to toxicity management concerns and inconsistent response rates across patient populations, limiting faster commercialization.

Key Market Opportunity: Expansion of AI-Driven Drug Discovery and Next-Generation Immunotherapy Platforms

The integration of artificial intelligence, computational biology, and high-throughput screening technologies presents a significant opportunity in the Combination Antibody Therapy market. AI-enabled drug discovery platforms are increasingly being used to design novel bispecific antibodies, optimize antigen binding affinity, and predict combination therapy response in cancer patients. For example, during 2024–2025, several biopharmaceutical companies in the U.S. and Europe adopted AI-driven protein modeling platforms to accelerate development of next-generation antibody combinations. In addition, advancements in personalized oncology, biomarker-driven treatment selection, and precision immunotherapy are expanding the application of combination antibody therapies across both developed and emerging healthcare markets.

Combination Antibody Therapy Market Scope

The Combination Antibody Therapy market is segmented on the basis of type, indication, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Combination Antibody Therapy Market is segmented into antibody/antibody combinations, antibody-drug conjugates, bispecific antibodies, chemotherapy-monoclonal antibodies, and others. The Bispecific Antibodies segment dominated the market in 2025 with a 38.62% share, driven by its strong dual-antigen targeting capability, improved therapeutic precision, and superior clinical efficacy in oncology and immune disorders. Rising adoption in cancer immunotherapy, increasing regulatory approvals, and strong late-stage pipeline development are further strengthening its dominance. Continuous R&D investments by leading pharmaceutical and biotechnology companies are accelerating innovation in bispecific platforms, making them a preferred choice for next-generation antibody therapies. In addition, growing demand for highly targeted and personalized treatment approaches is reinforcing market leadership of this segment.

The Antibody-Drug Conjugates segment is expected to witness the fastest growth with a CAGR of 9.1% from 2026 to 2033, driven by increasing demand for targeted oncology therapies with reduced systemic toxicity. Advancements in linker chemistry, payload design, and antibody engineering are improving drug stability and therapeutic effectiveness. Expanding clinical trials across multiple cancer indications and rising combination use with immunotherapy agents are accelerating adoption. In addition, strong pipeline expansion by biotech companies and increasing regulatory approvals are supporting rapid global growth.

- By Indication

On the basis of indication, the market is segmented into cancer, HIV, and others. The Cancer segment dominated the market in 2025 with a 72.45% share, driven by the rising global cancer burden, increasing use of antibody-based immunotherapy combinations, and strong clinical success of monoclonal antibody therapies. Expanding oncology drug pipelines, growing adoption of precision medicine, and rising approvals for combination regimens are further strengthening segment dominance. Hospitals and research institutions are increasingly integrating antibody-based therapies to improve treatment outcomes. Continuous advancements in oncology biologics are also supporting strong market leadership.

The HIV segment is expected to witness the fastest growth with a CAGR of 7.8% from 2026 to 2033, driven by increasing research into long-acting antibody therapies and broadly neutralizing antibodies. Growing demand for alternatives to conventional antiretroviral therapy and increasing focus on functional cure development are accelerating growth. Rising funding from global health organizations and strong clinical trial activity are further supporting innovation. Expanding pipeline developments in immune-based HIV treatment strategies are boosting adoption globally.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The Parenteral segment dominated the market in 2025 with a 91.26% share, driven by widespread use of intravenous and subcutaneous administration for antibody therapies ensuring high bioavailability and rapid therapeutic response. Strong hospital infrastructure, established clinical protocols, and physician preference for injectable biologics further support dominance. Most approved antibody-based therapies currently rely on parenteral delivery, reinforcing its leading position in clinical practice. In addition, controlled dosing and better treatment monitoring contribute to its widespread adoption.

The Oral segment is expected to witness the fastest growth with a CAGR of 8.2% from 2026 to 2033, driven by advancements in oral biologics delivery technologies and improved formulation stability. Increasing patient preference for non-invasive treatment options is supporting demand. Innovations in nanoparticle delivery systems and encapsulation technologies are enabling oral administration of complex biologics. Growing R&D investments in oral antibody development are further accelerating market expansion.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, speciality centres, and others. The Hospitals segment dominated the market in 2025 with a 63.18% share, driven by high patient inflow, strong adoption of antibody-based therapies in oncology and infectious diseases, and availability of advanced infusion infrastructure. Hospitals also conduct major clinical trials and provide controlled administration of biologics under expert supervision. Increasing demand for specialized cancer treatment and centralized healthcare delivery systems further support dominance. Strong integration of antibody therapies in hospital treatment protocols reinforces market leadership.

The Homecare segment is expected to witness the fastest growth with a CAGR of 8.5% from 2026 to 2033, driven by increasing demand for patient-centric care and convenience-based treatment models. Rising adoption of self-administered subcutaneous therapies is supporting this shift. Expansion of home infusion services and remote patient monitoring technologies is improving accessibility. In addition, cost reduction benefits and improved treatment compliance are accelerating adoption in homecare settings.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The Hospital Pharmacy segment dominated the market in 2025 with a 68.74% share, driven by centralized procurement of high-cost biologics and strict hospital-based distribution systems ensuring controlled and safe administration. Strong integration with hospital treatment pathways and regulatory compliance requirements further reinforce dominance. Hospitals remain the primary point of biologics administration, supporting steady demand. In addition, established procurement networks strengthen this segment’s market position.

The Online Pharmacy segment is expected to witness the fastest growth with a CAGR of 9.3% from 2026 to 2033, driven by rapid digital healthcare adoption and expanding e-pharmacy platforms. Increasing demand for home delivery of biologics and improved cold-chain logistics are supporting growth. Integration of telemedicine with online pharmacies is enhancing accessibility and patient convenience. Rising digital transformation in healthcare systems is further accelerating market expansion.

Combination Antibody Therapy Market Regional Analysis

North America dominated the Combination Antibody Therapy market and accounted for the largest revenue share of 38.62% in 2025, supported by advanced biologics manufacturing infrastructure, strong presence of key biopharmaceutical players, and increasing adoption of combination immunotherapy in oncology and infectious disease treatment. The region also benefits from robust clinical research activity, favorable regulatory pathways for monoclonal and bispecific antibody approvals, and strong investment in precision medicine and targeted biologics development across the U.S. and Canada. Rising prevalence of cancer and HIV, along with expanding access to advanced immunotherapy in specialty care settings, continues to strengthen North America’s leadership position in the global market.

U.S. Combination Antibody Therapy Market Insight

The U.S. Combination Antibody Therapy market is witnessing strong growth due to rising investment in advanced biologics research, expanding oncology treatment programs, and increasing adoption of combination immunotherapy for cancer and infectious diseases. The country’s well-established biopharmaceutical ecosystem, presence of leading global drug developers, and strong clinical trial activity are driving rapid innovation in monoclonal, bispecific antibodies, and antibody-drug conjugate combinations. In addition, favorable FDA approval pathways and growing focus on precision medicine are accelerating commercialization of next-generation antibody therapies across hospitals, specialty centers, and research institutions.

Europe Combination Antibody Therapy Market Insight

The Europe Combination Antibody Therapy market remains a major contributor to global revenue, driven by strong government support for biologics innovation, expanding cancer treatment programs, and increasing adoption of advanced immunotherapy solutions. The region benefits from a highly developed pharmaceutical manufacturing base and strong academic–industry collaboration in antibody research. Widespread use of combination therapies in oncology and infectious disease treatment is supporting market expansion across major economies such as Germany, France, and the U.K. Increasing investments in precision medicine and growing regulatory alignment for biologics approvals continue to strengthen regional growth.

U.K. Combination Antibody Therapy Market Insight

The U.K. Combination Antibody Therapy market is experiencing steady growth, supported by rising investment in biopharmaceutical research, increasing clinical trials for monoclonal and bispecific antibodies, and strong adoption of immunotherapy in oncology care. The presence of leading research universities and biotech firms is accelerating innovation in combination biologic therapies. Additionally, the National Health Service (NHS) focus on expanding access to advanced cancer treatments and personalized medicine is contributing to increased uptake of antibody-based therapies across specialty care settings.

Germany Combination Antibody Therapy Market Insight

The Germany Combination Antibody Therapy market is expanding steadily due to the country’s strong pharmaceutical manufacturing base, advanced clinical research infrastructure, and increasing focus on oncology and immunology therapeutics. German biotech and pharma companies are actively investing in next-generation antibody-drug conjugates and bispecific antibody platforms. High prevalence of cancer and strong healthcare reimbursement systems are further supporting adoption of combination immunotherapy across hospitals and specialty centers. Continuous innovation in biologics production and precision medicine is strengthening Germany’s position in the European market.

Asia-Pacific Combination Antibody Therapy Market Insight

The Asia-Pacific Combination Antibody Therapy market is expected to witness rapid growth, driven by rising healthcare expenditure, expanding biologics manufacturing capabilities, increasing burden of cancer and infectious diseases, and growing adoption of advanced immunotherapy treatments in emerging economies. Countries such as China, India, and Japan are significantly investing in biotechnology infrastructure and clinical research capacity. The region is also benefiting from increasing participation of global pharmaceutical companies in local manufacturing and clinical trials, improving access to monoclonal and bispecific antibody therapies across hospitals and specialty care centers.

Japan Combination Antibody Therapy Market Insight

The Japan Combination Antibody Therapy market is witnessing consistent growth due to strong focus on biotechnology innovation, rising cancer treatment demand, and increasing adoption of advanced immunotherapy approaches. Japanese pharmaceutical companies are actively involved in developing next-generation monoclonal and bispecific antibody combinations. The country’s aging population and high prevalence of chronic diseases are further driving demand for targeted biologic therapies. Strong regulatory support for innovative drug approvals is also supporting faster market adoption.

China Combination Antibody Therapy Market Insight

The China Combination Antibody Therapy market is growing rapidly, driven by rising cancer incidence, expanding biologics manufacturing capacity, and strong government support for biotechnology innovation. Increasing investments in domestic biopharma companies and rising participation in global clinical trials are accelerating development of combination antibody therapies. China is also witnessing growing adoption of monoclonal and bispecific antibody treatments in oncology and infectious diseases, supported by improving healthcare infrastructure and expanding access to advanced immunotherapy across hospitals and specialty centers.

Combination Antibody Therapy Market Share

The Combination Antibody Therapy industry is primarily led by well-established companies, including:

- Roche Holding AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- AstraZeneca plc (U.K.)

- Johnson & Johnson (U.S.)

- Amgen Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Sanofi S.A. (France)

- Genentech, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- BeiGene Ltd. (China)

- Innovent Biologics, Inc. (China)

- Zymeworks Inc. (Canada)

- Seagen Inc. (U.S.)

- MorphoSys AG (Germany)

- ImmunoGen Inc. (U.S.)

- MacroGenics, Inc. (U.S.)

- Sutro Biopharma, Inc. (U.S.)

- Xencor, Inc. (U.S.)

- IGM Biosciences, Inc. (U.S.)

- Akeso, Inc. (China)

- BeiGene (BeOne Medicines) (China)

- CureVac N.V. (Germany)

- BioNTech SE (Germany)

- GSK plc (U.K.)

- Takeda Pharmaceutical Company Limited (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Eisai Co., Ltd. (Japan)

- CSL Limited (Australia)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Amgen Research Munich GmbH (Germany)

Latest Developments in Combination Antibody Therapy Market

- In February 2021, Eli Lilly and Company received Emergency Use Authorization (EUA) from the U.S. FDA for its combination monoclonal antibody therapy bamlanivimab and etesevimab for the treatment of mild to moderate COVID-19 in high-risk patients. The combination demonstrated a significant reduction in hospitalization and death risk compared to placebo, marking one of the earliest large-scale antibody combination deployments during the pandemic and accelerating global adoption of antibody-based combination therapies

- In June 2021, the U.S. FDA authorized Regeneron’s antibody combination casirivimab and imdevimab (REGEN-COV) for the treatment and prevention of COVID-19 in high-risk individuals. Clinical studies showed strong efficacy in reducing viral load and preventing disease progression, reinforcing the role of dual-antibody cocktails as a rapid-response therapeutic strategy during infectious disease outbreaks

- In May 2021, the U.S. FDA approved Janssen Pharmaceutical Companies’ bispecific antibody amivantamab (Rybrevant) for the treatment of non-small cell lung cancer (NSCLC) with EGFR exon 20 insertion mutations. The therapy represents a next-generation bispecific antibody targeting both EGFR and MET pathways, expanding precision oncology treatment options for resistant lung cancer cases

- In March 2022, the U.S. FDA approved Opdualag, a combination of nivolumab and relatlimab, marking the first LAG-3 and PD-1 dual antibody combination therapy for unresectable or metastatic melanoma. This approval introduced a new checkpoint inhibitor combination approach, significantly advancing immuno-oncology treatment strategies

- In February 2023, the U.S. FDA granted full approval to sacituzumab govitecan-based antibody-drug conjugate combination therapy for hormone receptor-positive, HER2-negative metastatic breast cancer. This milestone expanded the clinical use of ADC-based combination therapies beyond late-line treatment into earlier therapeutic settings, strengthening oncology pipeline growth

- In August 2023, the U.S. FDA approved talquetamab (Talvey), a bispecific antibody targeting GPRC5D and CD3 for relapsed or refractory multiple myeloma. This approval highlighted the growing role of T-cell redirecting bispecific antibodies in hematologic cancers and strengthened the commercialization of novel immune-engaging antibody combinations

- In September 2023, clinical advancements in anti-LAG-3 combination therapies such as favezelimab plus pembrolizumab showed promising results in relapsed Hodgkin lymphoma and solid tumors. These developments demonstrated expanding clinical pipelines for dual immune checkpoint antibody combinations targeting PD-1/LAG-3 pathways

- In April 2025, the UK Medicines and Healthcare products Regulatory Agency (MHRA) approved combination therapies involving GSK’s Blenrep (belantamab mafodotin), an antibody-drug conjugate used with bortezomib and dexamethasone for relapsed multiple myeloma. Clinical evidence showed improved survival outcomes compared to standard therapies, strengthening the role of ADC-based combinations in hematologic malignancies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.